IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

Athabasca Oil (OTC:ATHOF) Corporation (TSX:ATH) presented its Q2 2025 results on July 24, highlighting strong operational performance and accelerating shareholder returns. The Canadian energy producer, focused on thermal oil and Duvernay assets, continues to benefit from its low-decline production base and robust balance sheet in a supportive commodity price environment.

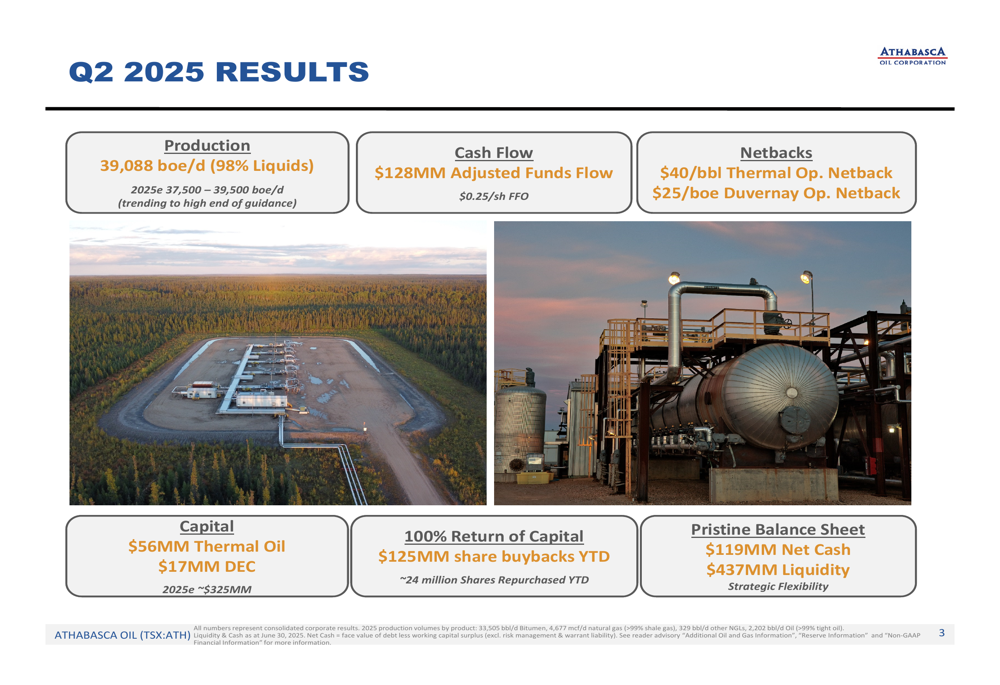

The company reported production of 39,088 boe/d (98% liquids) for the quarter, trending toward the high end of its 2025 guidance range. With a net cash position of $119 million and significant free cash flow generation, Athabasca has ramped up its share repurchase program while advancing strategic growth initiatives.

Quarterly Performance Highlights

Athabasca delivered solid financial and operational results in Q2 2025, generating $128 million in adjusted funds flow ($0.25 per share) while maintaining disciplined capital expenditure of $73 million ($56 million in Thermal Oil, $17 million in Duvernay Energy Corp). The company achieved strong operating netbacks of $40/bbl in its Thermal Oil division and $25/boe in its Duvernay assets.

As shown in the following quarterly results summary:

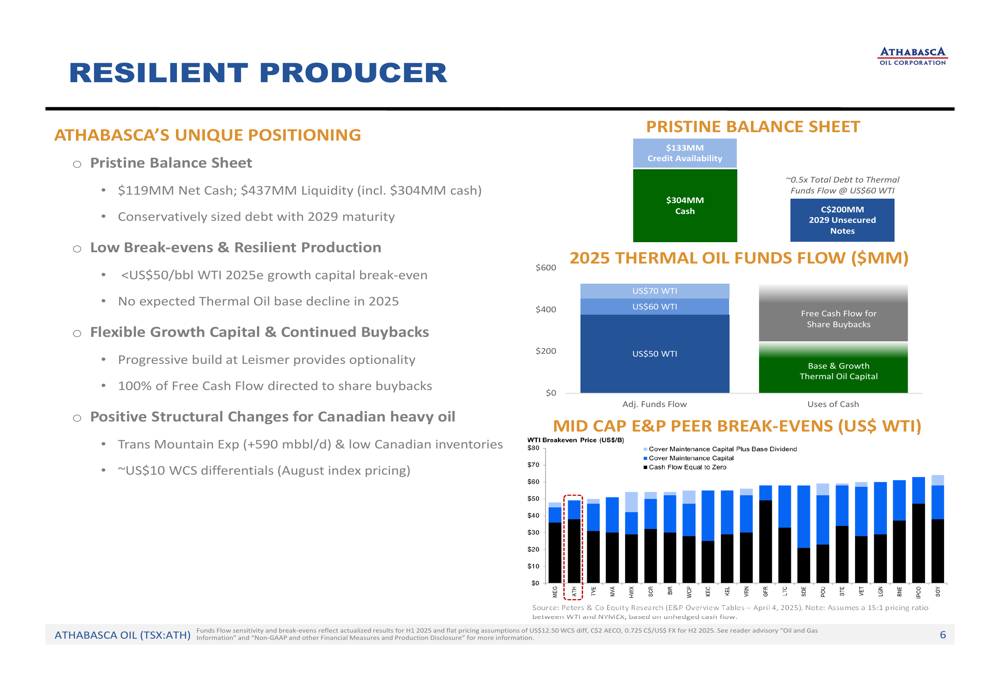

Shareholder returns remained a priority, with $125 million allocated to share buybacks year-to-date, representing approximately 24 million shares repurchased. The company maintains a pristine balance sheet with $119 million in net cash and $437 million in available liquidity, providing strategic flexibility for both growth initiatives and continued shareholder returns.

Strategic Growth Initiatives

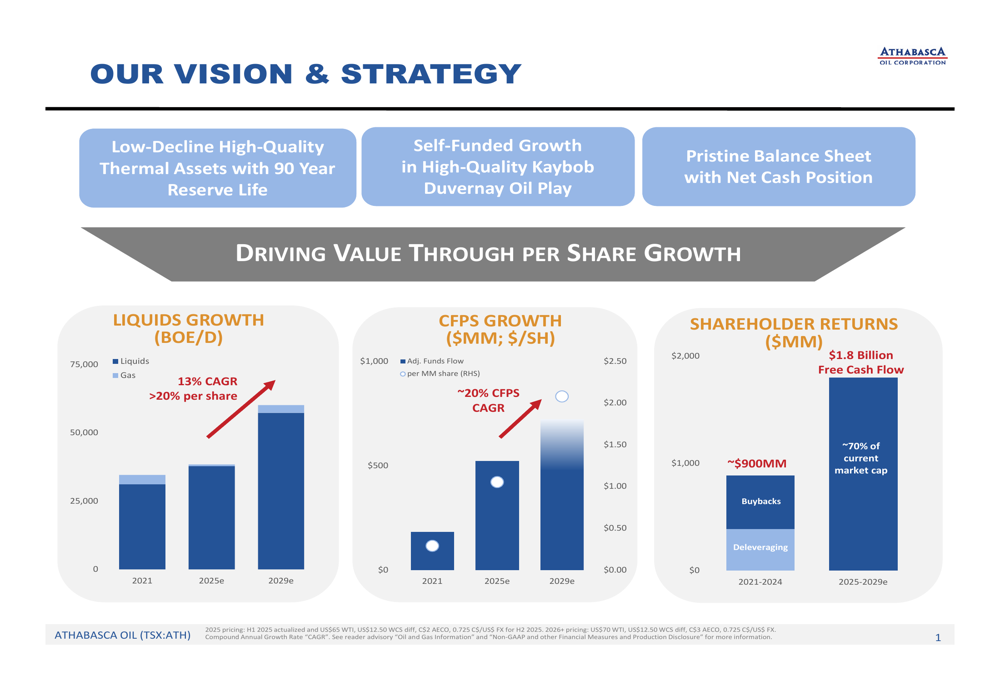

Athabasca’s long-term strategy centers on leveraging its low-decline, high-quality thermal assets with a 90-year reserve life while pursuing self-funded growth in its high-quality Kaybob Duvernay oil play. The company projects significant production and cash flow growth through 2029, as illustrated in its strategic vision:

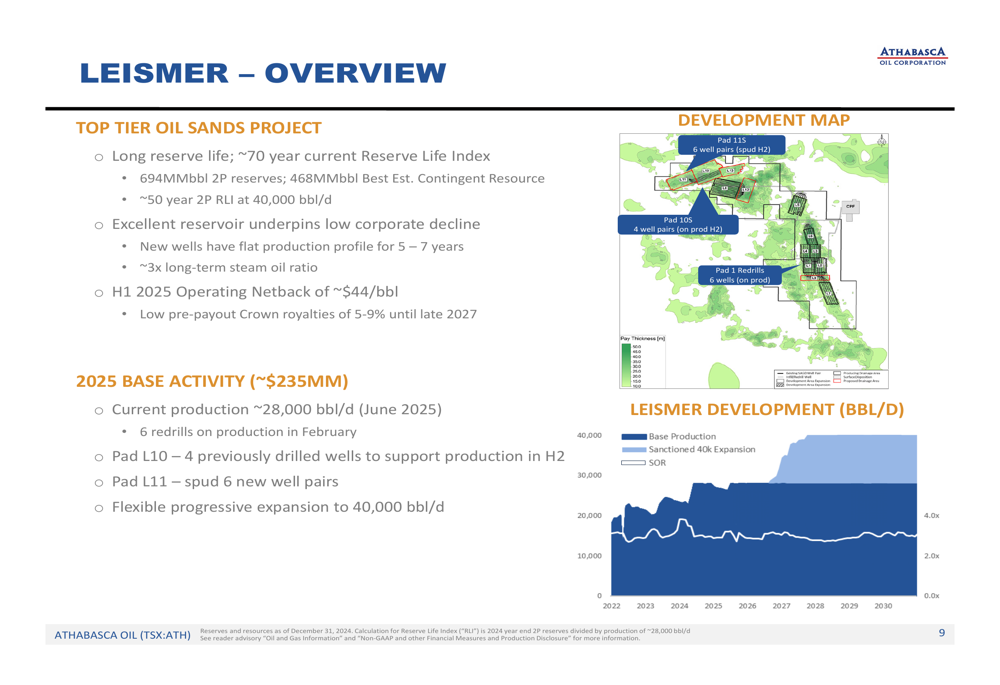

The company’s Leismer thermal project forms the cornerstone of its growth strategy, with a progressive expansion plan to increase production from current levels of approximately 28,000 bbl/d to 40,000 bbl/d by the end of 2027. In July 2024, Athabasca sanctioned this expansion with a project cost of approximately $300 million and a capital efficiency of around $25,000/bbl.

Complementing its thermal oil operations, Athabasca holds a 70% stake in Duvernay Energy Corporation (DEC), with Cenovus owning the remaining 30%. This subsidiary provides exposure to the Kaybob Duvernay oil window, with plans to grow production from approximately 4,000 boe/d in 2025 to around 6,000 boe/d by year-end, and ultimately to approximately 20,000 boe/d in the late 2020s.

Detailed Financial Analysis

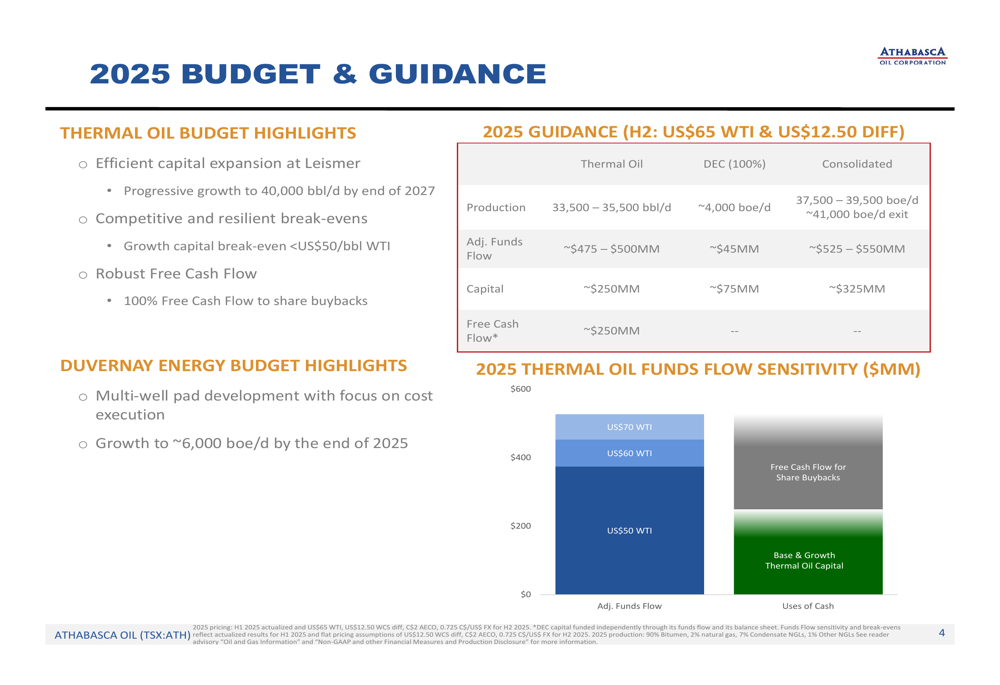

Athabasca’s financial position continues to strengthen, supported by robust commodity prices and operational efficiencies. The company projects adjusted funds flow of approximately $525-550 million for 2025 (based on US$65 WTI and US$12.50 differential in H2), with approximately $475-500 million from Thermal Oil and $45 million from DEC.

The company’s 2025 budget and guidance demonstrates its financial resilience across various commodity price scenarios:

With a growth capital break-even below US$50/bbl WTI, Athabasca maintains competitive positioning among its mid-cap E&P peers. This low break-even, combined with its net cash position, provides significant downside protection while maintaining exposure to commodity price upside.

Forward-Looking Statements

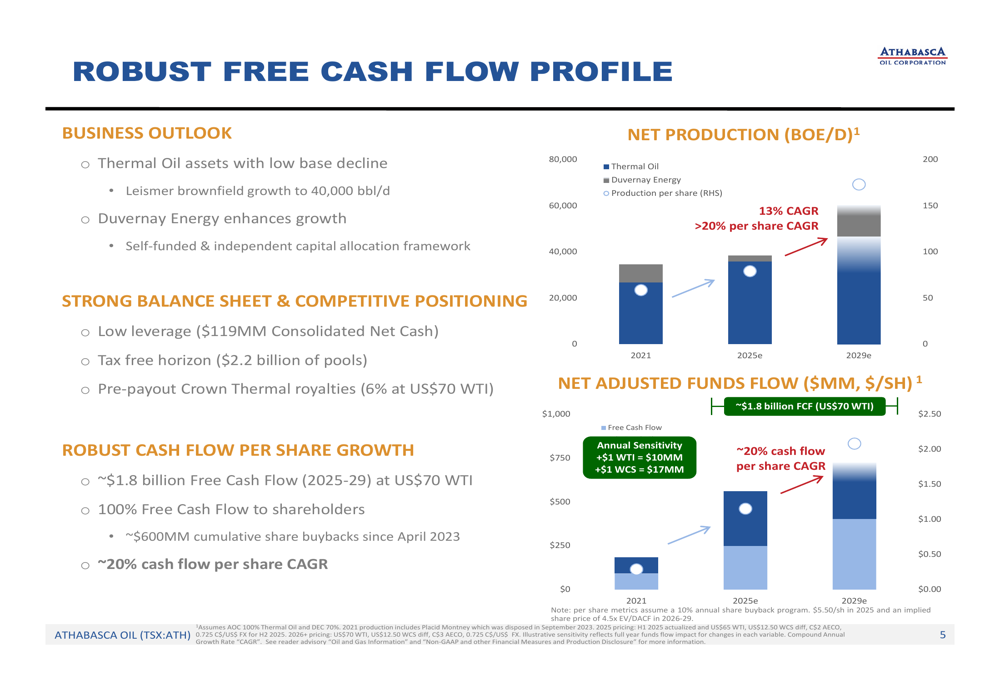

Looking ahead, Athabasca has provided 2025 guidance with production between 37,500-39,500 boe/d and an exit rate of approximately 41,000 boe/d. The company expects to generate approximately $1.8 billion in free cash flow between 2025-2029 at US$70 WTI, with a commitment to return 100% of free cash flow to shareholders.

The company’s long-term cash flow profile shows strong growth potential through the end of the decade:

Athabasca’s capital allocation framework prioritizes maintaining its strong balance sheet while funding growth initiatives and returning excess cash to shareholders. The company benefits from significant tax pools ($2.2 billion) and pre-payout Crown Thermal royalties (6% at US$70 WTI), enhancing its cash flow generation capabilities.

With production growth projected at a 13% CAGR from 2021-2029 and cash flow per share growth at approximately 20% CAGR over the same period, Athabasca is well-positioned to deliver substantial value to shareholders while maintaining financial flexibility in a volatile commodity price environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.