Bitcoin price today: dips below $112k, near 6-wk low despite Fed cut bets

Introduction & Market Context

Aspen Aerogels (NYSE:ASPN) presented its Q1 2025 financial results on May 8, revealing a significant $301.2 million net loss primarily driven by a $286.6 million impairment charge on property, plant, and equipment. The company’s stock, which has already fallen from $9.40 after Q4 2024 results to $5.69 at the previous close, faced additional pressure with premarket trading showing a further 10.54% decline to $5.09.

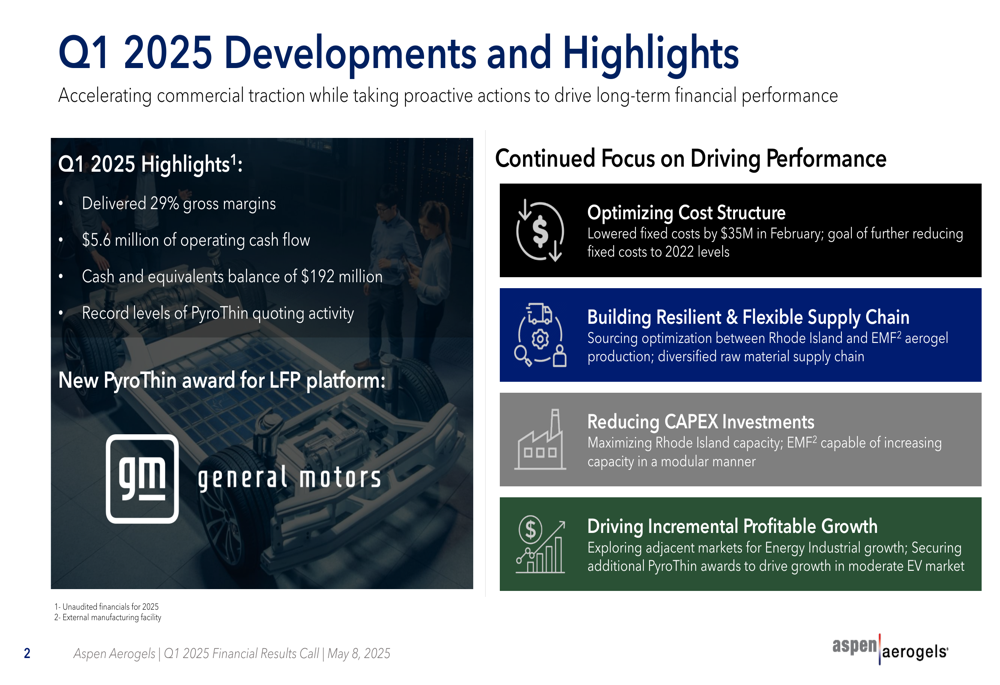

Despite the headline loss, management emphasized progress on cost structure optimization and highlighted positive developments including a new PyroThin award from General Motors (NYSE:GM) and improved operating cash flow of $5.6 million, reversing the previous year’s negative cash flow.

Quarterly Performance Highlights

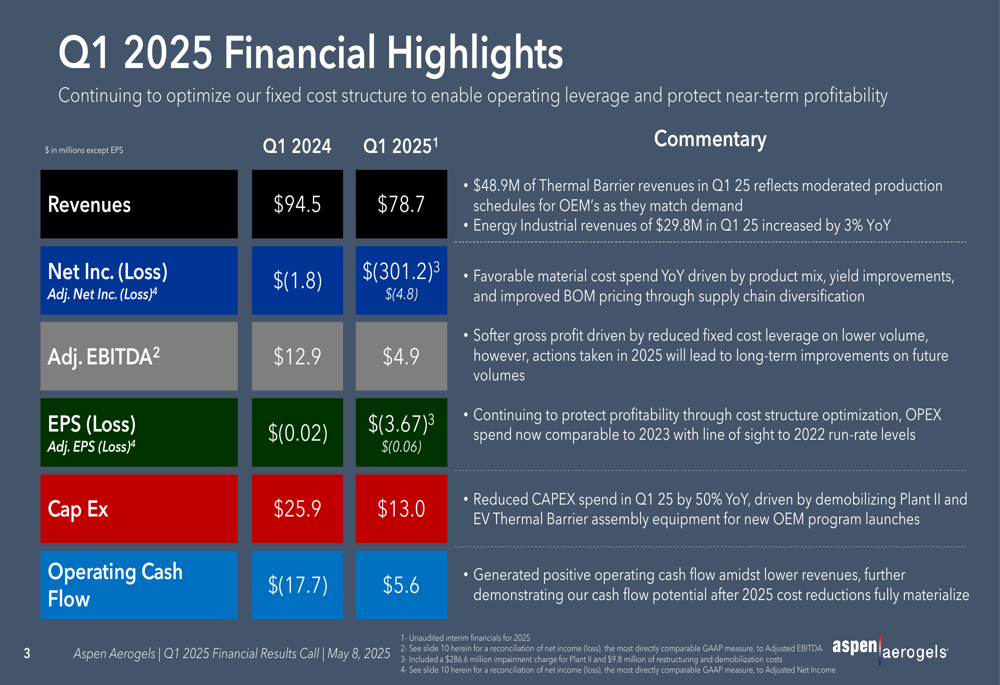

Aspen Aerogels reported Q1 2025 revenue of $78.7 million, a decline from $94.5 million in Q1 2024. While overall revenue decreased, the Energy Industrial segment showed modest growth of 3% year-over-year, reaching $29.8 million. Thermal Barrier revenue, the company’s largest segment, came in at $48.9 million.

The company achieved a 29% gross margin and generated $5.6 million in operating cash flow, a significant improvement from the negative $17.7 million in the same period last year. Adjusted EBITDA was $4.9 million, down from $12.9 million in Q1 2024.

As shown in the following financial highlights:

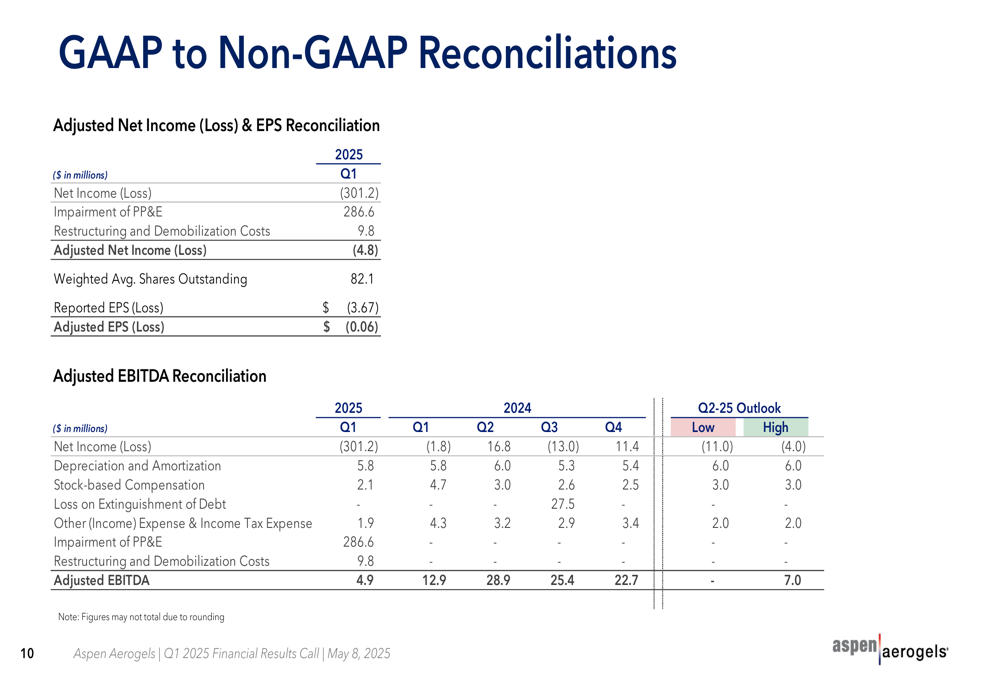

The massive net loss of $301.2 million was primarily attributable to a $286.6 million impairment of property, plant, and equipment, along with $9.8 million in restructuring and demobilization costs. Excluding these charges, the adjusted net loss was $4.8 million, or $(0.06) per share.

Capital expenditures decreased to $13.0 million from $25.9 million in Q1 2024, reflecting the company’s more disciplined approach to investments. The company maintained a strong cash position with $192 million in cash and equivalents.

Strategic Initiatives

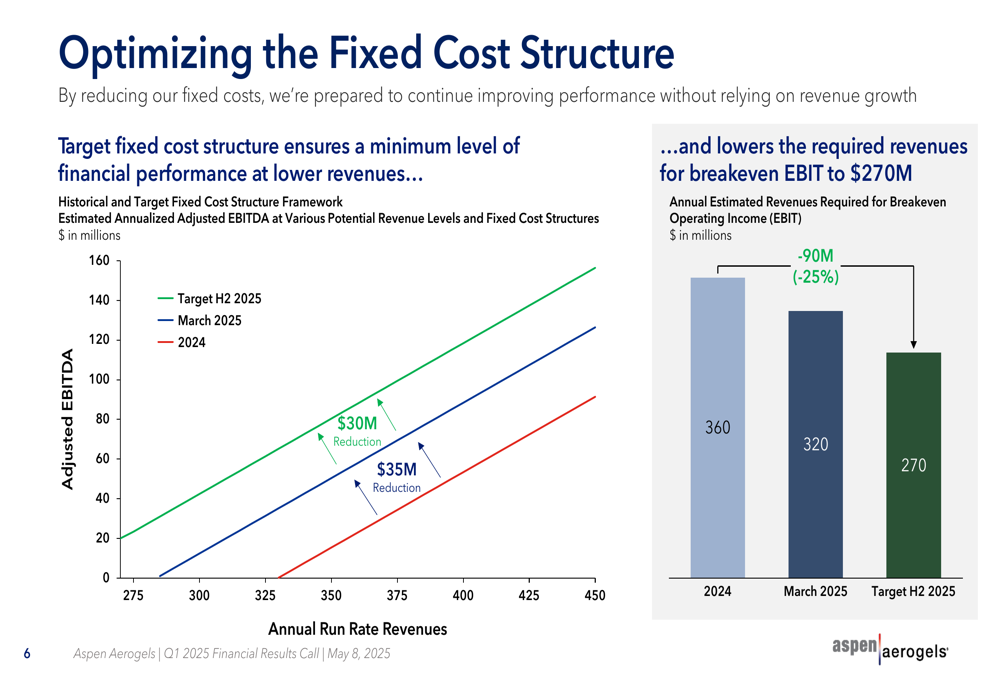

Aspen Aerogels is implementing an aggressive cost optimization strategy, having reduced fixed costs by $35 million. This restructuring aims to lower the revenue threshold required for profitability from $360 million to $270 million by the second half of 2025, representing a 25% reduction.

The following chart illustrates how these cost structure changes impact profitability at various revenue levels:

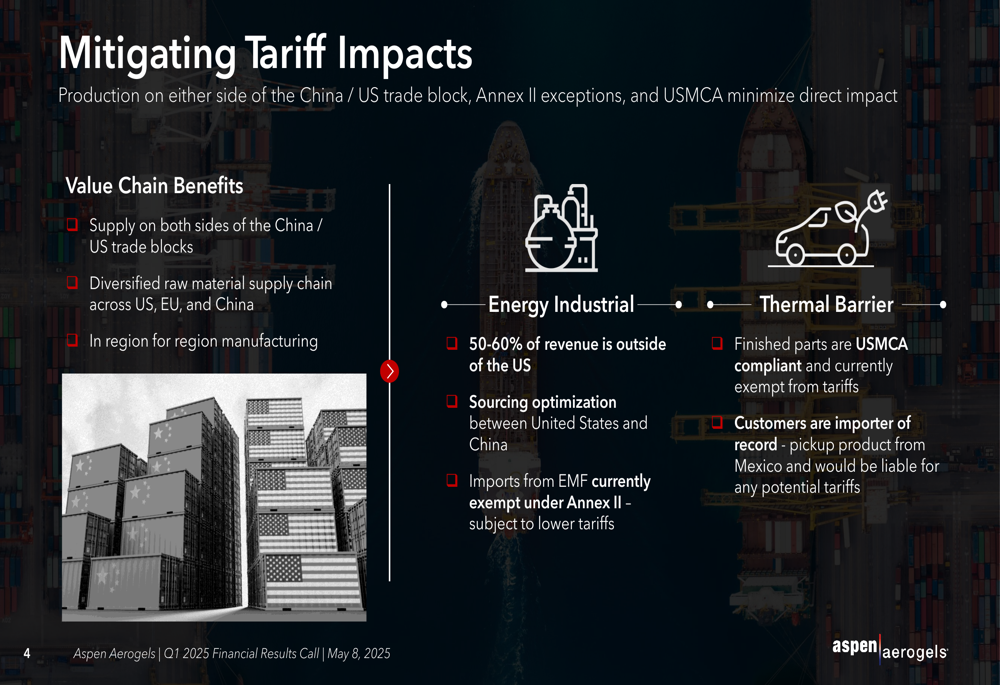

The company is also actively working to mitigate potential tariff impacts by diversifying its supply chain across the US, EU, and China. For its Thermal Barrier business, finished parts are currently USMCA compliant and exempt from tariffs, with customers serving as the importer of record. The Energy Industrial segment benefits from having 50-60% of revenue outside the US and sourcing optimization between manufacturing locations.

As shown in the following tariff mitigation strategy:

Competitive Industry Position

The presentation highlighted shifting dynamics in the US electric vehicle market, with General Motors and Honda (NYSE:HMC) capturing approximately 16.6% of all US EV sales year-to-date in 2025. GM’s Ultium platform, which uses Aspen’s thermal barriers, has seen 227% growth in sales. Meanwhile, Tesla (NASDAQ:TSLA) has experienced an 8% decline in its US sales.

The following market update illustrates these changing competitive positions:

Despite some near-term adjustments, particularly an 18% projected volume reduction in GM’s EV forecast for 2025, the long-term outlook remains positive. Global EV production is projected to increase at a 17% CAGR through 2030, with North America and Europe expected to grow at a more robust 25% CAGR.

Aspen Aerogels secured a new PyroThin award for GM’s LFP platform, adding to its existing relationships with major automotive manufacturers. The company is focusing on expanding into adjacent markets to drive incremental growth in its Energy Industrial segment.

Forward-Looking Statements

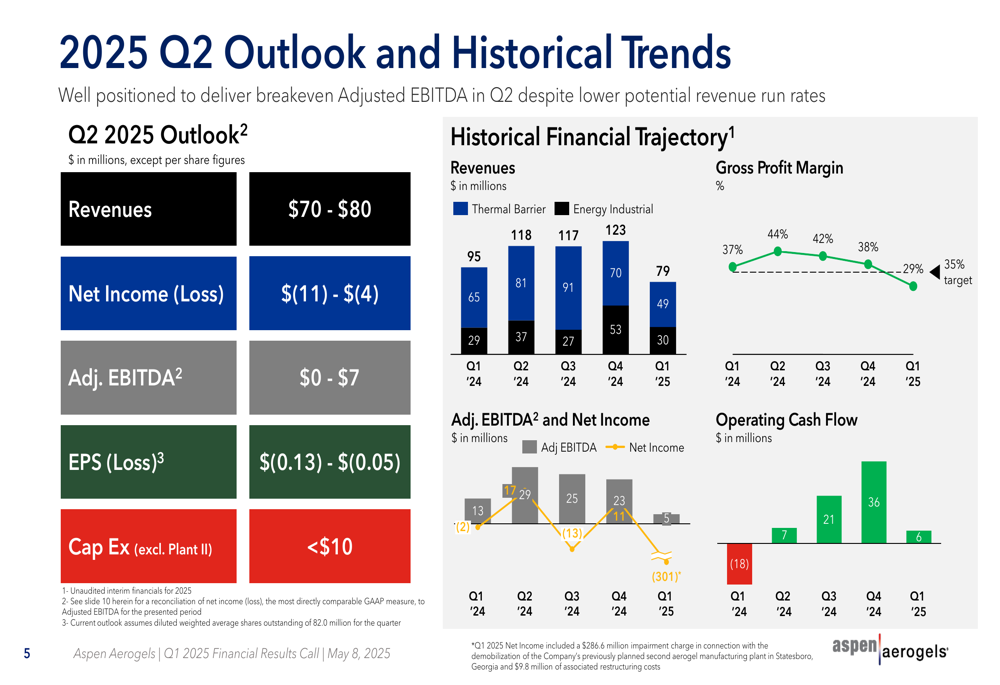

For Q2 2025, Aspen Aerogels provided guidance of:

- Revenue between $70-80 million

- Net loss between $(11)-$(4) million

- Adjusted EBITDA between $0-7 million

- EPS loss between $(0.13)-$(0.05)

- Capital expenditures below $10 million (excluding Plant II)

The quarterly outlook and historical trends are visualized in the following chart:

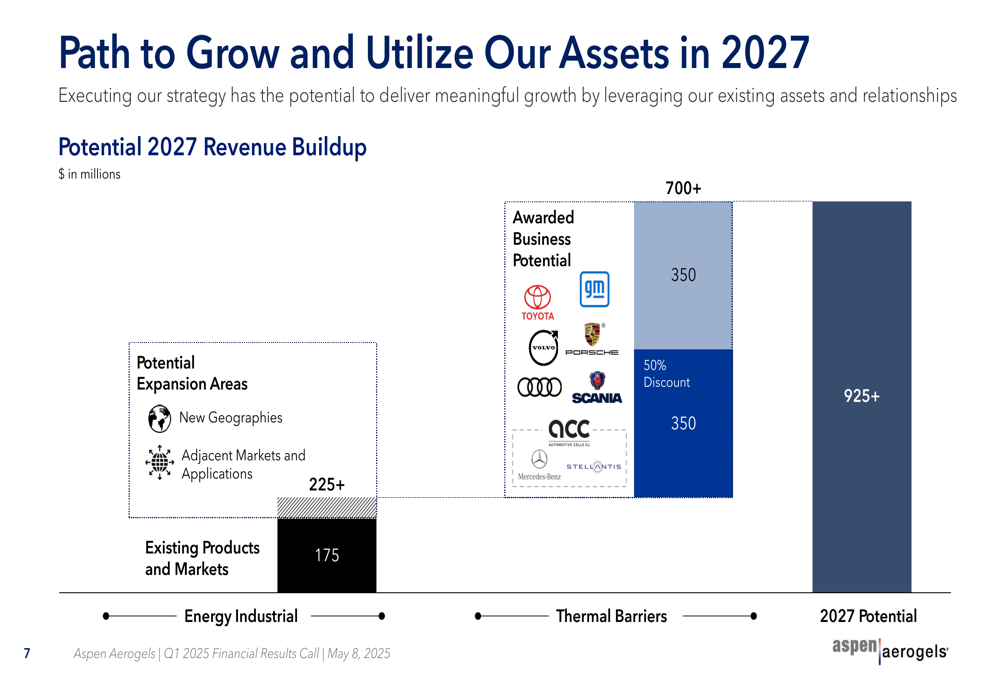

Looking further ahead, management outlined a path to potential 2027 revenue of $925+ million, comprised of $700+ million from awarded business (applying a 50% discount factor), $175 million from existing products and markets, and $225+ million from expansion opportunities.

The following chart illustrates this potential revenue buildup:

Detailed Financial Analysis

The significant impairment charge of $286.6 million represents a material write-down of the company’s assets, likely related to production facilities. This non-cash charge, combined with restructuring costs, dramatically affected the bottom line but doesn’t impact the company’s operational cash flow, which improved year-over-year.

The reconciliation between GAAP and non-GAAP measures provides additional context for understanding the company’s underlying performance:

The company’s focus on cost structure optimization appears to be yielding results, with gross margins at 29% despite lower revenue. Management indicated that favorable material costs year-over-year were driven by product mix, yield improvements, and improved BOM pricing through supply chain diversification.

Conclusion

Aspen Aerogels faces significant near-term challenges, as evidenced by the substantial impairment charge and declining revenue. However, the company is taking decisive action to optimize its cost structure, strengthen its supply chain, and position itself for long-term growth in the evolving EV market.

The success of these initiatives will depend on the company’s ability to execute its cost reduction plans, secure additional thermal barrier contracts, and effectively navigate potential tariff and trade challenges. While management has outlined an ambitious path to nearly $1 billion in revenue by 2027, investors appear cautious given the current financial performance and broader market uncertainties in the EV sector.

The company’s summary of key focus areas highlights its strategic priorities:

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.