Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

AVITA Medical (TASE:BLWV) Ltd (NASDAQ:RCEL) presented its Q1 2025 earnings on May 8, 2025, outlining an ambitious growth strategy and market expansion plans even as the company faces immediate challenges in meeting its quarterly targets. The presentation highlighted AVITA’s transformation from a burn-focused company to a broader acute wound care provider, targeting a significantly expanded addressable market.

Following the release of disappointing Q1 results showing commercial revenue of $11.1 million (a modest 5.8% year-over-year increase) and a net loss of $18.7 million, AVITA’s stock plummeted 15.33% in after-hours trading to $7.90, approaching its 52-week low of $6.90.

Quarterly Performance Highlights

AVITA Medical’s Q1 2025 performance fell short of expectations, with the company citing challenges in converting new accounts and lower device utilization for its RECELL technology. Despite maintaining a strong gross profit margin of 86.4%, the revenue miss has raised concerns about the company’s ability to achieve its ambitious growth targets.

The company reported slower growth in burn wound admissions and device utilization, potentially impacted by a data breach affecting claims data. Management also noted 8 rejections out of 178 submissions for the RECELL product, though they stated no significant pattern was observed and these rejections are not expected to materially impact guidance.

Strategic Initiatives

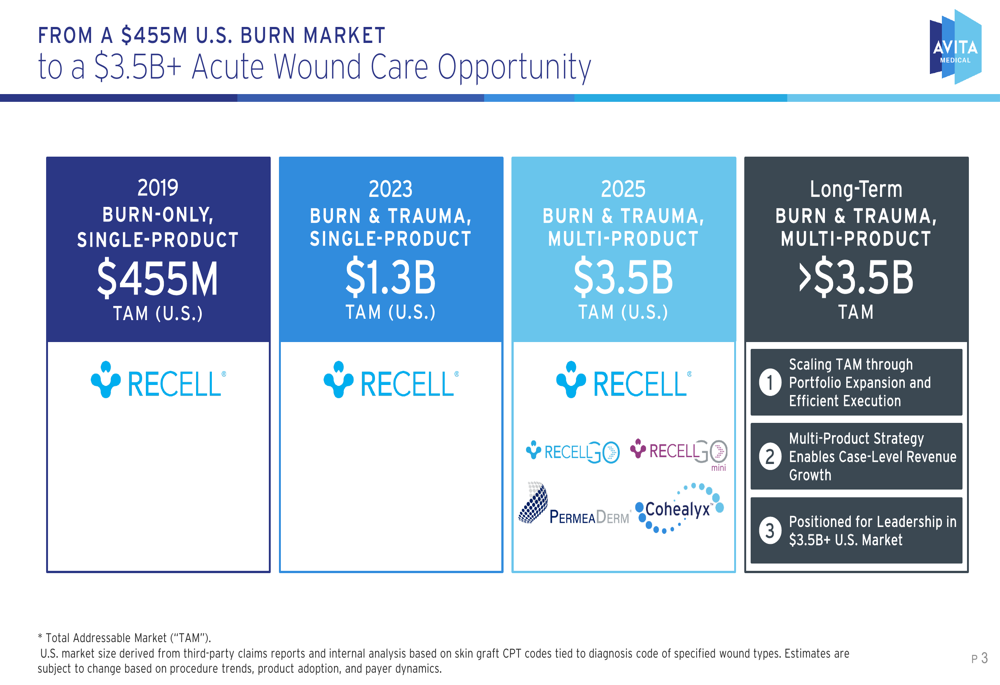

AVITA Medical’s presentation emphasized its strategic shift from a burn-focused single-product company to a multi-product acute wound care provider. As shown in the following market expansion strategy chart:

The company has progressively expanded its total addressable market (TAM) from $455 million in 2019 (burn-only, single-product focus) to $1.3 billion in 2023 (burn and trauma, single-product focus), with plans to reach a $3.5 billion TAM by 2025 through a burn and trauma multi-product approach.

This expansion is being driven by a portfolio that now includes RECELL, RECELL GO, RECELL GO mini, PERMEADERM, and Cohealyx. The company believes this multi-product strategy will enable significant case-level revenue growth and position AVITA for leadership in the U.S. acute wound care market.

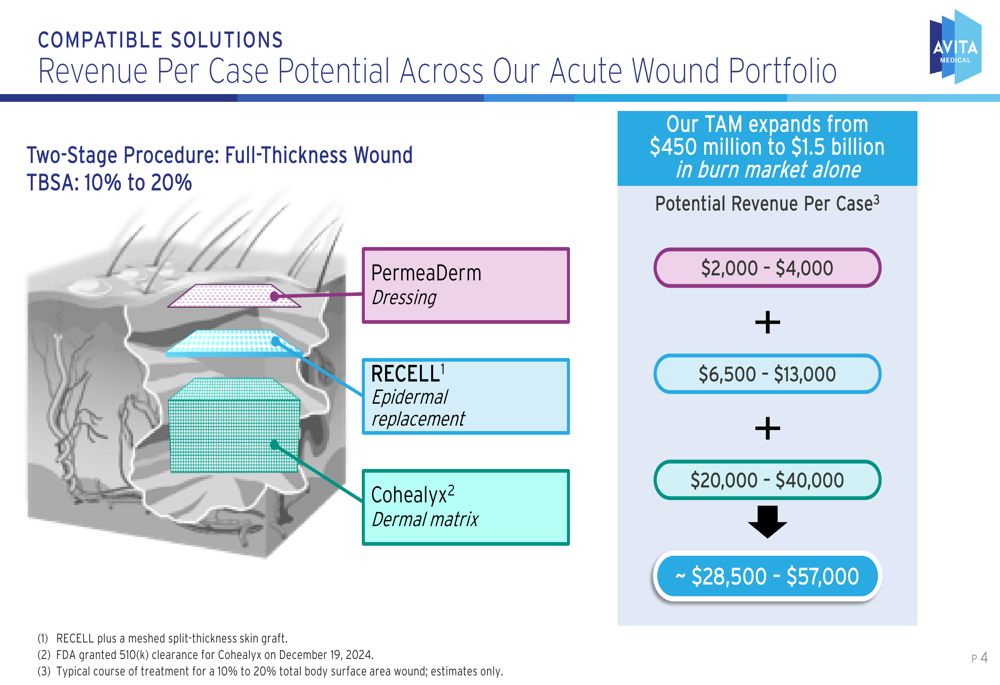

The revenue potential per case across this expanded portfolio is substantial, as illustrated in the following breakdown:

For full-thickness wounds with a Total (EPA:TTEF) Body Surface Area (TBSA) of 10% to 20%, AVITA’s two-stage procedure approach could generate approximately $28,500 to $57,000 per case, with PermeaDerm contributing $2,000-$4,000, RECELL adding $6,500-$13,000, and Cohealyx providing $20,000-$40,000. This represents a significant expansion from the company’s initial burn market focus.

Detailed Financial Analysis

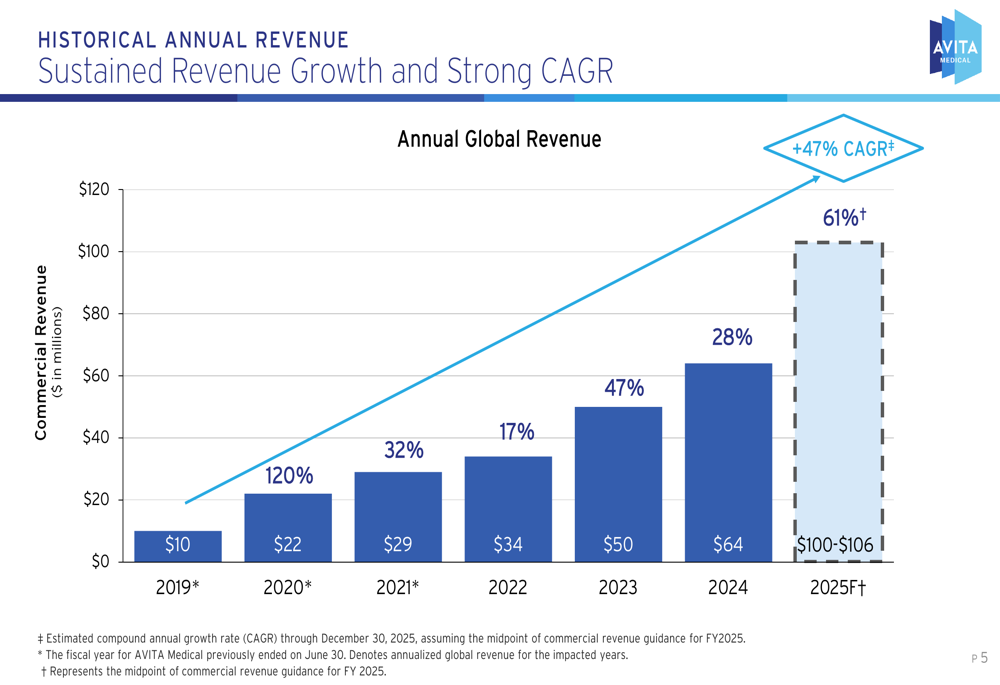

AVITA Medical’s presentation highlighted its strong historical revenue growth trajectory and ambitious projections for 2025, as shown in the following chart:

The company has demonstrated consistent revenue growth since 2019, with commercial revenue increasing from $10 million in 2019 to $64 million in 2024, representing a compound annual growth rate (CAGR) of 47%. The growth rates have fluctuated year to year, with particularly strong performance in 2020 (120% growth) and 2023 (47% growth).

For 2025, AVITA projects revenue of $100-$106 million, representing a 61% increase over 2024. However, this projection appears increasingly challenging given the Q1 2025 results. The company has maintained its full-year guidance of $78.5 million to $84.5 million, suggesting confidence in accelerating growth in the coming quarters.

Despite the ambitious long-term projections, AVITA’s Q1 2025 commercial revenue of $11.1 million represents only about 14% of the lower end of its annual guidance, indicating the company will need significant acceleration in the remaining quarters to meet its targets.

Forward-Looking Statements

AVITA Medical remains optimistic about its future prospects despite the current challenges. The company expects Q2 commercial revenues between $14.3 million and $15.3 million and reaffirmed its full-year guidance.

As shown in the company’s legal disclaimer:

AVITA acknowledges various risks and uncertainties that could affect its forward-looking statements, including regulatory approvals, market acceptance, product liability risks, and external factors.

The company is particularly focused on the upcoming launch of RECELL GO, which it expects to drive growth in the latter half of the year due to its ease of use in burn accounts and full-thickness cases. AVITA also plans international expansion into major EU countries and Australia, with RECELL GO expected to receive CE mark approval in the EU.

Management aims to reach cash flow breakeven and GAAP profitability by the third quarter of 2025, a goal that will require significant execution improvement given the current trajectory.

While AVITA’s presentation emphasizes its long-term growth potential and market expansion strategy, the immediate challenges in meeting quarterly targets and the significant stock price decline highlight the execution risks the company faces in realizing its ambitious vision of transforming lives through its expanded acute wound care portfolio.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.