Gold prices hit 2-week high as Trump-Fed feud escalates with Cook firing

Introduction & Market Context

Arcosa Inc (NYSE:ACA) presented its first quarter 2025 earnings results on May 7, 2025, highlighting strong adjusted EBITDA growth despite a significant decline in net income. The infrastructure company, which has been strategically transforming its business mix since 2018, reported continued progress in its margin expansion initiatives while maintaining its full-year guidance.

The company’s stock has shown volatility in recent months, with a notable drop following its Q4 2024 earnings miss but has since partially recovered. Currently trading at $85.97, Arcosa remains focused on its long-term strategic vision while navigating segment-specific challenges.

Quarterly Performance Highlights

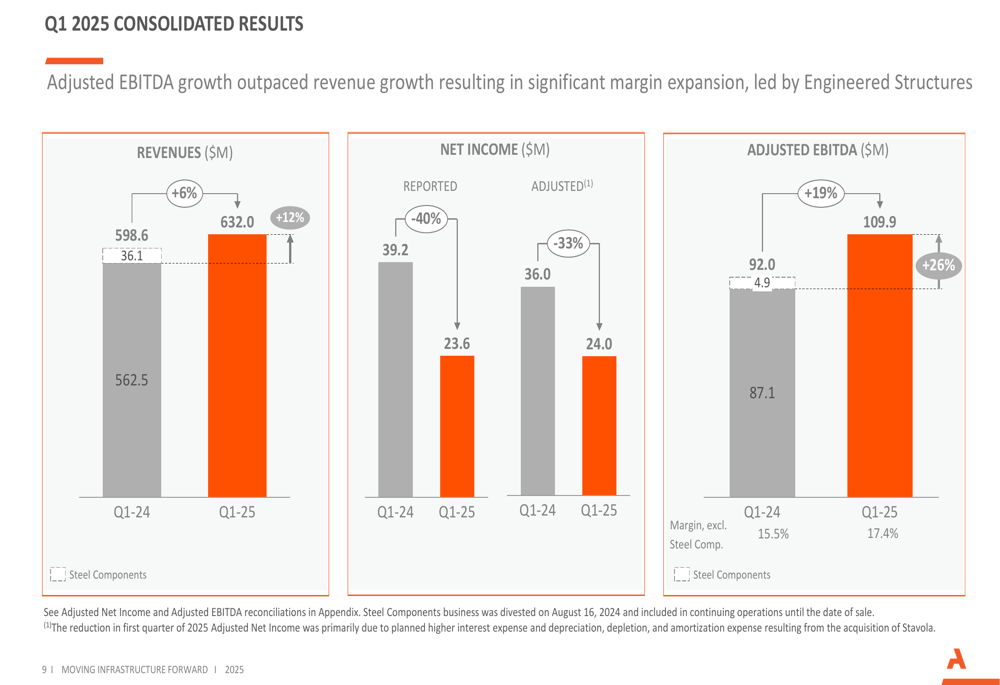

Arcosa reported Q1 2025 revenues of $632 million, representing a 12% increase from the $562.5 million reported in Q1 2024. However, when excluding the divested Steel Components business, organic revenue growth was 6%. The company’s adjusted EBITDA showed impressive growth of 26% year-over-year, reaching $109.9 million compared to $87.1 million in the prior year period.

Despite these positive top-line and adjusted earnings metrics, reported net income declined significantly by 40%, falling to $23.6 million from $39.2 million in Q1 2024. Adjusted net income also decreased by 33% to $24 million.

As shown in the following consolidated results chart:

The company’s adjusted EBITDA margin expanded by 190 basis points to 17.4%, demonstrating Arcosa’s ability to improve profitability despite challenges. Management attributed approximately 275 basis points of this improvement to organic margin expansion, highlighting the success of operational efficiency initiatives.

Segment Analysis

Arcosa’s performance varied significantly across its three business segments:

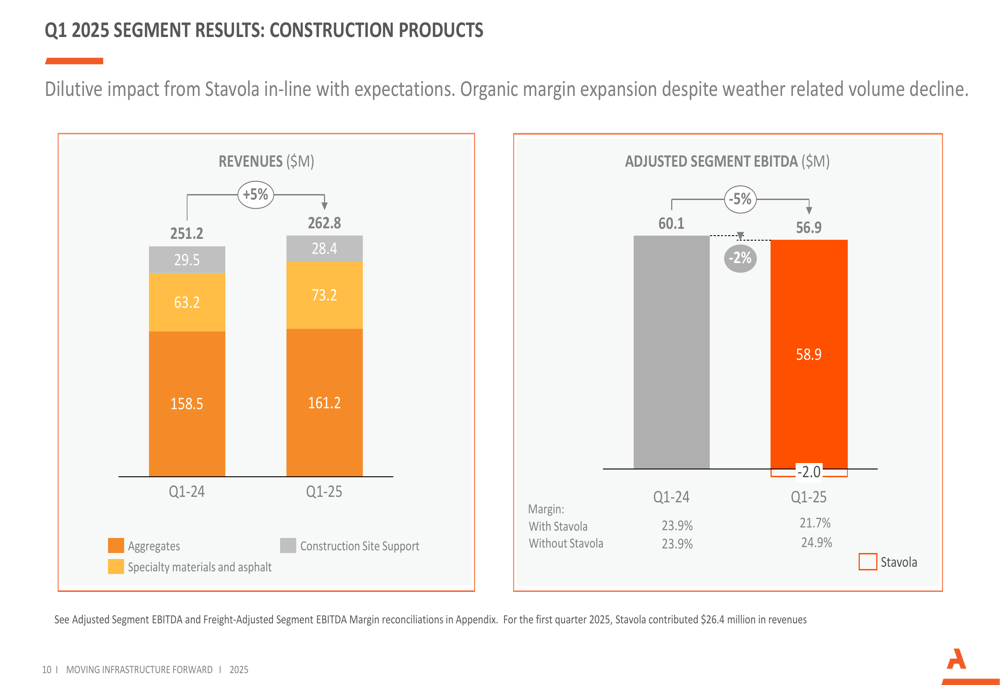

The Construction Products segment, which now represents the largest portion of Arcosa’s business at 59% of revenue, saw modest revenue growth of 5% to $262.8 million. However, adjusted segment EBITDA declined by 5% to $56.9 million, with margins contracting from 23.9% to 21.7%. This decline was primarily attributed to the dilutive impact of the Stavola acquisition, which contributed $26.4 million in revenues but faced seasonal challenges. Excluding Stavola, the segment’s margin would have expanded to 24.9%.

As illustrated in the Construction Products segment results:

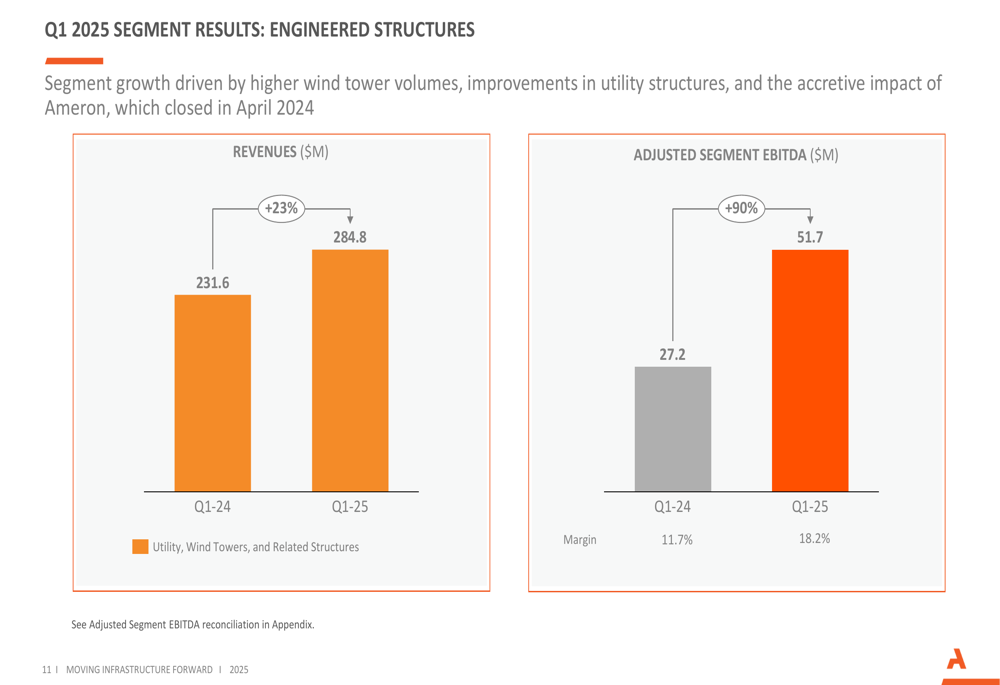

The Engineered Structures segment delivered the strongest performance, with revenues increasing 23% to $284.8 million and adjusted segment EBITDA surging 90% to $51.7 million. Margins in this segment expanded dramatically from 11.7% to 18.2%, driven by strong utility structures and wind tower demand.

The segment’s performance is visualized here:

The Transportation Products segment saw revenues decline by 27% to $84.4 million, largely due to the divestiture of Steel Components. Excluding this impact, the segment achieved 6% organic growth. Similarly, adjusted segment EBITDA fell 17% to $15.5 million, but increased 13% on an organic basis. Margins improved from 17.2% to 18.4%.

Strategic Transformation Progress

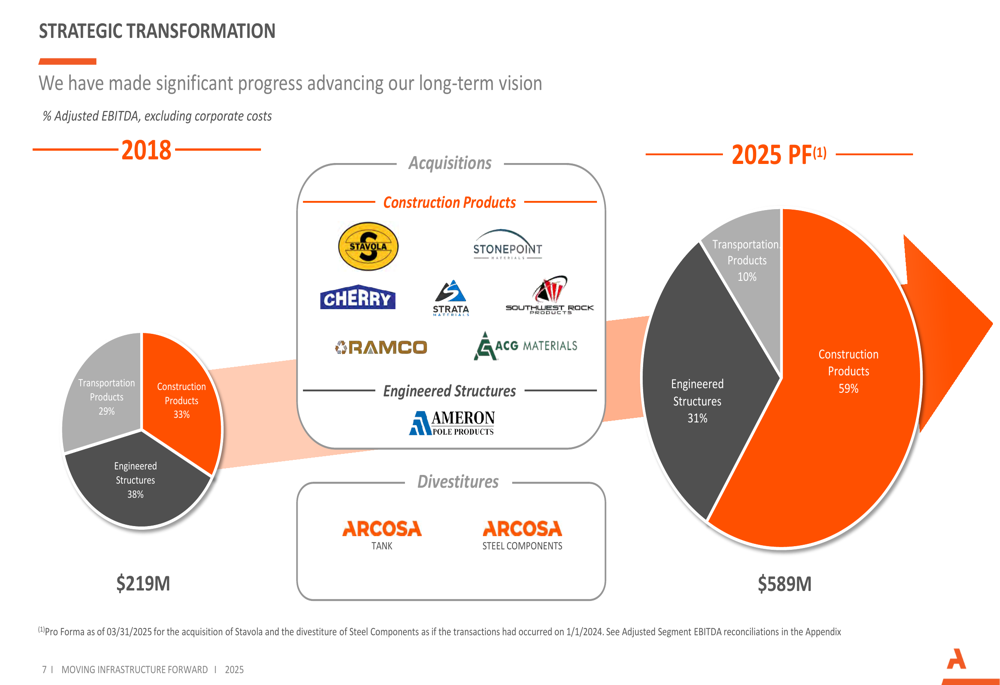

A key focus of Arcosa’s presentation was its ongoing strategic transformation, which has significantly altered its business mix since 2018. The company has shifted from a more balanced revenue distribution to one heavily weighted toward Construction Products, which now represents 59% of revenue compared to 33% in 2018.

This transformation is illustrated in the following strategic chart:

Through strategic acquisitions including Cherry, Strata, Southwest Rock, ACG Materials, Ameron Pole Products, and most recently Stavola, alongside divestitures of Arcosa Tank and Arcosa Steel Components, the company has reshaped its portfolio to focus on higher-margin, less cyclical businesses.

The company’s adjusted EBITDA has grown from $219 million in 2018 to a projected $589 million in 2025 (pro forma), representing a significant expansion in both scale and profitability.

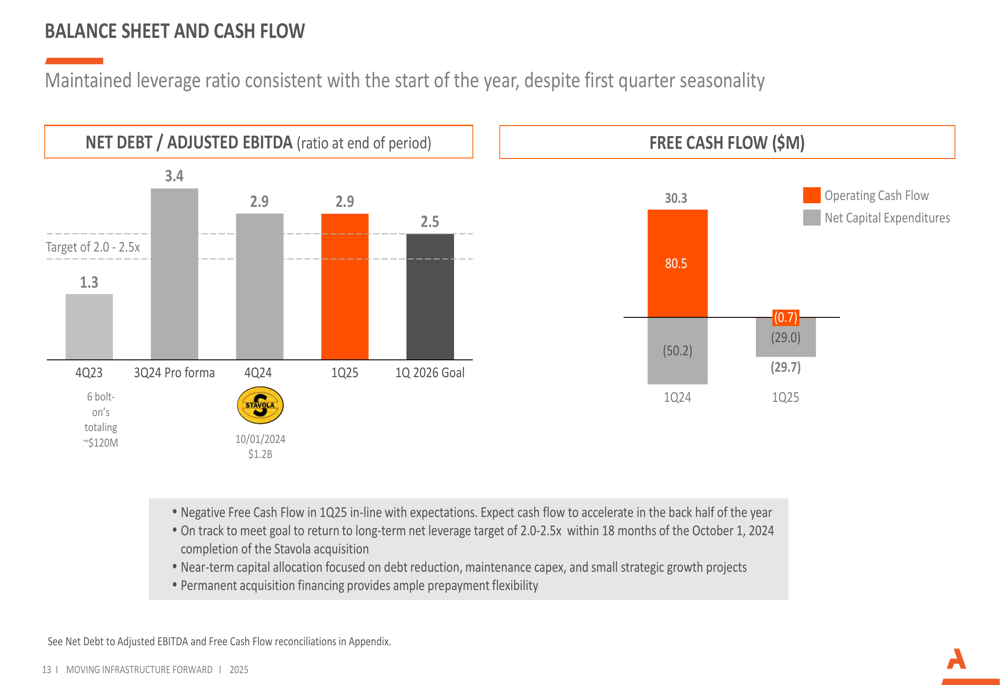

Balance Sheet and Cash Flow

Arcosa reported maintaining its Net Debt to Adjusted EBITDA ratio at 2.9x, despite typical first-quarter seasonality in its Construction Products segment. The company remains committed to deleveraging, with a target of returning to its long-term leverage ratio of 2.0-2.5x within the next twelve months.

Free cash flow was negative at $(29.7) million in Q1 2025, compared to positive $30.3 million in Q1 2024. Management indicated this was in line with expectations and projected cash flow to accelerate in the second half of the year.

The company’s balance sheet metrics and deleveraging plans are shown here:

Liquidity remains strong at $868 million, including full availability under the company’s revolving credit facility. Management emphasized that near-term capital allocation priorities include debt reduction, maintenance capital expenditures, and small strategic growth projects.

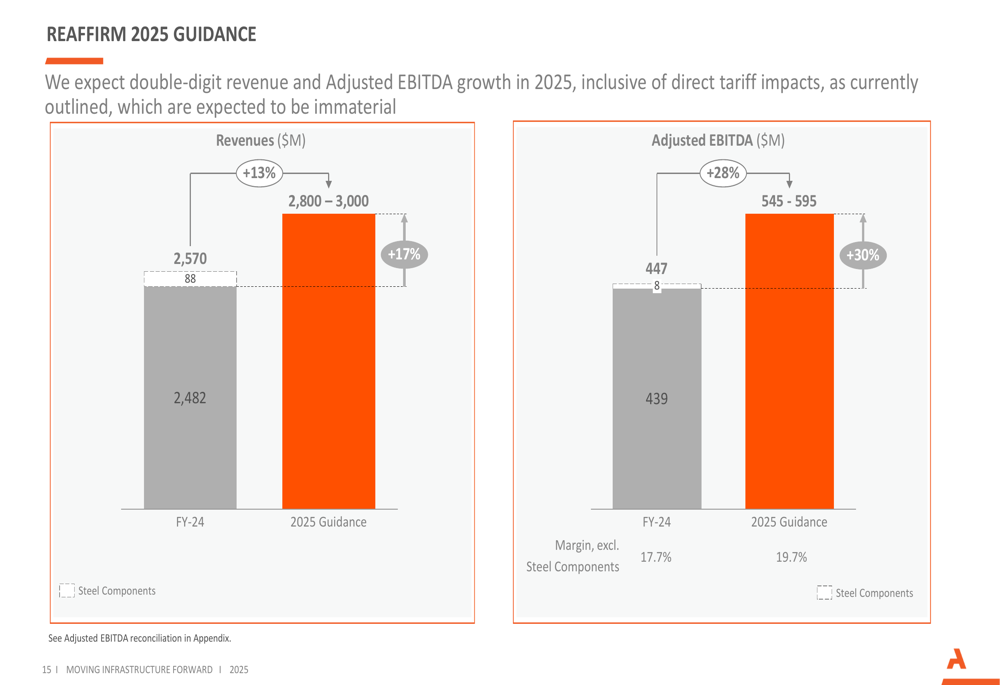

2025 Outlook and Guidance

Arcosa reaffirmed its full-year 2025 guidance, projecting revenues of $2.8-3.0 billion (representing 13% growth) and adjusted EBITDA of $545-595 million (representing 28% growth). The company expects adjusted EBITDA margin expansion of approximately 200 basis points, with roughly 60% of adjusted EBITDA growth coming from inorganic sources and 40% from organic growth.

The company’s 2025 guidance is visualized in this chart:

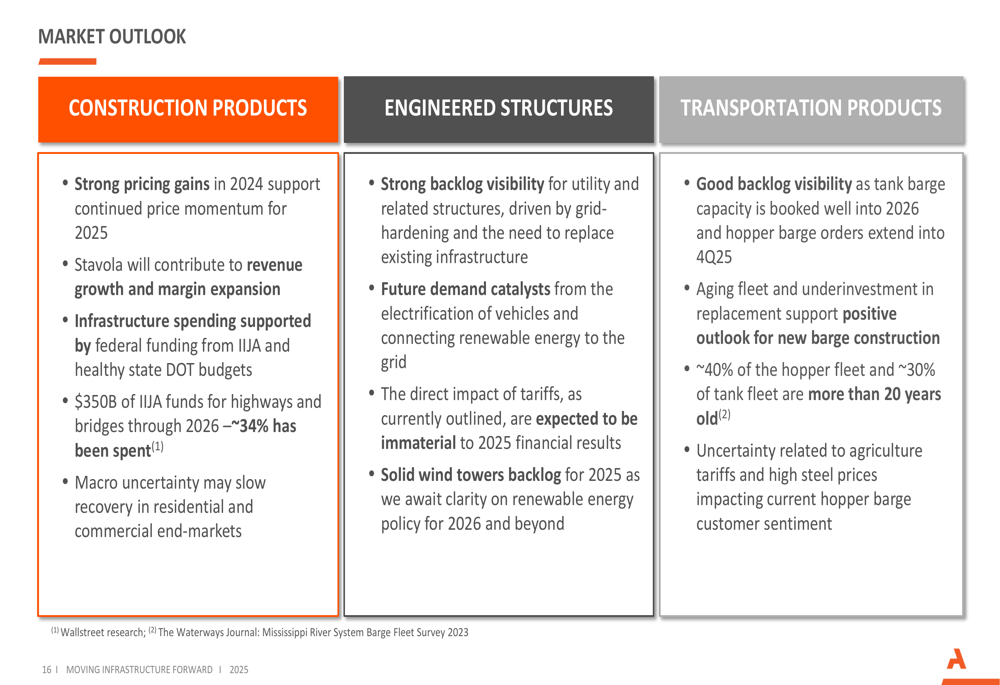

Management provided a positive market outlook across all segments:

In Construction Products, the company expects strong pricing gains and infrastructure spending support. The Engineered Structures segment benefits from strong backlog visibility and future demand catalysts, with management noting an immaterial impact from tariffs. For Transportation Products, the company cited good backlog visibility and a positive outlook for new barge construction, though acknowledged some uncertainty related to agriculture tariffs.

Additional guidance details include a tax rate of 19-20%, capital expenditures of $145-165 million, and depreciation, depletion, and amortization expense of $230-235 million for 2025.

Despite the mixed Q1 results, Arcosa’s management remains confident in the company’s strategic direction and ability to deliver on its full-year targets, emphasizing the ongoing transformation toward higher-margin, less cyclical business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.