AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Arrow Electronics , Inc. (NYSE:ARW) reported its second-quarter 2025 financial results on July 31, 2025, showing strong revenue growth but declining profitability metrics, which likely contributed to a significant stock price drop following the release.

Introduction & Market Context

Arrow Electronics shares fell 9.66% following the earnings presentation, despite the company reporting consolidated sales of $7.6 billion, which exceeded the high end of its guidance range. The market reaction appears to reflect concerns about margin compression and negative operating cash flow, overshadowing the robust top-line growth.

The electronic components distributor and enterprise computing solutions provider operates in a cyclical industry that appears to be showing signs of recovery, with book-to-bill ratios above parity and growing backlogs across all regions.

Quarterly Performance Highlights

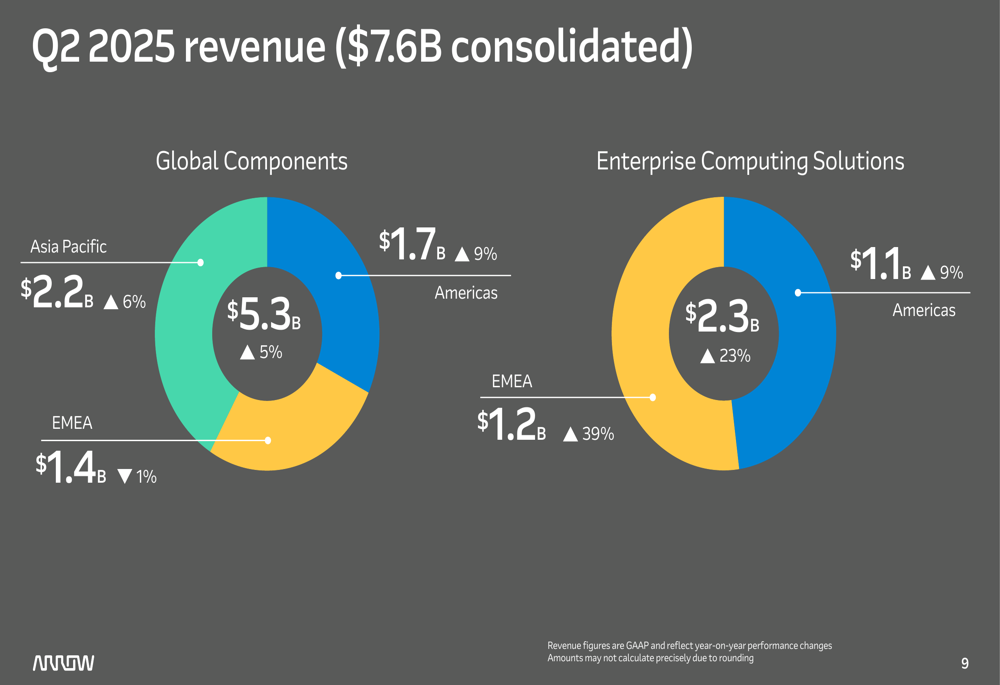

Arrow reported consolidated sales of $7.6 billion for Q2 2025, representing a 10% year-over-year increase and an 11% sequential improvement from Q1 2025. Both the Global Components and Enterprise Computing Solutions (ECS) segments exceeded guidance expectations.

As shown in the following revenue breakdown:

The Global Components segment generated $5.3 billion in revenue, up 5% year-over-year, with the Americas region leading growth at 9%. Meanwhile, the Enterprise Computing Solutions segment delivered exceptional performance with $2.3 billion in revenue, surging 23% compared to the prior year, with particularly strong growth of 39% in the EMEA region.

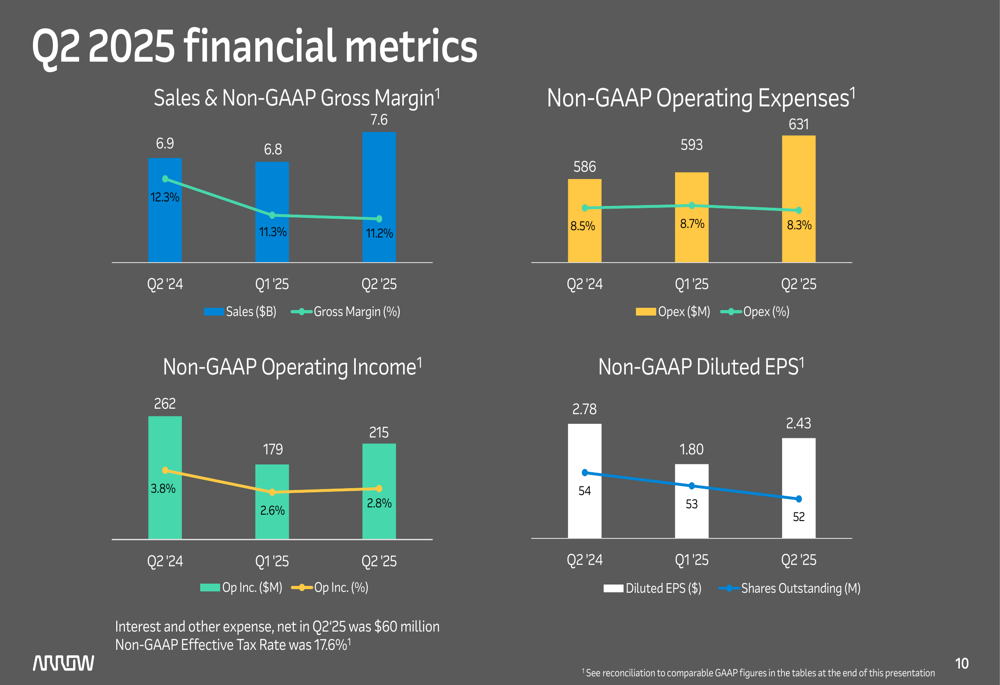

The company’s key financial metrics show revenue growth but declining profitability:

Non-GAAP operating income reached $215 million in Q2 2025, representing 2.8% of sales, down from $262 million or 3.8% in Q2 2024. Similarly, non-GAAP diluted earnings per share decreased to $2.43 from $2.78 in the prior-year period, though still above the $1.80 reported in Q1 2025.

Detailed Financial Analysis

Arrow’s gross margin compressed to 11.2% in Q2 2025, down from 12.3% in the same period last year. While the company managed to reduce operating expenses as a percentage of sales to 8.3% from 8.5% a year ago, this was not enough to offset the gross margin decline.

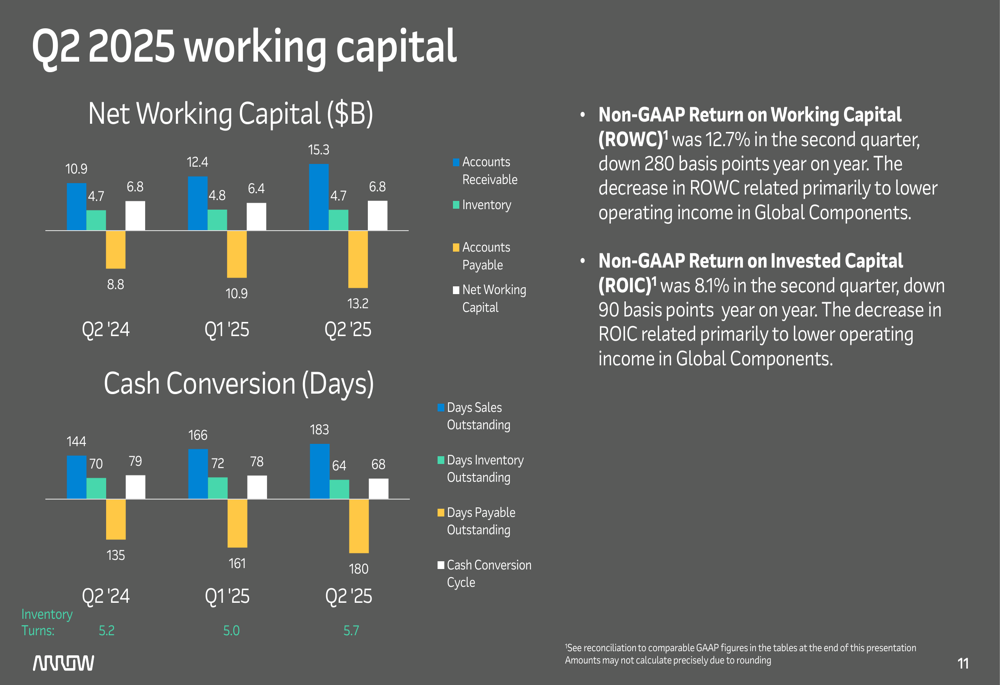

Working capital metrics showed mixed results, with inventory turns improving to 5.7 from 5.2 in Q2 2024:

However, the company’s cash flow position deteriorated significantly, with operating cash flow at negative $206 million for the quarter. This contrasts with the positive cash flow reported for seven consecutive quarters through Q1 2025, as mentioned in the previous earnings article.

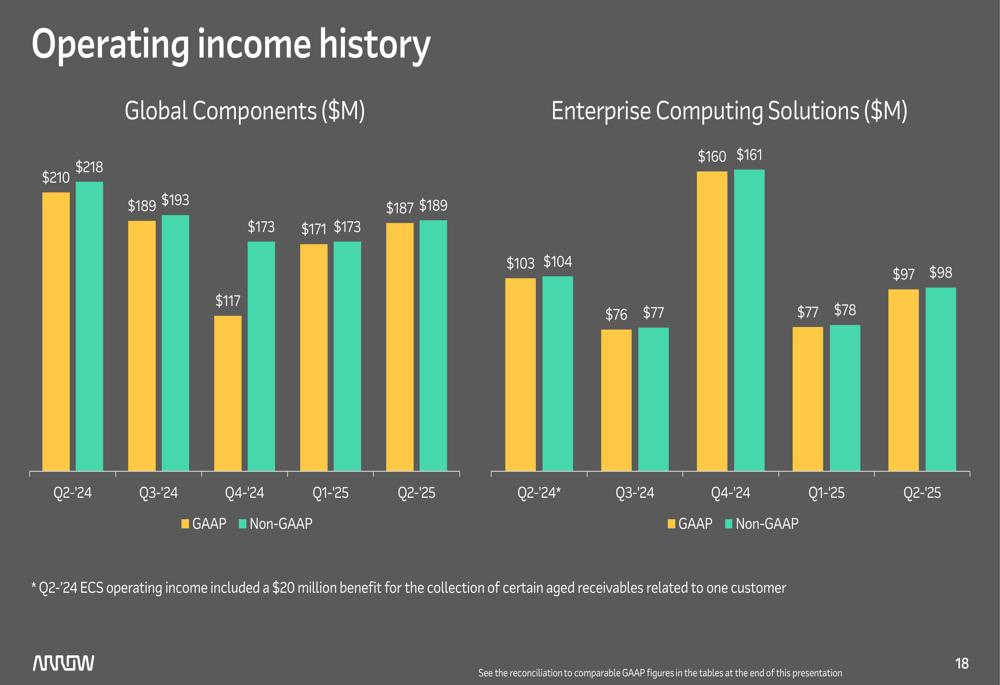

The historical operating income comparison reveals the extent of the profitability challenges facing both business segments:

Segment Performance Analysis

The Global Components business showed signs of recovery across all regions, with management noting that all three regions performed ahead of typical seasonal patterns. Industrial and Transportation markets are improving, with continued strength in IP&E (Interconnect, Passive & Electromechanical) components.

According to the presentation, leading indicators suggest continued recovery in the components business:

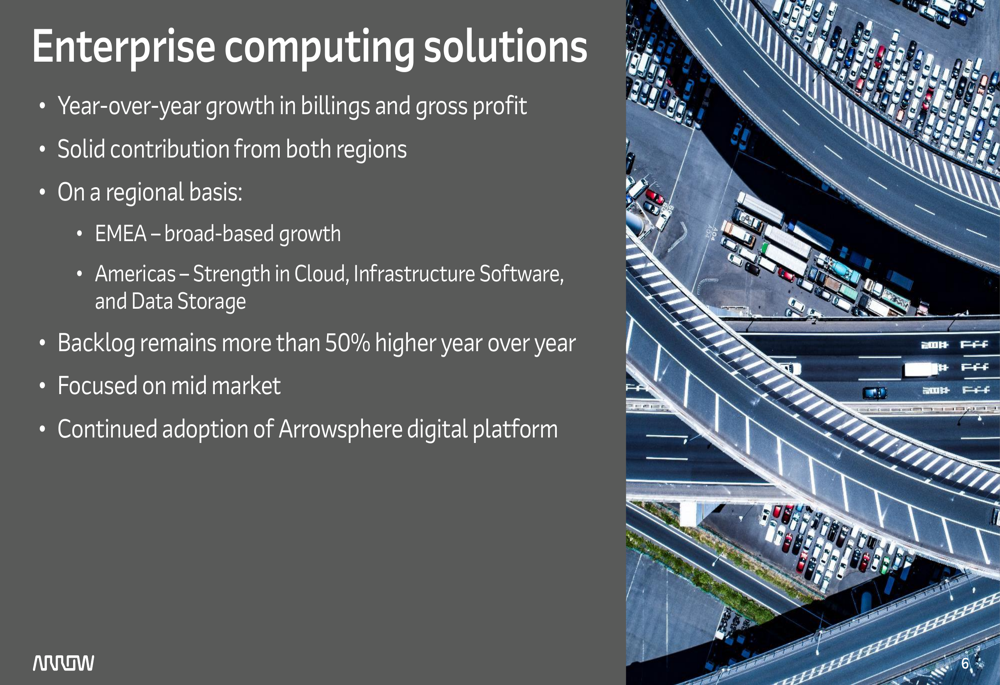

The Enterprise Computing Solutions segment delivered impressive results, with year-over-year growth in both billings and gross profit. The EMEA region showed broad-based growth, while the Americas demonstrated strength in Cloud, Infrastructure Software (ETR:SOWGn), and Data Storage. Management highlighted that backlog remains more than 50% higher year-over-year, suggesting continued momentum.

Forward-Looking Statements

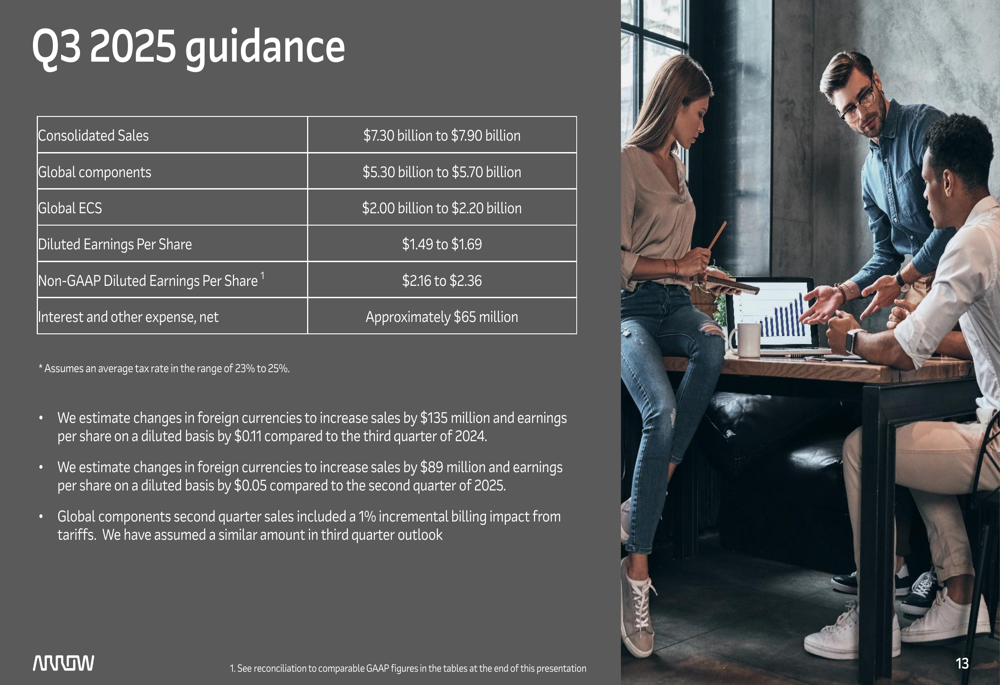

Arrow provided the following guidance for Q3 2025:

The company expects consolidated sales between $7.30 billion and $7.90 billion for Q3 2025, with Global Components sales of $5.30 billion to $5.70 billion and ECS sales of $2.00 billion to $2.20 billion. Non-GAAP diluted earnings per share is projected to be between $2.16 and $2.36.

This guidance suggests continued revenue growth but does not indicate a significant improvement in profitability metrics in the near term. Management expressed confidence in the company’s growth potential, citing alignment to attractive end markets in both segments and expectations that the cyclical recovery in Global Components will lead to better-than-seasonal sales patterns.

Conclusion

Arrow Electronics’ Q2 2025 results present a mixed picture for investors. While the company delivered strong revenue growth, particularly in its Enterprise Computing Solutions segment, the decline in profitability metrics and negative operating cash flow raise concerns about the quality of earnings.

The nearly 10% stock price drop following the earnings release suggests investors are focusing on margin compression and cash flow challenges rather than top-line growth. Looking ahead, the company’s ability to improve profitability while maintaining revenue momentum will be crucial for stock performance.

Management’s outlook remains cautiously optimistic, pointing to cyclical recovery in components and continued momentum in enterprise computing solutions. However, investors will likely need to see tangible improvements in margins and cash flow in coming quarters to regain confidence in Arrow’s long-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.