Uxin shares drop 45% as predicted by InvestingPro’s Fair Value model

Introduction & Market Context

Atomera Inc (NASDAQ:ATOM) presented its Q2 2025 results on August 5, highlighting its continued focus on commercializing its Mears Silicon Technology (MST) in the semiconductor industry. Despite a growing customer base and technological advancements, the company reported zero revenue for the quarter, reflecting ongoing challenges in converting its intellectual property into commercial success.

The company's stock closed at $4.57 on the day of the presentation, showing a modest gain of 1.97% in regular trading and an additional 1.09% in after-hours trading. However, the stock remains significantly below its 52-week high of $17.55, indicating persistent investor concerns about the company's path to profitability.

Quarterly Performance Highlights

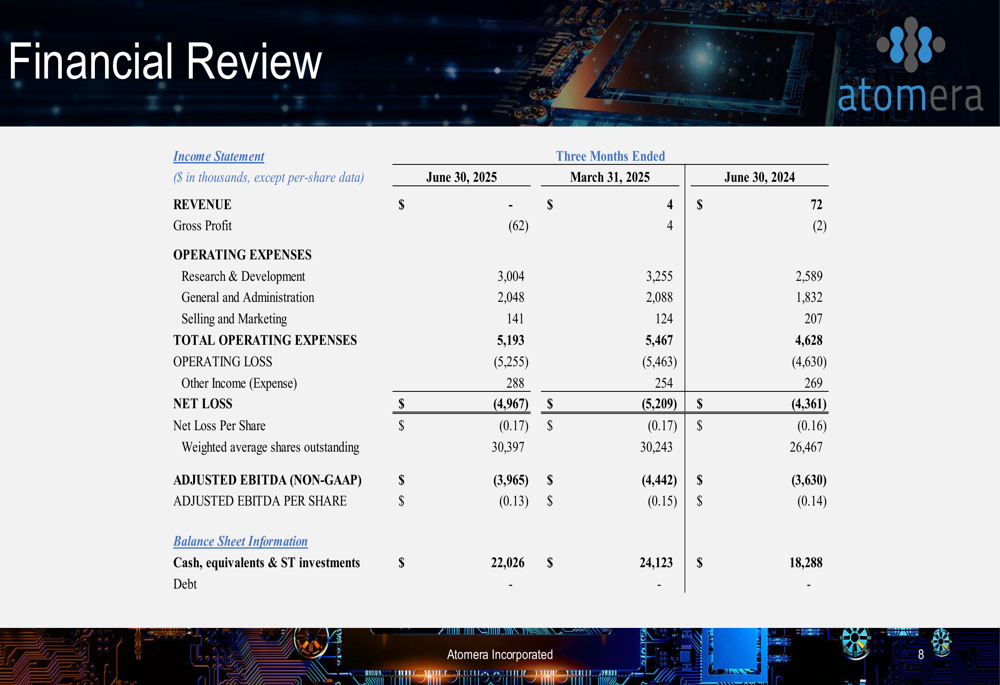

Atomera's Q2 2025 financial results revealed a continued absence of meaningful revenue generation. The company reported zero revenue for the quarter, down from $4,000 in Q1 2025 and $72,000 in the same quarter last year. This performance fell short of the company's previous guidance of $0-$50,000 for Q2.

The company posted a net loss of $4.97 million for the quarter, a slight improvement from the $5.21 million loss in Q1 2025 but worse than the $4.36 million loss in Q2 2024. This represents a continuation of Atomera's pattern of substantial quarterly losses as it invests in technology development without corresponding revenue.

As shown in the following financial review slide:

Customer Engagement Status

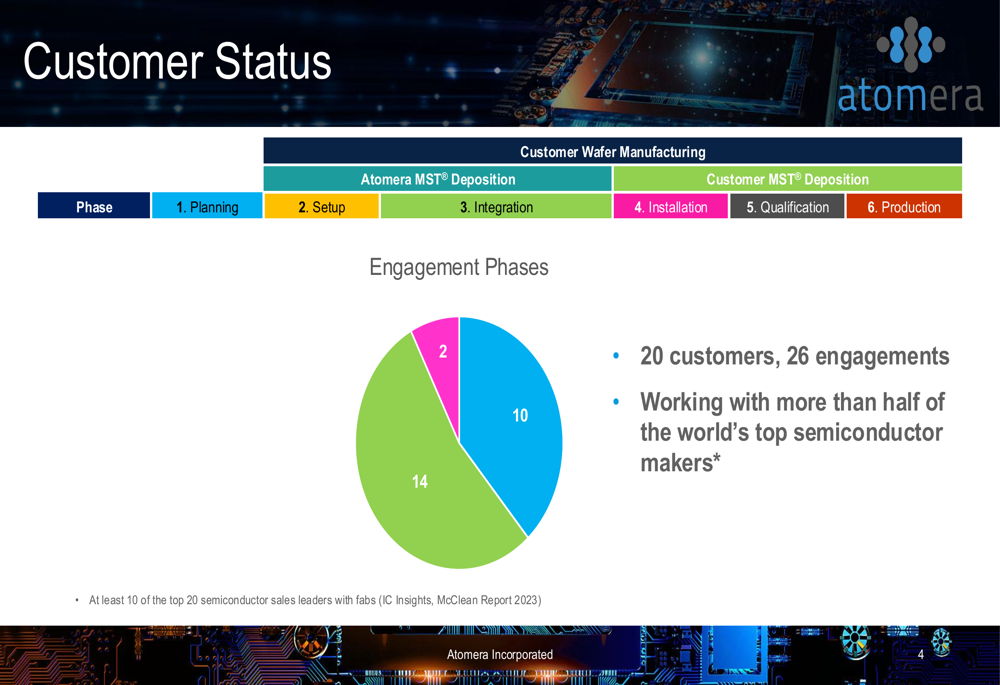

Despite the lack of revenue, Atomera maintains an active customer engagement pipeline. The company reported working with 20 customers across 26 engagements, including relationships with more than half of the world's top semiconductor manufacturers. These engagements are categorized across different phases of integration, with 14 customers in the Integration phase, 2 in Setup, and 10 in Installation.

The company's customer engagement model follows a six-phase approach from Planning to Production, with most customers currently in the middle phases. The challenge remains converting these engagements into Phase 5 (Qualification) and Phase 6 (Production), which would generate meaningful licensing revenue.

The following slide illustrates Atomera's current customer distribution across various engagement phases:

Technology Focus and IP Portfolio

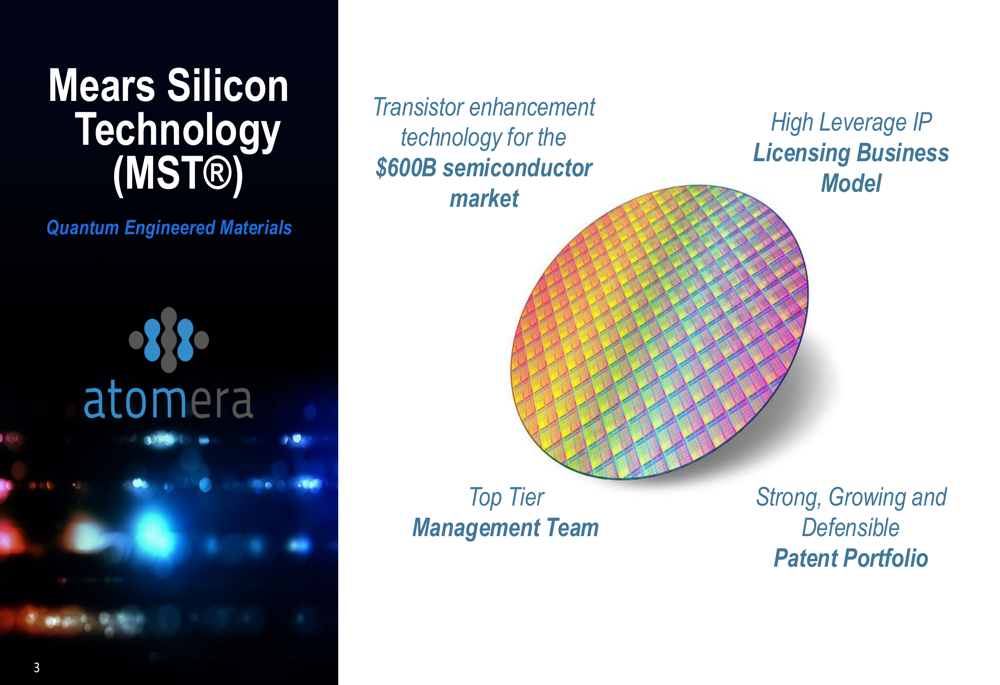

Atomera continues to position its MST technology as a quantum-engineered material enhancement for the $600 billion semiconductor market. The company's presentation highlighted four key focus areas: Power SP/SPX, RF-SOI, Advanced Nodes, and DRAM.

The company's core technology offering is visualized in this slide:

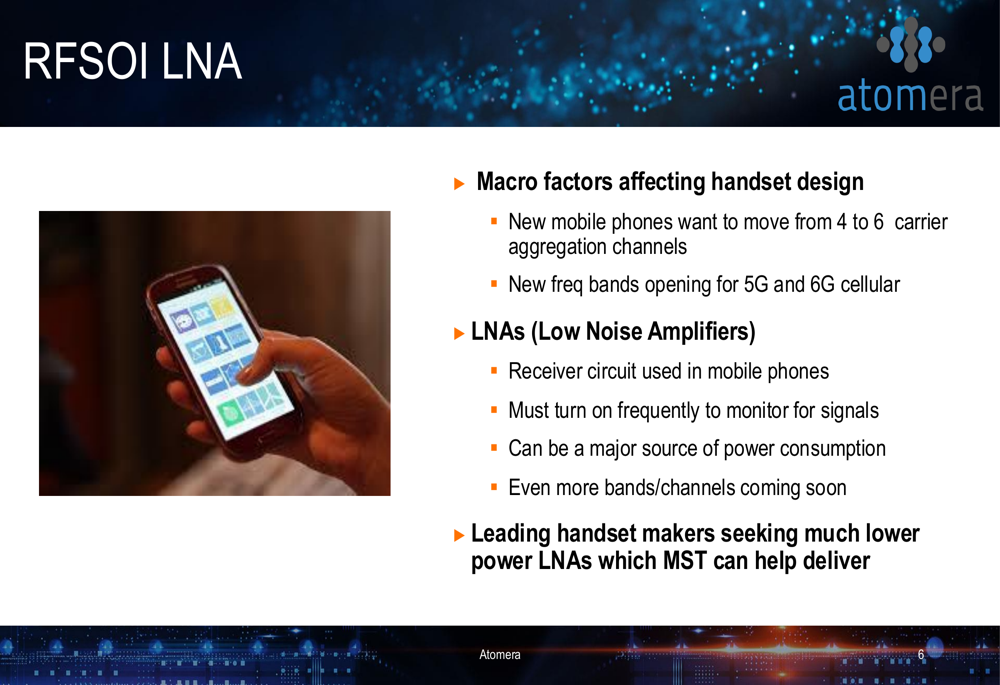

A particular emphasis was placed on RFSOI Low Noise Amplifier (LNA) applications for mobile phones. Atomera highlighted industry trends toward increased carrier aggregation channels in new mobile phones and the opening of new frequency bands for 5G and 6G cellular networks. The company positions its MST technology as a solution for reducing power consumption in LNAs, which are critical receiver circuits in mobile phones that must frequently activate to monitor for signals.

The following slide details Atomera's focus on RFSOI LNA technology:

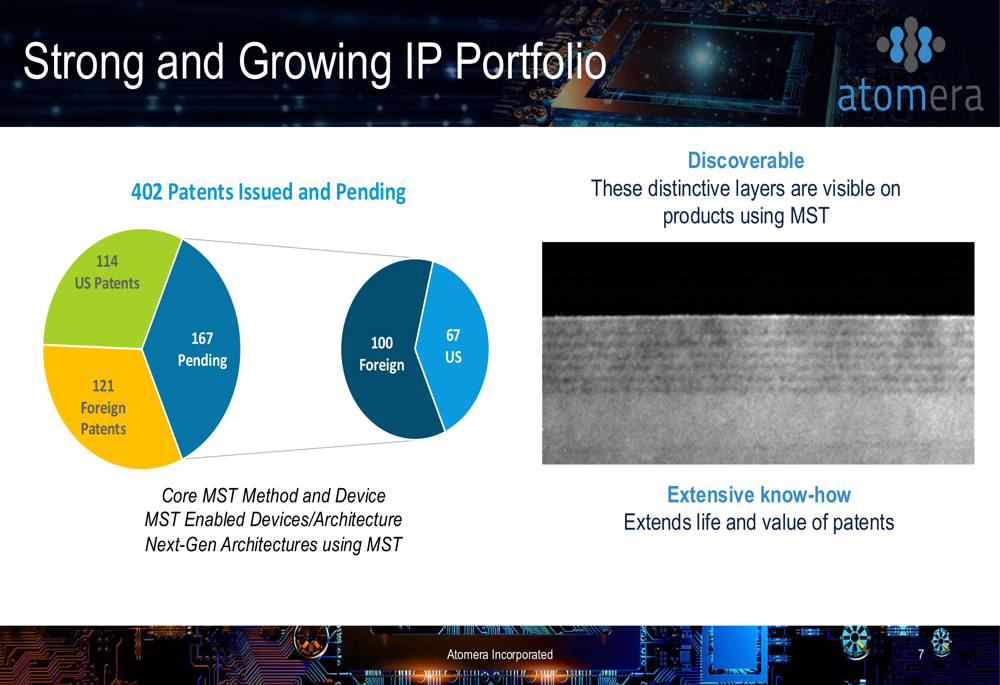

Atomera's intellectual property position remains strong, with 402 patents issued and pending (114 US patents, 121 foreign patents, and 167 pending). The company emphasized that its technology is "discoverable" through visible distinctive layers on products using MST, providing additional protection beyond the patents themselves.

The company's patent portfolio is illustrated in this slide:

Financial Analysis

Atomera's financial position continues to show the strain of ongoing research and development without corresponding revenue. The company's cash, equivalents, and short-term investments stood at $22.03 million as of June 30, 2025, down from $24.12 million at the end of Q1 2025 but up from $18.29 million a year earlier.

The quarterly cash burn of approximately $2.1 million suggests that at the current rate, Atomera has roughly 10-11 quarters of runway remaining. This represents a slight improvement in burn rate compared to the previous quarter but still highlights the urgency of commercializing the company's technology.

In the Q1 2025 earnings call, Atomera had missed its EPS forecast, reporting a loss of $0.17 per share versus an expected loss of $0.14. The Q2 results show a continued pattern of financial challenges, though the sequential improvement in net loss may indicate some success in controlling costs.

Forward-Looking Statements

Atomera's presentation maintained an optimistic outlook despite the financial challenges. The company's mission statement emphasizes collaboration with customers to integrate MST technology for mutual financial benefit. However, the presentation did not provide specific revenue guidance for upcoming quarters or a clear timeline for reaching commercial production with key customers.

The company's technology focus areas, particularly in mobile phone applications, suggest potential growth opportunities as the industry moves toward 5G and 6G networks. The emphasis on power efficiency in LNAs addresses a genuine industry need, but the timeline for converting this opportunity into revenue remains uncertain.

As shown in the company's mission statement slide:

For investors, Atomera remains a high-risk, high-potential play in the semiconductor space. The company's extensive patent portfolio and relationships with major industry players provide a foundation for potential success, but the persistent lack of revenue and ongoing cash burn highlight the challenges ahead in commercializing its innovative technology.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.