Europe’s Stoxx 600 inches lower amid French political crisis

Executive Summary

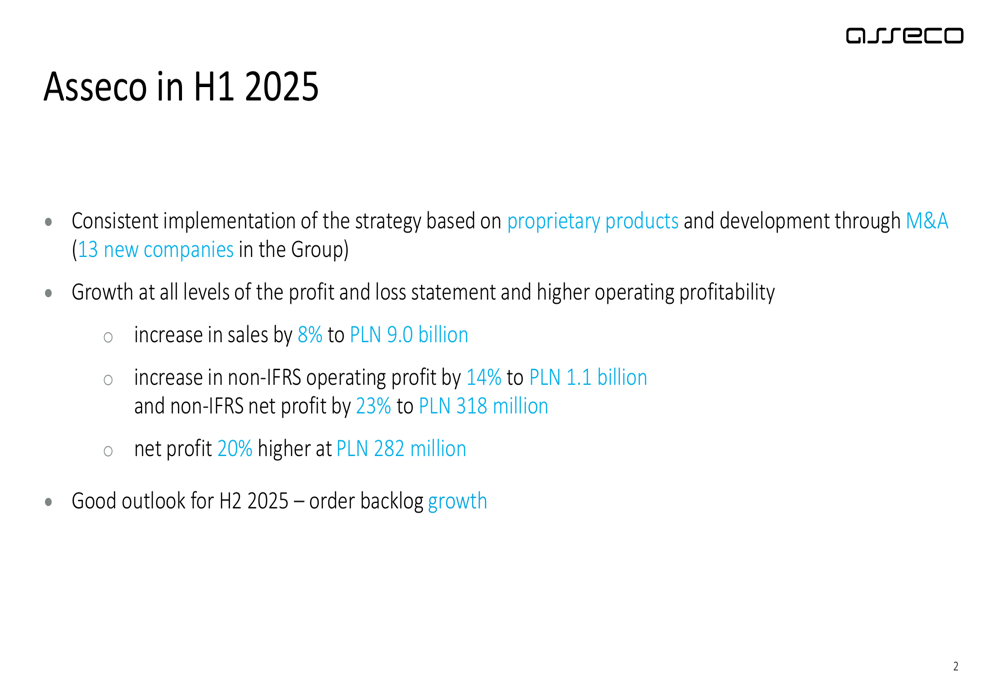

Asseco Poland SA ADR (OTC:ASOZY) presented its H1 2025 financial results on September 3, 2025, showcasing strong performance across all business segments. The company reported an 8% increase in sales revenues to PLN 9.0 billion, while non-IFRS operating profit jumped 14% to PLN 1.1 billion. Non-IFRS net profit attributable to shareholders of the parent company grew even more impressively at 23% to reach PLN 318 million.

The company highlighted its consistent implementation of a two-pronged growth strategy: developing proprietary software solutions and expanding through strategic acquisitions, with 13 new companies joining the Group during the period. Management expressed optimism about the second half of 2025, pointing to a growing order backlog.

As shown in the following summary of key financial metrics, Asseco has maintained strong growth momentum across all major indicators:

Detailed Financial Analysis

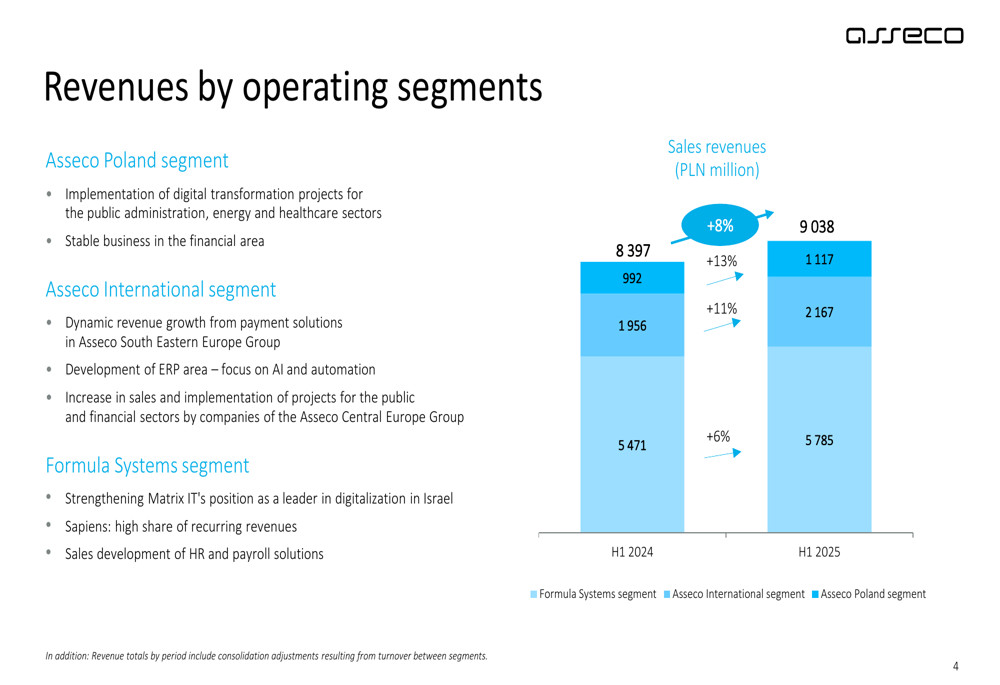

Asseco’s growth was broad-based across all three of its operating segments. The Asseco Poland segment grew revenues by 8% to PLN 1,116.5 million, while the Asseco International segment showed the strongest performance with an 11% increase to PLN 2,167 million. The Formula Systems segment, which represents the largest portion of the Group’s revenue, grew by 6% to PLN 5,785 million.

The following chart illustrates the revenue breakdown by operating segment:

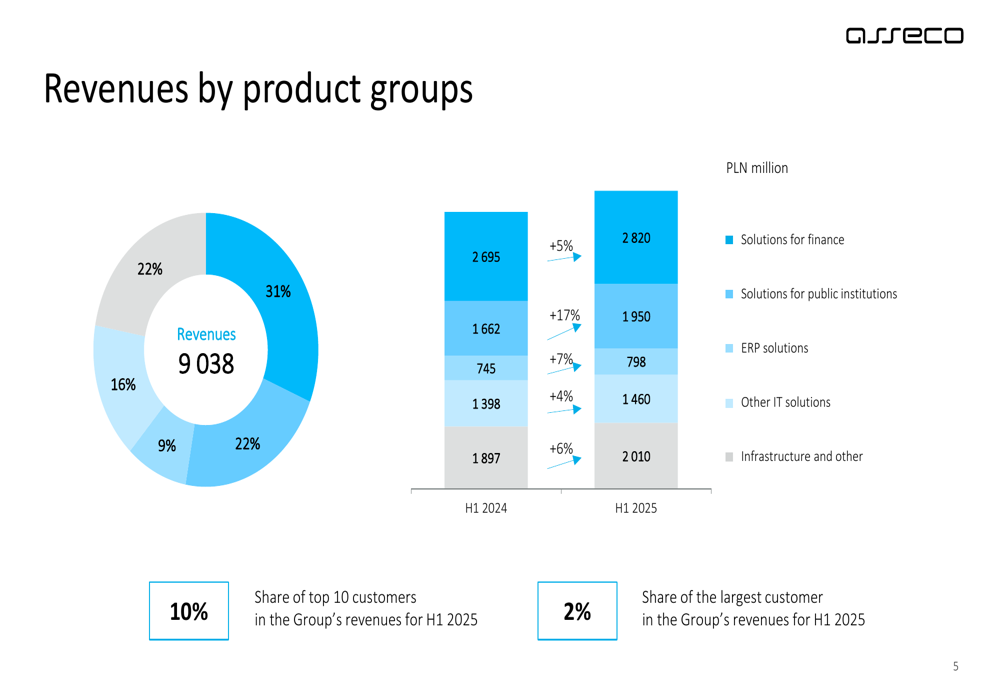

Looking at performance by product groups, solutions for public institutions showed the strongest growth at 17%, reaching PLN 1,950 million. Solutions for finance, which represents the largest product category, grew by 5% to PLN 2,820 million. ERP solutions increased by 7% to PLN 798 million, while other IT solutions and infrastructure grew by 4% and 6% respectively.

The pie chart below shows the distribution of revenue across product groups:

The company’s proprietary software and services, which form the core of its business model, grew by 8% to PLN 7,142 million and now represent 79% of total revenues. This focus on proprietary solutions has helped Asseco maintain healthy profit margins, with non-IFRS EBITDA margin reaching 15.7% in H1 2025.

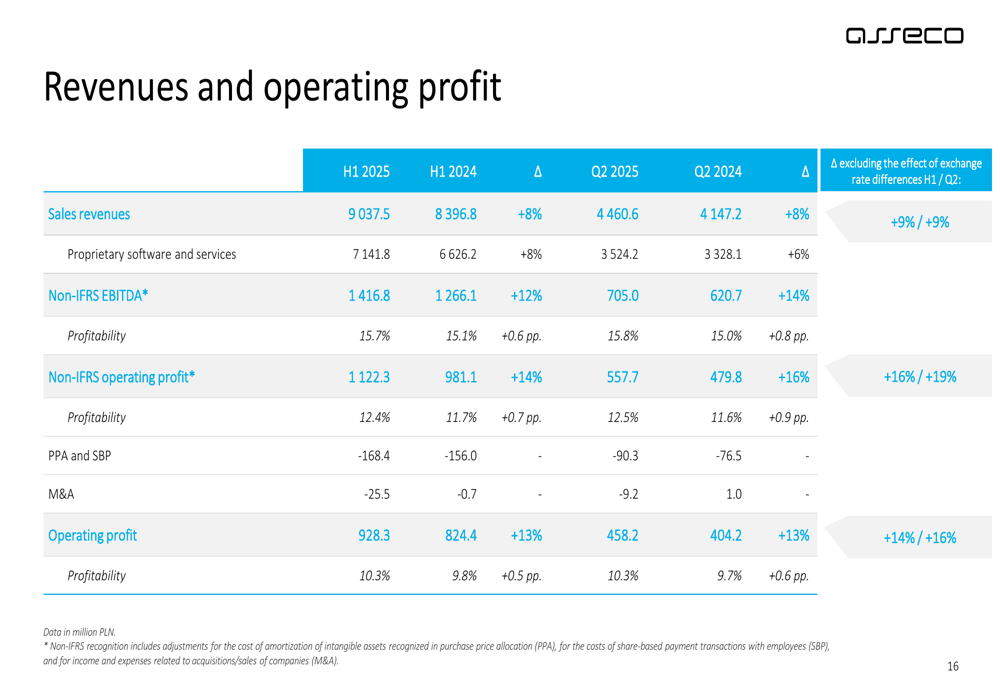

A detailed breakdown of the financial performance shows strong growth across all levels of the income statement:

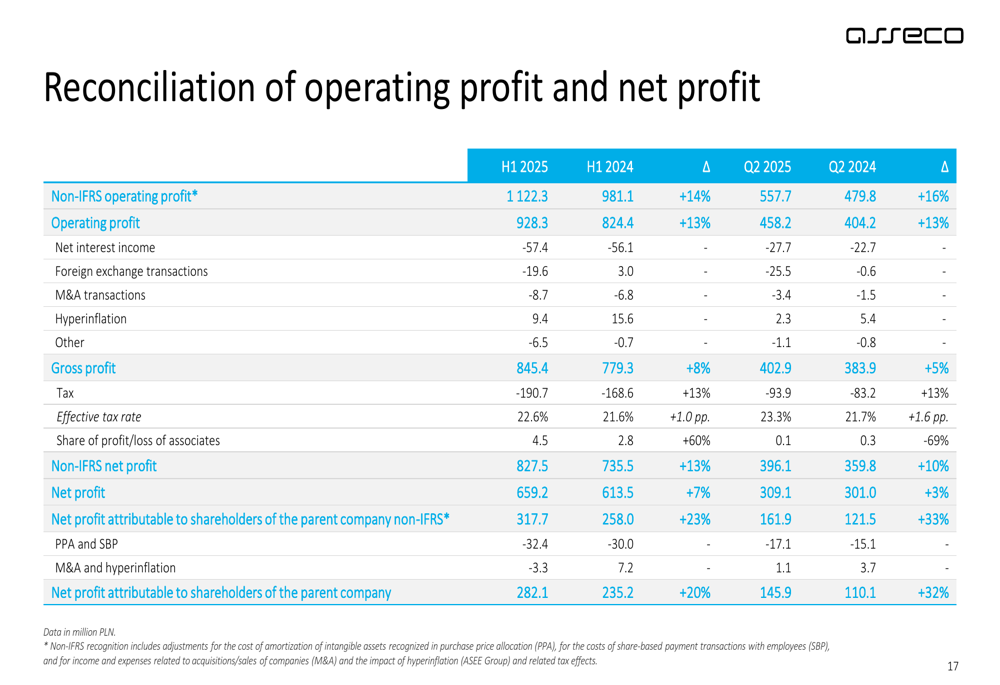

The reconciliation between operating profit and net profit further illustrates the company’s improved profitability:

Strategic Initiatives

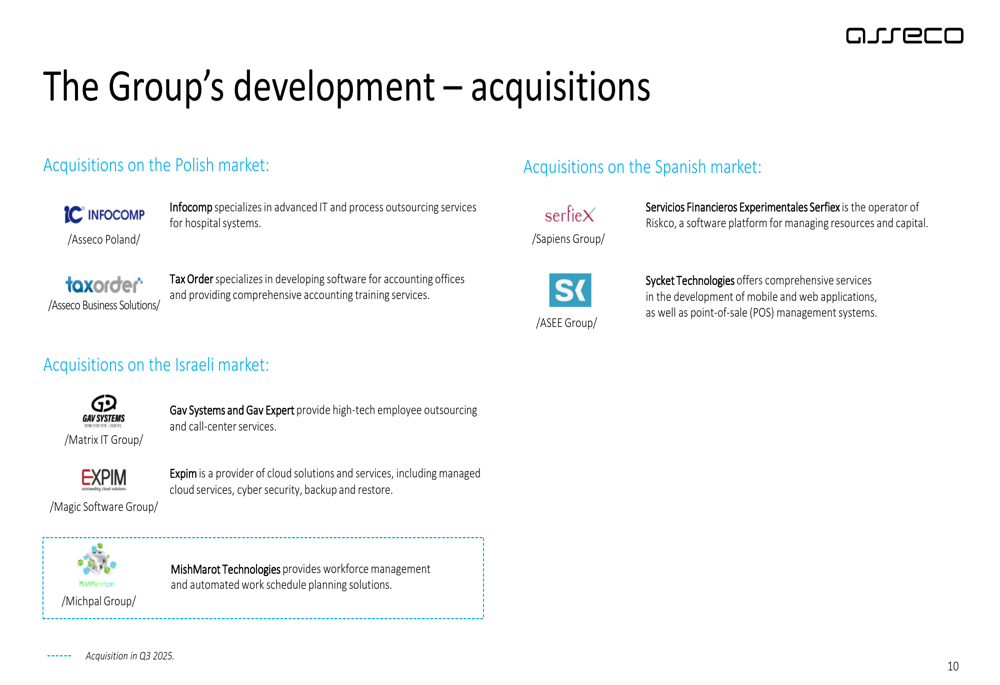

A key element of Asseco’s growth strategy has been its aggressive acquisition policy. During H1 2025, the Group added 13 new companies across multiple markets, significantly expanding its geographic footprint and technological capabilities.

In the Polish market, Asseco acquired InfoComp, which specializes in IT solutions for hospitals, and Tax Order, a provider of accounting software. The company also expanded in the Spanish market with the acquisition of Serfiex and Sycket Technologies, enhancing its financial management and mobile application development capabilities.

The following image highlights the company’s acquisition activity in the Polish, Spanish, and Israeli markets:

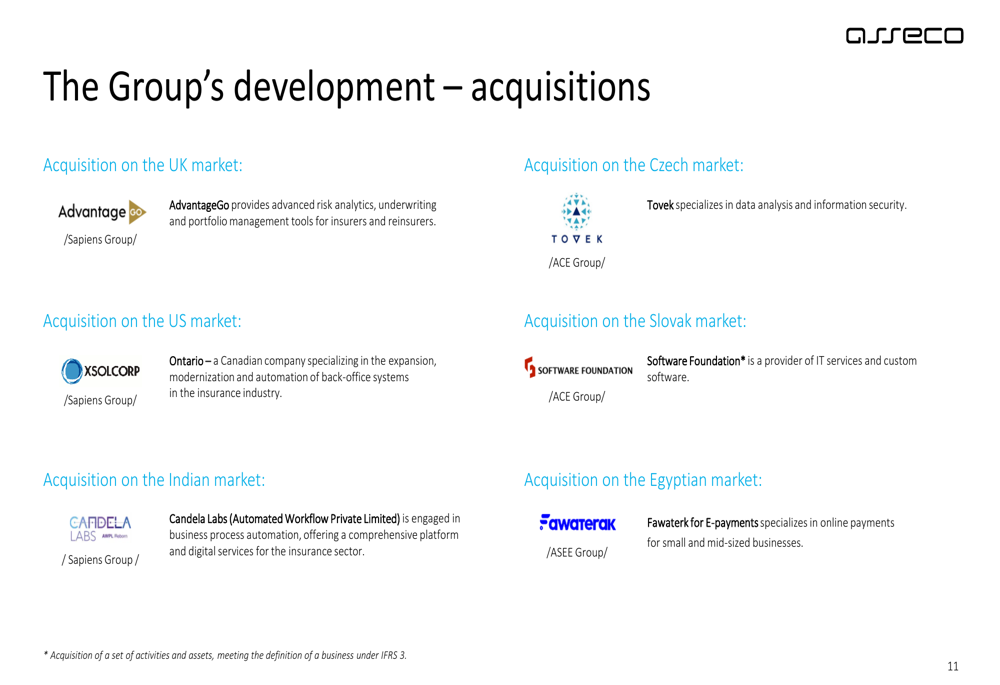

Asseco also made strategic acquisitions in the UK, Czech, Slovak, Indian, and Egyptian markets, further diversifying its geographic presence and technological portfolio:

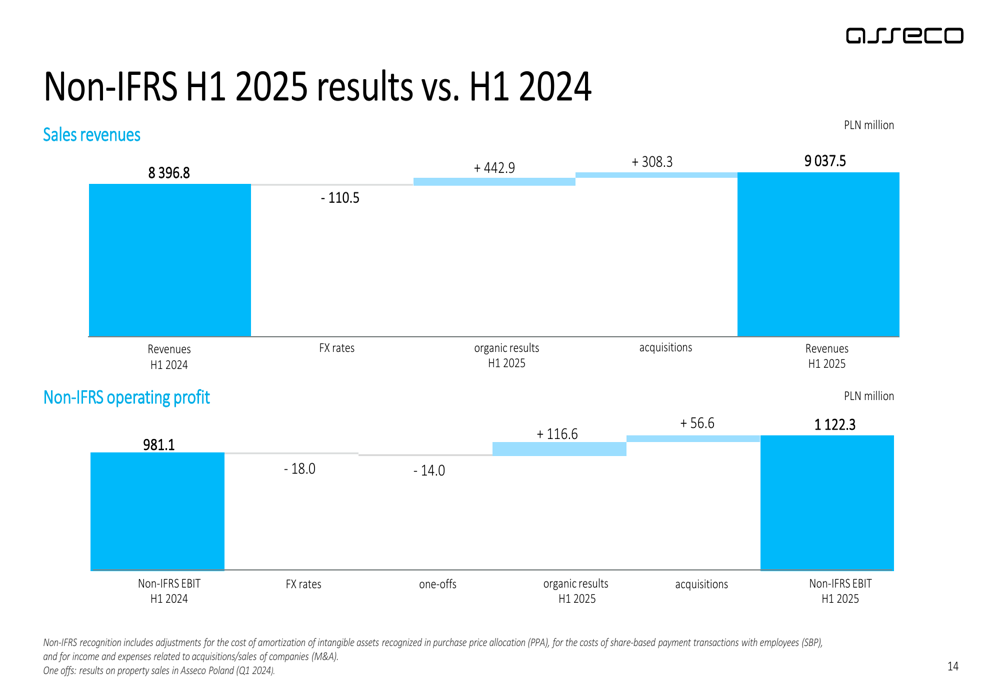

These acquisitions contributed PLN 308.3 million to the Group’s revenue growth in H1 2025, while organic growth added PLN 442.9 million, demonstrating a balanced approach to expansion.

The financial impact of these strategic initiatives can be seen in the following bridge analysis:

Forward-Looking Statements

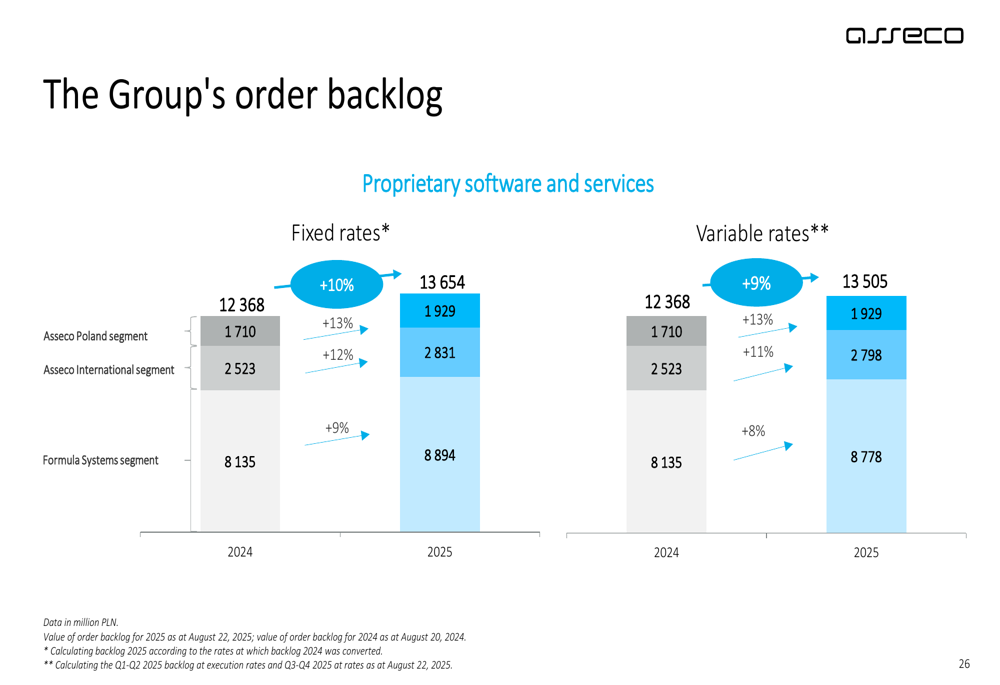

Asseco expressed confidence in its outlook for H2 2025, supported by a growing order backlog. The Group’s order backlog for 2025 shows significant growth compared to 2024 across all segments. At fixed exchange rates, the Asseco Poland segment’s backlog increased by 13%, while Asseco International and Formula Systems grew by 12% and 9% respectively.

The following chart illustrates the Group’s order backlog growth:

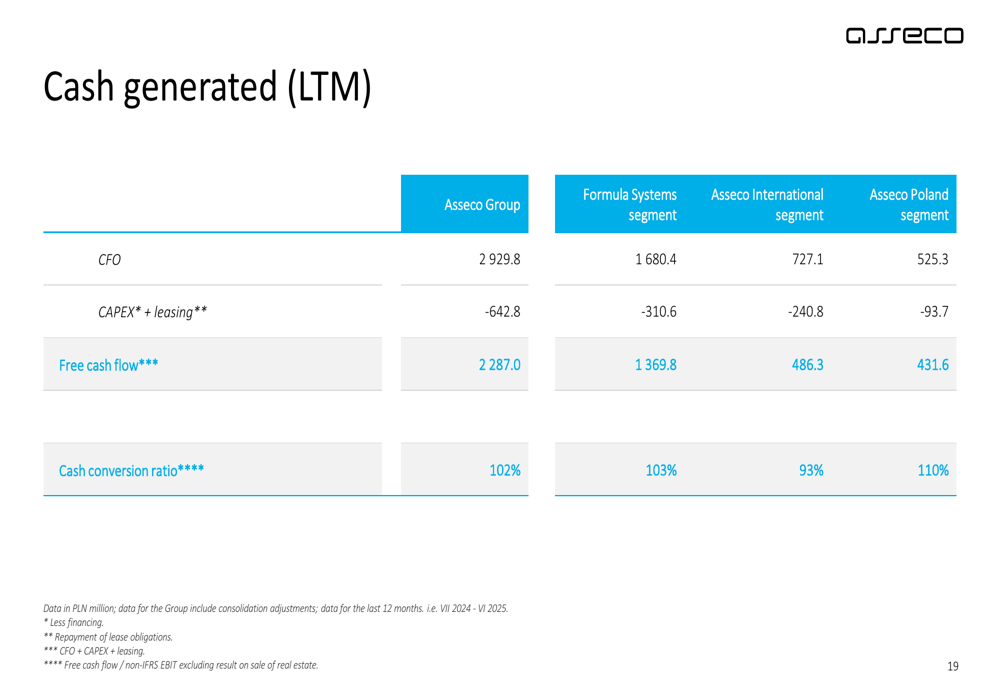

The company also highlighted its strong cash position, with PLN 2.47 billion in cash and a cash conversion ratio of 102% for the Group. This financial strength provides Asseco with the flexibility to continue its acquisition strategy while also investing in organic growth initiatives.

Asseco’s consistent performance across multiple geographies and product segments, combined with its strategic acquisition policy and growing order backlog, positions the company well for continued growth in the second half of 2025 and beyond. The company’s focus on proprietary software solutions and diversified revenue streams across finance, public institutions, and enterprise markets provides resilience against potential market fluctuations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.