Trump/Putin summit, UnitedHealth and Japan’s GDP - what’s moving markets

Apogee Enterprises (NASDAQ:APOG) shares jumped 6.25% in premarket trading after the architectural products company reported first-quarter fiscal 2026 results that exceeded management expectations despite significant profitability challenges. The company raised its full-year outlook for both revenue and earnings per share, signaling confidence in its ability to navigate current headwinds.

Quarterly Performance Highlights

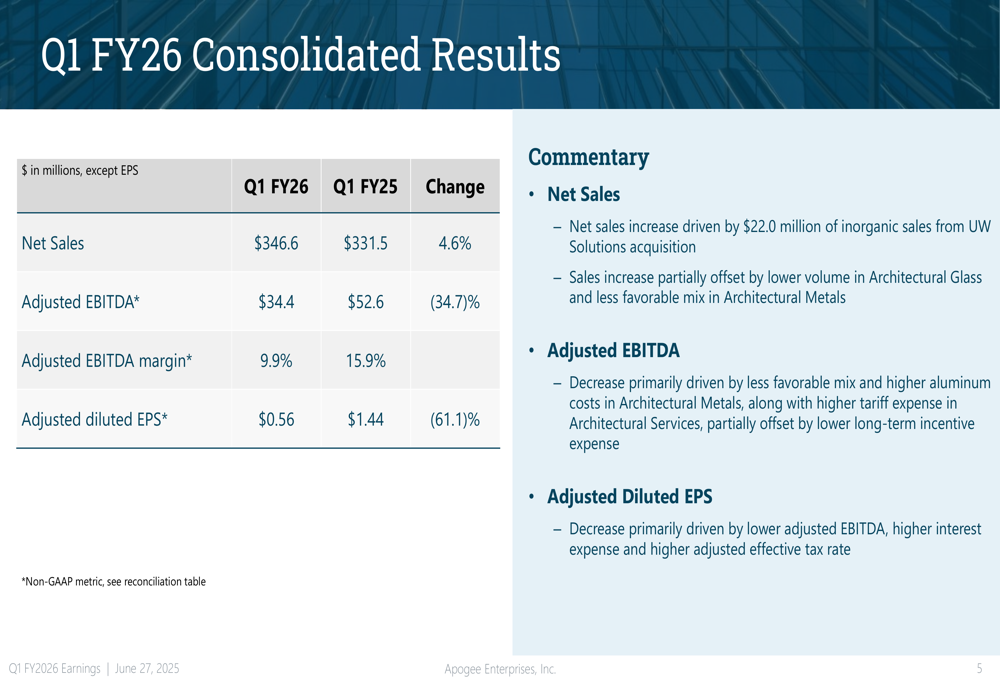

Apogee reported net sales of $346.6 million for Q1 FY26, representing a 4.6% increase compared to the same period last year. However, profitability metrics declined significantly year-over-year, with adjusted EBITDA falling 34.7% to $34.4 million and adjusted EBITDA margin contracting 600 basis points to 9.9%. Adjusted diluted earnings per share dropped 61.1% to $0.56 from $1.44 in the prior-year quarter.

As shown in the following consolidated results:

The sales increase was primarily driven by $22.0 million of inorganic revenue from the UW Solutions acquisition, partially offset by lower volume in Architectural Glass and less favorable mix in Architectural Metals. The significant decrease in profitability was attributed to less favorable mix and higher aluminum costs in Architectural Metals, along with higher tariff expenses in Architectural Services.

Segment Analysis

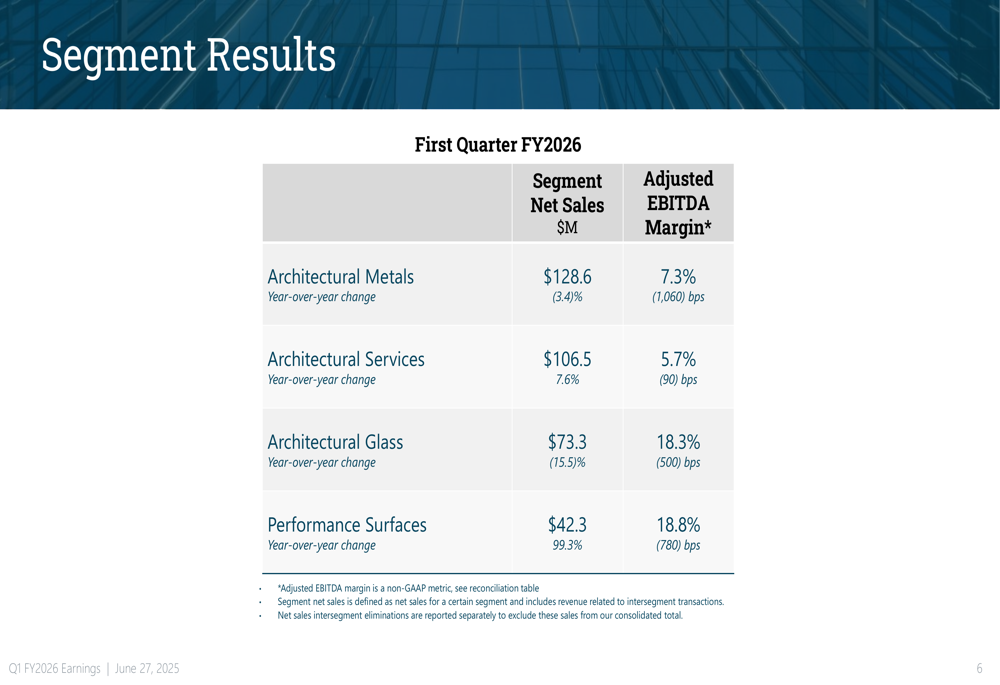

Performance varied significantly across Apogee’s business segments in the first quarter. The Performance Surfaces segment was the standout performer with 99.3% sales growth, while Architectural Glass struggled with a 15.5% decline. Architectural Services delivered its fifth consecutive quarter of sales growth, and Architectural Metals showed sequential improvement in revenue and adjusted EBITDA.

The segment breakdown reveals the divergent performance:

The Performance Surfaces segment, which includes the recently acquired UW Solutions business, maintained strong margins of 18.8% despite a 780 basis point year-over-year decline. Architectural Glass, despite its sales decline, delivered the second-highest margin at 18.3%, though this represented a 500 basis point contraction from the prior year.

Tariff Impact and Mitigation

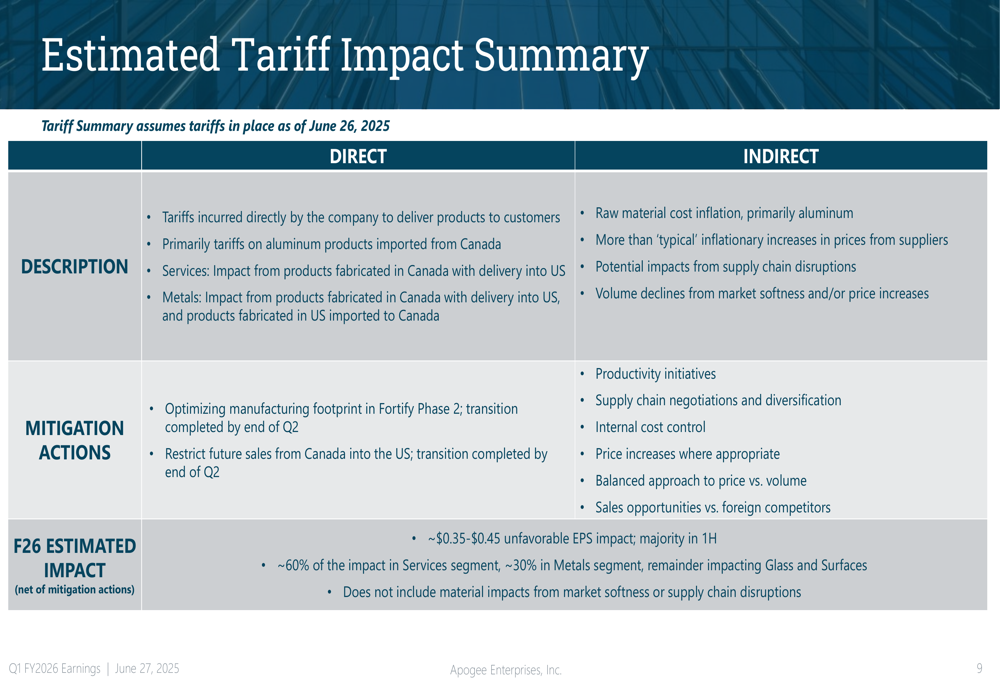

A significant factor affecting Apogee’s first-quarter performance was the impact of tariffs, which the company estimates will create a $0.35-$0.45 unfavorable EPS impact for fiscal 2026, with the majority of this impact concentrated in the first half of the year.

The company provided a detailed breakdown of both direct and indirect tariff impacts, along with mitigation strategies:

Management is implementing several initiatives to address these challenges, including optimizing manufacturing footprint and restructuring future sales from Canada. These efforts are expected to help mitigate the tariff impact as the fiscal year progresses.

Cash Flow and Balance Sheet

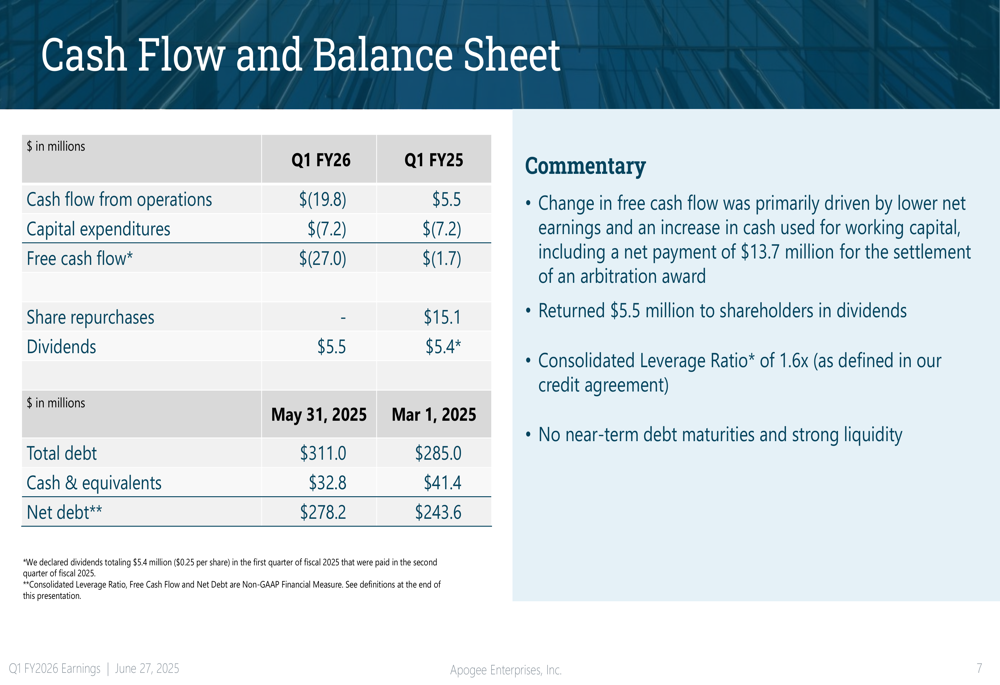

Despite the profitability challenges, Apogee maintained a solid financial position with a consolidated leverage ratio of 1.6x and strong liquidity. The company returned $5.5 million to shareholders through dividends during the quarter.

The cash flow details show:

The decline in cash flow from operations was attributed to lower earnings, working capital changes, and an arbitration award settlement. The company’s net debt increased slightly to $196.6 million as of May 31, 2025, compared to $180.0 million at the end of the previous quarter.

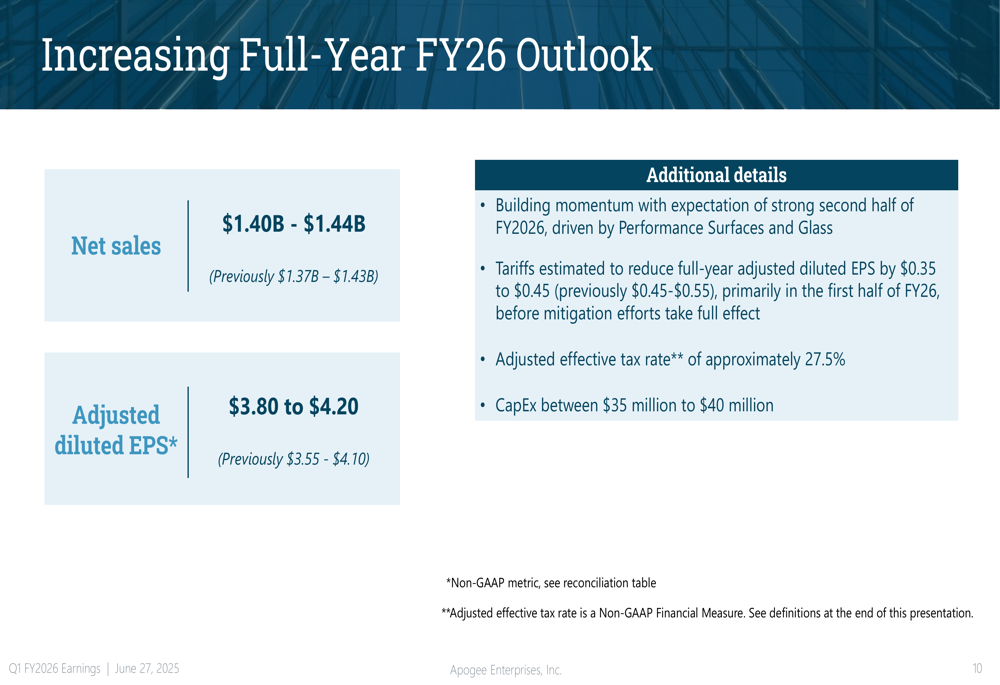

Revised Outlook and Guidance

In a positive development, Apogee raised its full-year fiscal 2026 guidance for both net sales and adjusted diluted EPS, reflecting management’s confidence in improving conditions as the year progresses.

The updated outlook shows:

The company now expects net sales between $1.40 billion and $1.44 billion, up from the previous range of $1.37 billion to $1.43 billion. Similarly, adjusted diluted EPS guidance was raised to $3.80-$4.20 from the previous range of $3.55-$4.10. Management cited building momentum and expectations for year-over-year growth in the second half of fiscal 2026.

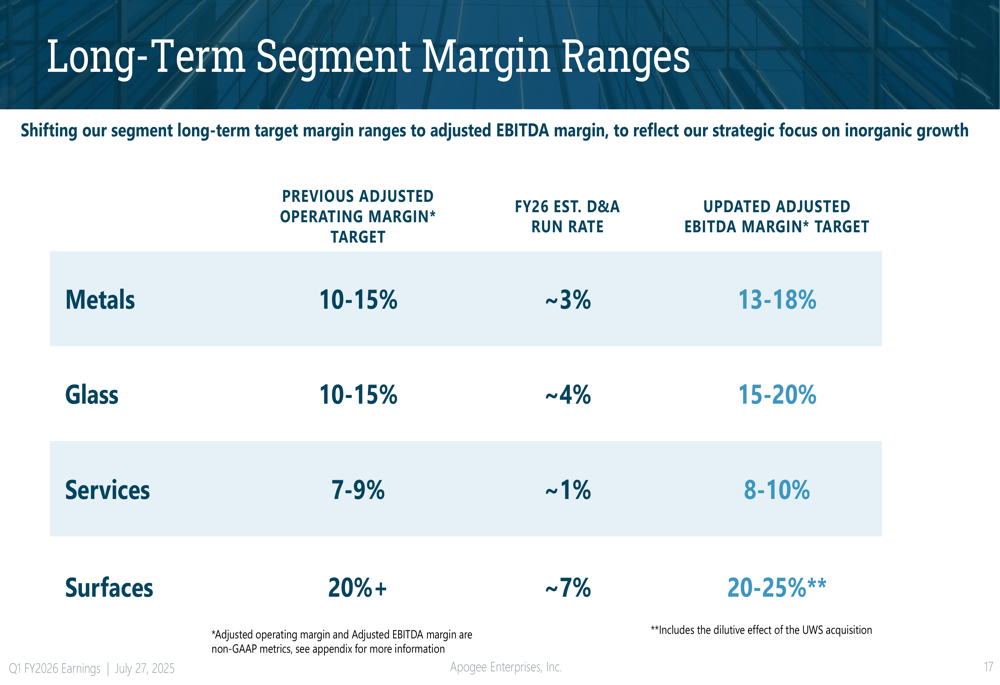

Strategic Initiatives

Apogee continues to execute its "Fortify Phase 2" strategy, focusing on driving improved outcomes through tariff mitigation, strategic execution, and active merger and acquisition activities. The company is positioning itself for long-term margin improvement across all segments.

The long-term segment margin targets illustrate this strategic direction:

These targets show Apogee’s commitment to improving profitability across its portfolio, with particularly ambitious goals for the Performance Surfaces segment, targeting adjusted EBITDA margins of 20-25%, though with some dilutive effect from the UWS acquisition in the near term.

In summary, while Apogee faces near-term challenges from tariffs and market conditions, management’s decision to raise full-year guidance suggests confidence in the company’s ability to navigate these headwinds and deliver improved performance in the second half of fiscal 2026. The positive premarket stock reaction indicates that investors share this optimism despite the significant year-over-year profitability declines in the first quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.