Vertex Pharmaceuticals stock falls after pain drug fails in Phase 2 study

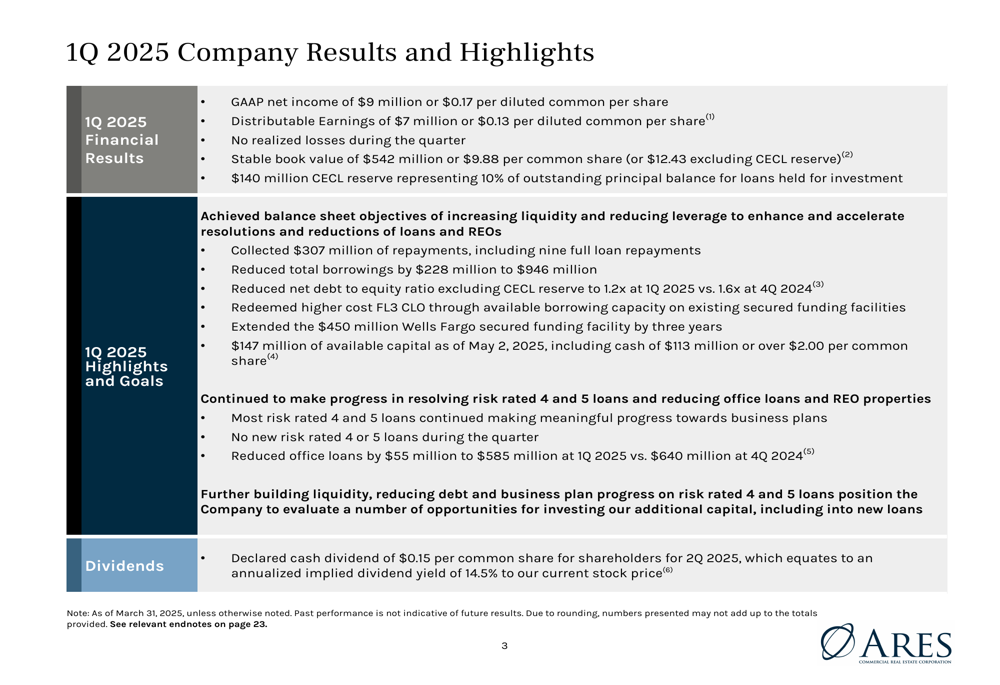

Ares Commercial Real Estate Corporation (NYSE:ACRE) returned to profitability in the first quarter of 2025, reporting GAAP net income of $9 million after posting losses in the previous quarter. The company’s May 7 earnings presentation highlighted continued progress in its strategic deleveraging efforts and reduction of office loan exposure.

Quarterly Performance Highlights

ACRE reported GAAP net income of $9 million ($0.17 per diluted common share) for Q1 2025, a significant improvement from the $10.7 million loss ($0.20 per share) in Q4 2024. Distributable earnings came in at $7 million ($0.13 per diluted common share).

The company maintained a stable book value of $542 million ($9.88 per common share, or $12.43 excluding CECL reserve) and declared a cash dividend of $0.15 per common share for Q2 2025, representing an annualized implied dividend yield of 14.5% based on the current stock price.

As shown in the following quarterly results summary:

ACRE collected $307 million in loan repayments during the quarter, including nine full loan repayments, which helped strengthen its balance sheet position. The company reported no realized losses during the quarter, a positive sign after previous periods of financial strain.

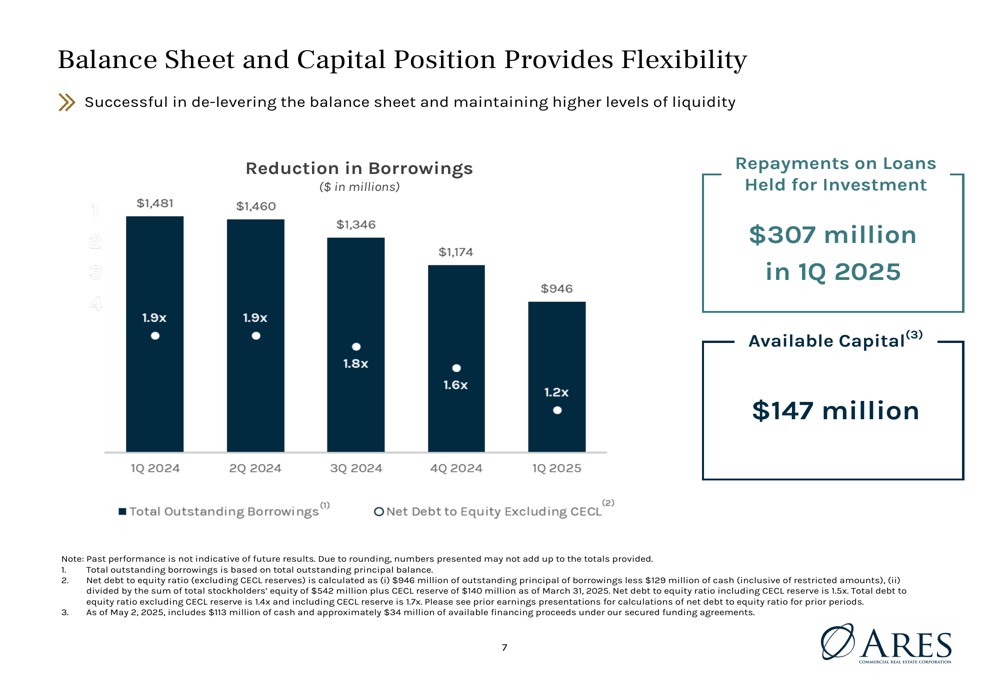

Strategic Deleveraging Initiative

A key focus of ACRE’s strategy has been reducing leverage and improving its capital position. The company reduced total borrowings by $228 million to $946 million and lowered its net debt to equity ratio (excluding CECL reserve) to 1.2x at Q1 2025, compared to 1.6x at Q4 2024.

The following chart illustrates the company’s consistent deleveraging progress over the past year:

This represents a significant improvement from the 1.9x leverage ratio reported in Q1 2024, demonstrating management’s commitment to strengthening the balance sheet. The company also redeemed its higher-cost FL3 CLO through available borrowing capacity on existing secured funding facilities and extended its $450 million Wells Fargo (NYSE:WFC) secured funding facility by three years.

As of May 2, 2025, ACRE reported $147 million of available capital, including cash of $113 million (over $2.00 per common share), providing substantial liquidity for future operations.

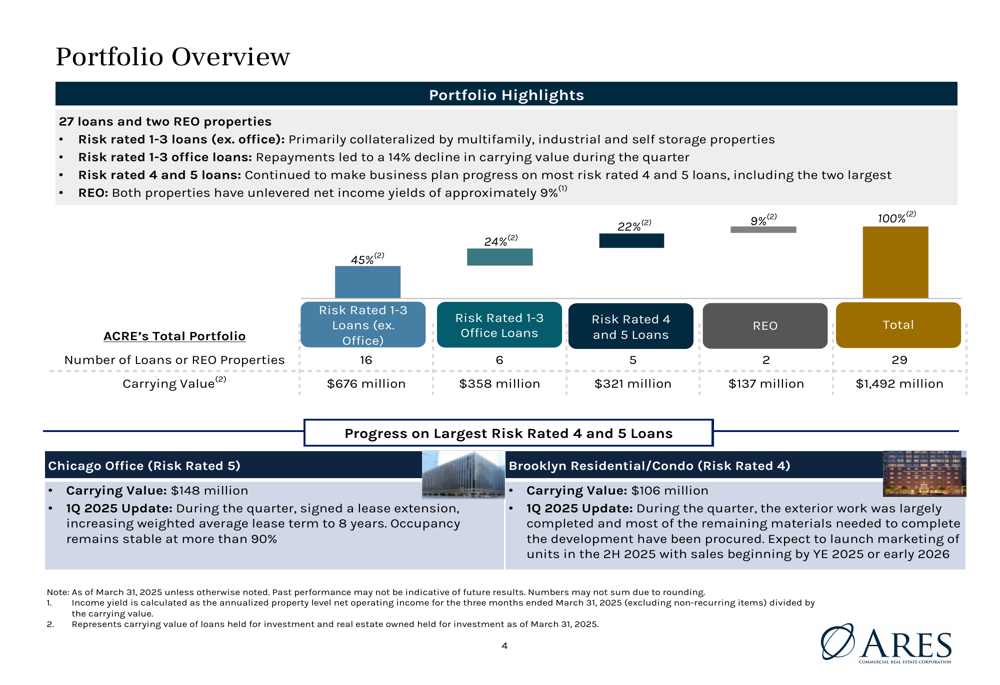

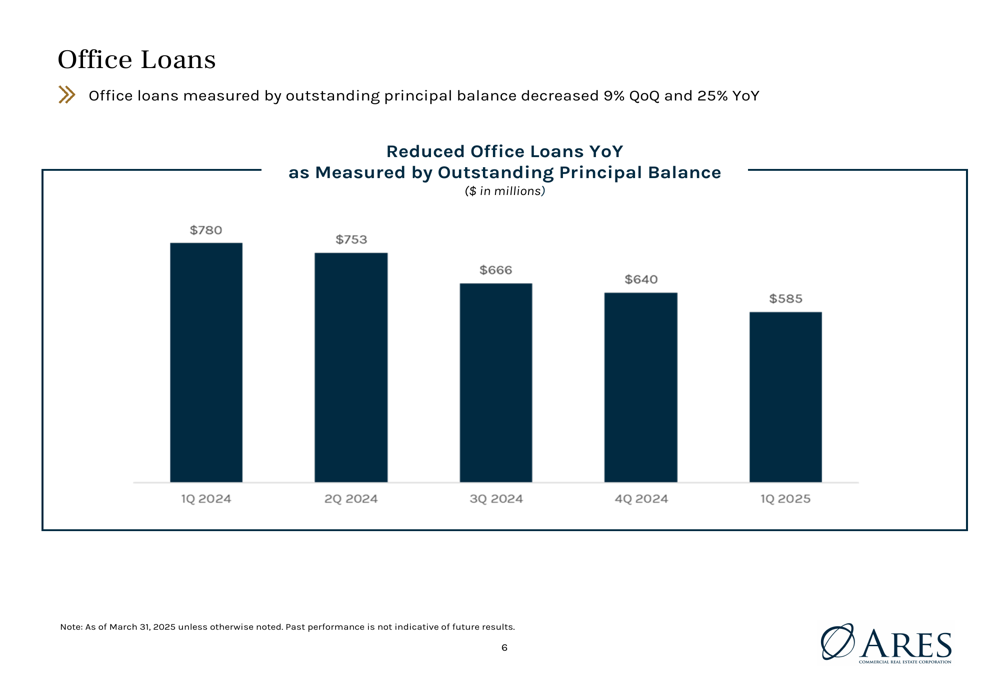

Portfolio Repositioning and Risk Management

ACRE’s portfolio consists of 27 loans and two REO properties, with a strategic focus on reducing exposure to higher-risk office properties. The company’s office loans measured by outstanding principal balance decreased 9% quarter-over-quarter and 25% year-over-year.

The portfolio breakdown shows a diversification across property types and risk ratings:

The company continues to make progress on its largest risk-rated loans, including a Chicago office property (Risk Rated 5) where it signed a lease extension, increasing the weighted average lease term to 8 years with occupancy remaining stable at more than 90%. For its Brooklyn Residential/Condo project (Risk Rated 4), exterior work was largely completed with unit marketing expected to launch in the second half of 2025.

The following chart demonstrates ACRE’s consistent reduction in office loan exposure:

Detailed Financial Analysis

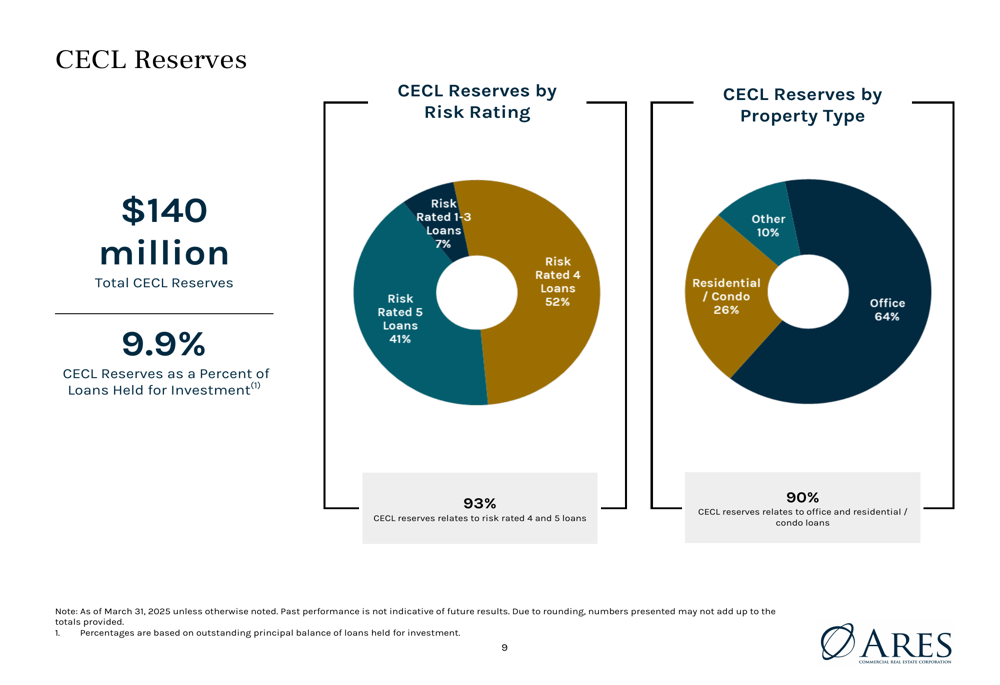

ACRE maintains a $140 million CECL (Current Expected Credit Losses) reserve, representing 10% of the outstanding principal balance for loans held for investment. The CECL reserve decreased slightly from $145 million in Q4 2024, reflecting some improvement in the company’s risk assessment.

The breakdown of CECL reserves provides insight into where management perceives the greatest risks:

Notably, 93% of CECL reserves relate to risk-rated 4 and 5 loans, while 90% relate to office and residential/condo loans. This concentration highlights the continued challenges in these sectors of the commercial real estate market.

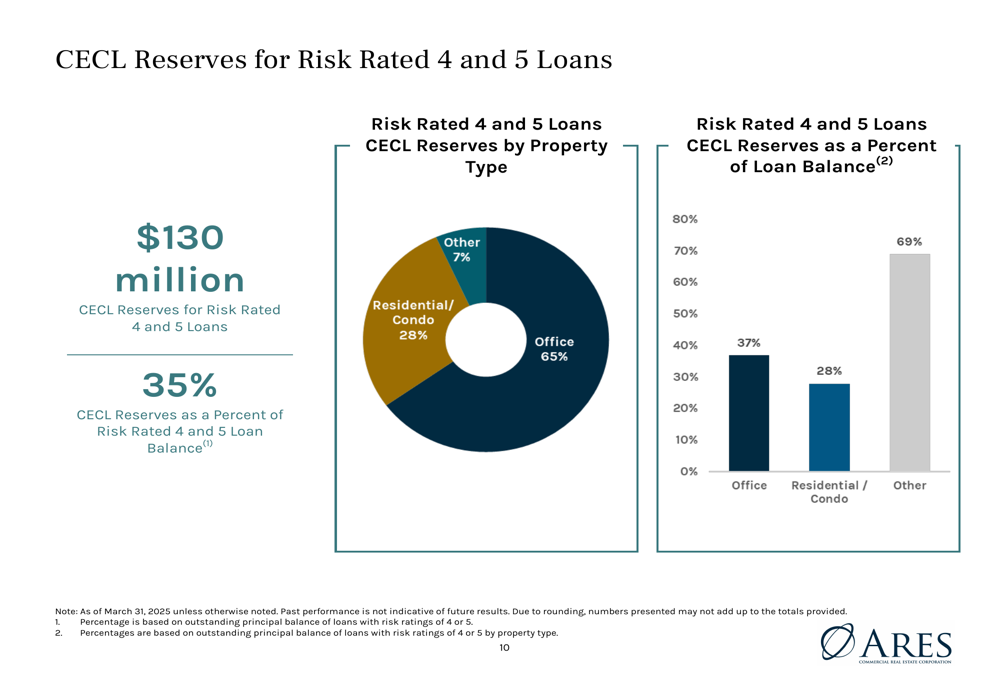

For higher-risk loans specifically, the company has set aside substantial reserves:

CECL reserves for risk-rated 4 and 5 loans total $130 million, representing 35% of the loan balance for these higher-risk assets. By property type, office loans account for 65% of these reserves, followed by residential/condo at 28%.

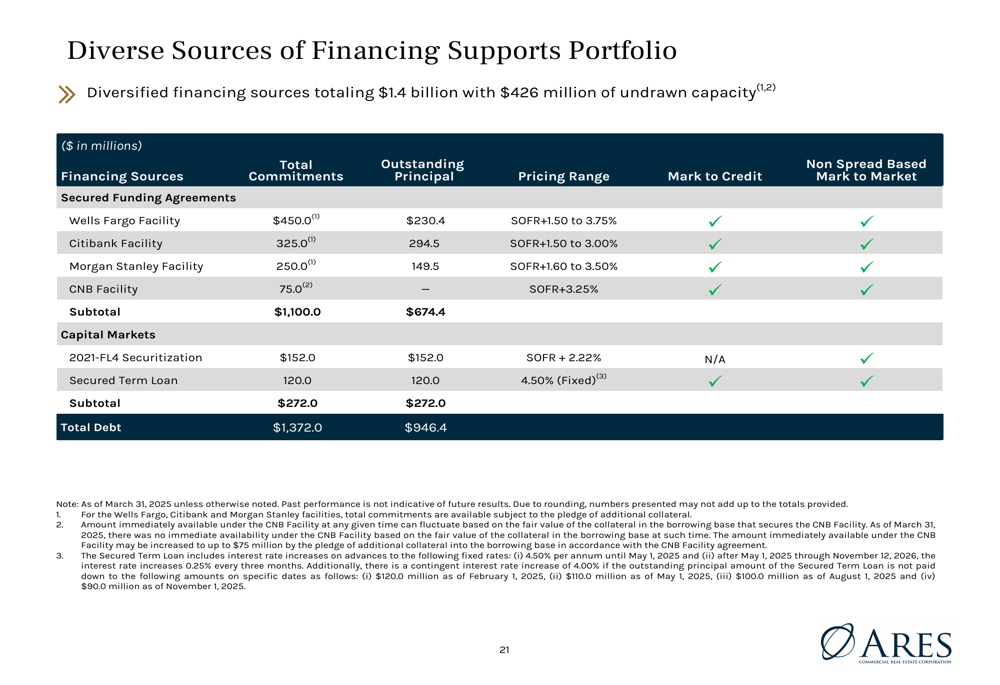

Financing Structure and Capital Management

ACRE has diversified its financing sources to support its portfolio while maintaining flexibility:

With $1.4 billion in total financing and $426 million of undrawn capacity, the company has positioned itself to navigate market challenges while pursuing strategic opportunities. The Wells Fargo facility extension provides additional stability to its capital structure.

Forward-Looking Statements

As part of Ares Management (NYSE:ARES) Corporation, a global alternative investment manager with approximately $546 billion in assets under management, ACRE benefits from the resources and expertise of its parent company. Management indicated it will continue to focus on maintaining a strong balance sheet, reducing exposure to higher-risk assets, and generating sustainable returns for shareholders.

The company’s return to profitability in Q1 2025 represents a potential turning point after the challenges faced in previous quarters. With its stock trading at $4.12 as of May 6, 2025 (with a 1.94% gain in after-hours trading), investors appear cautiously optimistic about the company’s improved performance and strategic direction.

The sustainability of ACRE’s 14.5% dividend yield will likely remain a key focus for income-oriented investors as the company continues to navigate the evolving commercial real estate landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.