IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

Aspo Oyj (HEL:ASPO) reported strong first-quarter results for 2025, with sales growing 13.9% despite challenging market conditions in Europe. The Finnish conglomerate saw its stock price rise 6.72% to €5.40 following the presentation on May 12, as investors responded positively to improved profitability across all business segments.

The company’s Q1 performance demonstrates successful execution of its strategic priorities, with acquisitions driving growth in Telko and Leipurin, while ESL Shipping improved profitability through operational adjustments despite weak market demand.

"Strong start for year 2025 with continued profitability improvement," stated CEO Rolf Jansson in the presentation, highlighting the company’s focus on maximizing benefits from acquisitions and organic growth initiatives.

Quarterly Performance Highlights

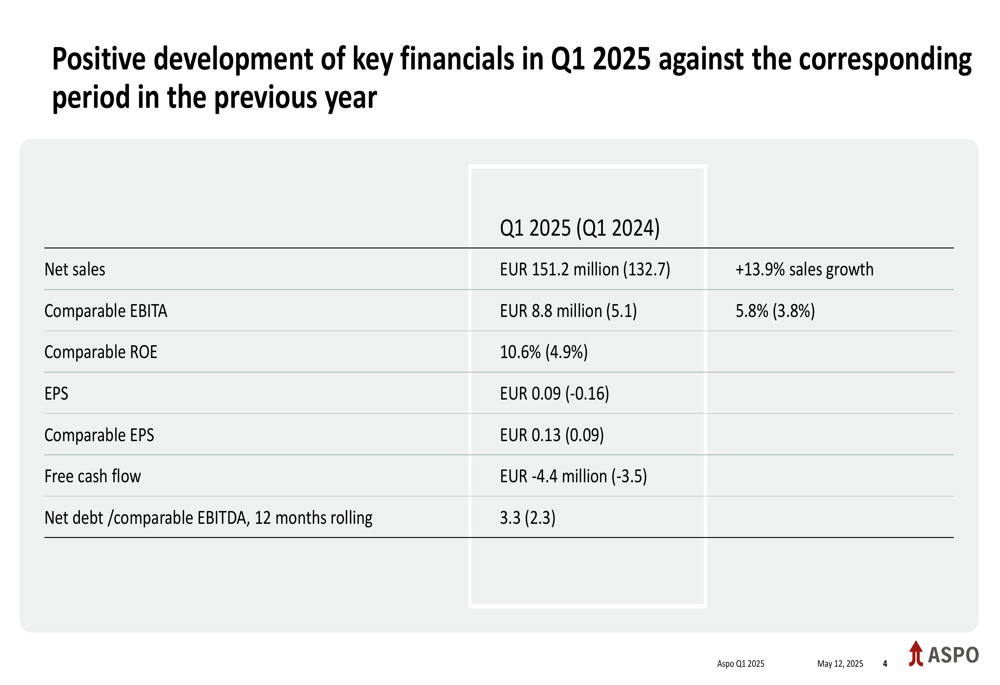

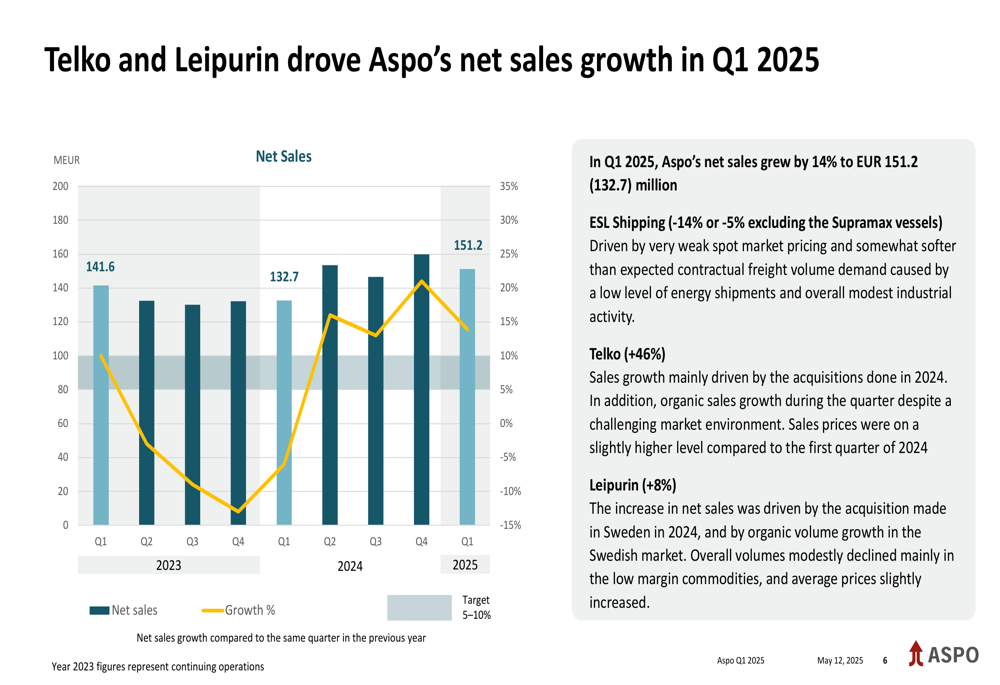

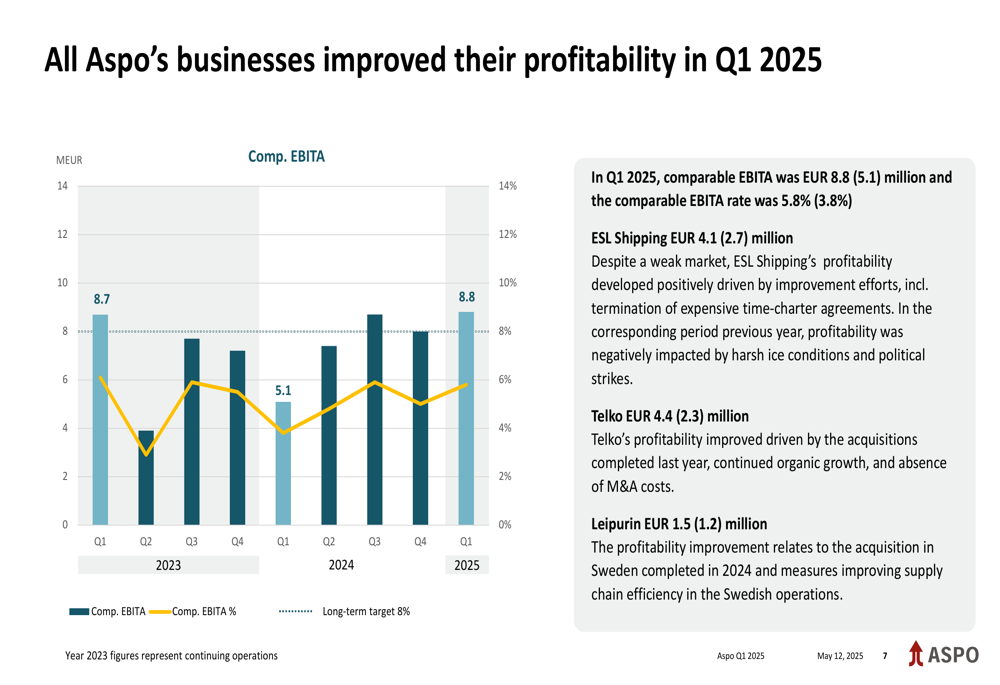

Aspo’s net sales increased to €151.2 million in Q1 2025, up 13.9% from €132.7 million in the same period last year. Comparable EBITA rose significantly to €8.8 million from €5.1 million, with the margin expanding to 5.8% from 3.8%.

As shown in the following chart of key financial metrics:

The company’s comparable return on equity improved to 10.6% from 4.9%, while earnings per share turned positive at €0.09 compared to -€0.16 in Q1 2024. Comparable EPS increased to €0.13 from €0.09.

Growth was primarily driven by Telko and Leipurin, which offset a decline in ESL Shipping’s sales. Telko’s sales grew by an impressive 46%, while Leipurin achieved 8% growth. ESL Shipping’s sales decreased by 14%, or 5% when excluding Supramax vessels.

The following chart illustrates the sales growth trajectory:

All three business segments improved their profitability compared to Q1 2024:

"Aspo’s businesses improved profitability despite challenging market conditions with low industrial activity and demand in Europe," noted CFO Erkka Repo during the presentation.

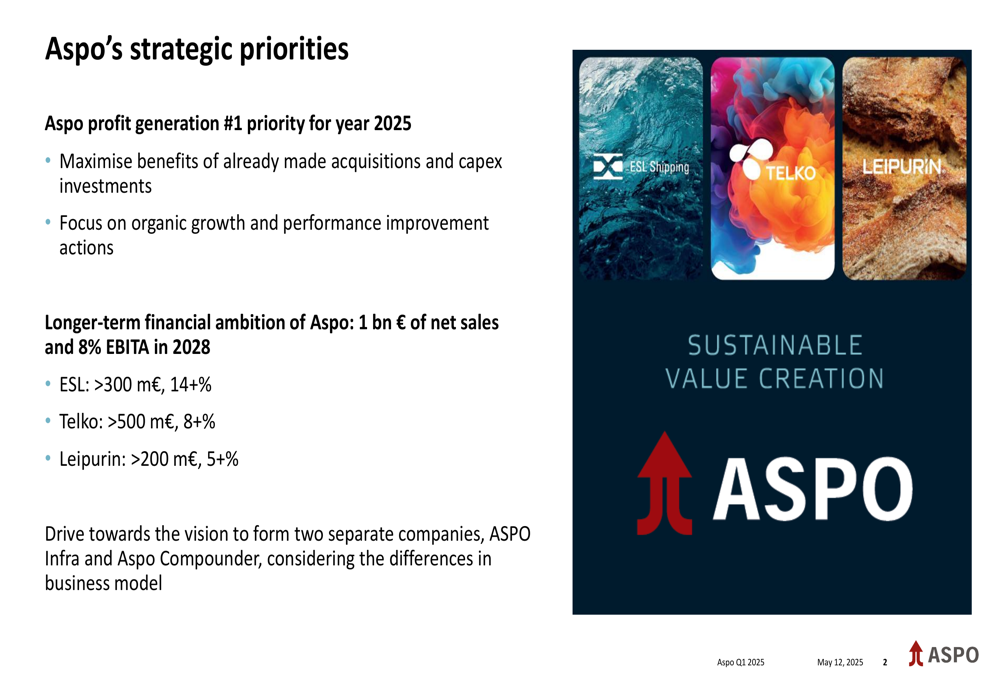

Strategic Initiatives

Aspo continues to execute its strategic vision of forming two separate companies - ASPO Infra and ASPO Compounder - while targeting €1 billion in net sales and 8% EBITA by 2028.

The company’s strategic priorities for 2025 focus on profit generation through maximizing benefits from acquisitions and capital expenditure investments:

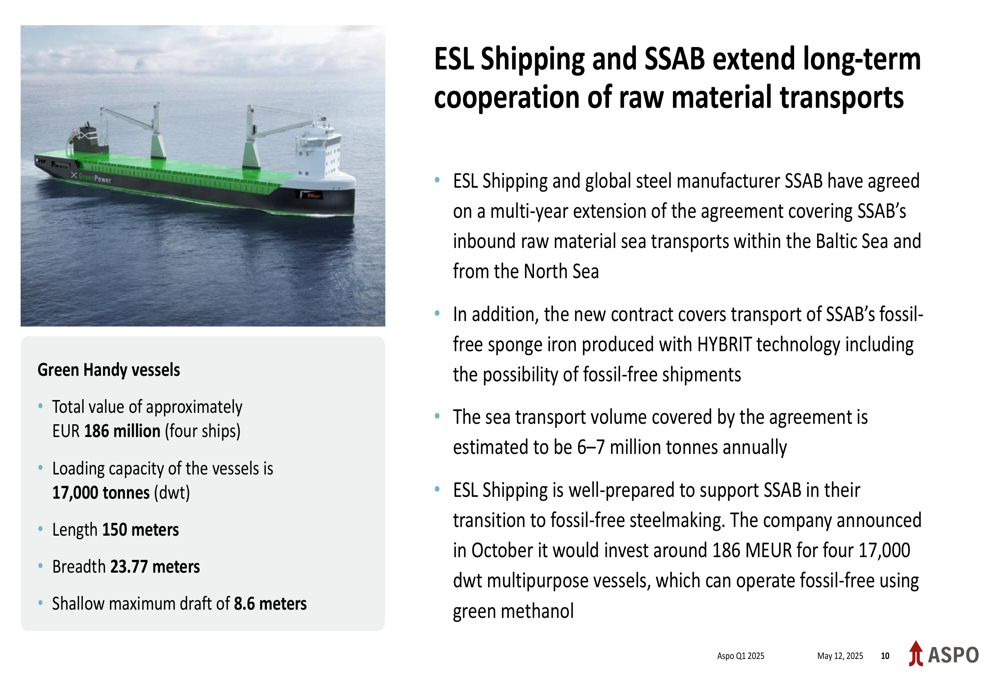

A significant development for ESL Shipping was the extension of its long-term cooperation with SSAB covering raw material sea transports. The agreement includes transport of SSAB’s fossil-free sponge iron produced with HYBRIT technology, with an estimated annual volume of 6-7 million tonnes.

ESL Shipping is also investing approximately €186 million in four 17,000 dwt multipurpose vessels capable of operating fossil-free using green methanol, supporting the company’s sustainability goals.

Leipurin expanded its presence in the Baltics through the acquisition of Kartagena UAB’s food ingredients distribution business, completed in February 2025. This acquisition is expected to generate close to €2 million in new revenues and approximately €0.15 million in EBITA annually.

Detailed Financial Analysis

Despite the overall positive performance, Aspo faced some challenges in Q1. Free cash flow was negative at -€4.4 million compared to -€3.5 million in Q1 2024, primarily due to investments in ESL Shipping’s Green Coaster vessels.

Operating cash flow decreased to €0.7 million from €5.4 million, mainly derived from Telko. Investments amounted to €4.5 million, significantly higher than the €0.6 million in Q1 2024.

The company’s net debt to comparable EBITDA ratio increased to 3.3 from 2.3, largely due to the €8.8 million investment in Green Coaster vessels. However, Aspo maintained a strong liquidity position with €23.9 million in cash and €40 million in unused revolving credit facilities.

In April 2025, Aspo participated in a multi-issuer bond guaranteed by Garantia with a €15 million loan share and announced the redemption of its €30 million hybrid bond, which will be paid back in June 2025.

Business Segment Performance

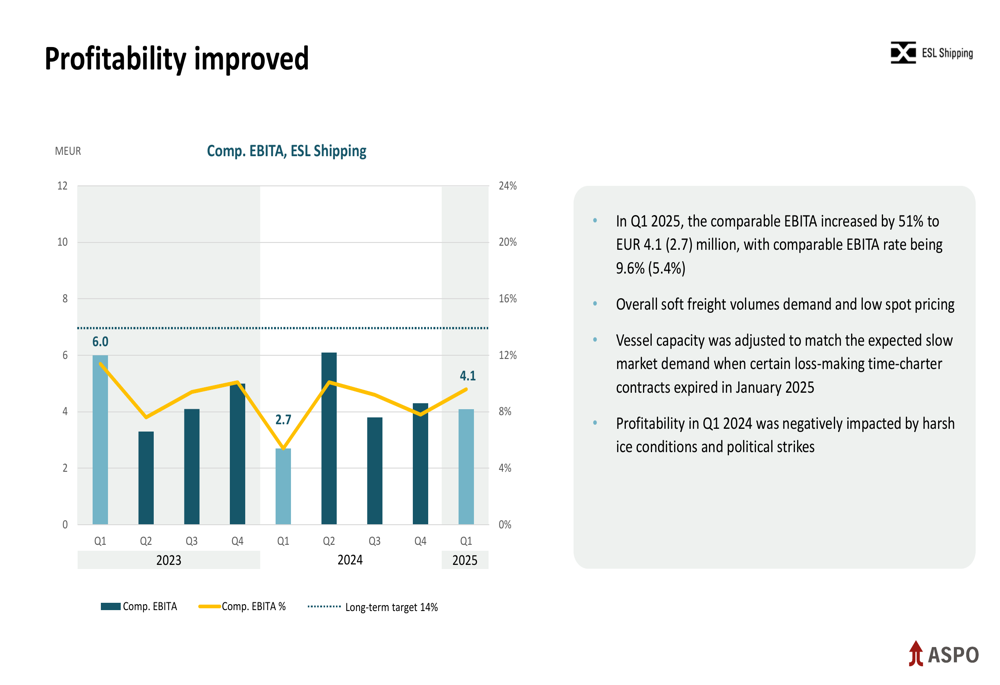

ESL Shipping improved its profitability despite challenging market conditions. The segment’s comparable EBITA increased by 51% to €4.1 million from €2.7 million, with the margin expanding to 9.6% from 5.4%. This improvement came despite a 14% decrease in net sales, as the company adjusted vessel capacity by allowing certain loss-making time-charter contracts to expire in January 2025.

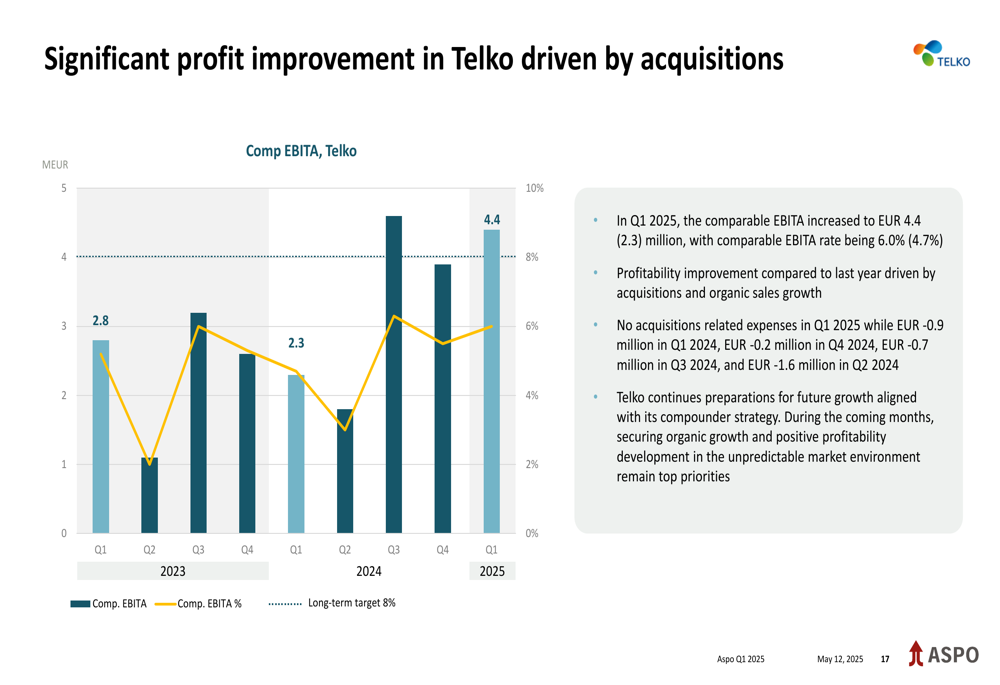

Telko achieved significant growth through acquisitions and organic volume expansion. Its comparable EBITA nearly doubled to €4.4 million from €2.3 million, with the margin improving to 6.0% from 4.7%. Sales grew by 46%, with increases across all business segments and main geographies.

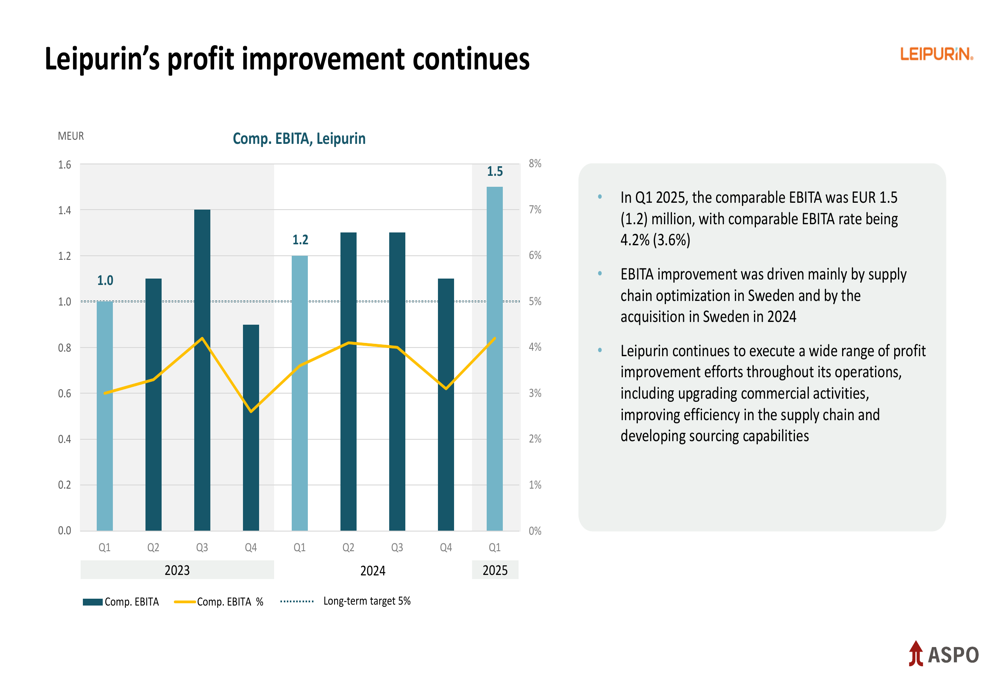

Leipurin continued its profit improvement trajectory, with comparable EBITA rising to €1.5 million from €1.2 million and the margin expanding to 4.2% from 3.6%. The improvement was driven mainly by supply chain optimization in Sweden and the acquisition completed in 2024.

Forward-Looking Statements

Aspo provided a positive outlook for 2025, expecting comparable EBITA to reach €35-45 million, up from €29.1 million in 2024. This improvement is anticipated to come primarily from the profit generation of the Green Coaster vessels, Telko’s and Leipurin’s acquisitions completed in 2024, and various intensified profit improvement actions throughout Aspo’s businesses.

The company maintains its long-term financial ambition to achieve €1 billion in net sales and 8% EBITA by 2028, with specific targets for each business unit: ESL Shipping (>€300 million, 14+%), Telko (>€500 million, 8+%), and Leipurin (>€200 million, 5+%).

For the remainder of 2025, Aspo expects demand to be weak for ESL Shipping during the first half of the year, while Telko and Leipurin markets are anticipated to remain stable.

"During 2025, our focus is on profitability improvement," emphasized CEO Jansson, highlighting the company’s commitment to delivering on its strategic objectives despite the challenging market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.