Can anything shut down the Gold rally?

Introduction & Market Context

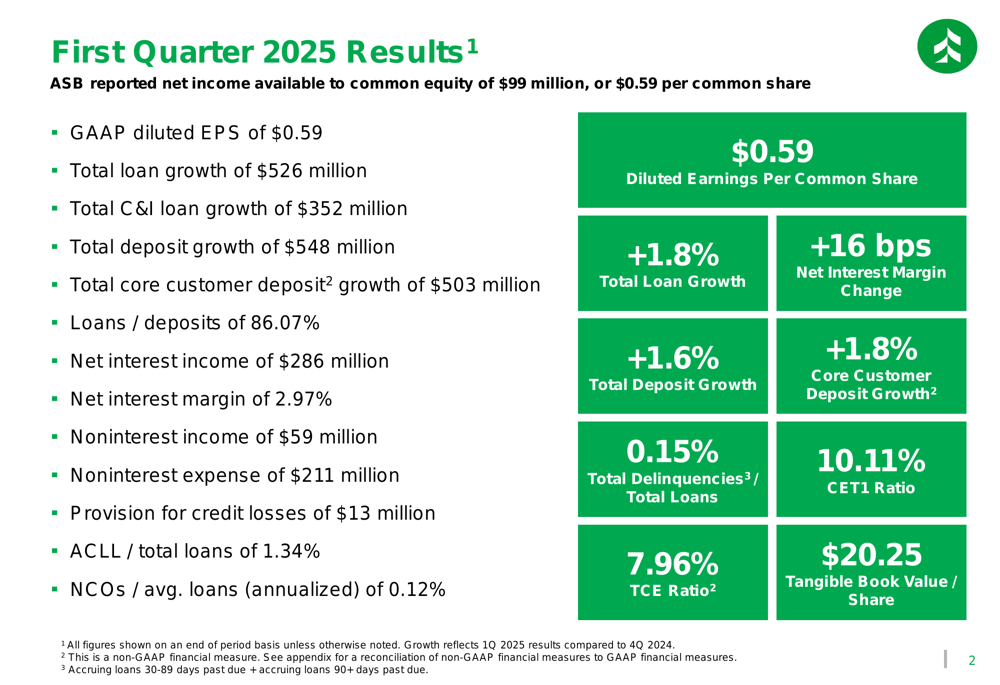

Associated Banc-Corp (NYSE:ASB) reported first quarter 2025 earnings on April 24, 2025, delivering solid results with growth in key metrics. The Wisconsin-based bank holding company posted net income available to common equity of $99 million, or $0.59 per common share, continuing its positive momentum from the previous quarter.

Following the earnings release, ASB shares rose 3.09% in after-hours trading to $22.70, building on a 2.85% gain during the regular session. The stock has been trading between $18.32 and $28.18 over the past 52 weeks.

Quarterly Performance Highlights

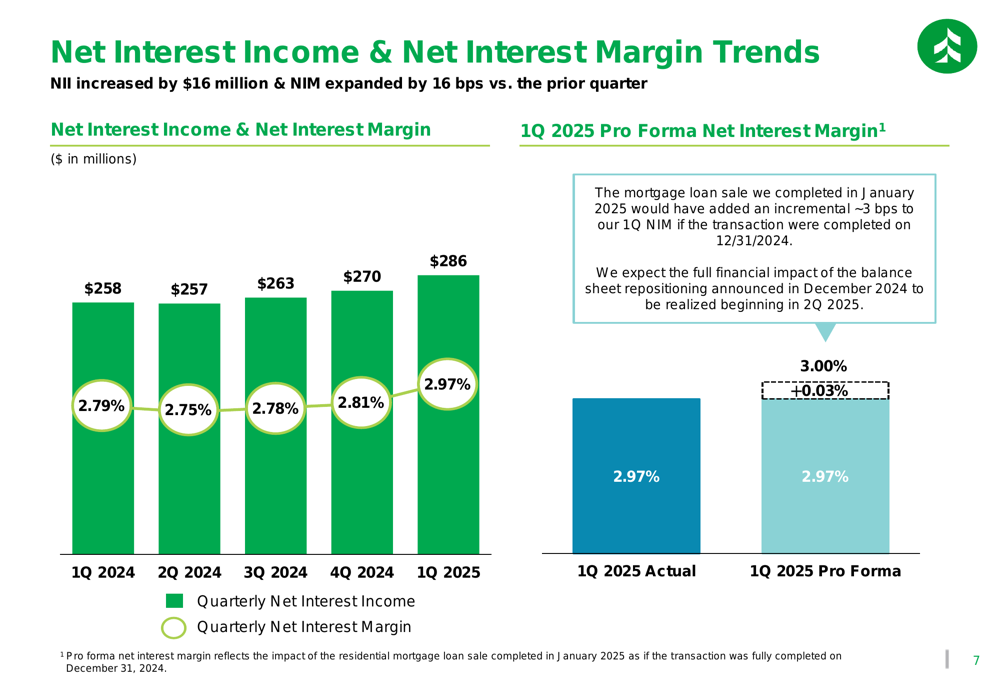

Associated Banc-Corp’s first quarter results demonstrated improvement across several key financial metrics. The company reported net interest income of $286 million, up from $263 million in the previous quarter, while net interest margin expanded by 16 basis points to 2.97%.

As shown in the following summary of first quarter results, the company achieved growth in both loans and deposits while maintaining strong capital positions:

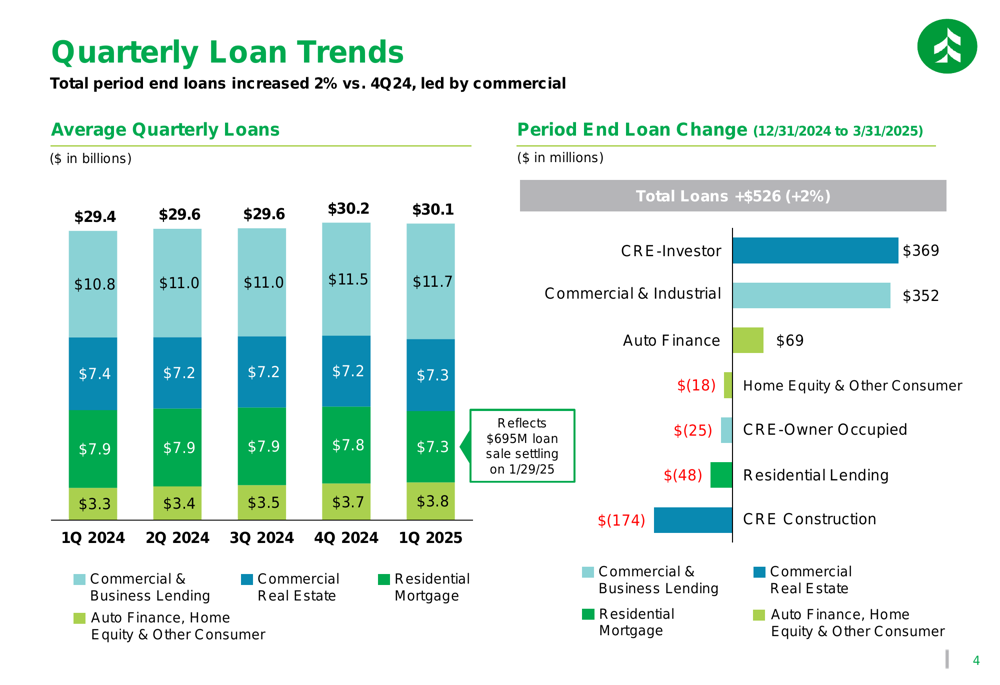

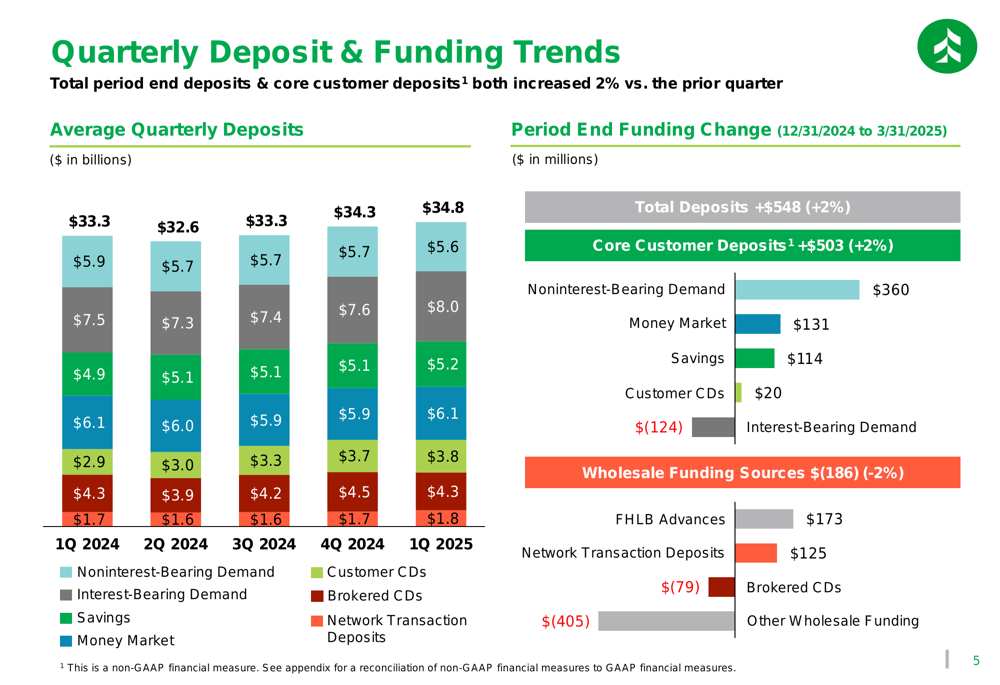

Total (EPA:TTEF) loans increased by $526 million or 1.8% during the quarter, primarily driven by commercial and industrial (C&I) lending, which grew by $352 million. The company also reported total deposit growth of $548 million (+1.6%), with core customer deposits increasing by $503 million (+1.8%).

The quarterly loan trends reveal a continued shift toward commercial lending, consistent with the company’s strategic initiatives:

On the deposit side, Associated Banc-Corp maintained a stable funding base with growth across multiple deposit categories:

Net Interest Income and Margin Expansion

A key highlight of the quarter was the significant improvement in net interest income and margin. Net interest income increased by $16 million compared to the previous quarter, while net interest margin expanded by 16 basis points to 2.97%.

The following chart illustrates this positive trend in net interest income and margin:

This improvement was driven by a favorable shift in the balance sheet composition, with interest-bearing liability costs decreasing by 23 basis points while earning asset yields decreased by just 1 basis point during the quarter. The company noted that the mortgage loan sale completed in January 2025 would have added an incremental 3 basis points to the Q1 NIM if the transaction had been completed by December 31, 2024.

Balance Sheet Repositioning Strategy

Associated Banc-Corp has successfully completed its balance sheet repositioning strategy, which was initiated in late 2024. The company sold $695 million in residential mortgage balances in January 2025, following the sale of $1.295 billion in available-for-sale securities in Q4 2024.

The following summary details the completed actions:

This strategic repositioning has reduced the company’s mortgage loan concentration from 29% in Q3 2023 to 23% in Q1 2025, while simultaneously increasing its commercial lending focus. Commercial and business relationship managers have increased by nearly 30% compared to Q3 2023, contributing to C&I loan growth of $1.1 billion year-over-year.

Credit Quality & Capital Position

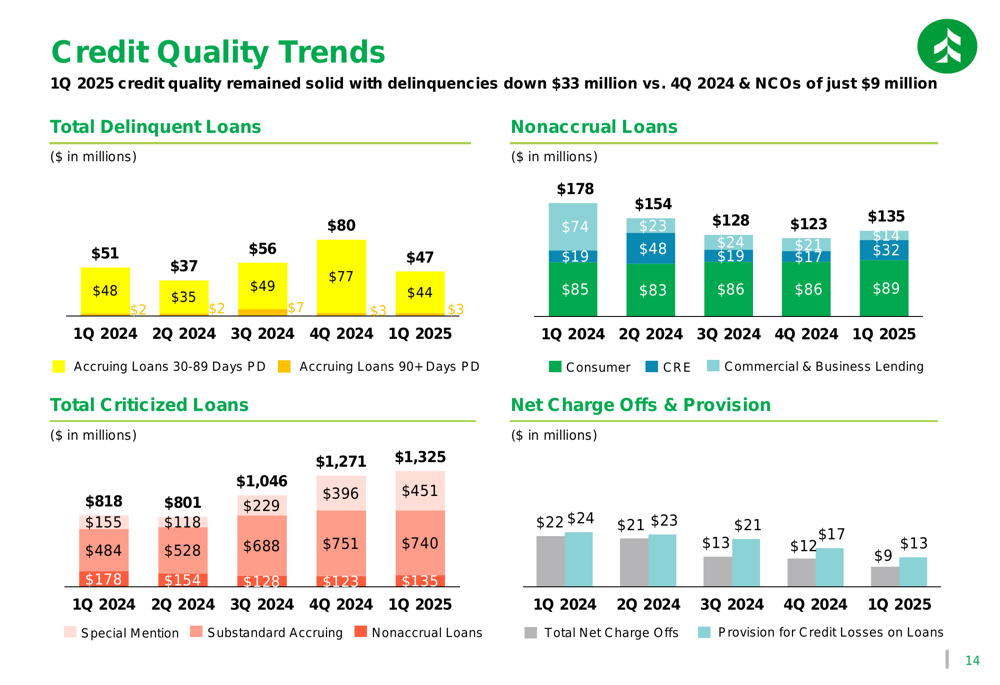

Associated Banc-Corp maintained solid credit quality metrics during the quarter. The allowance for credit losses on loans (ACLL) as a percentage of total loans decreased slightly by 1 basis point to 1.34% compared to the previous quarter.

The following chart illustrates the company’s credit quality trends:

Net charge-offs for the quarter were $13 million, representing 0.12% of average loans on an annualized basis, while the provision for credit losses was $9 million.

Capital ratios remained strong, with the Common Equity Tier 1 (CET1) ratio improving to 10.11%, up from 10.01% in the previous quarter. The tangible book value per share increased to $20.25 from $19.71 at the end of 2024.

Consumer Loan Portfolio Quality

Associated Banc-Corp emphasized the high quality of its consumer loan portfolio, noting that 94% of its $10.8 billion consumer loan portfolio consists of prime or super-prime borrowers. Residential mortgages make up the largest component at $7.0 billion (23.1% of total loans), followed by auto finance at $2.9 billion (9.5%).

The weighted average FICO scores across the consumer portfolio remain strong, with residential mortgages at 787, auto finance at 775, home equity at 793, and credit cards at 791.

Forward-Looking Statements

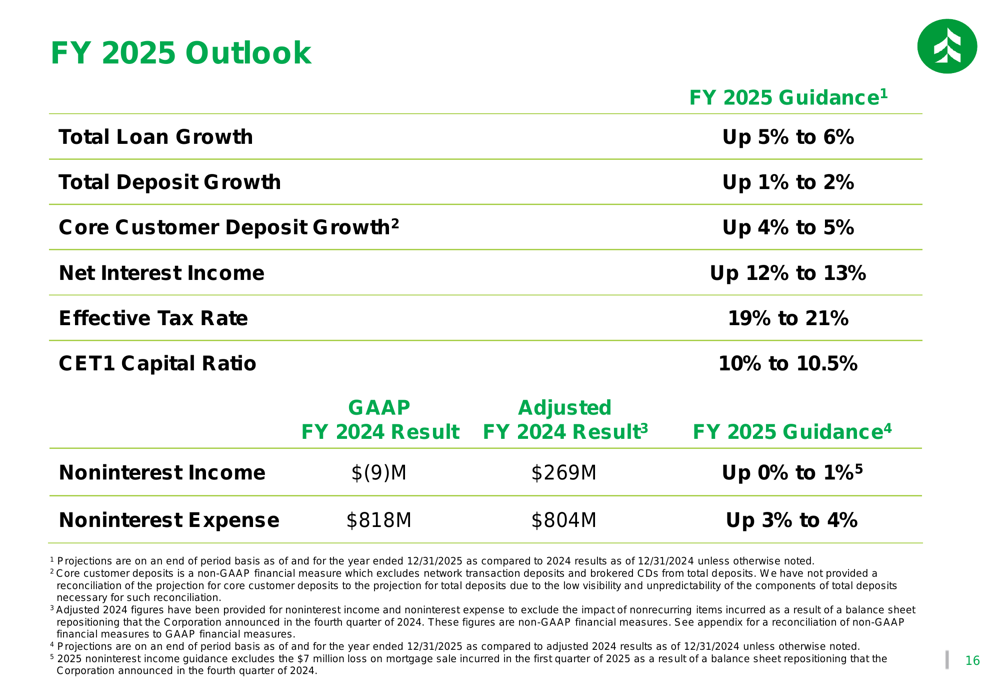

Looking ahead, Associated Banc-Corp provided a positive outlook for fiscal year 2025, projecting loan growth of 5-6% and total deposit growth of 1-2%. Core customer deposits are expected to grow by 4-5%, while net interest income is projected to increase by 12-13%.

The following slide outlines the company’s full-year 2025 guidance:

The company aims to maintain a CET1 capital ratio between 10% and 10.5% throughout 2025, while continuing to focus on expanding its commercial lending business and optimizing its balance sheet composition.

Strategic Initiatives

Associated Banc-Corp highlighted several completed strategic initiatives that position the company for continued growth. These include the addition of top talent in key leadership roles, commercial relationship manager expansion, quarterly product and digital upgrades, and a rebalanced consumer lending approach.

The company reported a net promoter score of 55 in Q1 2025 and total checking household growth of 1% (annualized). Mass Affluent deposits have seen $1.6 billion in net new deposits since the program’s launch in December 2022.

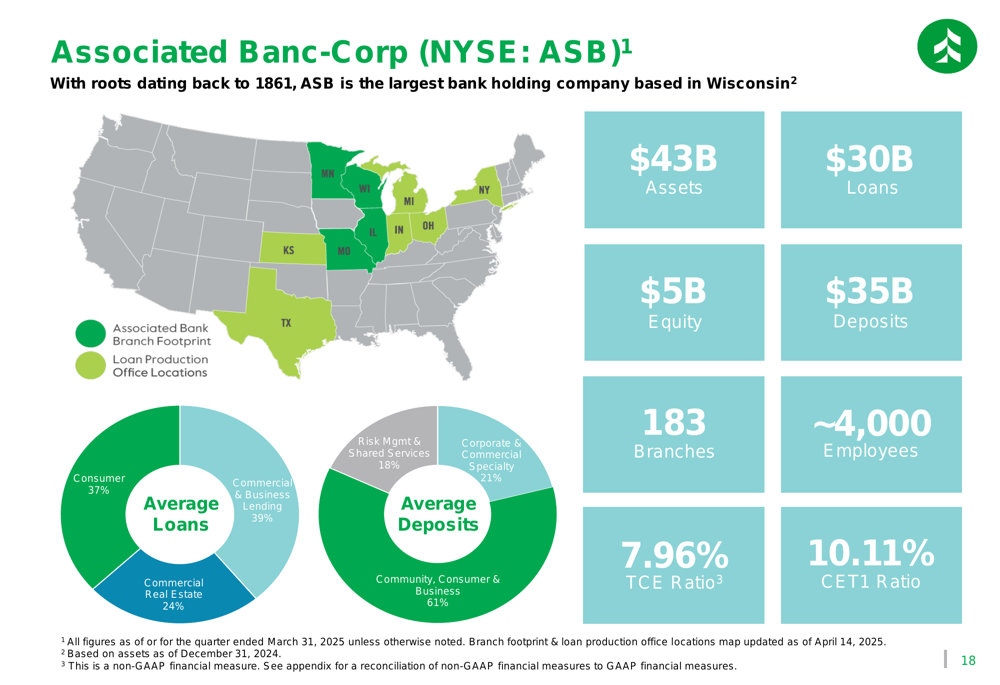

As the largest bank holding company based in Wisconsin, with $43 billion in assets and 183 branches across its footprint, Associated Banc-Corp continues to leverage its regional presence while implementing strategic initiatives to improve profitability and returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.