S&P, Nasdaq edge higher with gold spike, FOMC minutes in focus

Introduction & Market Context

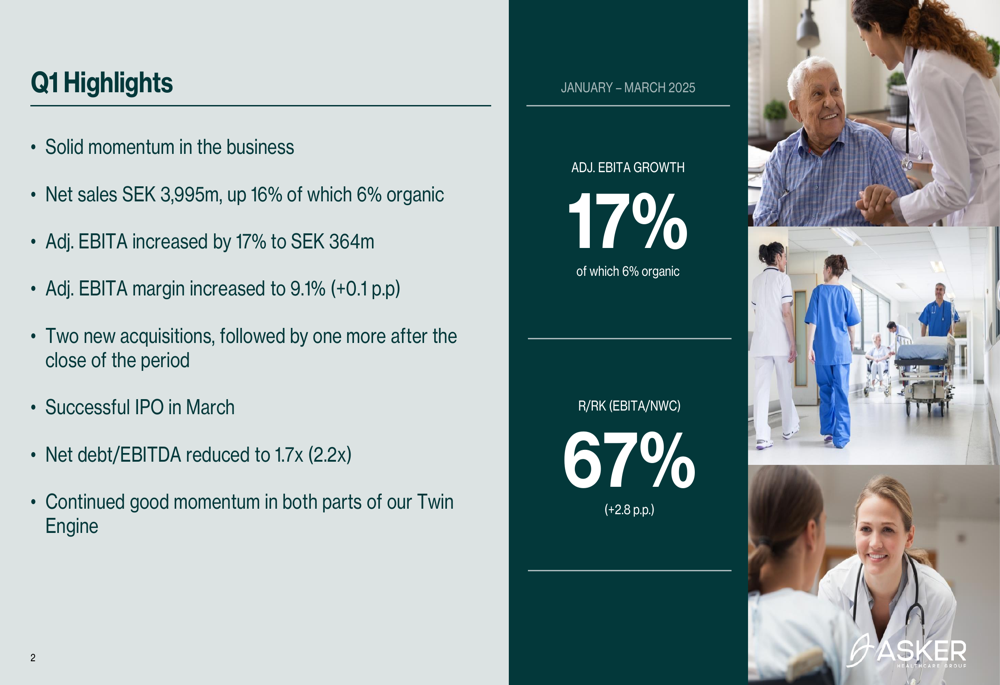

Asker Healthcare Group AB (NASDAQ:ASKR) reported a strong start to 2025, with double-digit growth in both sales and adjusted EBITA for the first quarter. The company’s Q1 2025 presentation, delivered by CEO Johan Falk and CFO Thomas Moss on May 13, highlighted continued momentum in Asker’s twin-engine growth strategy combining organic development with strategic acquisitions.

The healthcare distributor, which recently completed its IPO in March 2025, demonstrated resilience in a competitive European healthcare market. With its stock trading near SEK 100.44 as of July 21, 2025, up 0.47% and approaching its 52-week high of SEK 111.88, investor confidence appears strong following these results.

Quarterly Performance Highlights

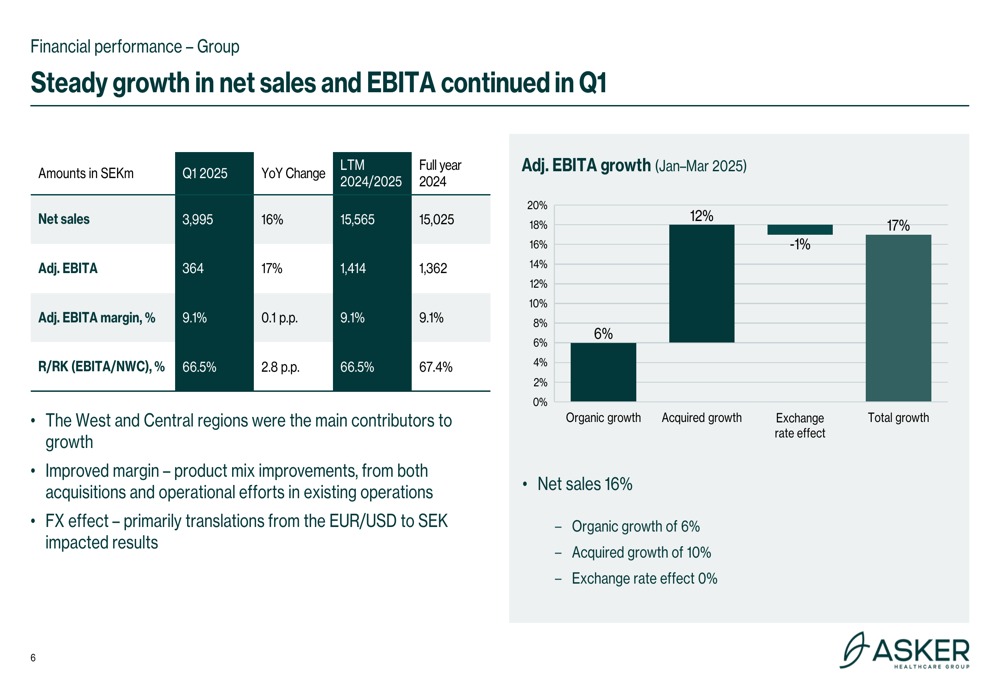

Asker Healthcare reported net sales of SEK 3,995 million for Q1 2025, representing a 16% increase compared to the same period last year. This growth was driven by 6% organic growth and 10% acquired growth, with minimal impact from exchange rate fluctuations.

Adjusted EBITA rose 17% to SEK 364 million, with organic growth contributing 6%, acquisitions adding 12%, and a slight negative impact (-1%) from exchange rates. The adjusted EBITA margin improved slightly to 9.1%, up 0.1 percentage points year-over-year, as the company continues its progress toward its medium-term target of exceeding 10%.

As shown in the following comprehensive overview of Q1 2025 results:

The company’s return on risked capital (R/RK), measured as EBITA divided by net working capital, improved to 66.5%, an increase of 2.8 percentage points. This metric significantly exceeds Asker’s target of greater than 50%, demonstrating efficient capital utilization.

Acquisition Strategy

Asker Healthcare’s growth strategy continues to be heavily focused on acquisitions, with two completed during Q1 2025 and another following the close of the period. Over the last twelve months, the company has completed 12 acquisitions with combined annual sales of SEK 1,820 million, significantly expanding its international footprint.

The acquisition details are illustrated in this comprehensive overview:

The most significant Q1 acquisition was Hospital Services Limited (HSL), a leading provider of medical equipment, supplies, maintenance, and digital health solutions serving healthcare providers in Ireland and the UK. With annual sales of SEK 800 million and 150 full-time employees, HSL represents an important platform for Asker’s continued growth in the region.

The following image highlights the strategic importance of the HSL acquisition:

Regional Performance Analysis

Asker Healthcare’s performance varied across its three business regions, with the West and Central areas showing particularly strong growth while the North region experienced a slight decline in profitability.

The West region, which includes the UK, Ireland, and the Netherlands, delivered impressive results with sales increasing 19% to SEK 2,008 million and adjusted EBITA surging 35% to SEK 161 million. The adjusted EBITA margin improved by 1.0 percentage point to 8.0%. This strong performance was driven by high organic growth from increased patient numbers and efficiency gains from closer cooperation between homecare companies.

The Central region, covering Germany, Switzerland, and other central European markets, posted the highest growth rates with sales up 37% to SEK 725 million and adjusted EBITA jumping 75% to SEK 54 million. The adjusted EBITA margin improved significantly by 1.6 percentage points to 7.5%, driven by both acquisitions and improved product mix.

The North region, which includes the Nordic countries, saw more modest growth with sales increasing 2% to SEK 1,263 million, while adjusted EBITA declined 2% to SEK 177 million. Despite this slight decrease, the North region maintains the highest profitability with an adjusted EBITA margin of 14.0%.

The following chart illustrates the Group’s overall financial performance:

Financial Position

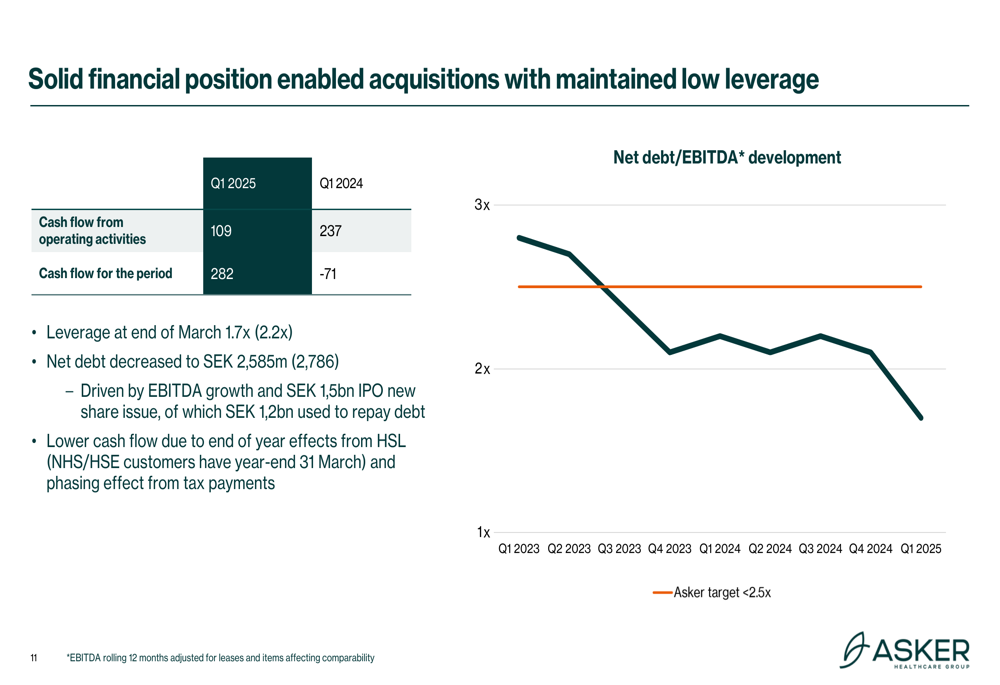

Asker Healthcare significantly strengthened its financial position during Q1 2025, primarily due to its successful IPO in March. Net debt decreased to SEK 2,585 million (down from SEK 2,786 million), with the company using SEK 1.2 billion from the IPO proceeds of SEK 1.5 billion to repay debt.

The company’s leverage ratio, measured as net debt to EBITDA, improved to 1.7x from 2.2x previously, well below the target ceiling of 2.5x. This reduced leverage provides Asker with additional financial flexibility for future acquisitions.

Cash flow from operating activities decreased to SEK 109 million in Q1 2025 compared to SEK 237 million in Q1 2024. The company attributed this decline to end-of-year effects from HSL, as National Health Service (NHS) and Health Service Executive (HSE) customers in the UK and Ireland have a March 31 fiscal year-end, as well as phasing effects from tax payments.

The following chart demonstrates Asker’s improved financial position and reduced leverage:

Forward-Looking Statements

Looking ahead, Asker Healthcare expressed confidence in its ability to continue delivering steady growth. The company has achieved a last-twelve-months adjusted EBITA growth of 22%, well above its target of greater than 15%, and management indicated that the acquisition pipeline remains strong.

CEO Johan Falk emphasized the company’s position in market consolidation, supported by its entrepreneurs, acquisition pipeline, and twin-engine strategy. The development of a new distribution center in Gothenburg is proceeding as planned, which should further enhance operational efficiency in the North region.

As summarized in the company’s Q1 overview:

With its solid balance sheet, reduced leverage, and demonstrated ability to identify and integrate strategic acquisitions, Asker Healthcare appears well-positioned to continue its growth trajectory. The company’s focus on improving patient outcomes while reducing the total cost of care aligns with broader healthcare trends across Europe, potentially providing tailwinds for future growth.

While the company faces challenges including slight underperformance in its North region and lower cash flow from operations, its overall financial health and strategic direction suggest continued momentum as it progresses through 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.