Gold prices slide further as easing US-China tensions curb haven demand

Introduction & Market Context

Antero Resources Corp (NYSE:AR) released its 2025 guidance presentation on May 1, 2025, outlining production targets, capital expenditure plans, and hedging strategies for the coming year. The presentation comes after a strong Q4 2024 performance where the company reported earnings per share of $0.48, significantly exceeding analyst expectations of $0.31, despite a slight revenue miss.

The natural gas producer’s stock has delivered an impressive 87.5% return over the past year, though it recently experienced a 3.73% decline in the latest trading session, closing at $34.83. The company’s forward-looking guidance focuses on maintaining stable production while dramatically increasing free cash flow generation.

2025 Production and Financial Guidance

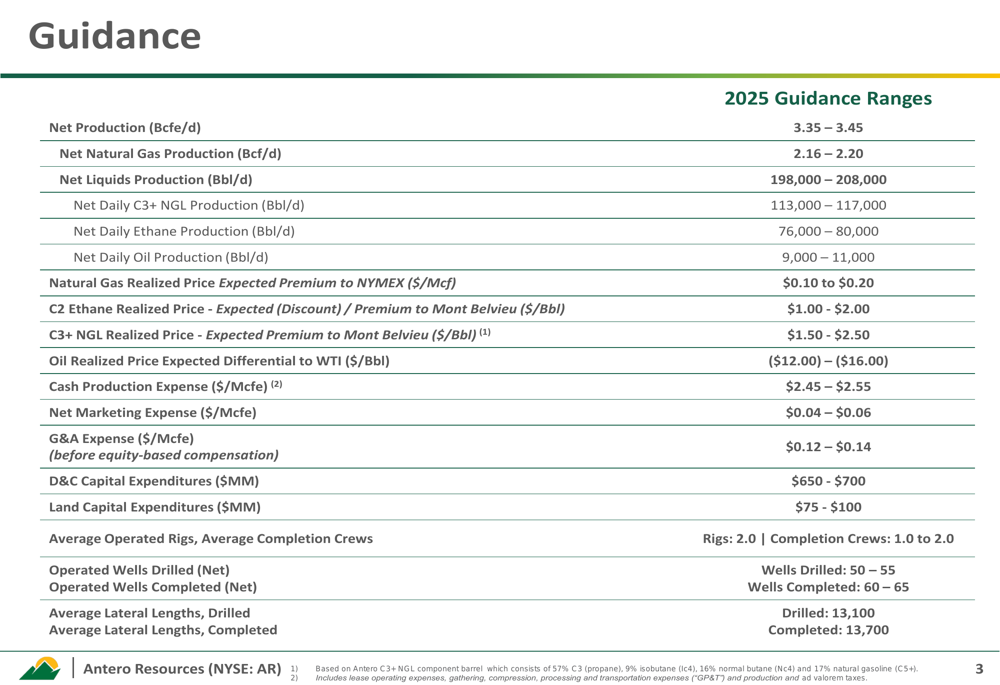

Antero Resources has outlined comprehensive operational and financial targets for 2025, maintaining production levels near current rates while focusing on efficiency improvements. The company projects net production between 3.35-3.45 Bcfe/d, with natural gas comprising approximately 2.16-2.20 Bcf/d of the total.

As shown in the detailed guidance table below, Antero plans to maintain a lean operational structure with just two drilling rigs and 1-2 completion crews, consistent with its current operations:

The company’s capital discipline is evident in its projected drilling and completion (D&C) expenditures of $650-700 million and land capital expenditures of $75-100 million. This controlled spending approach aligns with management’s recent statements about prioritizing free cash flow generation over production growth.

During the recent earnings call, CEO Paul Rady characterized 2024 as "a remarkable year" for operational efficiency, which has positioned the company for its projected step change in free cash flow for 2025. The guidance indicates Antero will complete slightly more wells (60-65) than it drills (50-55) in 2025, suggesting the company is working through its inventory of drilled but uncompleted wells.

Hedging Strategy and Risk Management

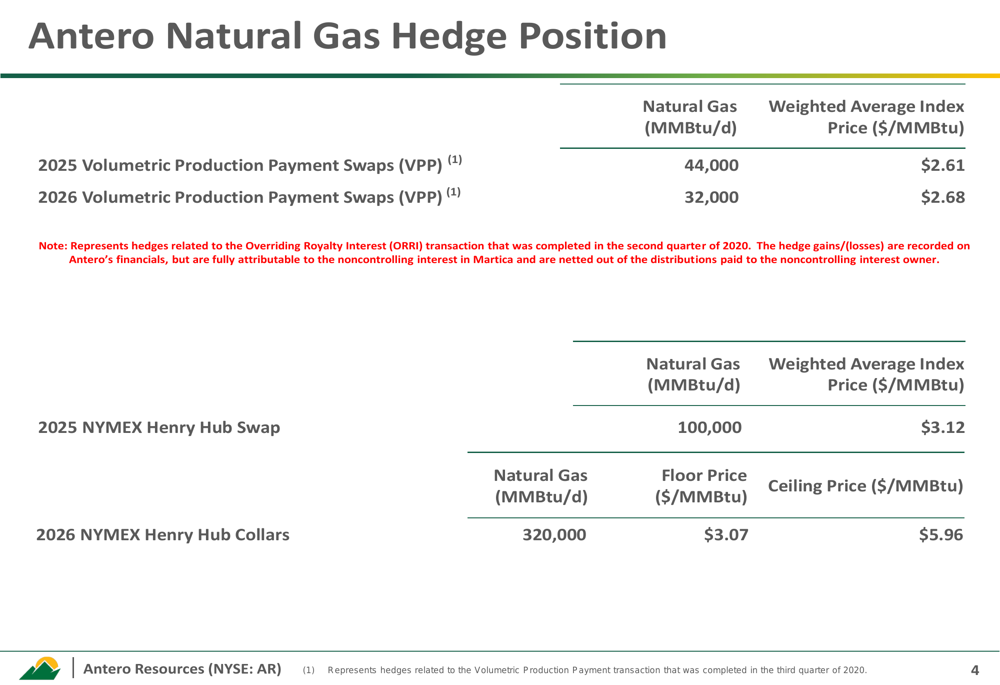

A key component of Antero’s 2025 strategy is its comprehensive hedging program designed to mitigate natural gas price volatility. The company has implemented a multi-year approach with a combination of swaps and collars extending through 2026.

The following table details Antero’s natural gas hedge positions, which include both Volumetric Production Payment (VPP) swaps and NYMEX Henry Hub instruments:

Notably, for 2026, Antero has secured collars on 320,000 MMBtu/d with a floor price of $3.07/MMBtu and a ceiling of $5.96/MMBtu, providing significant downside protection while allowing for upside participation if natural gas prices strengthen. This approach reflects management’s cautious outlook on natural gas prices while positioning the company to benefit from potential market improvements as new LNG export facilities come online.

The hedging strategy complements the company’s operational focus, creating a more predictable cash flow stream that supports debt reduction goals and potential shareholder returns.

Financial Outlook and Strategic Priorities

Antero Resources projects a dramatic increase in free cash flow for 2025, forecasting over $1.6 billion compared to just $73 million in 2024. This 21-fold increase represents a significant inflection point for the company’s financial trajectory and forms the foundation of its capital allocation strategy.

Management has indicated plans to allocate approximately $500 million toward debt reduction in 2025, strengthening the company’s balance sheet. The substantial remaining free cash flow could potentially support shareholder returns through dividends or share repurchases, though specific plans were not detailed in the presentation.

CFO Michael Kennedy emphasized during the recent earnings call that "2025 [will] deliver a substantial year-over-year step change in free cash flow," underscoring the company’s financial strength and strategic focus on capital efficiency rather than production growth.

The company’s guidance also reflects its expectation of premium pricing for its production, with natural gas realized prices projected at $0.10-$0.20/Mcf above NYMEX benchmarks and C3+ NGL realized prices at $1.50-$2.50/Bbl premium to Mont Belvieu.

Market Reaction and Analyst Perspectives

Investor reaction to Antero’s recent performance and forward guidance has been generally positive, with the stock trading near its 52-week high of $42.63. Following the Q4 earnings release, the stock saw a modest 0.46% increase in after-hours trading, reflecting confidence in the company’s operational efficiency and future cash flow projections.

According to recent analyst data, seven analysts have revised their earnings expectations upward for the upcoming period, suggesting continued optimism about the company’s prospects. However, some analysts have expressed concerns about the flat production guidance, which may not appeal to growth-focused investors.

The company faces several challenges, including the potential impact of steel tariffs (estimated between $5-10 million) and ongoing volatility in natural gas prices. Despite these headwinds, Antero’s substantial hedging program and focus on operational efficiency position it well to deliver on its 2025 financial targets.

As natural gas demand continues to grow with expanding LNG export capacity, Antero’s strategic positioning in the Marcellus Shale with its long-term inventory provides a solid foundation for sustainable operations beyond the 2025 guidance period.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.