Domo signs strategic collaboration agreement with AWS for AI solutions

Apollo Commercial Real Estate Finance, Inc. (NYSE:ARI) presented its second quarter 2025 financial results on July 29, showcasing improved distributable earnings and significant portfolio expansion. The company reported distributable earnings of $0.26 per share, up from $0.24 in the previous quarter, fully covering its $0.25 quarterly dividend.

Quarterly Performance Highlights

Apollo Commercial RE Finance reported net income available to common stockholders of $18 million, or $0.12 per diluted share for Q2 2025. More importantly, distributable earnings reached $36 million, or $0.26 per diluted share, representing an 8.3% increase from the first quarter’s $0.24 per share.

The company declared common stock dividends of $0.25 per share, implying a dividend yield of 10.2% based on current market prices. This marks a significant improvement in dividend coverage compared to Q1, when distributable earnings covered 96% of the dividend.

As shown in the following chart of distributable earnings and book value per share:

Book value per share slightly decreased to $12.59 at quarter-end, compared to $12.66 in the previous quarter. The company ended the quarter with total common equity book value of $1.7 billion and $208 million of total liquidity, including $182 million of cash and $26 million available leverage.

In after-hours trading following the release, Apollo’s stock moved up 0.82% to $9.84, building on the day’s 0.41% gain during regular trading hours.

Loan Portfolio and Origination Activity

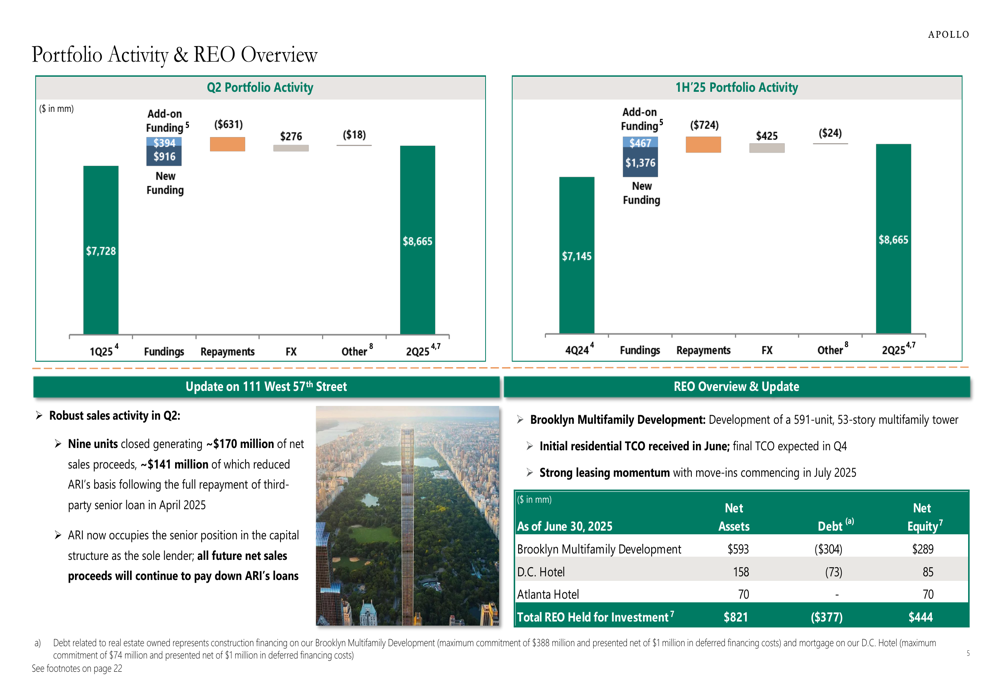

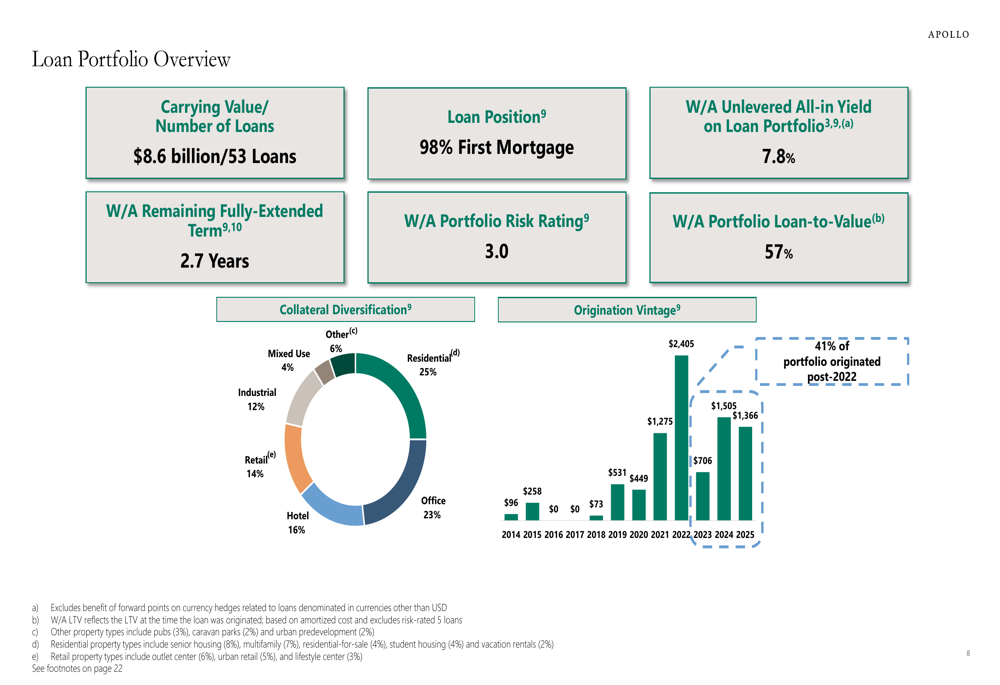

Apollo significantly expanded its loan portfolio in Q2, with the total portfolio reaching $8.6 billion, up from $7.7 billion reported at the end of Q1 2025. The portfolio maintains a weighted-average unlevered all-in yield of 7.8%, with 98% in first mortgages and 96% in floating rate loans.

The company’s portfolio activity for Q2 and the first half of 2025 is illustrated in the following chart:

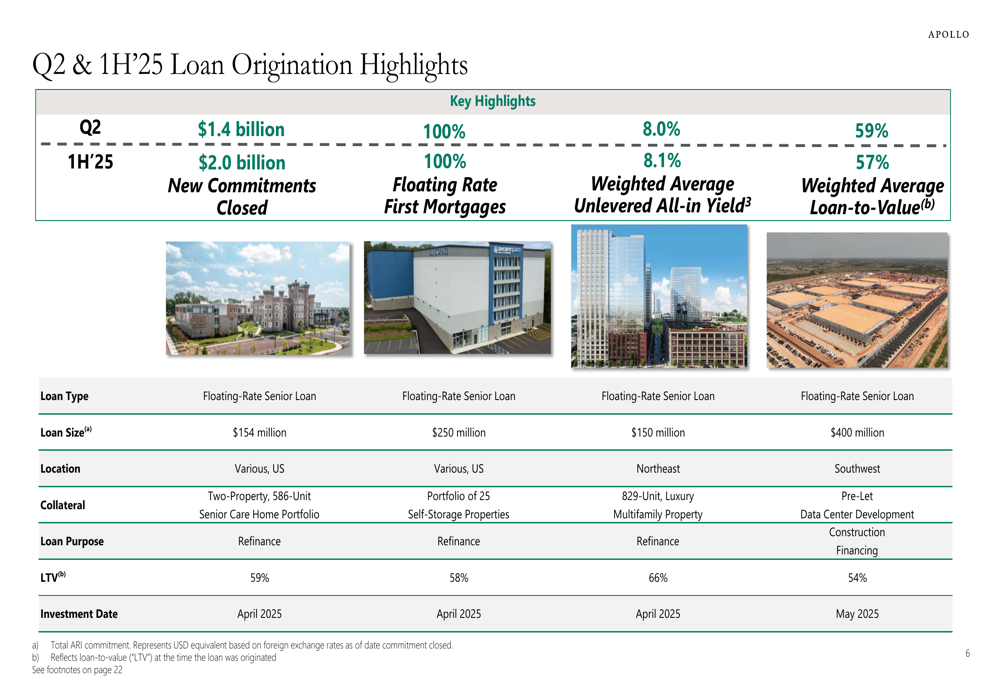

Loan origination was particularly strong in the second quarter, with $1.4 billion in new commitments closed. For the first half of 2025, new commitments totaled $2.0 billion, all in floating rate first mortgages with a weighted average unlevered all-in yield of 8.1% and a conservative weighted average loan-to-value ratio of 57%.

The following slide highlights some of the major loan originations during the quarter:

Apollo’s loan portfolio remains well-diversified across property types and geographies. Residential properties represent the largest segment at 25% of the portfolio, followed by office at 23%, hotel at 16%, retail at 14%, and industrial at 12%.

The geographic distribution shows significant international exposure, with 36% in the United Kingdom (TADAWUL:4280), 17% in New York City, and 13% in other European locations. This diversification strategy is illustrated in the following portfolio overview:

The company also provided an update on its REO (Real Estate Owned) properties, noting that its Brooklyn Multifamily Development received initial residential TCO (Temporary Certificate of Occupancy) in June, with strong leasing momentum and move-ins commencing in July 2025.

Capital Structure and Risk Management

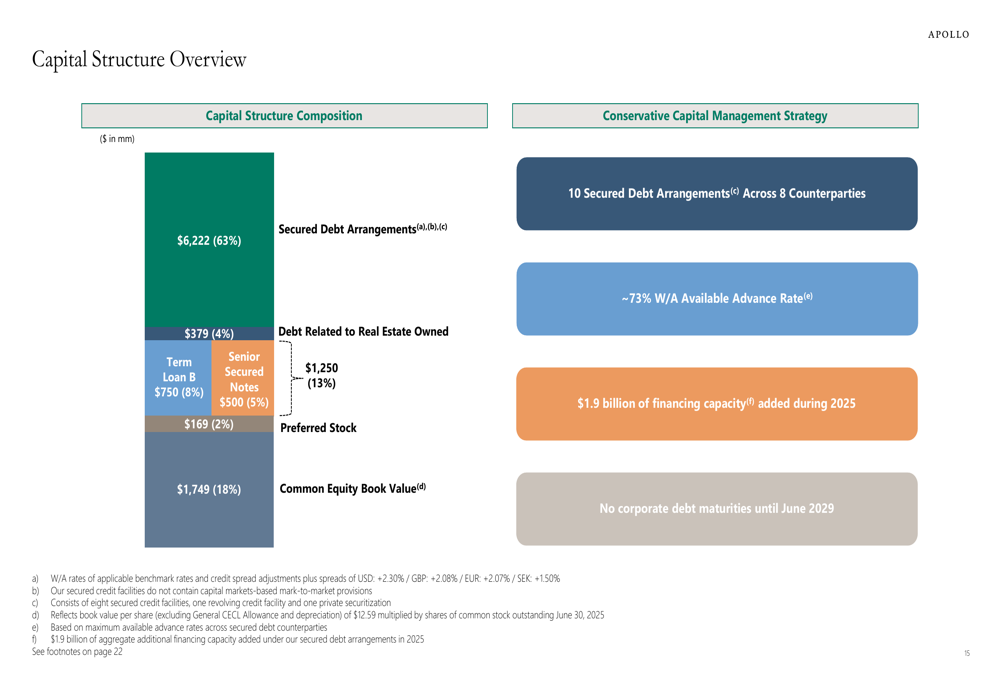

Apollo maintains a conservative capital management strategy with a diversified funding base. The capital structure consists of 63% secured debt arrangements, 13% debt related to real estate owned, 2% preferred stock, and 18% common equity book value.

As shown in the following capital structure overview:

The company has 10 secured debt arrangements across 8 counterparties with approximately 73% weighted average available advance rate. During 2025, Apollo added $1.9 billion of financing capacity and has no corporate debt maturities until June 2029.

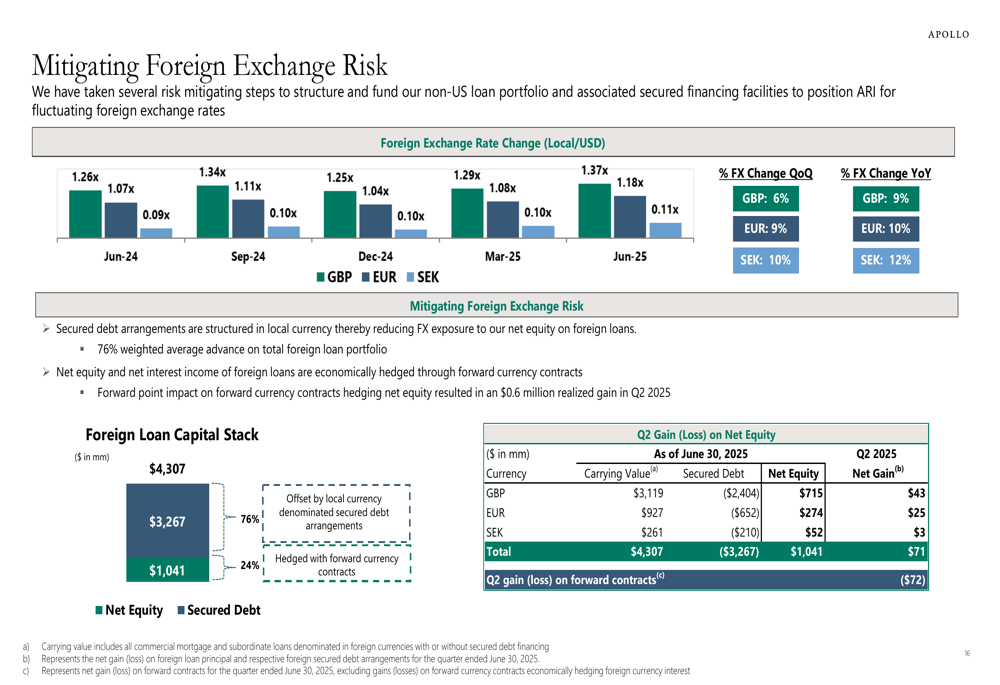

Given its significant international exposure, Apollo has implemented strategies to mitigate foreign exchange risk. Secured debt arrangements are structured in local currency, while net equity and net interest income of foreign loans are economically hedged through forward currency contracts.

The following chart illustrates the company’s approach to managing foreign exchange exposure:

In Q2, the company recorded a net gain of $71 million on net equity due to foreign exchange rate changes, largely offset by a $72 million loss on forward contracts, effectively demonstrating the hedging strategy’s performance.

Forward-Looking Statements

Apollo reported several significant subsequent events that will impact future quarters. The company received a full repayment of a $250 million first mortgage secured by a retail property in Manhattan, NY. Additionally, it reached a settlement agreement with Massachusetts Healthcare in which the commonwealth agreed to pay Saint Elizabeth, LLC an additional $44 million by August 20, 2025, with $18 million attributable to ARI.

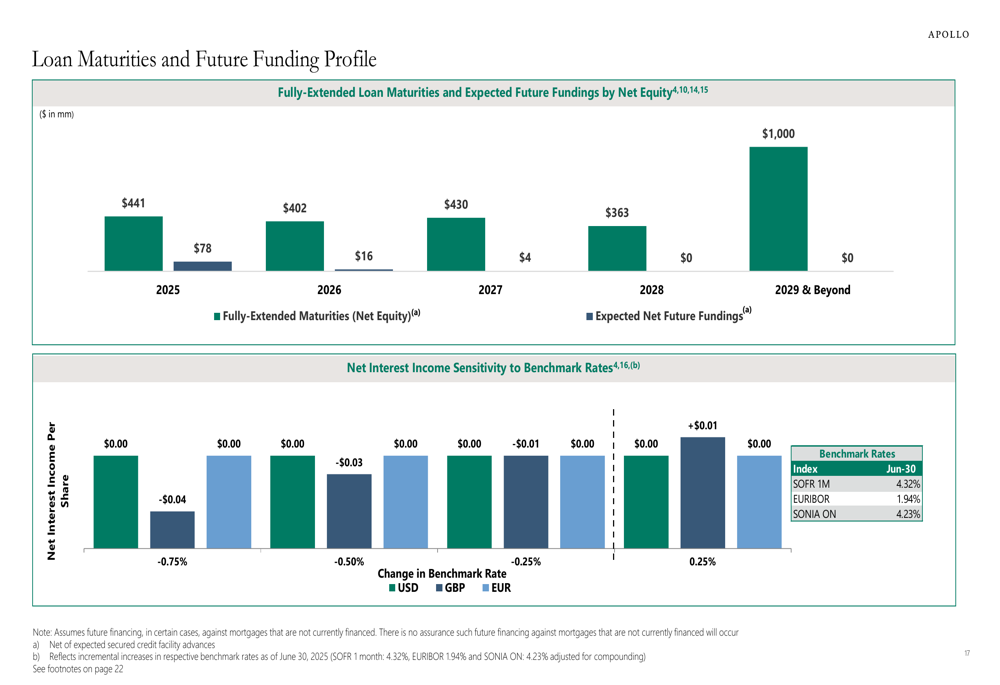

The company’s loan maturity and future funding profile suggests a balanced approach to managing upcoming obligations:

Looking ahead, Apollo appears well-positioned to navigate the commercial real estate market with its diversified portfolio, conservative loan-to-value ratios, and strong capital structure. The improvement in distributable earnings and full dividend coverage demonstrate the company’s ability to generate stable returns for shareholders despite ongoing market volatility.

The stock’s current trading level of $9.84 in after-hours represents a significant discount to book value of $12.59 per share, potentially offering value for investors seeking exposure to commercial real estate finance with an attractive dividend yield of over 10%.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.