IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

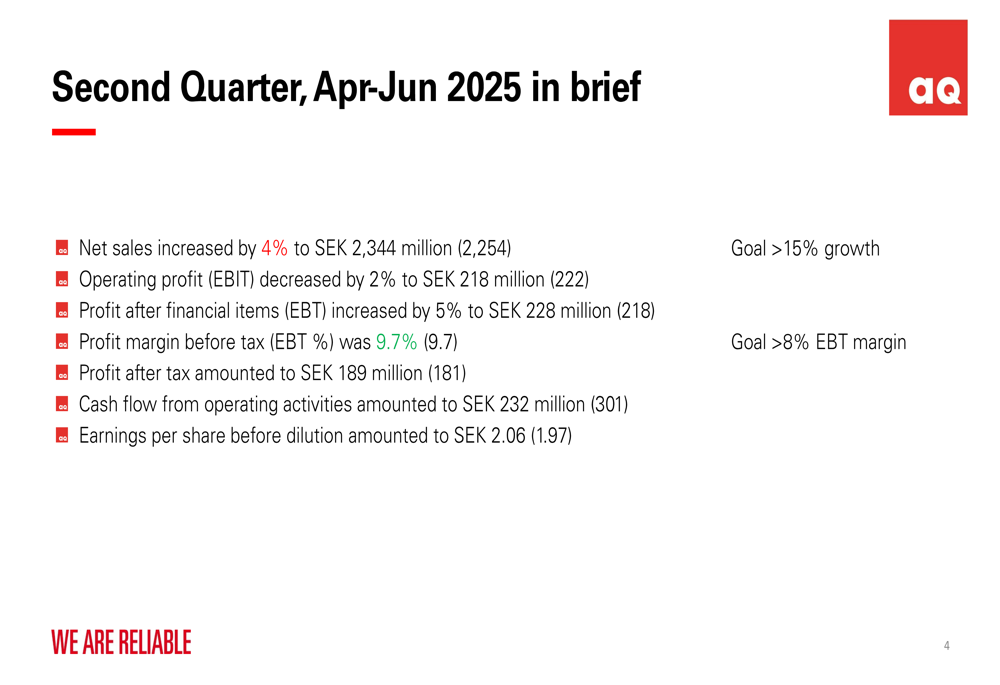

AQ Group AB (STO:AQ) reported its second quarter 2025 results on July 15, showing a 4% increase in net sales to SEK 2,344 million, primarily driven by acquisitions while organic growth remained minimal. The company’s stock closed at SEK 185.50 on July 14, down 0.8% ahead of the presentation, but still trading near its 52-week high of SEK 189.80.

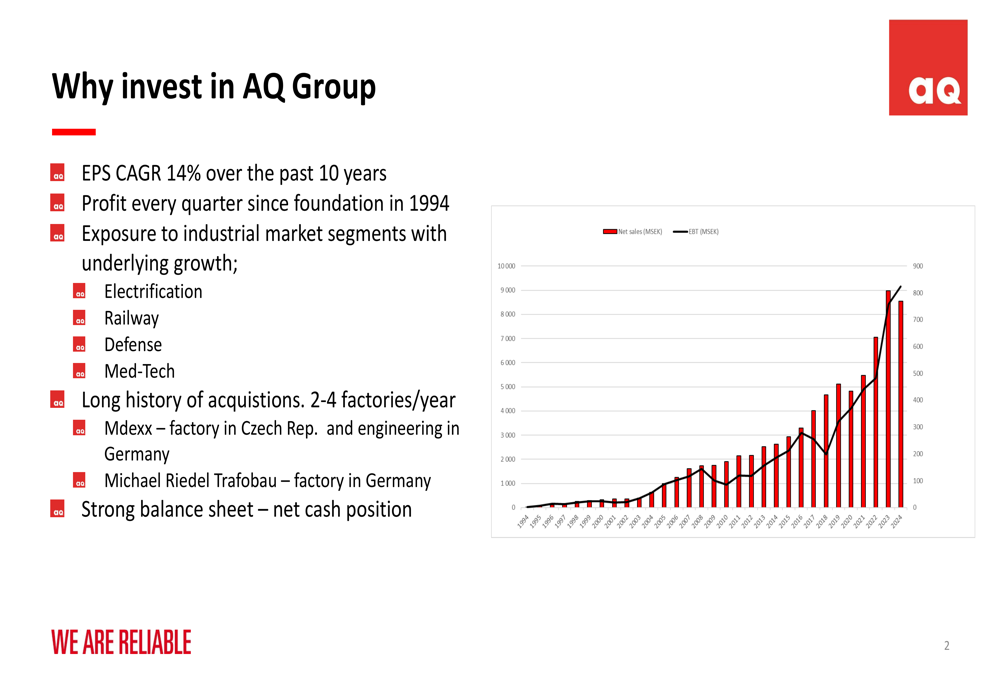

The industrial manufacturer, which operates across 17 countries with approximately 8,000 employees, continues to focus on growing market segments including electrification, railway, defense, and med-tech. These strategic sectors have helped AQ Group maintain its 30-year streak of quarterly profitability despite challenging market conditions in some segments.

Quarterly Performance Highlights

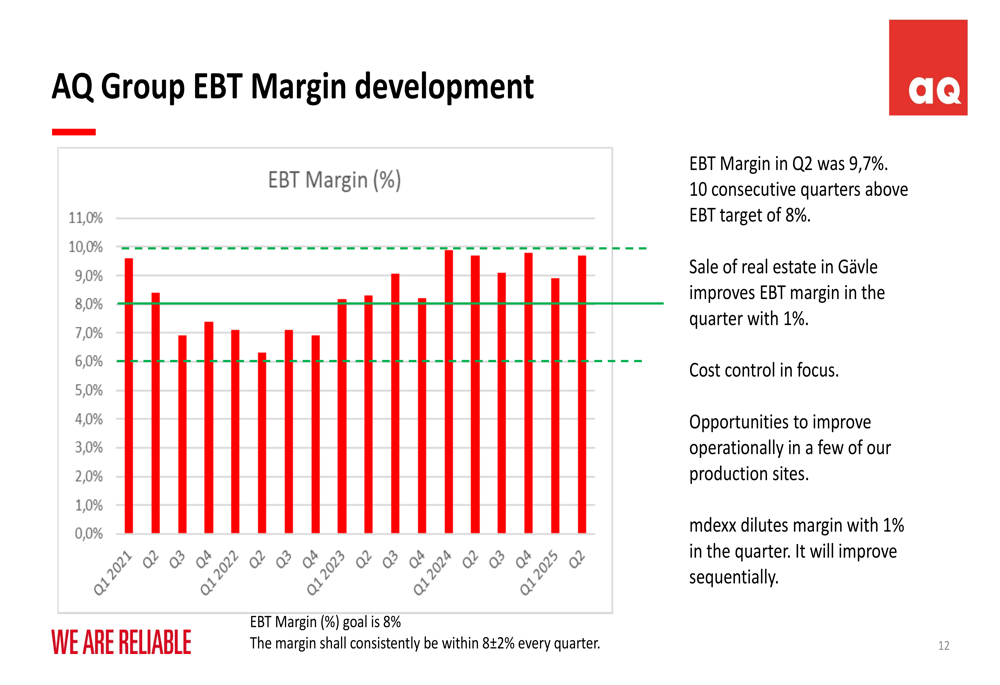

For Q2 2025, AQ Group reported a slight 2% decrease in operating profit (EBIT) to SEK 218 million, while profit after financial items (EBT) increased by 5% to SEK 228 million. The profit margin before tax remained stable at 9.7%, exceeding the company’s target of 8% for the tenth consecutive quarter.

As shown in the following chart summarizing the Q2 2025 performance:

Earnings per share before dilution rose to SEK 2.06, up from SEK 1.97 in the same period last year, representing a 4.6% increase. Cash flow from operating activities amounted to SEK 232 million, down from SEK 301 million in Q2 2024, reflecting some pressure on working capital.

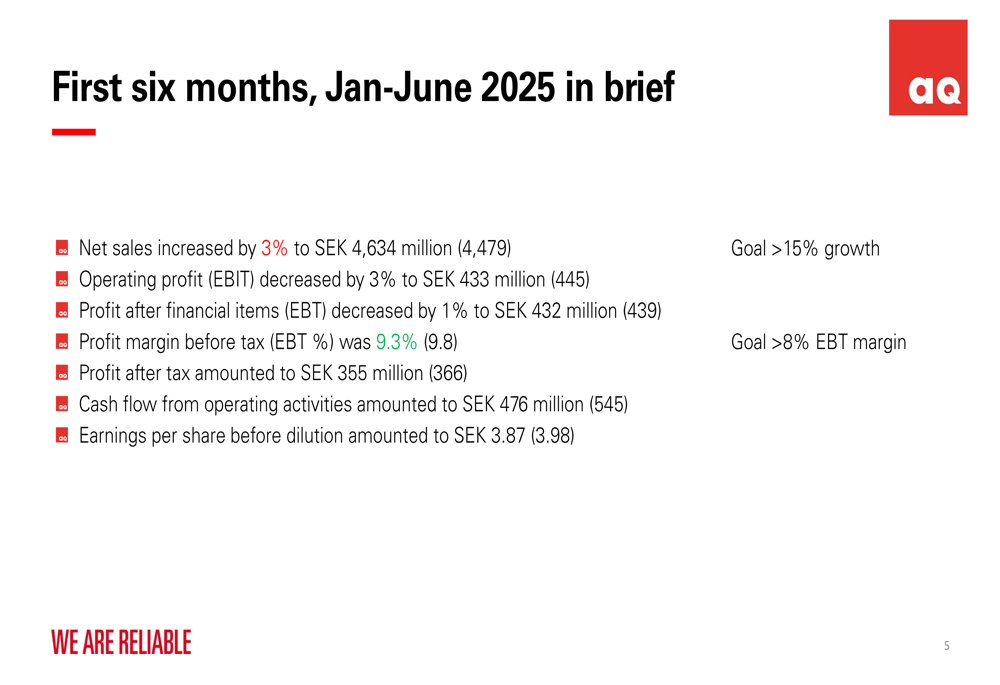

For the first half of 2025, the company reported a 3% increase in net sales to SEK 4,634 million, though both operating profit and profit after financial items showed slight decreases of 3% and 1% respectively.

Growth Strategy Analysis

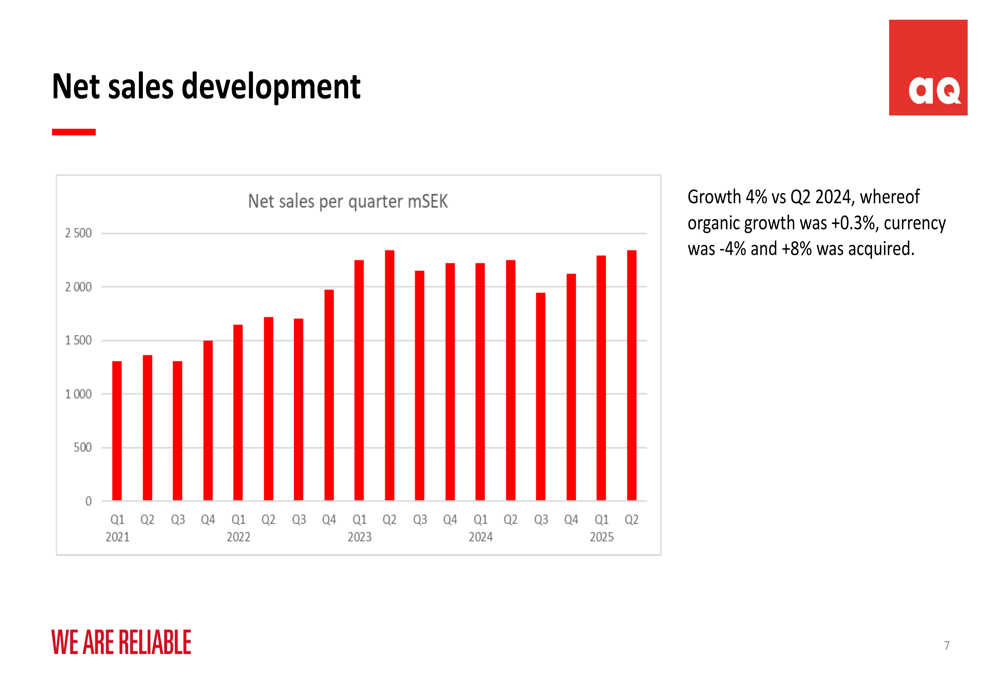

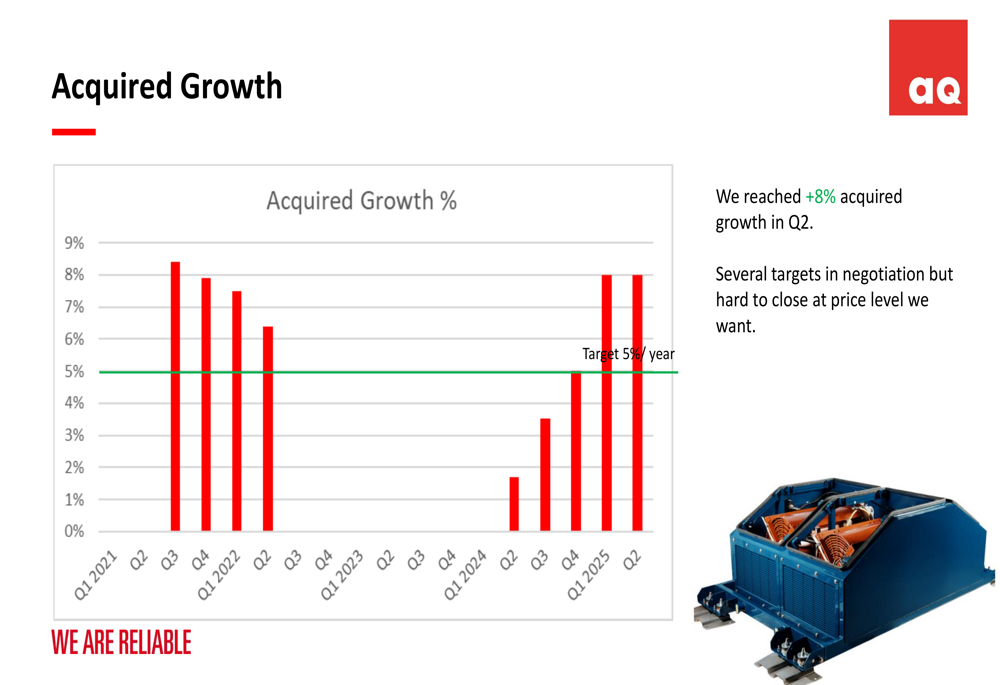

AQ Group’s growth strategy continues to rely heavily on acquisitions, with acquired growth contributing 8% in Q2 2025, while organic growth was minimal at just 0.3%. Currency effects had a negative 4% impact on overall growth.

The company’s net sales development shows a generally positive trend over the past several years, with some quarterly fluctuations:

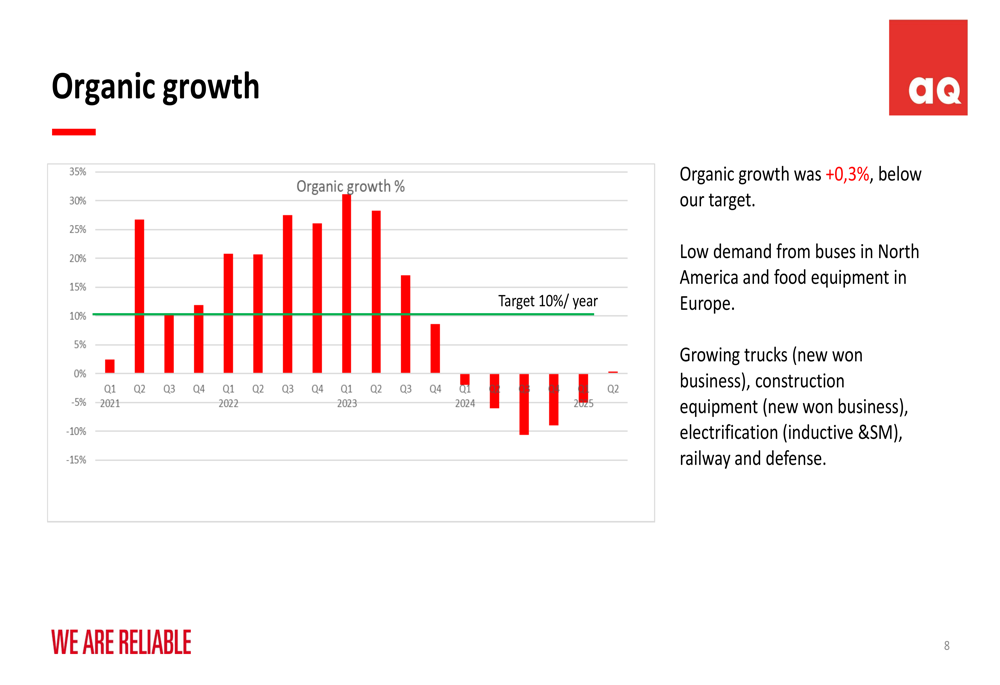

The organic growth chart reveals significant volatility, with the current 0.3% growth rate falling well below the company’s 10% annual target. Management identified trucks, construction, and railway sectors as the main growth drivers, while buses and food equipment segments acted as detractors.

Acquisitions remain central to AQ Group’s strategy, with the company historically averaging 2-4 factory acquisitions per year. However, management noted challenges in the current environment: "Several targets in negotiation but hard to close at price level we want."

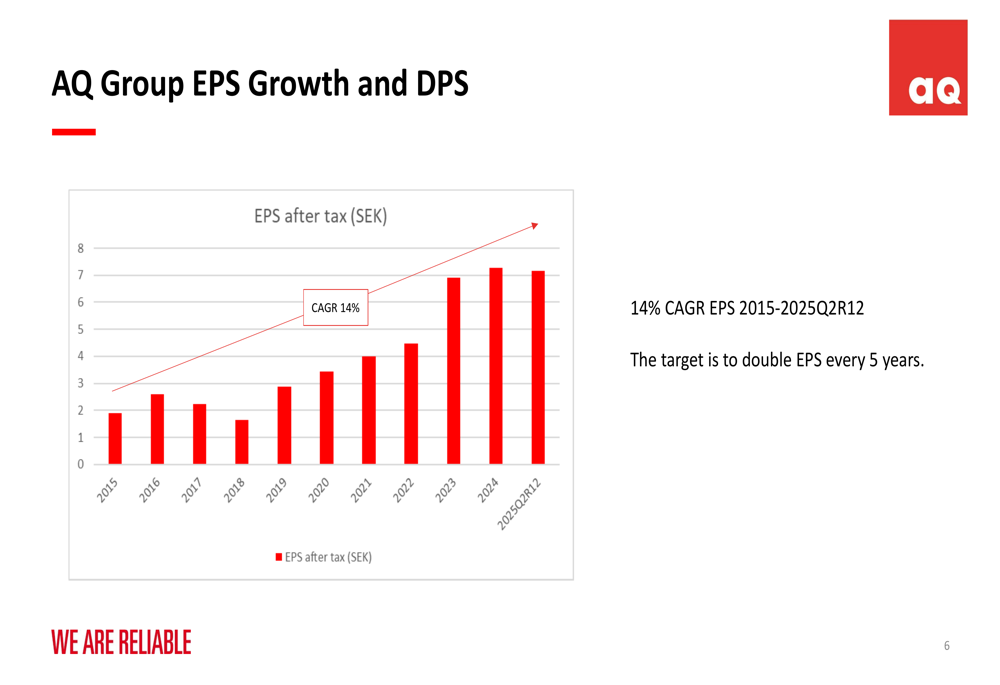

The company’s long-term earnings per share growth remains impressive, with a 14% CAGR over the past decade, aligning with its target of doubling EPS every five years.

Operational Challenges and Improvements

AQ Group highlighted several operational areas requiring attention. The integration of mdexx, a recent acquisition, is diluting the company’s margin by approximately 1% in the quarter, though management expects sequential improvement. The presentation noted that a hailstorm at the mdexx Riedel facility affected June turnover, though most costs will be covered by insurance.

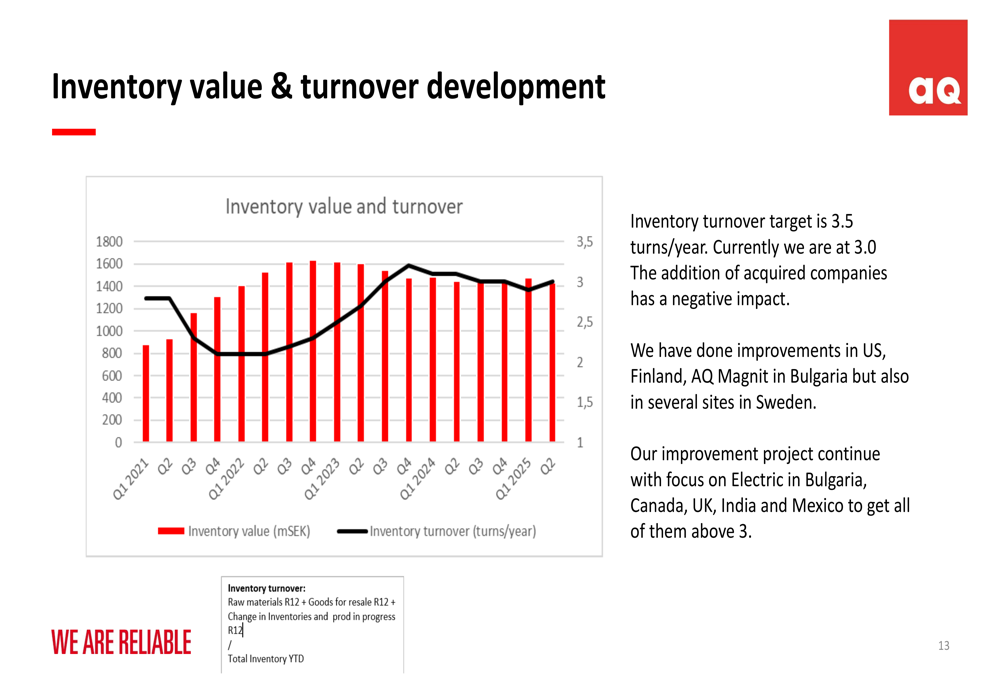

Inventory management remains challenging, with inventory turnover at 3.0 turns/year against a target of 3.5. The company reported improvements in operations in the US, Finland, and Bulgaria, with ongoing projects focused on sites in Bulgaria, Canada, UK, India, and Mexico.

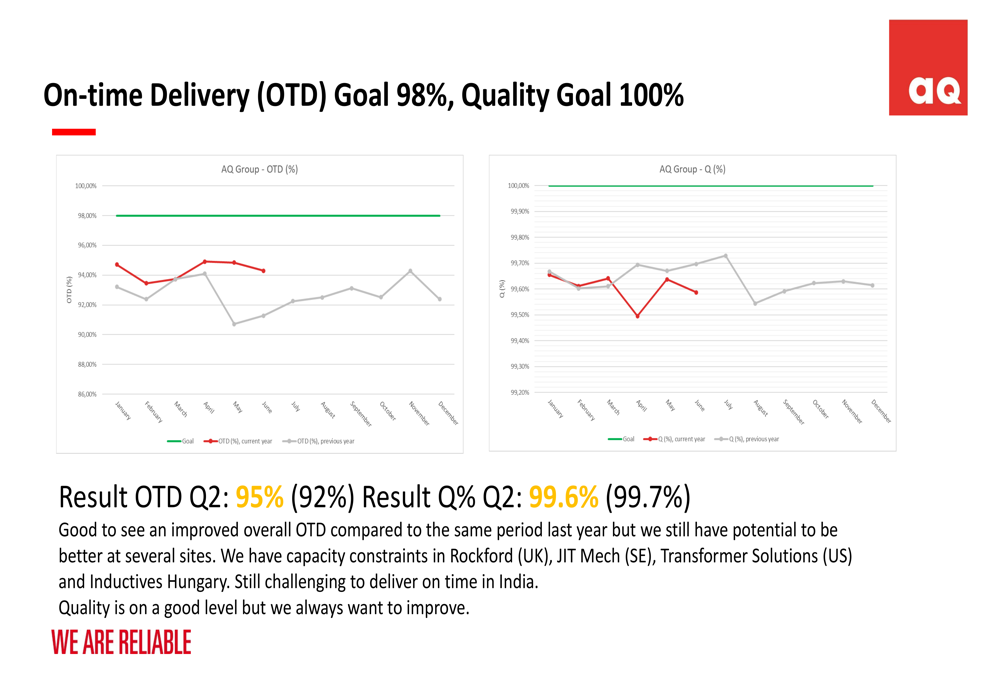

On-time delivery performance improved to 95% in Q2 2025, up from 92% in the same period last year, though still below the 98% target. Quality metrics remained strong at 99.6%, close to the 100% goal. The company identified capacity constraints at several facilities including Rockford (UK), JIT Mech (SE), Transformer Solutions (US), and Inductives Hungary, with ongoing delivery challenges in India.

Profitability remains a bright spot, with the company maintaining an EBT margin of 9.7% in Q2, supported by a 1% boost from the sale of real estate in Gävle. Management emphasized that "cost control is in focus" while acknowledging opportunities for operational improvements at several production sites.

Forward-Looking Statements

AQ Group maintains a positive outlook based on its exposure to growing industrial segments and strong balance sheet with a net cash position of 219 mSEK. The company continues to target annual growth exceeding 15% and an EBT margin above 8%.

Management expects the mdexx integration to improve sequentially, with several initiatives underway including ERP implementation planned for Q1 2026, refinancing of factoring and external loans expected to complete in Q4 2025, and the merger of mdexx Weyhe and AQ Paderborn facilities by the end of 2025.

The company highlighted recent project wins in power electric modules, offshore wind solutions, electric vehicles, and railway solutions as indicators of future growth potential. With approximately 8,000 employees, operations across 7 business areas, and presence in over 15 market segments, AQ Group continues to position itself as a reliable partner for industrial customers across its global footprint.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.