AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

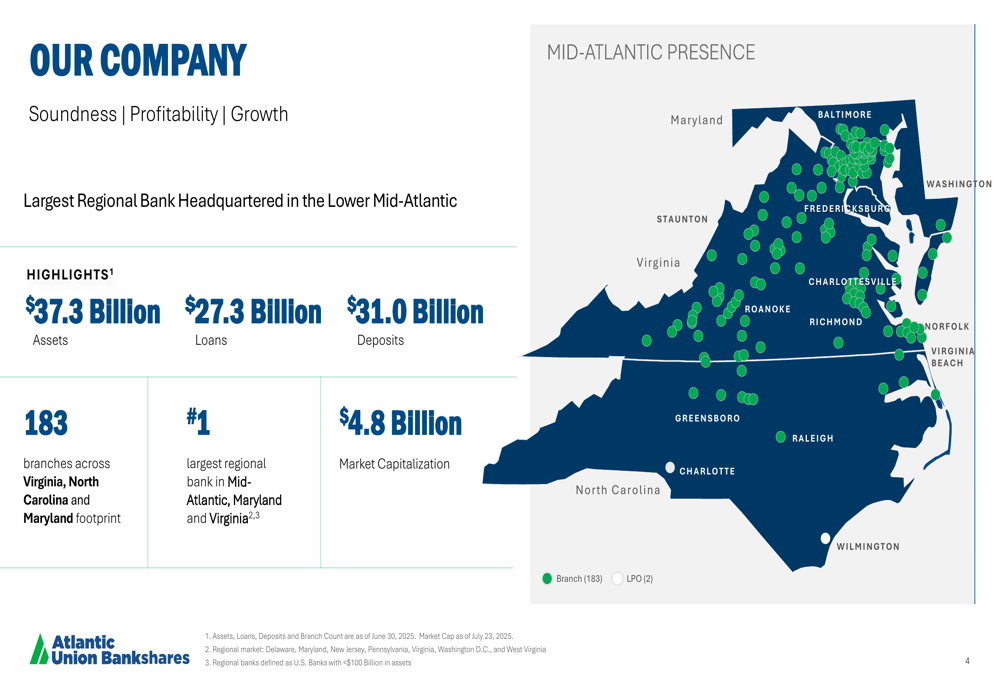

Atlantic Union Bankshares Corporation (NYSE:AUB) presented its second quarter 2025 earnings on July 24, 2025, revealing a significant rebound from its first-quarter performance. The Richmond, Virginia-based financial institution reported strong results following the completion of its Sandy Spring acquisition, positioning itself as the largest regional bank headquartered in the Lower Mid-Atlantic region.

The bank’s stock has shown positive momentum, trading at $33.68 as of July 23, 2025, representing a 1.54% increase. This marks a substantial recovery from the post-Q1 earnings price of $26.35, when the company missed EPS expectations. The current stock price sits comfortably above its 52-week low of $22.85, though still below its 52-week high of $44.54.

As shown in the following company overview, Atlantic Union now boasts $37.3 billion in assets, $27.3 billion in loans, and $31.0 billion in deposits, with a market capitalization of $4.8 billion:

Quarterly Performance Highlights

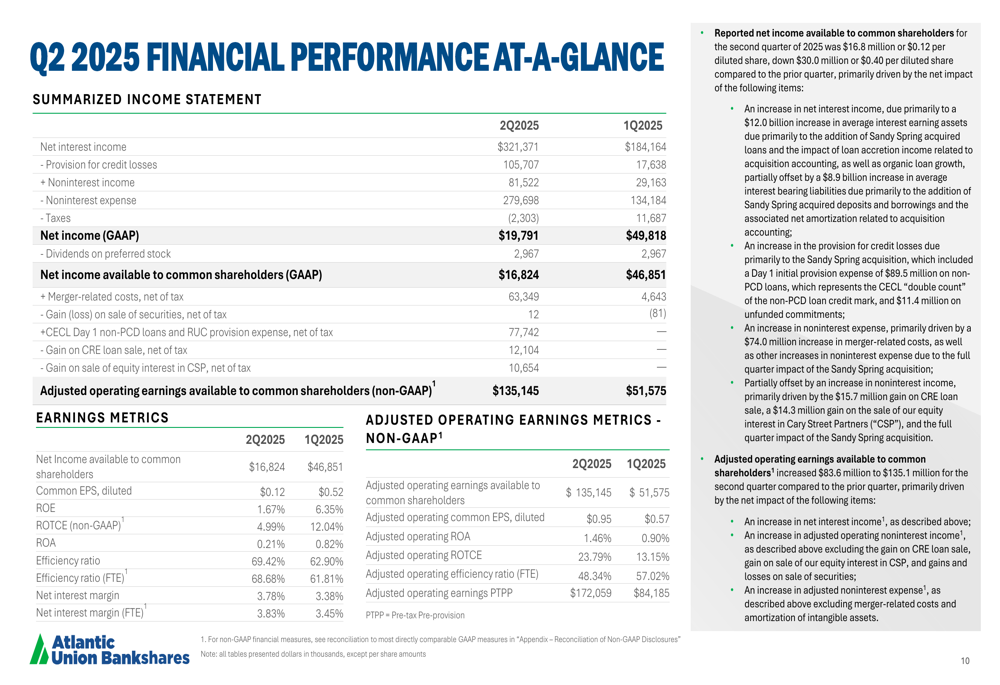

Atlantic Union demonstrated robust performance in Q2 2025, with adjusted operating earnings available to common shareholders of $135.1 million, a substantial improvement from the $51.6 million reported in Q1. The company achieved an impressive adjusted operating return on tangible common equity (ROTCE) of 23.79%, significantly higher than the 13.2% reported in the previous quarter.

The bank’s efficiency also improved markedly, with the adjusted operating efficiency ratio declining to 48.3% from 57% in Q1, indicating better cost control and operational synergies following the Sandy Spring acquisition.

The following slide summarizes the key highlights from the quarter, including 4% annualized loan growth and extremely low net charge-offs at just 1 basis point of total average loans:

A more detailed look at the financial performance shows the significant improvement across key metrics compared to the previous quarter:

Detailed Financial Analysis

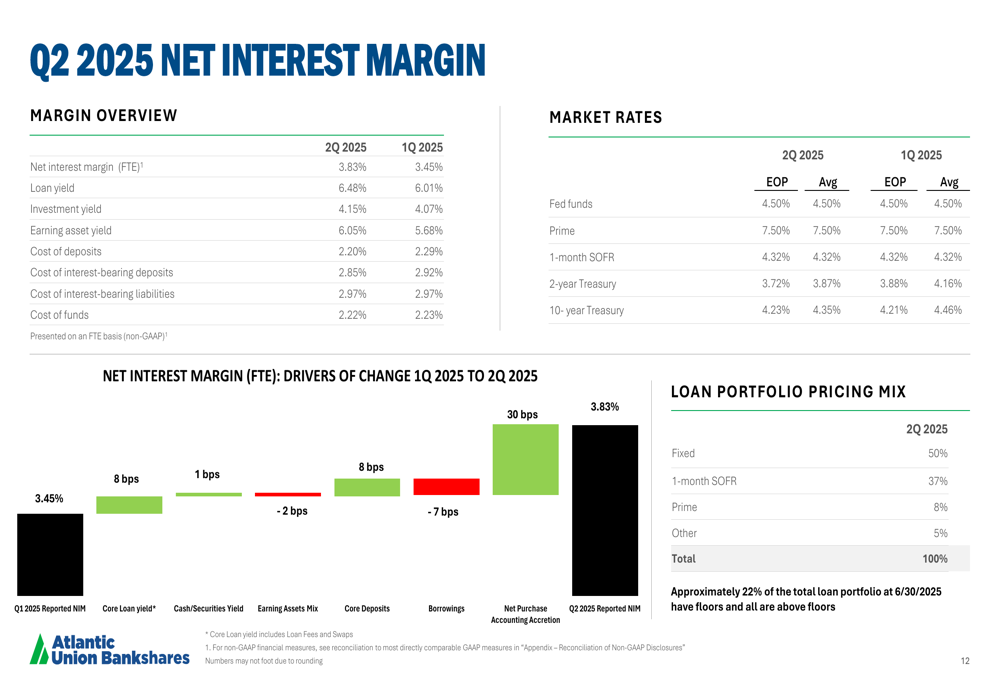

Atlantic Union’s net interest margin (NIM) expanded to 3.83% in Q2 2025, continuing the positive trend from Q1 when NIM increased by 12 basis points. The loan yield reached 6.48%, while the cost of deposits was 2.20%. This healthy spread has contributed significantly to the bank’s profitability.

The following chart breaks down the drivers of the net interest margin:

The bank’s loan and deposit portfolios both showed solid growth. Total (EPA:TTEF) loans held for investment reached $27.3 billion, while deposits totaled $31.0 billion. The loan-to-deposit ratio stood at 88.2%, indicating a well-balanced funding structure.

As shown in the detailed breakdown below, commercial real estate and commercial & industrial loans represent significant portions of the portfolio, with consumer loans also making a substantial contribution:

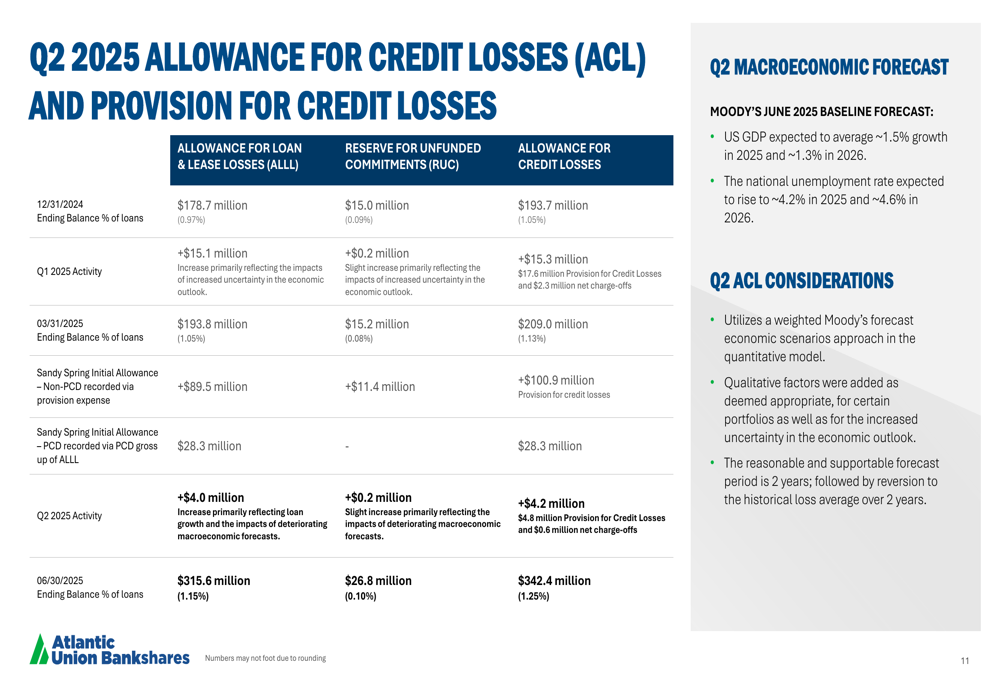

Credit quality remained exceptionally strong, with net charge-offs at just 1 basis point of total average loans annualized. The bank increased its allowance for credit losses to 1.25%, demonstrating prudent risk management in the face of economic uncertainties. This represents a slight increase from the previous quarter’s allowance.

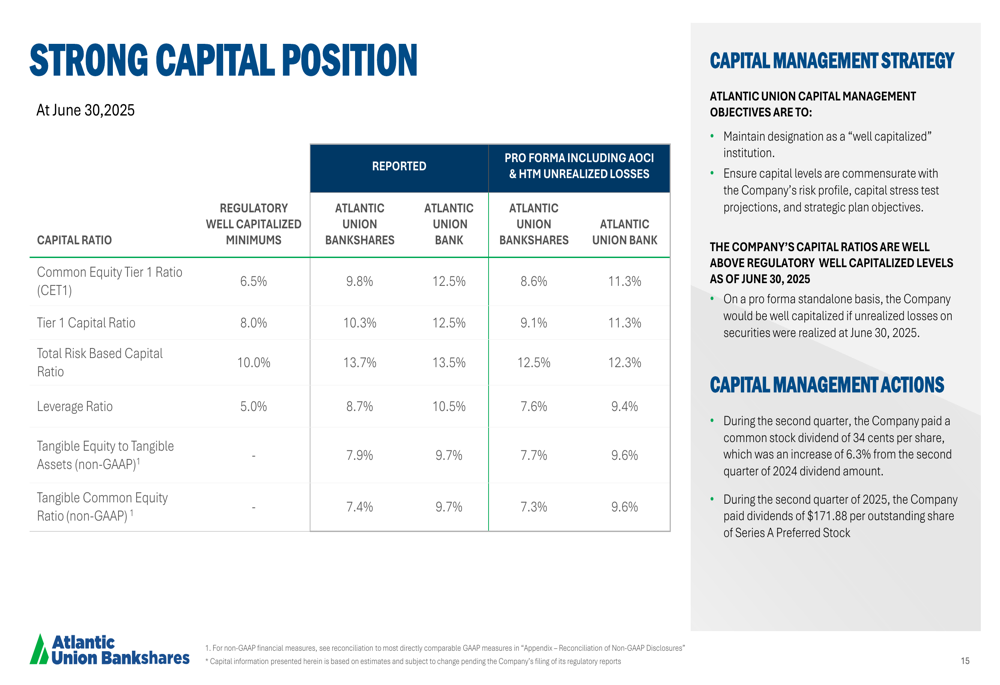

Atlantic Union maintains a strong capital position, with a Common Equity Tier 1 ratio of 9.8% and a total risk-based capital ratio of 13.7%, both well above regulatory requirements:

Strategic Initiatives

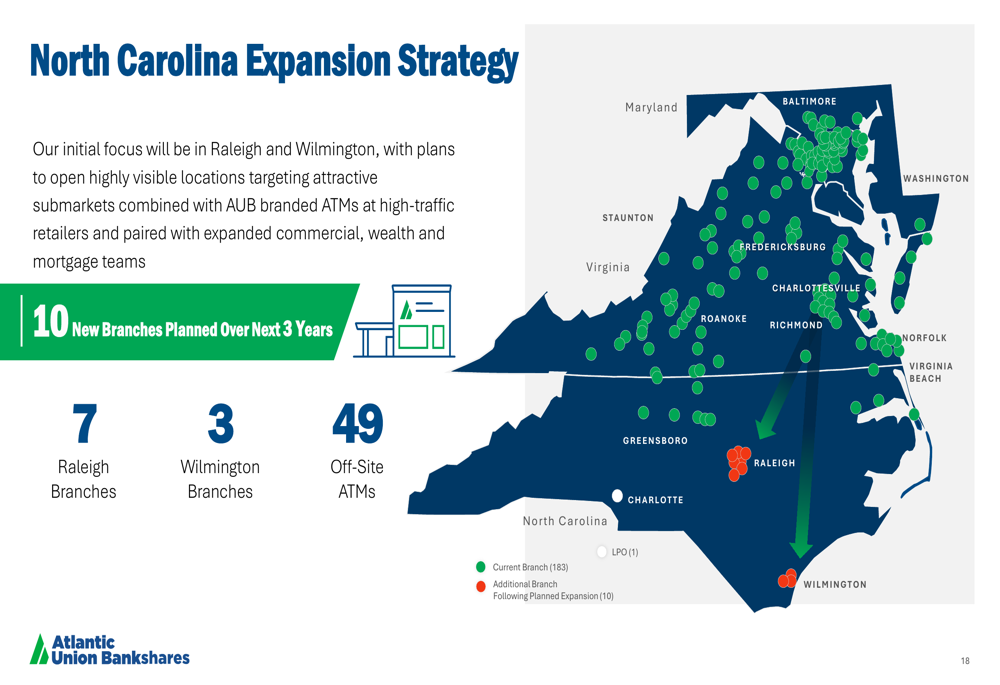

A key strategic focus for Atlantic Union is its expansion in North Carolina. The bank plans to open 10 new branches over the next three years, with 7 in Raleigh and 3 in Wilmington. This expansion will strengthen its presence in one of the fastest-growing regions in its footprint.

The North Carolina expansion strategy is illustrated in the following map:

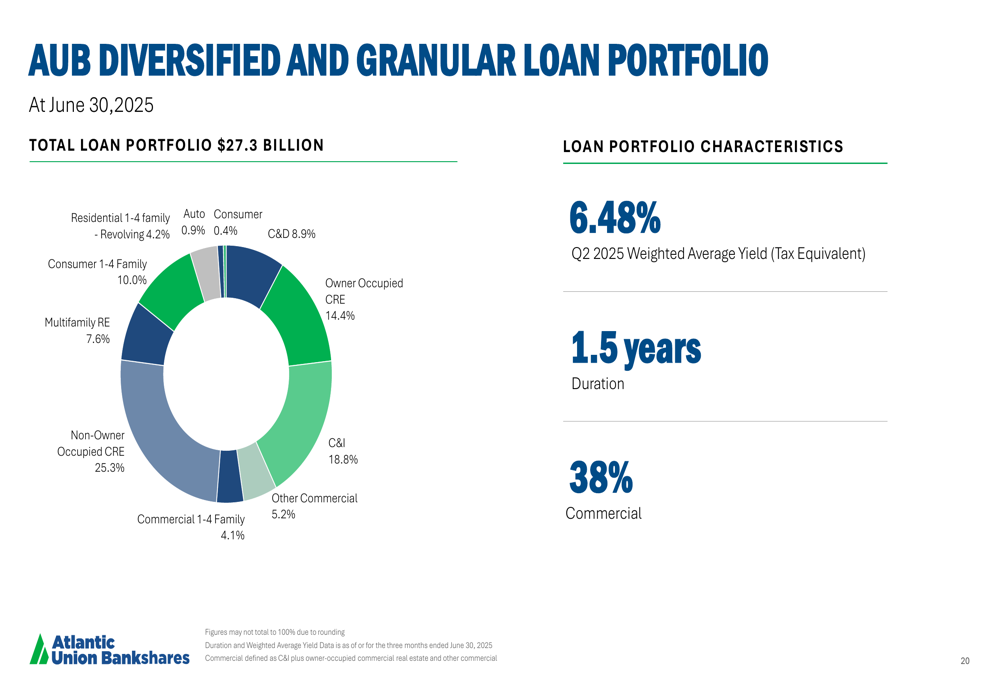

The bank’s loan portfolio remains well-diversified across various sectors, reducing concentration risk. Commercial real estate represents a significant portion, but is spread across different property types, including office, retail, industrial/warehouse, and multifamily.

As shown in the following breakdown of the loan portfolio composition:

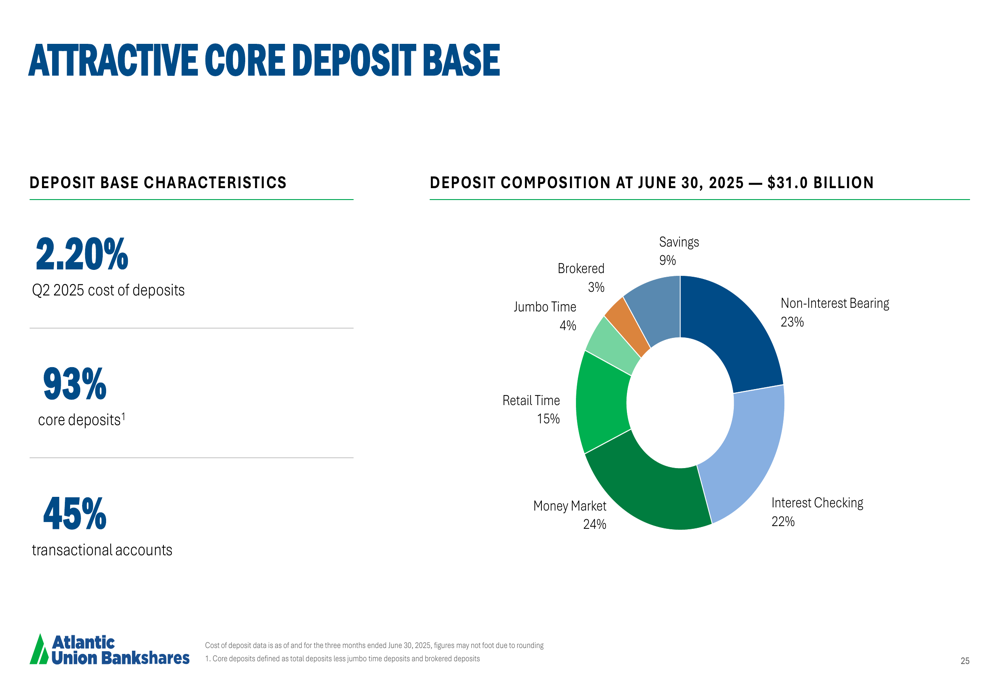

Atlantic Union’s deposit base is another area of strength, with 93% core deposits and 45% transactional accounts. The bank reduced its reliance on brokered deposits during the quarter, paying down approximately $340 million in this category.

The following chart illustrates the composition of the bank’s $31.0 billion deposit base:

Forward-Looking Statements

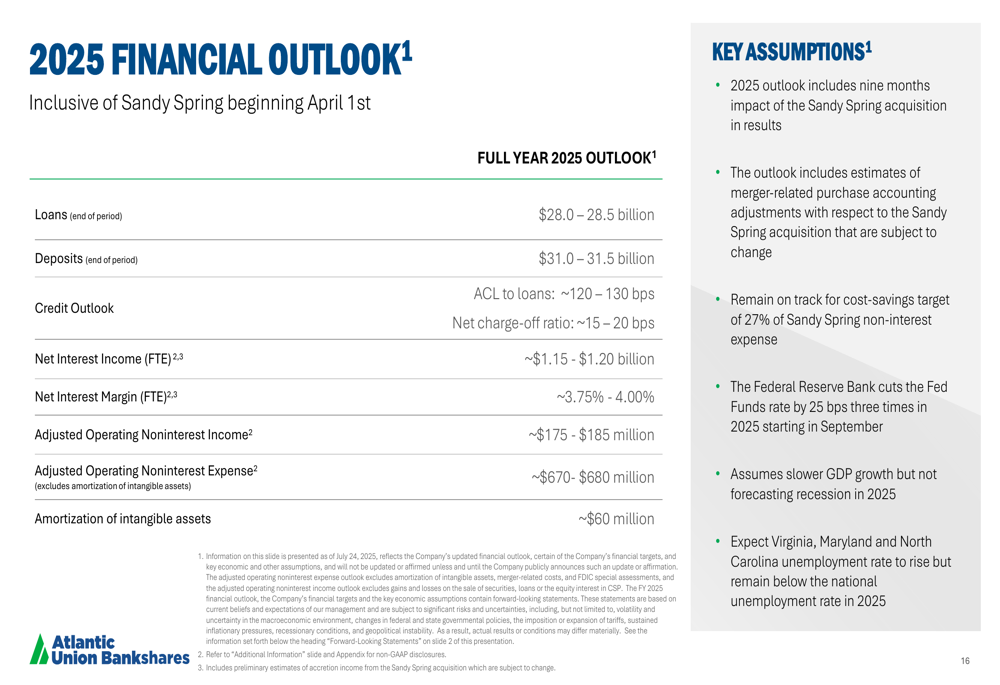

Looking ahead, Atlantic Union provided a comprehensive financial outlook for 2025, which includes the impact of the Sandy Spring acquisition that closed on April 1, 2025. The bank expects loan balances to reach $28.0-28.5 billion by year-end, with deposits projected at $31.0-31.5 billion.

The net interest margin is expected to remain strong at 3.75-4.00%, while the net charge-off ratio is projected to be 15-20 basis points, slightly higher than the current exceptionally low level but still indicating strong credit quality.

The bank’s full-year outlook is detailed in the following slide:

A key upcoming milestone is the Sandy Spring core systems conversion, scheduled for October 2025. The successful integration of this acquisition appears to be driving significant value, as evidenced by the strong Q2 results.

The bank’s performance represents a substantial improvement from Q1 2025, when it missed EPS expectations with earnings of $0.57 per share against a forecast of $0.72. The current results suggest that the Sandy Spring acquisition is already delivering the anticipated benefits, with significant operational synergies and expanded market presence.

With its strengthened position as the largest regional bank in the Mid-Atlantic region, solid capital ratios, strong credit quality, and clear expansion strategy, Atlantic Union appears well-positioned for continued growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.