Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Avanos Medical (TASE:BLWV) Inc (NYSE:AVNS) shares plummeted 12.89% on Tuesday after the medical device company presented its second-quarter 2025 earnings results, which showed modest revenue growth but a significant decline in profitability. The company maintained its full-year guidance despite the challenges.

Quarterly Performance Highlights

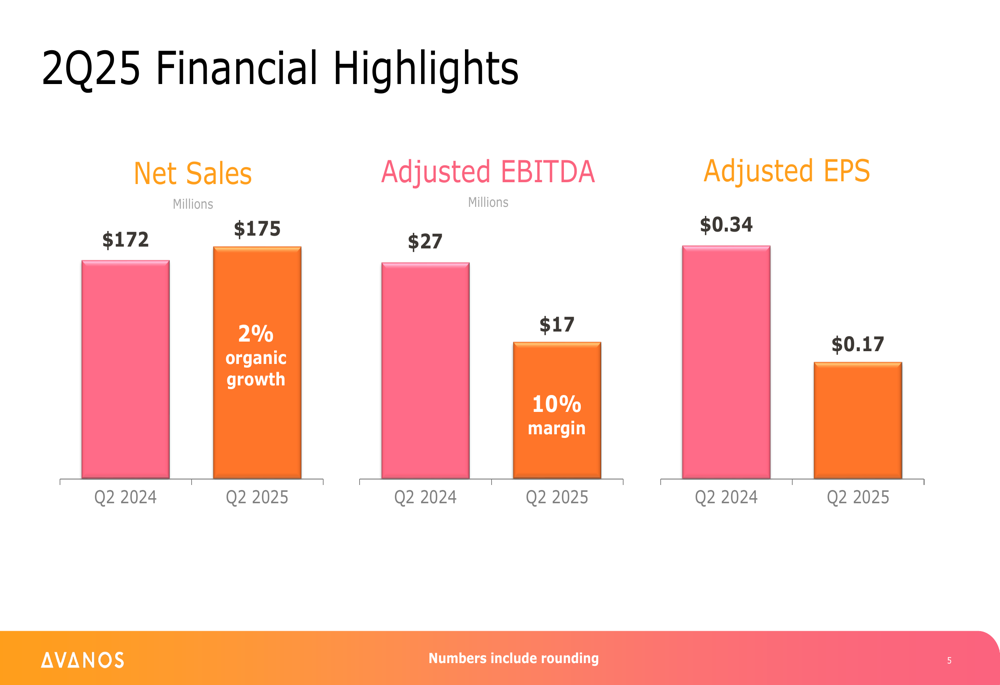

Avanos reported Q2 2025 net sales of $175 million, representing a 2% organic growth compared to $172 million in the same period last year. However, adjusted EBITDA fell to $17 million from $27 million in Q2 2024, and adjusted earnings per share dropped to $0.17 from $0.34 a year earlier.

CEO Dave Pacitti characterized the quarter as "strong" and building "momentum for back half of the year," despite the significant year-over-year profit decline. The company also recorded a non-cash goodwill impairment charge of $77 million in the quarter, which was excluded from adjusted figures.

As shown in the following financial highlights chart:

Segment Analysis

Avanos operates through two primary business segments following the divestiture of its Hyaluronic Acid product line. Both segments showed organic growth, though with different profitability trajectories.

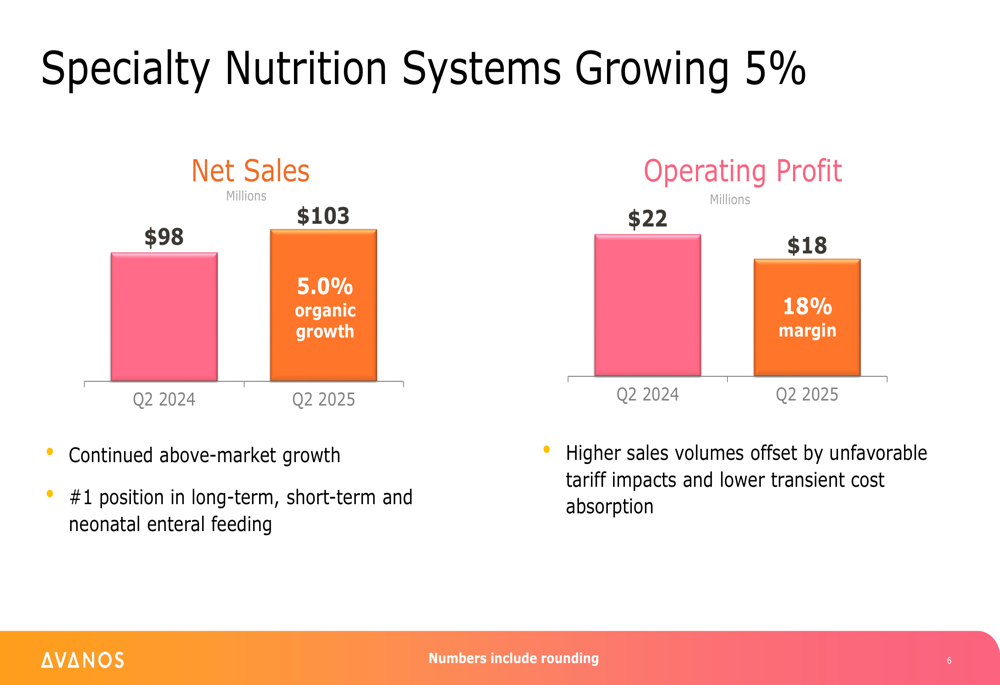

The Specialty Nutrition Systems segment, which represents the company’s largest revenue stream, posted sales of $103 million in Q2 2025, a 5.0% organic growth compared to $98 million in Q2 2024. However, operating profit declined to $18 million (18% margin) from $22 million in the prior year. The company cited "unfavorable tariff impacts and lower transient cost absorption" as factors offsetting the higher sales volumes.

The company maintains a "#1 position in long-term, short-term and neonatal enteral feeding" within this segment, as illustrated in the following chart:

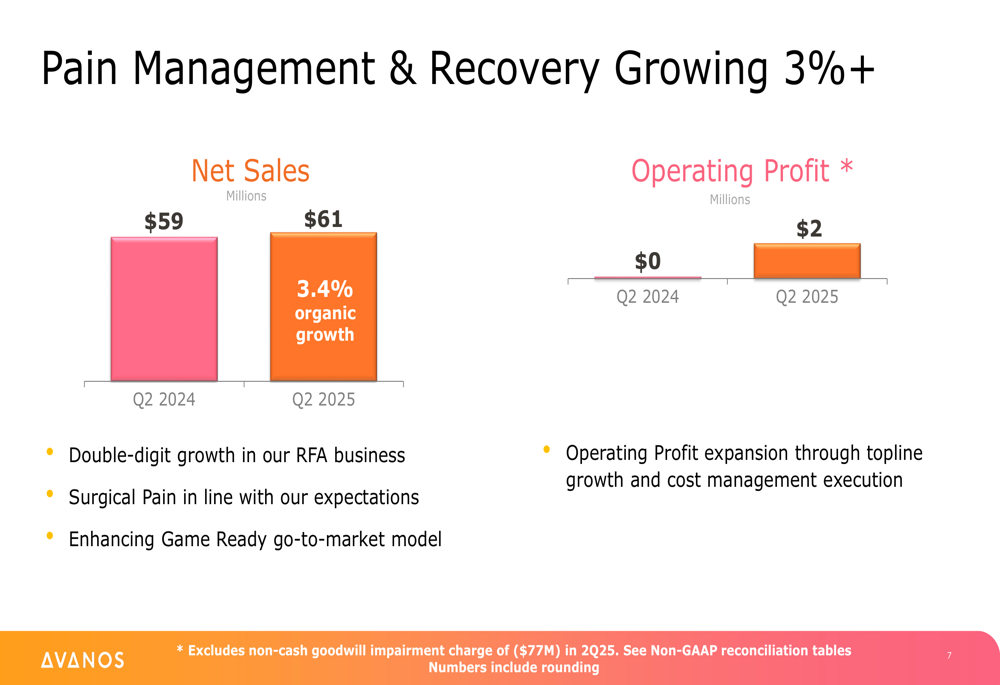

The Pain Management & Recovery segment showed more positive momentum, with net sales of $61 million in Q2 2025, representing 3.4% organic growth compared to $59 million in Q2 2024. Operating profit improved to $2 million from $0 million in the prior year. The company highlighted "double-digit growth in our RFA business" as a key driver of performance.

The segment’s performance is detailed in this chart:

Financial Position & Outlook

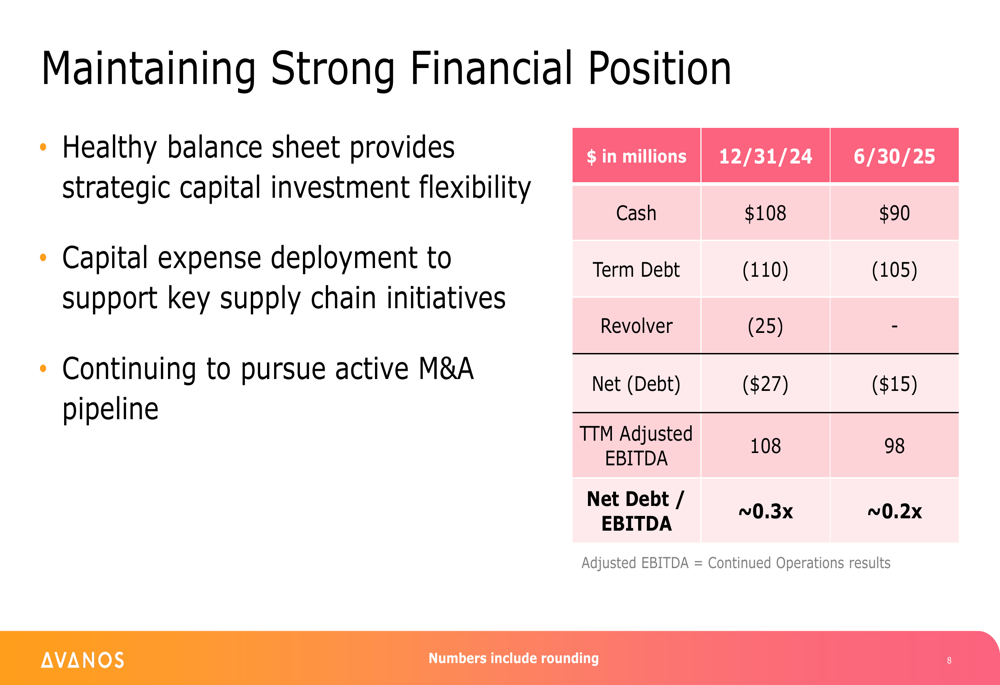

Despite the profit challenges, Avanos maintains a strong balance sheet with $90 million in cash as of June 30, 2025, and net debt of just $15 million. The company’s net debt to EBITDA ratio stands at approximately 0.2x, providing what management described as "strategic capital investment flexibility."

As shown in the financial position summary:

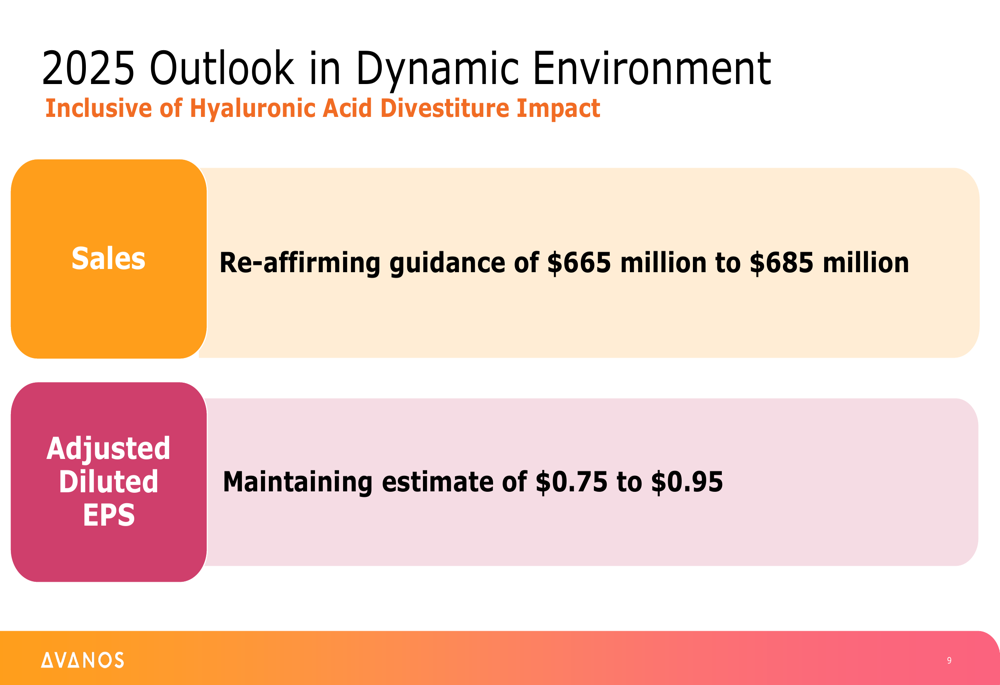

For the full year 2025, Avanos reaffirmed its sales guidance of $665 million to $685 million and maintained its adjusted diluted EPS forecast of $0.75 to $0.95. This guidance factors in the impact of the Hyaluronic Acid divestiture.

The outlook appears consistent with the company’s Q1 2025 guidance, when it also projected the same revenue and EPS ranges. In that quarter, Avanos had exceeded analyst expectations with an EPS of $0.26 against a forecast of $0.18, and revenue of $167.5 million versus an expected $162 million.

Strategic Initiatives

Avanos is continuing its transformation journey, with management "assessing additional cost opportunities and optimization initiatives" to extend the benefits of previous restructuring efforts. The company completed the divestiture of its Hyaluronic Acid product line during the quarter, which management indicated would enhance focus on the two strategic segments.

The company is also pursuing an active M&A pipeline and deploying capital to support key supply chain initiatives. For the Pain Management & Recovery segment, Avanos is enhancing the go-to-market model for its Game Ready product line.

Interim CFO Jason Pickett, who reassumed the position effective August 1, 2025, presented the financial results. The leadership team also includes Scott Galovan, SVP and Chief Financial Officer, who participated in the Q&A session.

The significant stock price decline following the presentation suggests investors were disappointed by the substantial year-over-year profit decline and the goodwill impairment charge, despite the modest revenue growth and maintained guidance. The company’s shares closed at $11.25, approaching the 52-week low of $9.73 and well below the 52-week high of $25.36.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.