Gold prices tick higher on fresh US tariff threats, Fed rate cut hopes

Introduction & Market Context

Asana Inc . (NYSE:ASAN) recently presented its Q1 2026 investor overview, highlighting the company’s strategic focus on AI-powered coordination while reporting 10% year-over-year revenue growth. Despite the positive messaging in the presentation, Asana’s stock has experienced significant volatility, dropping 8.6% during regular trading hours and 25.54% in after-hours trading following its Q4 2025 earnings report.

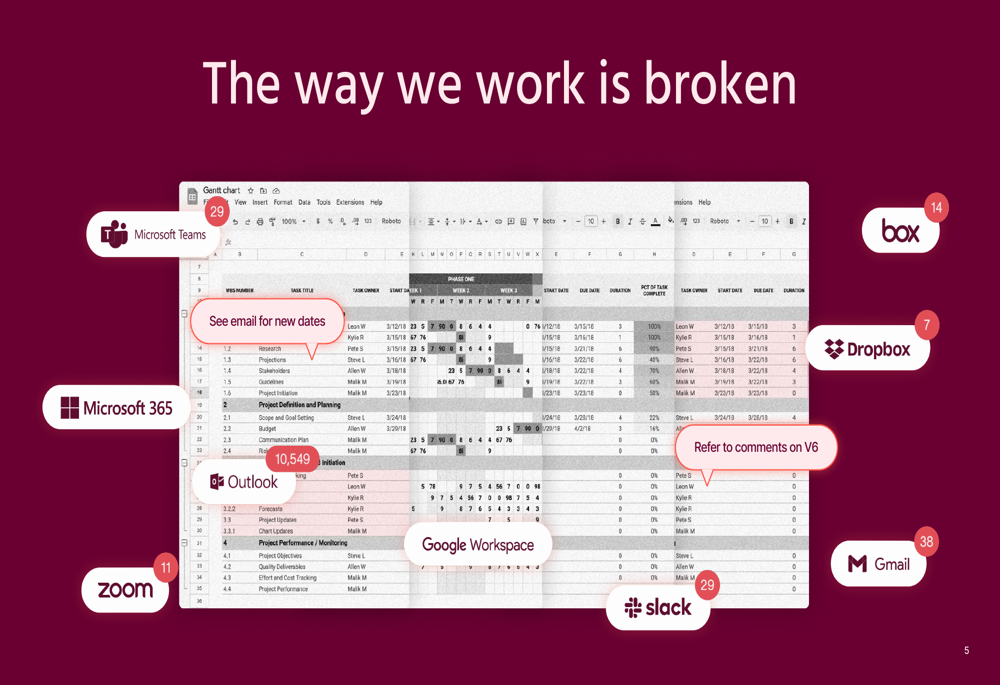

The work management platform provider continues to position itself as the solution to what it calls "the coordination tax" - the inefficiencies created by fragmented work processes across multiple applications. According to Asana’s research, 53% of knowledge workers’ time is spent on busywork, while 64% of executives struggle to track individual or team performance.

As shown in the following slide, Asana illustrates the fragmentation problem that its platform aims to solve:

Strategic Positioning and AI Focus

Asana’s presentation emphasized its position as "the platform for Human + AI Coordination," highlighting how the company fits between content tools (like Microsoft (NASDAQ:MSFT) 365 and Google (NASDAQ:GOOGL) Workspace) and communication tools (like Slack and Zoom (NASDAQ:ZM)). This strategic positioning aims to address what Asana identifies as the fundamental challenge in modern work environments.

The following slide illustrates Asana’s role as the coordination layer between content and communication tools:

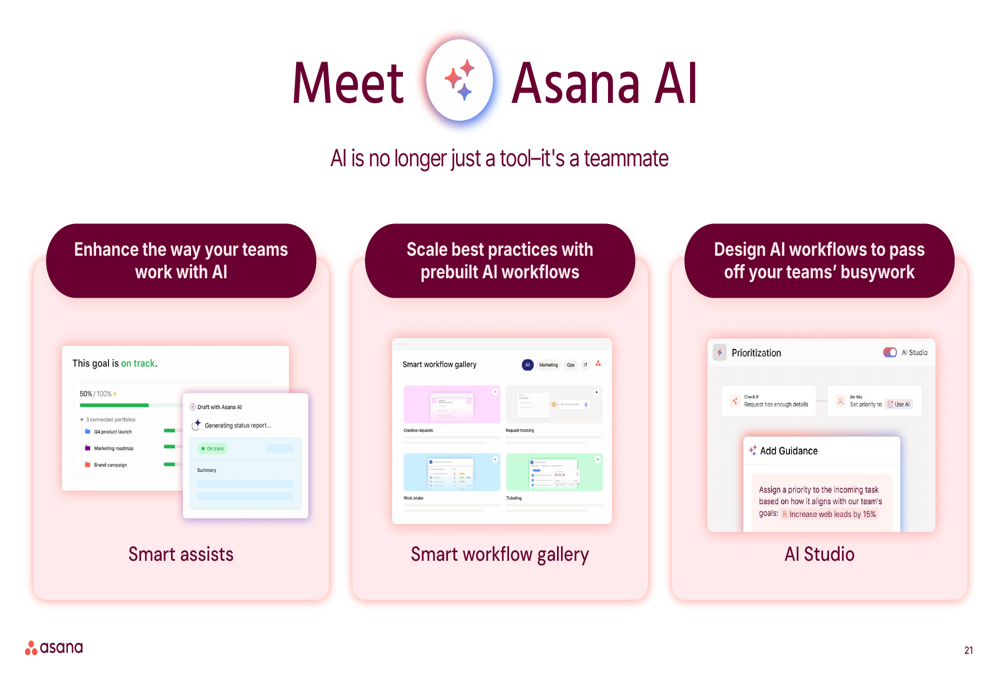

A major focus of the presentation was Asana AI, particularly the recently launched AI Studio, which exceeded $1 million in annual recurring revenue in its first quarter of general availability. The company presented AI Studio as a key differentiator that allows customers to build workflows with AI agents to automate routine tasks.

As shown in this slide, Asana is positioning its AI capabilities as a comprehensive solution for workflow automation:

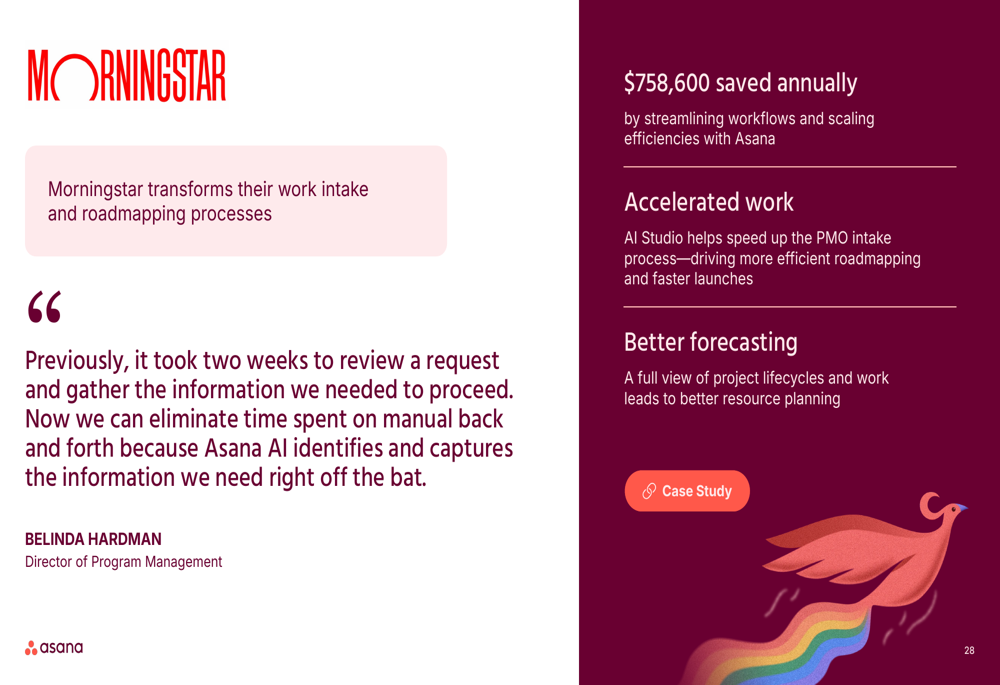

The company also highlighted early customer success stories with its AI tools. According to a testimonial from Morningstar, the financial services firm saved $758,600 annually by streamlining workflows with Asana. Similarly, Clear Channel Outdoor (NYSE:CCO) reported a 60% reduction in manual work and 69% reduction in time per request during the intake stage of its creative production process.

Financial Performance Highlights

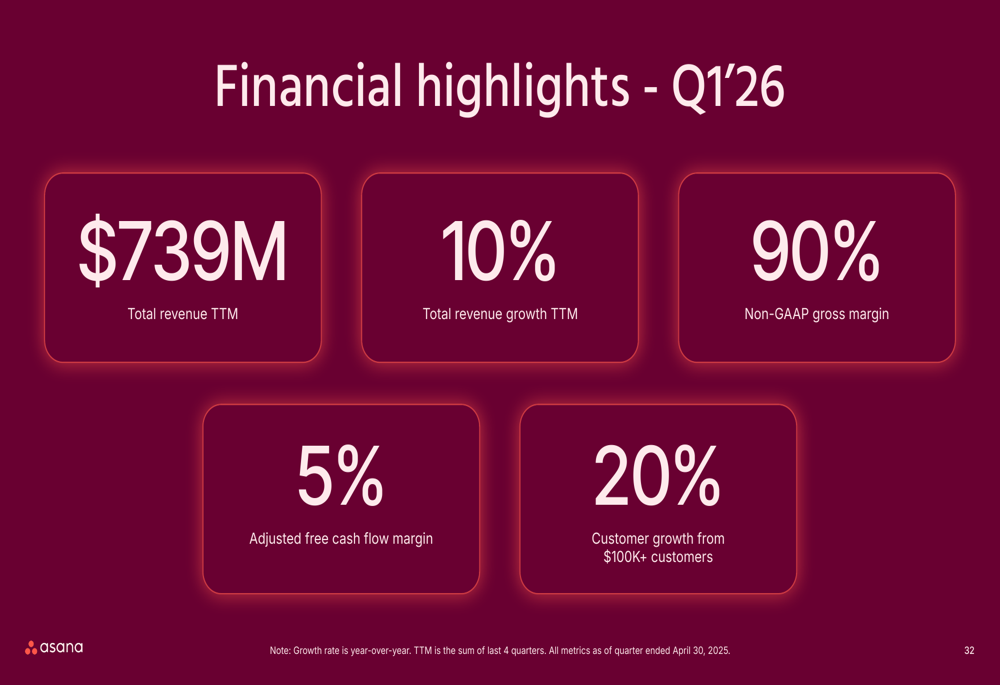

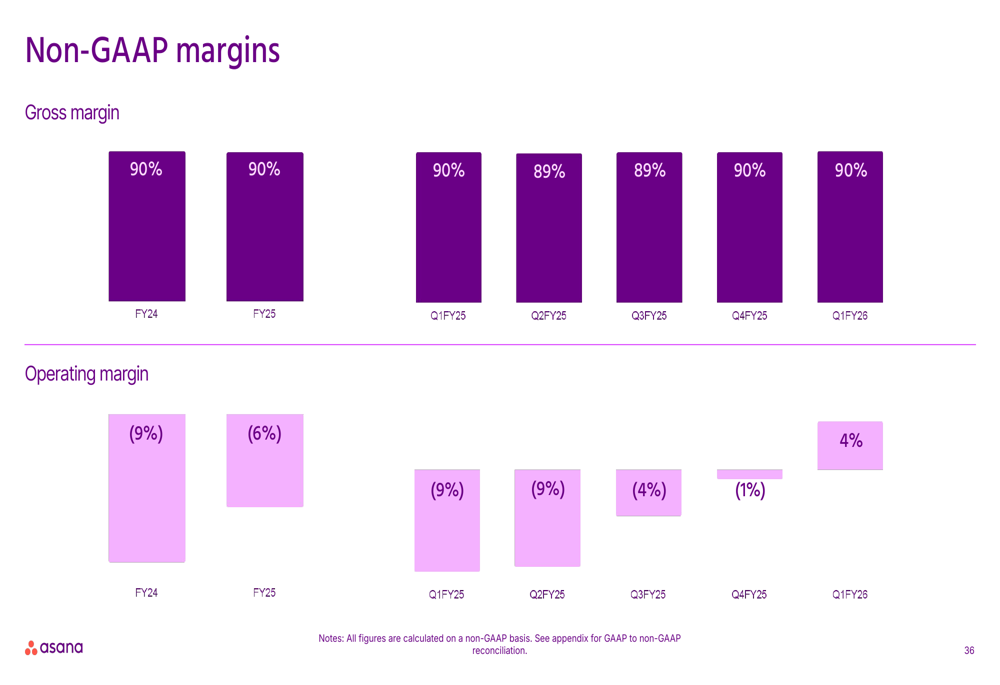

Asana reported total revenue of $739 million on a trailing twelve-month basis as of Q1 2026, representing 10% year-over-year growth. The company maintained a strong non-GAAP gross margin of 90% and achieved a 5% adjusted free cash flow margin.

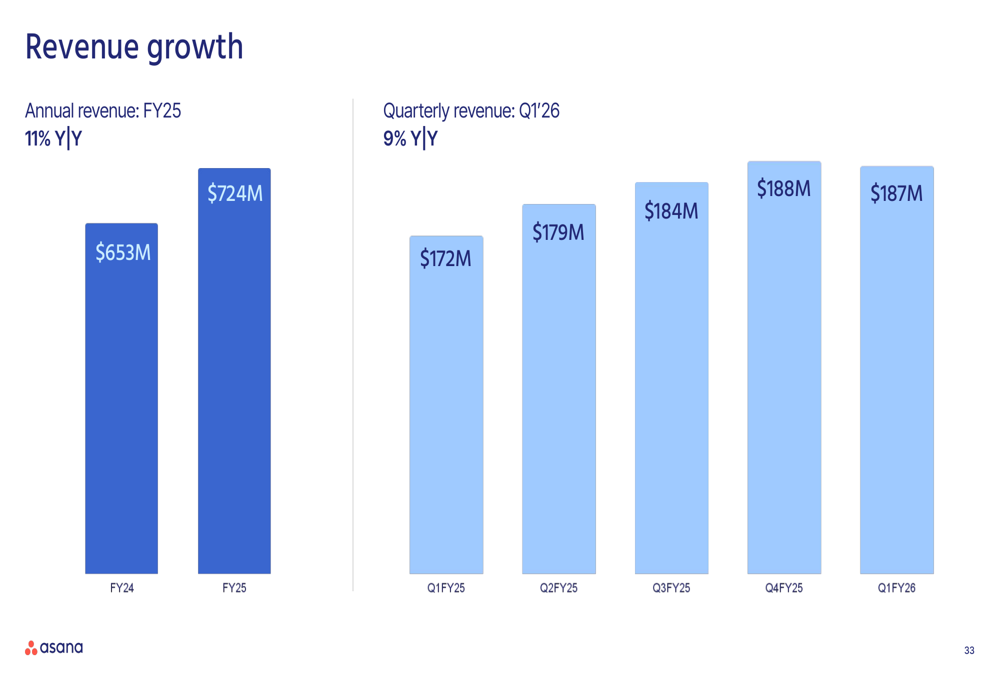

The following slide summarizes Asana’s key financial metrics:

Quarterly revenue for Q1 FY26 was $187 million, showing a slight sequential decline from Q4 FY25’s $188 million. Annual revenue for FY25 reached $724 million, up from $653 million in FY24.

A notable improvement was seen in Asana’s operating margins. The company reported a non-GAAP operating margin of 4% in Q1 FY26, compared to -9% in Q1 FY25, demonstrating significant progress toward profitability.

Customer Growth and Market Expansion

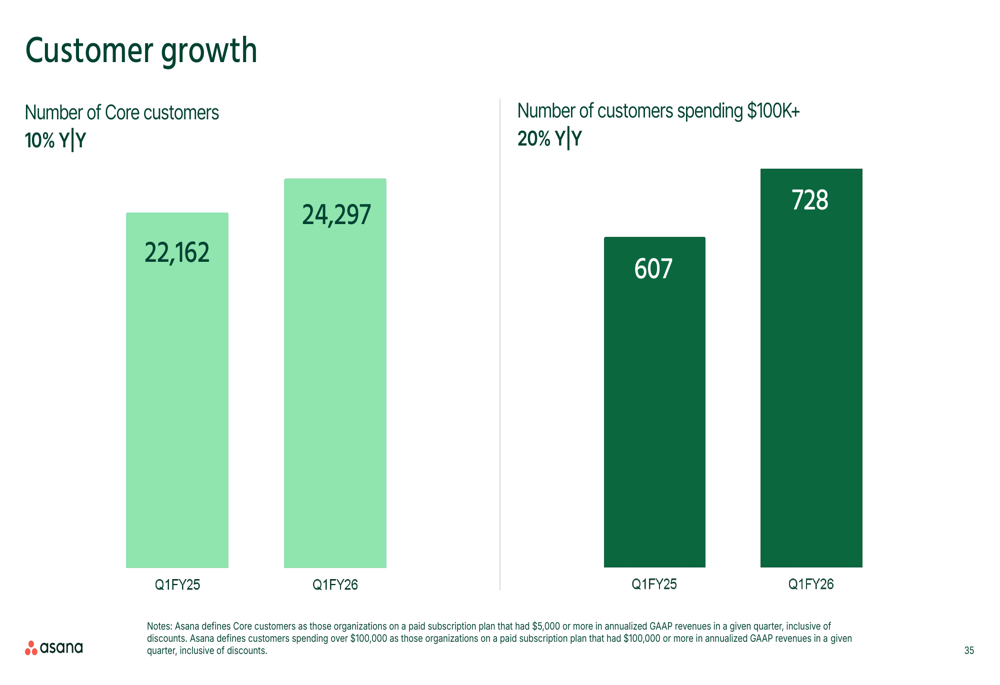

Asana reported strong customer growth metrics, particularly among high-value customers. The number of customers spending $100,000 or more annually increased by 20% year-over-year to 728 in Q1 FY26, up from 607 in Q1 FY25. The company’s total core customer base grew to 24,297, representing a 10% increase from the previous year.

The company highlighted its global footprint, serving customers in over 200 countries and territories, with 40% of revenue coming from outside the United States. Asana’s customer base includes notable companies such as Amazon (NASDAQ:AMZN), Johnson & Johnson (NYSE:JNJ), Accenture (NYSE:ACN), and Dell (NYSE:DELL).

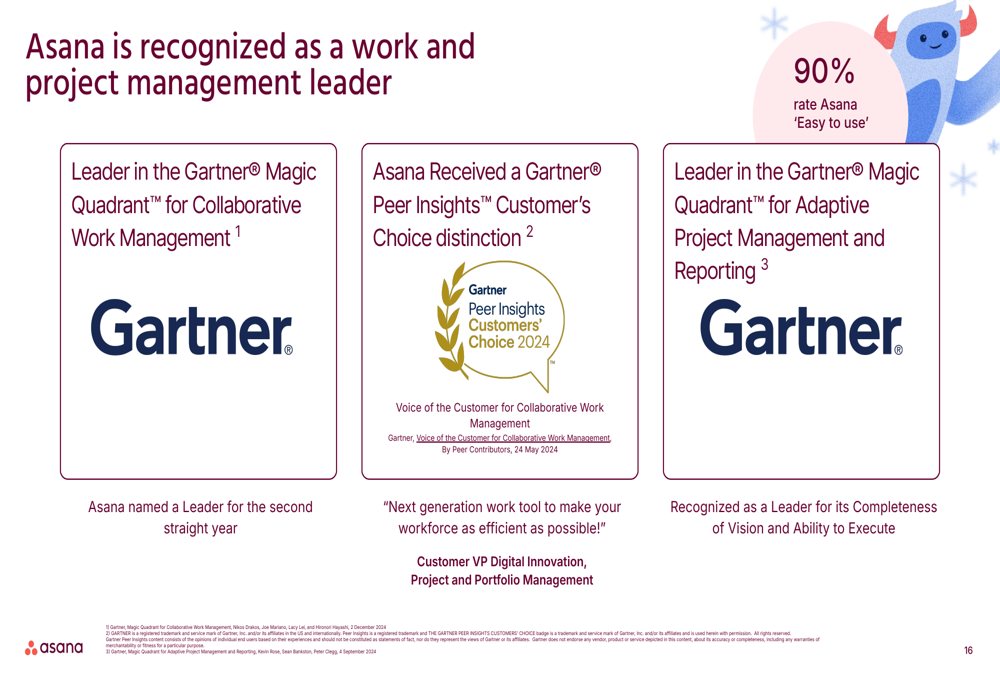

The presentation also emphasized Asana’s industry recognition, showcasing its position as a leader in the Gartner (NYSE:IT) Magic Quadrant for both Collaborative Work Management and Adaptive Project Management and Reporting.

Forward Guidance and Outlook

For Q2 FY26, Asana provided revenue guidance of $192.0-$194.0 million, representing 7-8% year-over-year growth. For the full fiscal year 2026, the company expects revenue between $775.0-$790.0 million, reflecting 7-9% growth.

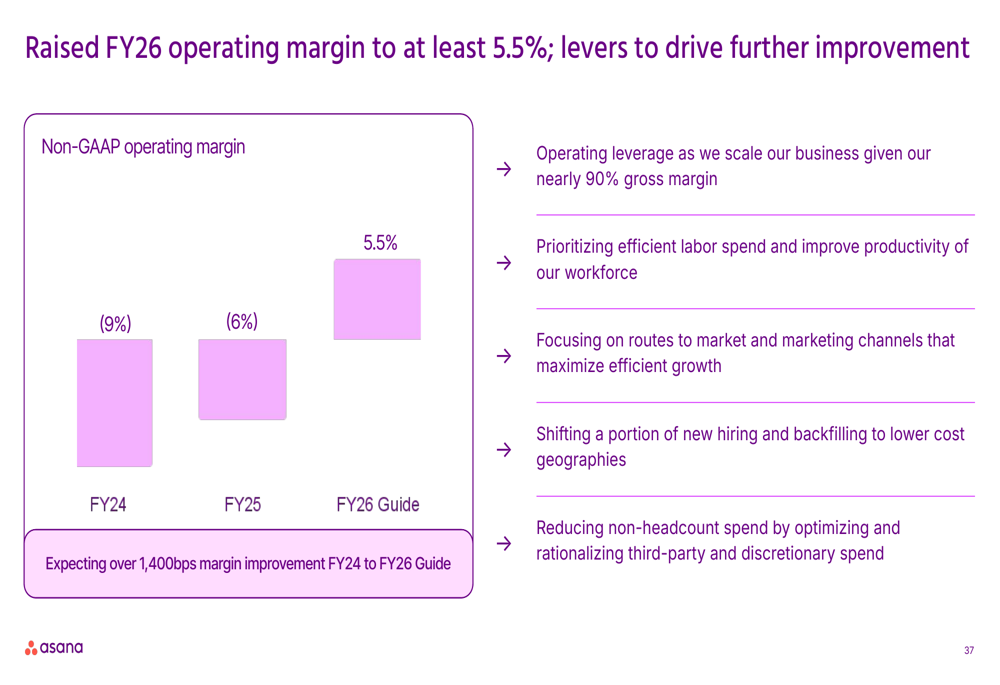

A key focus for FY26 is improving profitability, with Asana targeting a non-GAAP operating margin of at least 5.5%. The company outlined several initiatives to achieve this goal, including operating leverage, prioritizing efficient labor spend, and shifting some hiring to lower-cost geographies.

Asana also announced an expansion of its share repurchase program. In Q1 FY26, the company repurchased $15.6 million of Class A common stock (1.0 million shares). In May 2025, Asana’s board increased the share repurchase authorization by $100 million and removed the program’s previous expiration date, bringing the total available for future repurchases to $156 million.

Looking ahead, Asana identified three key priorities to drive growth and retention: customer health, customer acquisition, and customer value. The company expects these initiatives to lead to long-term acceleration in growth and improvement in net revenue retention.

Despite the optimistic outlook presented in the investor slides, market reaction suggests investors remain cautious about Asana’s growth trajectory and path to profitability. The company’s focus on AI capabilities represents a strategic bet on differentiation in an increasingly competitive work management software market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.