S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Avista Corporation (NYSE:AVA) reported its first-quarter 2025 earnings on May 7, revealing a 7.7% year-over-year increase in consolidated earnings per share (EPS). The utility company, which closed at $41.80 on May 6, presented results that demonstrated continued momentum following its Q4 2024 performance, when the company exceeded revenue expectations despite missing EPS forecasts.

The company’s stock, which has traded between $33.45 and $43.09 over the past 52 weeks, showed minimal movement in premarket trading with a slight 0.07% increase. Avista’s presentation highlighted strong utility segment performance and regulatory progress across multiple states as key drivers for the quarter.

Quarterly Performance Highlights

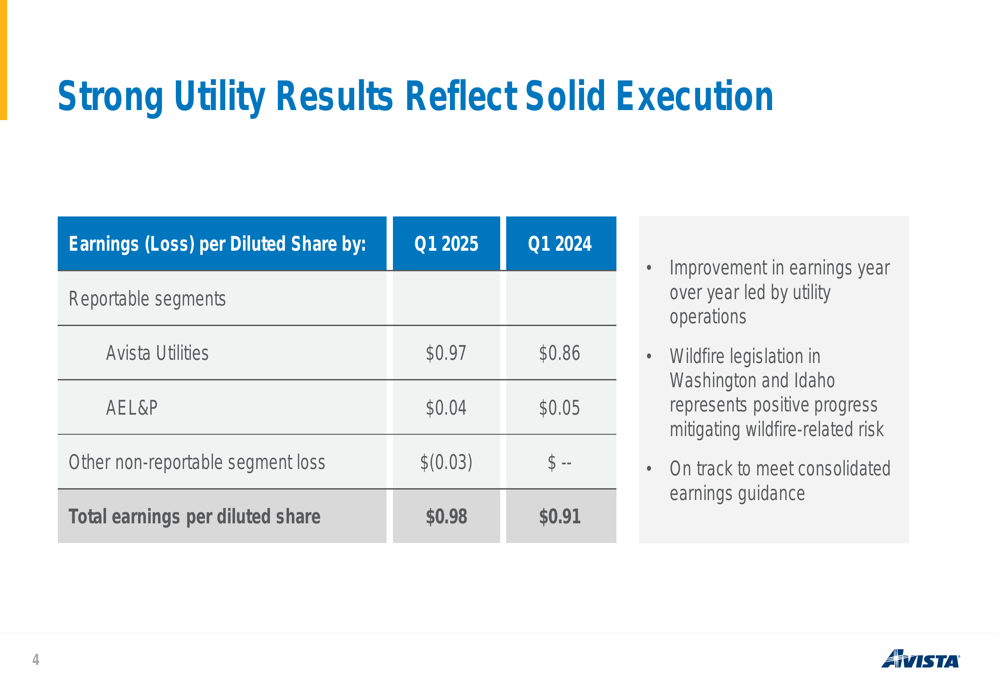

Avista reported consolidated earnings of $0.98 per diluted share for Q1 2025, compared to $0.91 in the same period last year. This improvement was primarily driven by the company’s core utility operations, with the Avista Utilities segment contributing $0.97 per share, up from $0.86 in Q1 2024.

As shown in the following breakdown of earnings by segment:

The company’s Alaska Electric Light and Power (AEL&P) segment contributed $0.04 per share, slightly down from $0.05 in the prior year. Meanwhile, other non-reportable segments posted a loss of $0.03 per share, compared to breakeven results in Q1 2024.

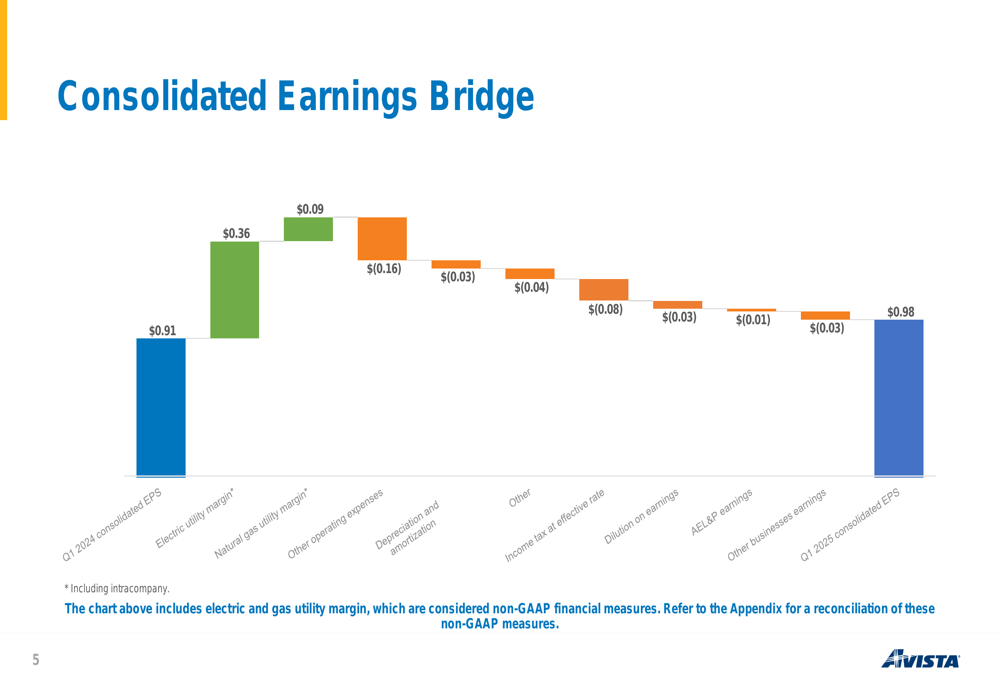

A detailed analysis of the factors contributing to the EPS change reveals that increased electric and natural gas utility margins were the primary drivers of growth, partially offset by higher operating expenses and tax impacts:

"Improvement in earnings year over year led by utility operations," noted the company in its presentation, adding that recent wildfire legislation in Washington and Idaho represents "positive progress mitigating wildfire-related risk."

Regulatory Developments

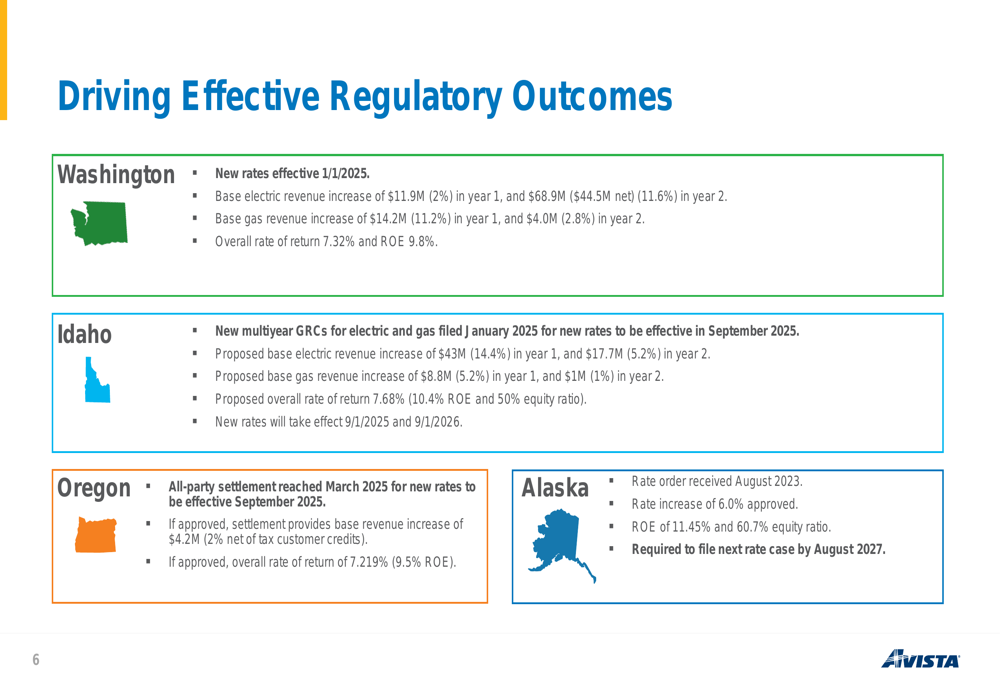

Avista highlighted significant regulatory progress across its service territories, which provides greater certainty for the company’s revenue streams and investment plans. In Washington, the company secured approval for new rates effective January 1, 2025, including a base electric revenue increase of 11.6% in year two and a base gas revenue increase of 11.2% in year one.

The regulatory landscape across all of Avista’s territories shows a pattern of constructive outcomes:

In Idaho, Avista has filed new multiyear general rate cases for both electric and gas, proposing base electric revenue increases of 14.4% in year one and 5.2% in year two, with new rates expected to take effect on September 1, 2025. In Oregon, the company reached an all-party settlement in March 2025 that, if approved, would provide a base revenue increase of 4.2%.

These regulatory outcomes are crucial for Avista’s ability to recover costs associated with its ambitious capital expenditure program while maintaining its financial health and delivering returns to shareholders.

Capital Investment Strategy

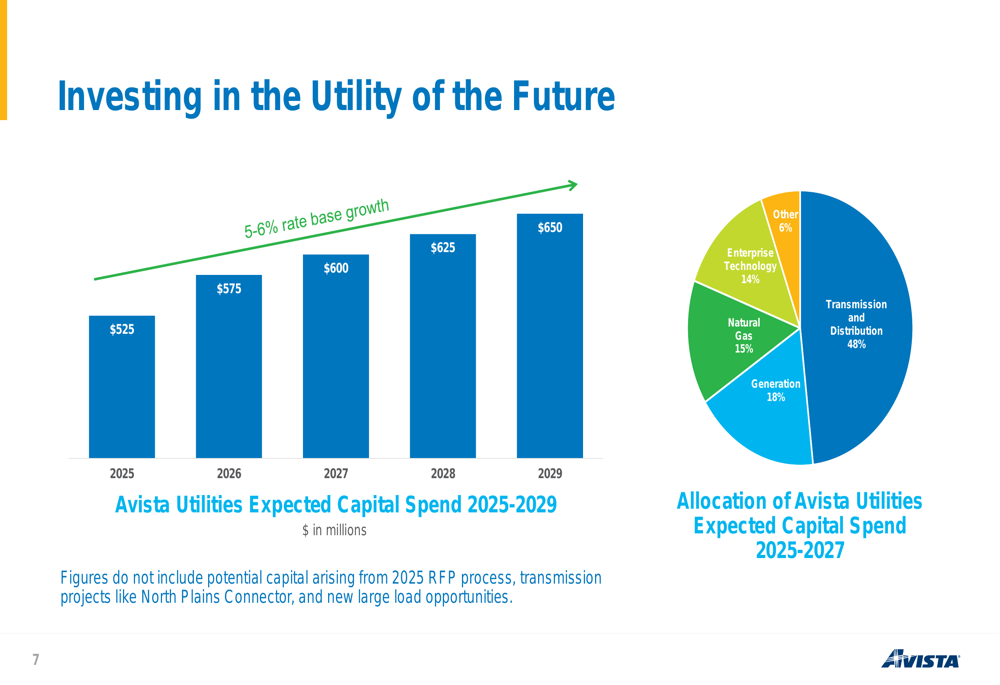

Avista outlined an aggressive five-year capital expenditure plan totaling approximately $3 billion from 2025 through 2029. The investment strategy shows a steady annual increase in capital spending, starting at $525 million in 2025 and growing to $650 million by 2029.

The company’s detailed capital expenditure plan and allocation is illustrated in the following chart:

Nearly half (48%) of the planned capital spend for 2025-2027 is allocated to transmission and distribution infrastructure, with generation (18%), natural gas (15%), and enterprise technology (14%) making up most of the remainder. The company noted that these figures do not include potential additional capital arising from the 2025 RFP process, transmission projects like the North Plains Connector, or new large load opportunities.

This substantial investment program underscores Avista’s commitment to modernizing its infrastructure and addressing the evolving needs of its service territories, particularly as the energy landscape continues to transform.

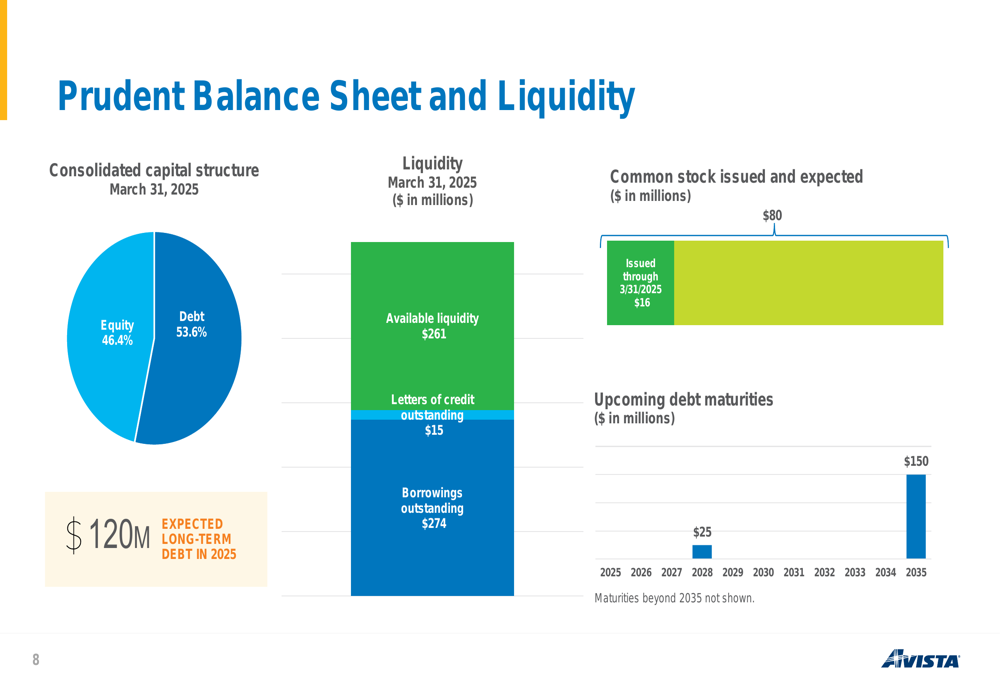

Financial Position & Outlook

Avista maintains a balanced capital structure with 46.4% equity and 53.6% debt. The company reported available liquidity of $261 million as of March 31, 2025, with $15 million in outstanding letters of credit and $274 million in borrowings.

The company’s capital structure and liquidity position are summarized in the following chart:

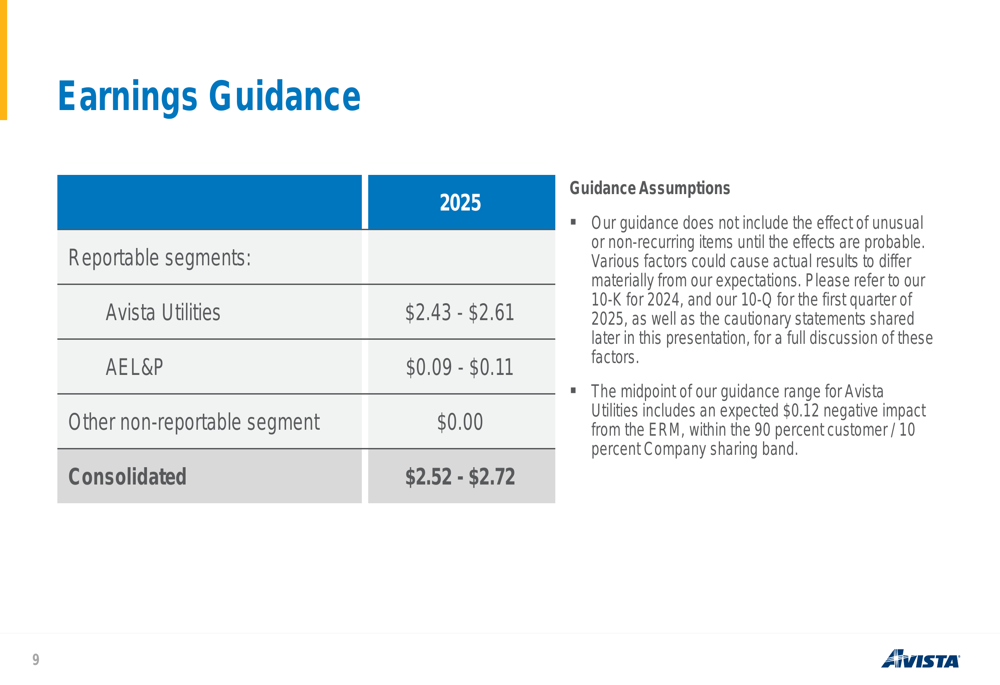

Looking ahead, Avista reaffirmed its 2025 earnings guidance of $2.52 to $2.72 per diluted share, consistent with the outlook provided in its Q4 2024 earnings report. The guidance breakdown by segment shows Avista Utilities contributing between $2.43 and $2.61, with AEL&P adding $0.09 to $0.11 per share.

The company’s earnings guidance and assumptions are detailed in the following table:

"Our guidance does not include the effect of unusual or non-recurring items until the effects are probable," the company noted, adding that the midpoint of its guidance range for Avista Utilities includes an expected $0.12 negative impact from the Energy Recovery (NASDAQ:ERII) Mechanism (ERM).

Avista’s Q1 2025 results position the company well to achieve its full-year targets, supported by favorable regulatory outcomes and a clear capital investment strategy. The utility’s focus on infrastructure modernization and regulatory engagement continues to provide a foundation for stable, long-term growth in an evolving energy landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.