TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

AT&T Inc (NYSE:T) released its second quarter 2025 earnings presentation on July 23, highlighting continued momentum in its core growth areas despite facing premarket trading pressure. The telecommunications giant reported a 1.1% year-over-year increase in service revenue and a 3.5% rise in adjusted EBITDA, demonstrating progress on its strategic priorities.

Shares were trading down 1.53% in premarket at $27.00, following the previous day’s close of $27.42, suggesting investors may have had higher expectations after the company’s Q1 results slightly missed analyst projections on earnings per share.

Quarterly Performance Highlights

AT&T’s presentation emphasized strong subscriber growth across its strategic focus areas, particularly in mobility and fiber segments, which continue to be the cornerstones of the company’s transformation strategy.

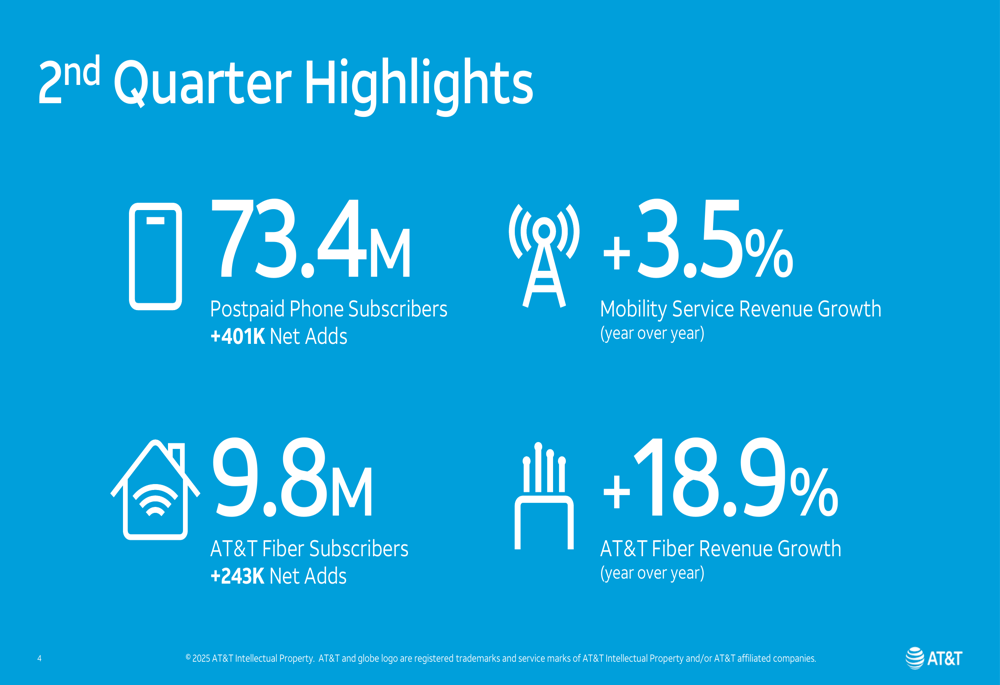

As shown in the following quarterly highlights:

The company added 401,000 postpaid phone subscribers in Q2, bringing its total postpaid phone subscriber base to 73.4 million. AT&T Fiber continued its strong performance with 243,000 net additions, reaching 9.8 million total subscribers. These subscriber gains translated into solid revenue growth, with mobility service revenue increasing 3.5% year-over-year and AT&T Fiber revenue surging 18.9%.

Detailed Financial Analysis

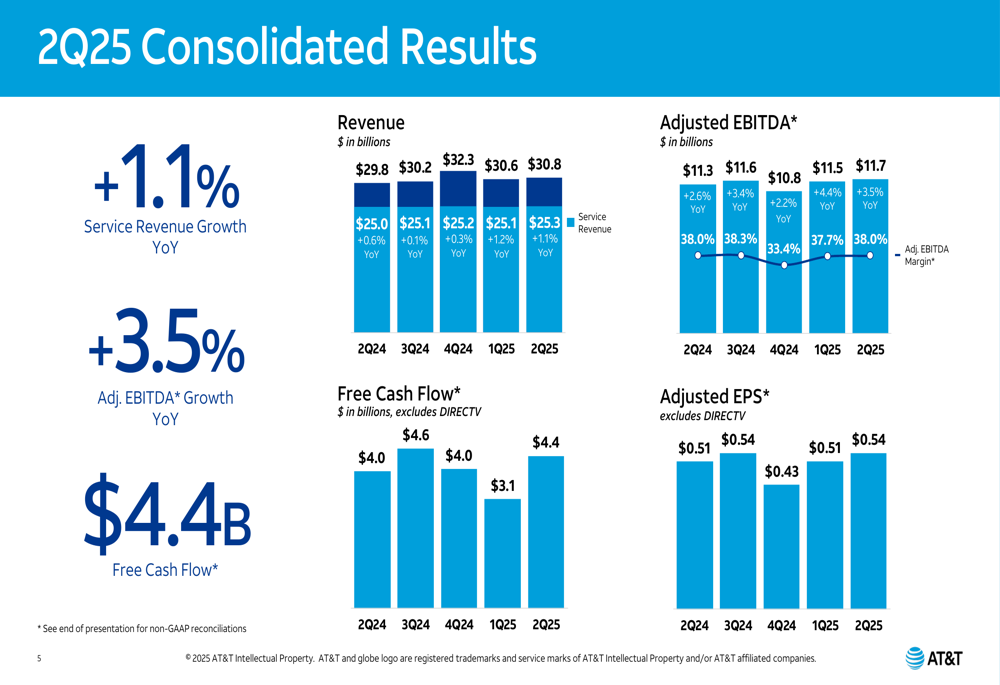

AT&T’s consolidated financial results showed improvement across key metrics compared to both the previous quarter and the same period last year. The company’s adjusted EPS of $0.54 represents an improvement from Q1 2025’s $0.51, which had missed analyst expectations.

The following chart illustrates AT&T’s consolidated financial performance:

Free cash flow remained robust at $4.4 billion, showing significant improvement from the $3.1 billion reported in Q1 2025. Service revenue reached $25.3 billion, while adjusted EBITDA grew to $11.7 billion with a margin of 38.0%.

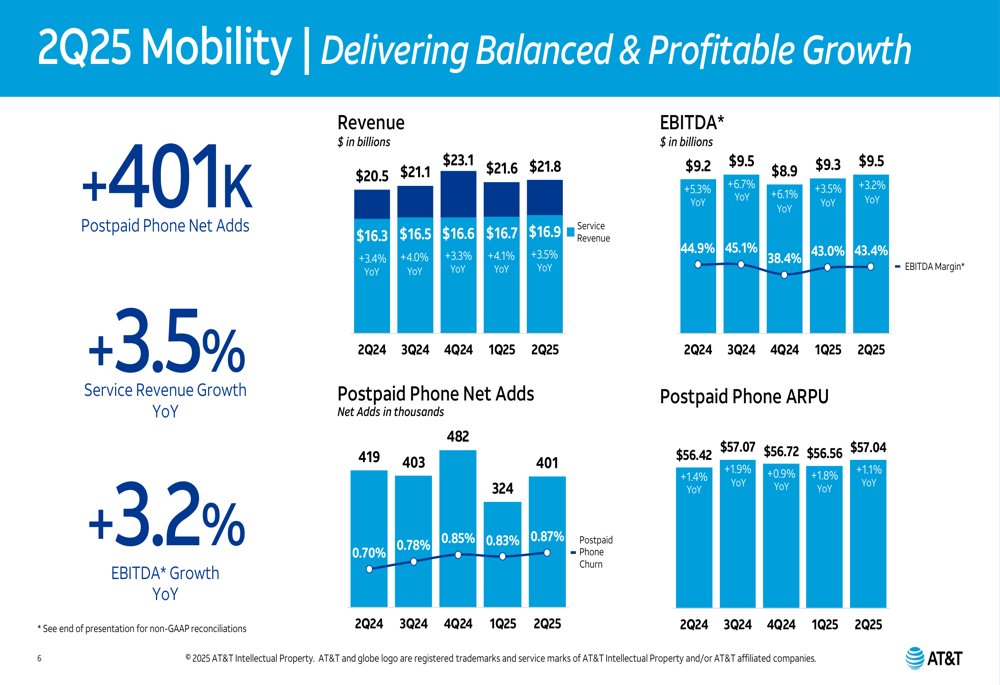

In the mobility segment, AT&T continued to demonstrate balanced growth with service revenue increasing 3.5% year-over-year to $16.9 billion:

The mobility segment’s adjusted EBITDA grew 3.2% year-over-year to $9.5 billion, with a margin of 43.4%. However, postpaid phone churn increased slightly to 0.87%, up from 0.83% in Q1 2025 and 0.70% in the year-ago quarter, potentially signaling increased competitive pressure in the wireless market.

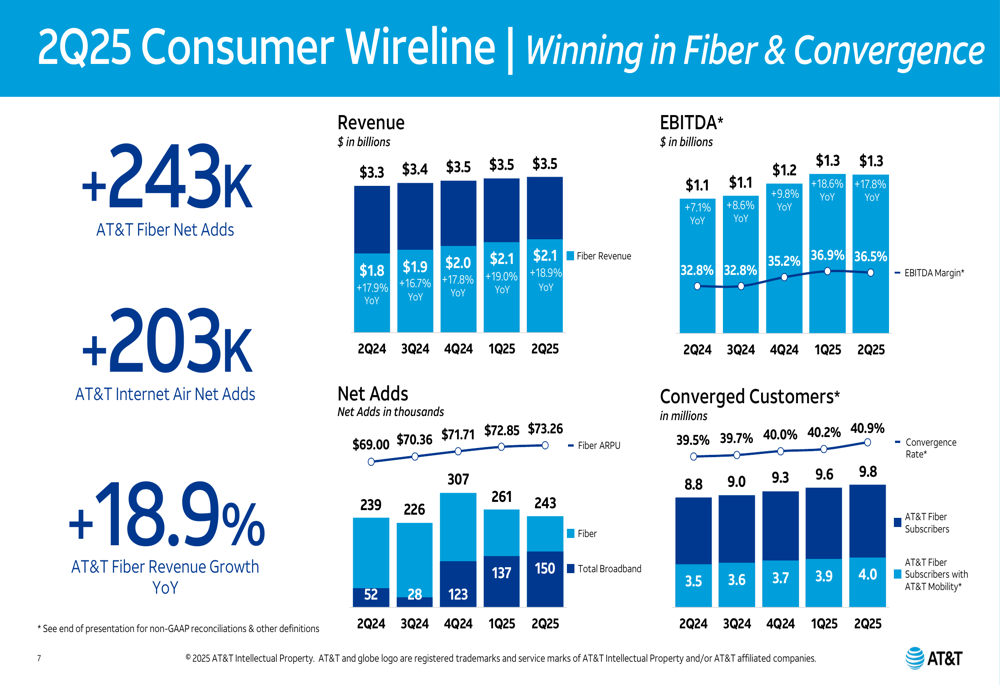

AT&T’s consumer wireline business, anchored by its fiber offerings, showed particularly strong results:

The consumer wireline segment posted impressive 18.9% year-over-year revenue growth, reaching $2.1 billion. The company’s converged customer base (those subscribing to both wireless and fiber services) continued to expand, reaching 9.8 million in Q2 2025.

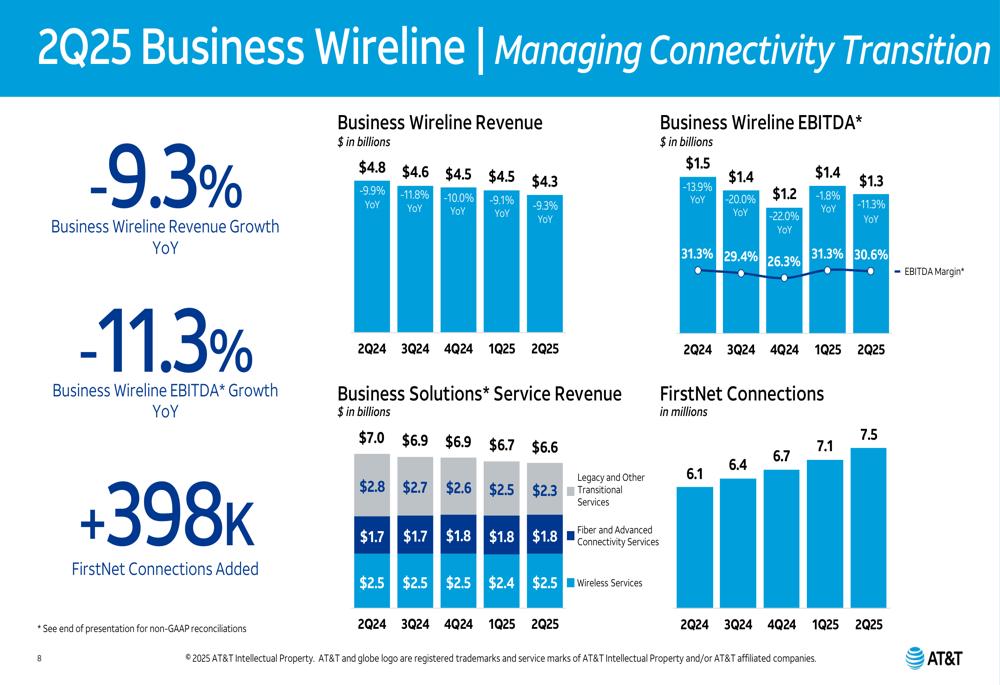

The business wireline segment remained a challenge, with revenue declining 9.3% year-over-year:

Despite the revenue decline, AT&T maintained relatively stable EBITDA margins in this segment at 30.6%, reflecting ongoing cost management efforts. The company added 398,000 FirstNet connections, highlighting continued traction in the public safety sector.

Strategic Initiatives

AT&T’s presentation outlined three key business priorities for 2025: growing durable 5G and Fiber relationships, operational efficiency, and deliberate capital allocation. The company emphasized its disciplined go-to-market strategy and focus on increasing converged customer penetration.

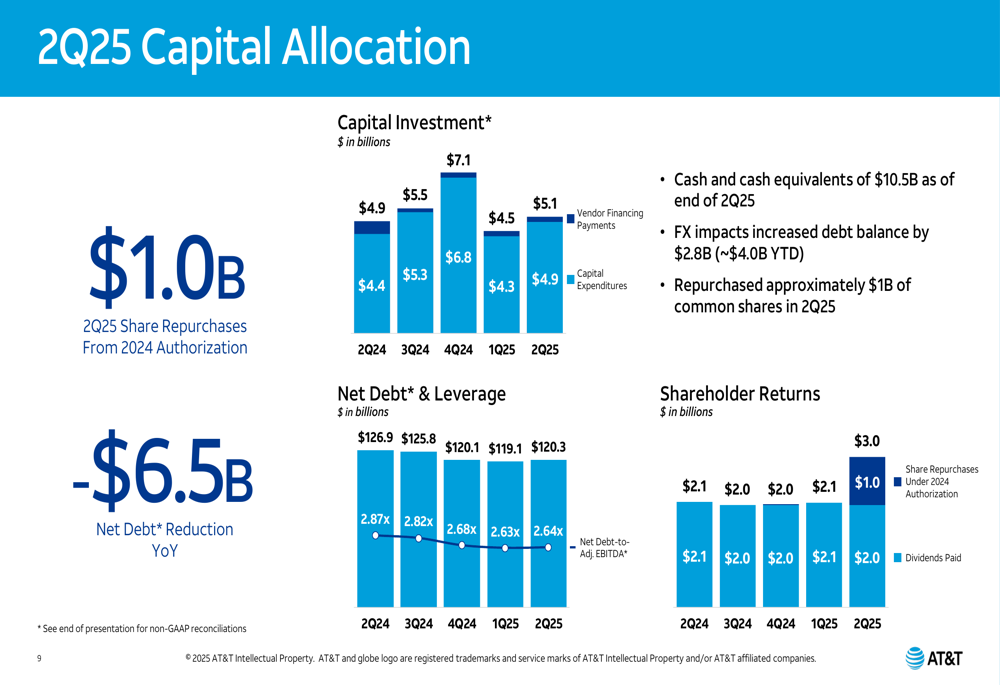

On the capital allocation front, AT&T continued its share repurchase program while maintaining its dividend:

The company repurchased approximately $1 billion of common shares in Q2 2025 under its 2024 authorization and paid $2.0 billion in dividends. AT&T also reported $10.5 billion in cash and cash equivalents at the end of Q2 and achieved a $6.5 billion year-over-year reduction in net debt, despite a $2.8 billion increase in debt balance due to foreign exchange impacts.

Forward-Looking Statements

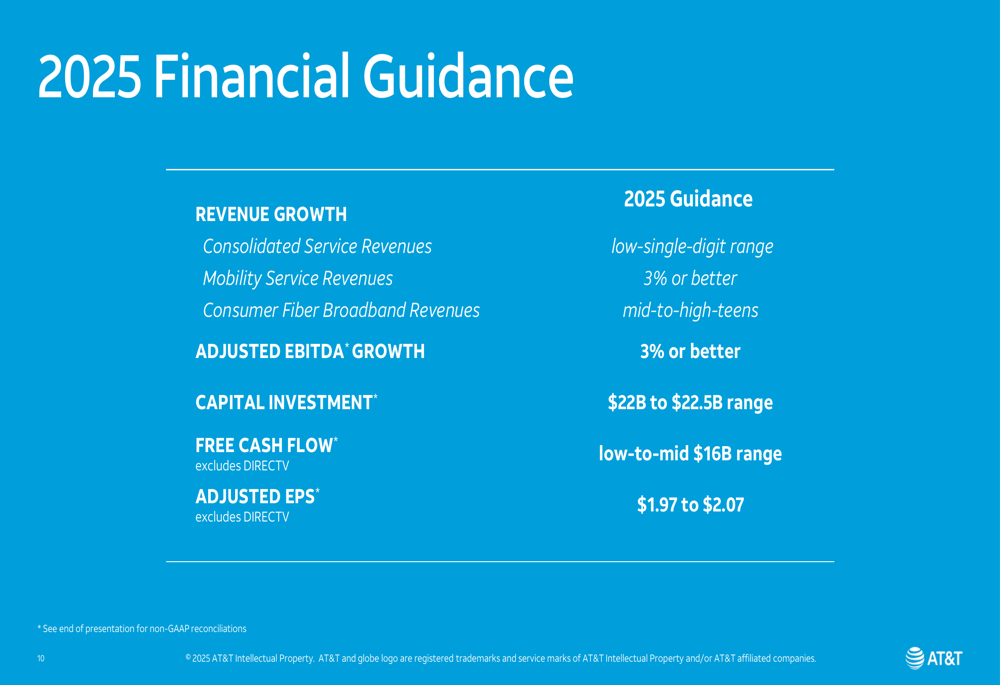

AT&T reaffirmed its financial guidance for 2025, maintaining confidence in its ability to deliver on its strategic objectives:

The company expects consolidated service revenue growth in the low-single-digit range, with mobility service revenue growing at 3% or better and consumer fiber broadband revenue increasing in the mid-to-high teens. AT&T projects adjusted EBITDA growth of 3% or better, capital investment in the $22 billion to $22.5 billion range, and free cash flow in the low-to-mid $16 billion range.

Analyst Perspectives

While AT&T’s Q2 results showed improvement from Q1, the premarket trading decline suggests investors may be concerned about rising churn rates in the mobility segment and the continued decline in business wireline revenue. The company’s ability to maintain its adjusted EBITDA margin at 38.0%, however, demonstrates effective cost management despite these challenges.

The $10 billion share repurchase authorization announced in Q1 2025 and continued in Q2 reflects management’s confidence in AT&T’s financial position and commitment to returning value to shareholders. With $1 billion of shares repurchased in Q2, the company appears to be executing this program at a measured pace while balancing other capital allocation priorities.

AT&T’s focus on expanding its fiber footprint and growing its 5G customer base remains central to its long-term strategy, with the company targeting cost savings of over $3 billion by the end of 2027 through increased operational efficiency and the integration of AI technologies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.