Uxin shares drop 45% as predicted by InvestingPro’s Fair Value model

Introduction & Market Context

AXA Group presented its Half Year 2025 earnings results on August 1, 2025, highlighting strong organic growth across all business segments. Despite reporting a 7% increase in revenue and 8% growth in underlying earnings per share, the results fell short of analyst expectations, leading to a negative market reaction. The insurer's stock declined 5.92% following the announcement, with shares trading near €39.28, well below its 52-week high of €43.08.

The company's underlying earnings increased by 6% to €4.5 billion compared to the first half of 2024, but its EPS of €2.03 missed the forecast of €2.11, representing a 3.79% shortfall. This mixed performance comes as AXA continues to execute its "Unlock the Future" strategic plan, which focuses on organic growth and digital transformation.

Quarterly Performance Highlights

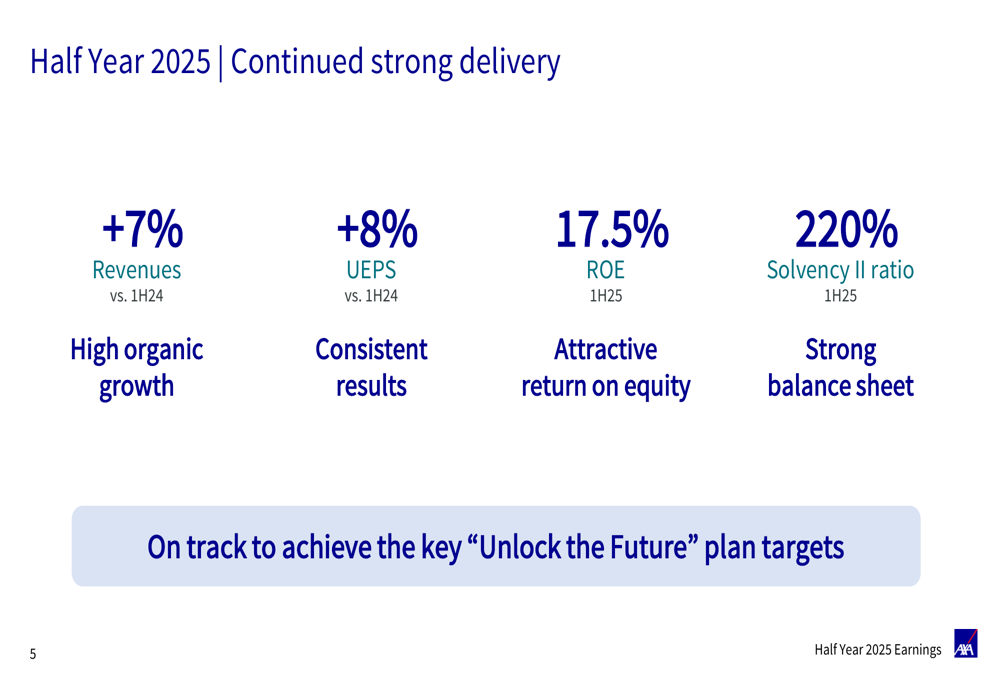

AXA reported consistent performance across its business segments, with key financial metrics showing positive momentum in the first half of 2025.

As shown in the following chart of key performance indicators:

The company achieved 7% revenue growth compared to the first half of 2024, with underlying earnings per share increasing by 8%. Return on equity reached an attractive 17.5%, while the Solvency II ratio strengthened to 220%, indicating a robust balance sheet position.

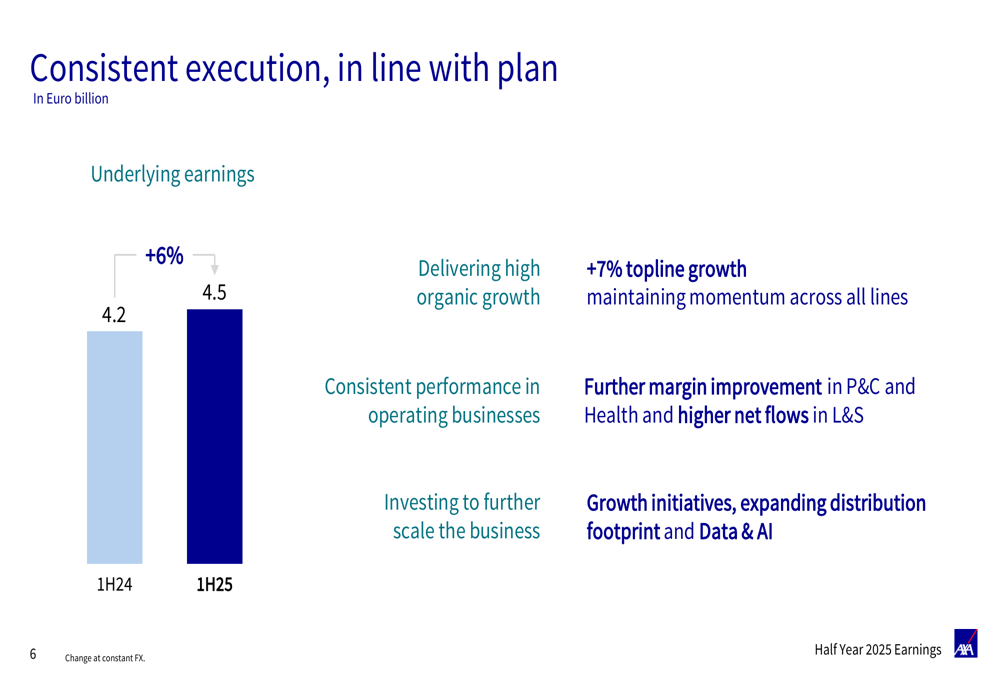

Breaking down the underlying earnings growth:

The company's underlying earnings rose from €4.2 billion in 1H24 to €4.5 billion in 1H25, representing a 6% increase at constant exchange rates. This growth was driven by high organic expansion across all lines of business, margin improvements in Property & Casualty (P&C) and Health segments, and higher net flows in Life & Savings.

Strategic Initiatives

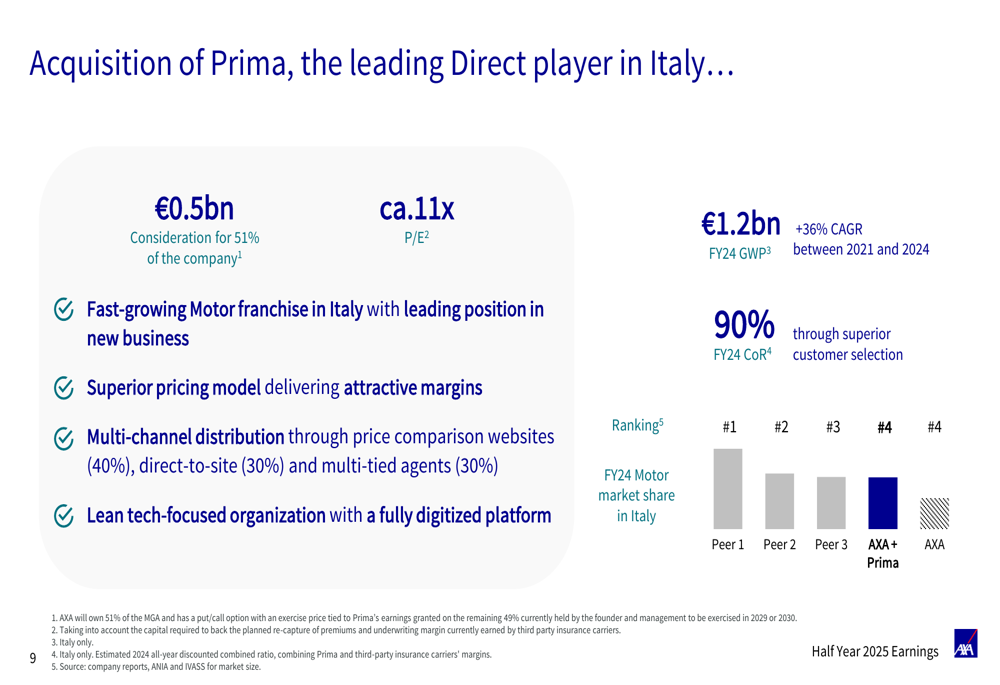

A significant highlight of AXA's presentation was the announcement of its acquisition of Prima, a leading direct insurance player in Italy. This strategic move aligns with the company's focus on expanding its direct distribution channels.

The following slide details the acquisition parameters:

AXA is acquiring a 51% stake in Prima for €0.5 billion, representing approximately 11 times earnings. Prima is characterized as a fast-growing motor franchise in Italy with a leading position in new business. The company boasts a superior pricing model that delivers attractive margins, with a 90% combined ratio for FY24. Prima utilizes a multi-channel distribution approach through price comparison websites (40%), direct-to-site (30%), and multi-tied agents (30%).

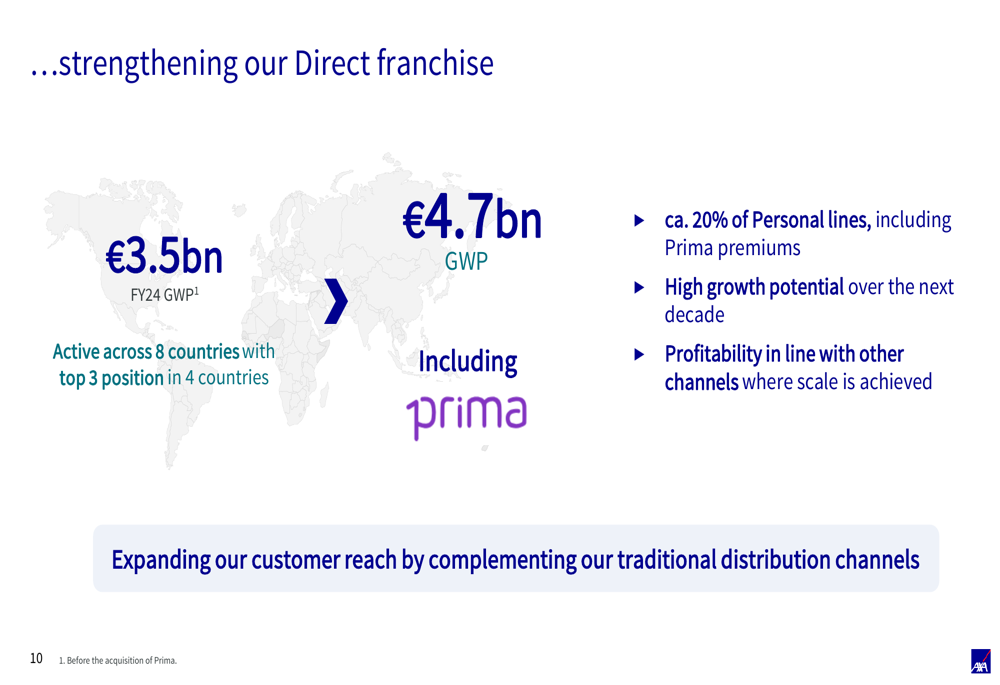

This acquisition significantly strengthens AXA's direct insurance franchise, as illustrated in the following slide:

With the Prima acquisition, AXA's direct franchise now represents €4.7 billion in gross written premiums across eight countries, with top three positions in four markets. The company views direct insurance as having high growth potential over the next decade, with profitability in line with other channels where scale is achieved.

Detailed Financial Analysis

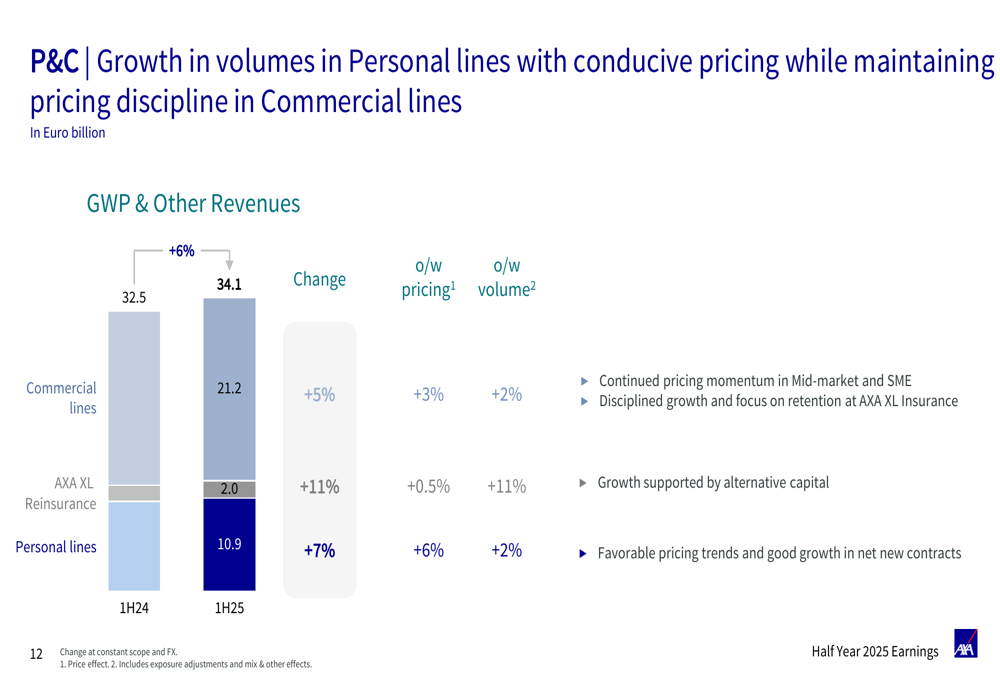

AXA's Property & Casualty segment showed strong volume growth across all business lines:

Total P&C gross written premiums increased by 6%, from €32.5 billion in 1H24 to €34.1 billion in 1H25. Commercial lines grew by 5%, AXA XL Reinsurance by 11%, and Personal lines by 7%. This growth was driven by both pricing actions and volume increases.

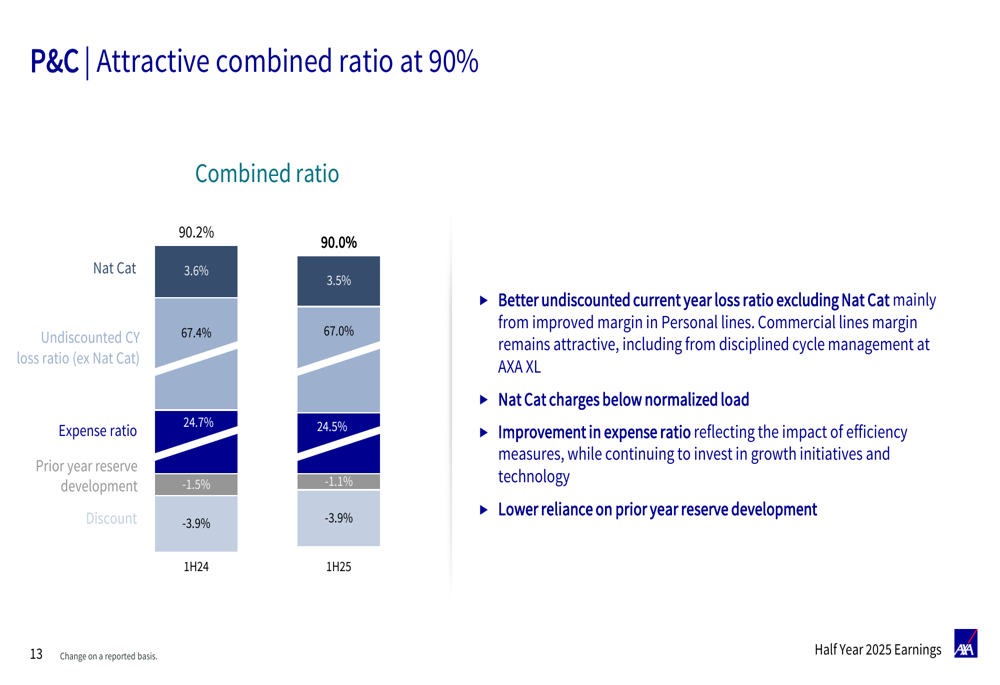

The P&C combined ratio remained attractive at 90%:

The combined ratio breakdown shows improvements in several key components, including the undiscounted current year loss ratio (excluding natural catastrophes), which improved from 67.4% to 67.0%, and the expense ratio, which decreased from 24.7% to 24.5%. Natural catastrophe charges were slightly below the normalized load at 3.5%.

However, the earnings article notes challenges in the UK motor market, which is experiencing softening that could pressure margins – a concern not prominently addressed in the presentation.

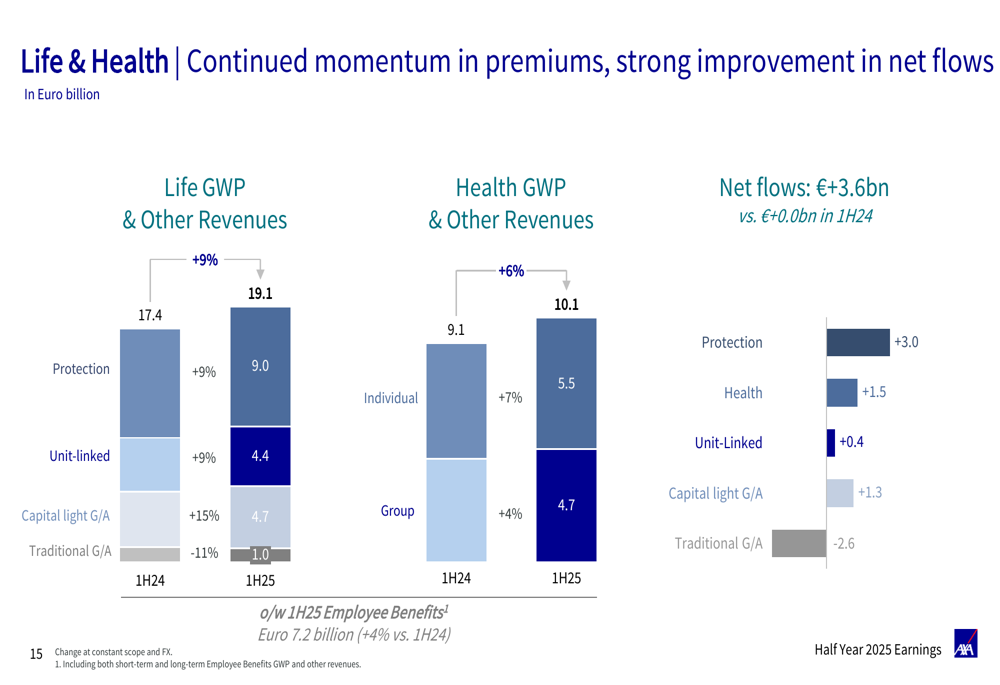

The Life & Health segment also demonstrated continued momentum:

Life gross written premiums increased by 9%, while Health premiums grew by 6%. Net flows improved significantly to €3.6 billion, compared to €0.0 billion in the first half of 2024. This improvement was driven by positive flows in Protection, Health, Unit-Linked, and Capital Light General Account products, partially offset by outflows in Traditional General Account products.

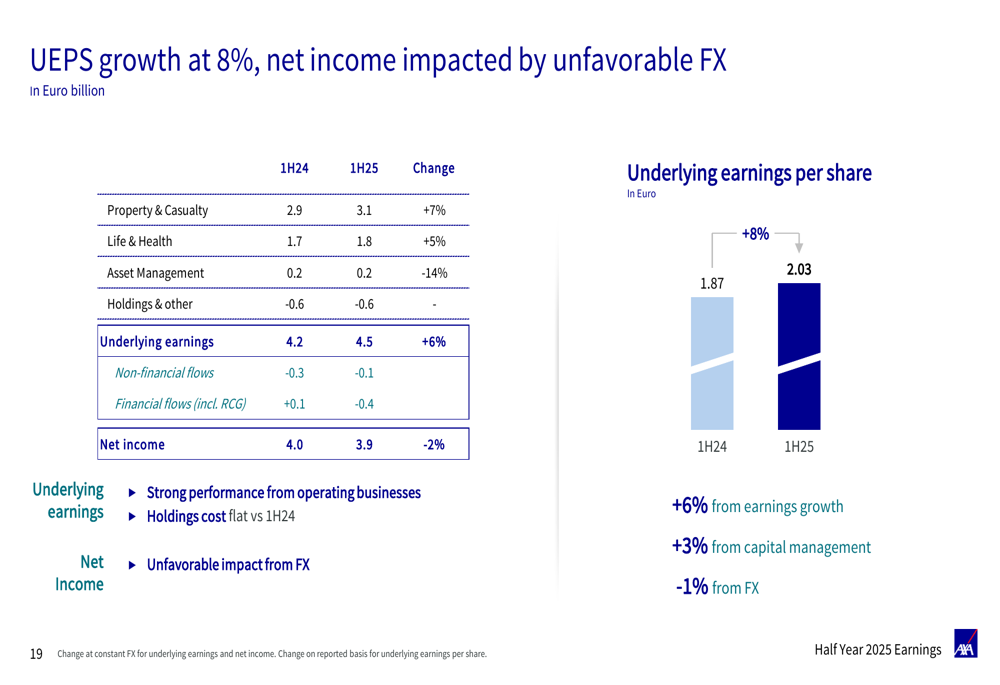

Overall, AXA's underlying earnings per share grew by 8%:

The UEPS increase from €1.87 to €2.03 was driven by earnings growth (+6%), positive impact from capital management (+3%), partially offset by negative foreign exchange impacts (-1%). Despite this growth, the €2.03 figure fell short of analyst expectations of €2.11.

Financial Position

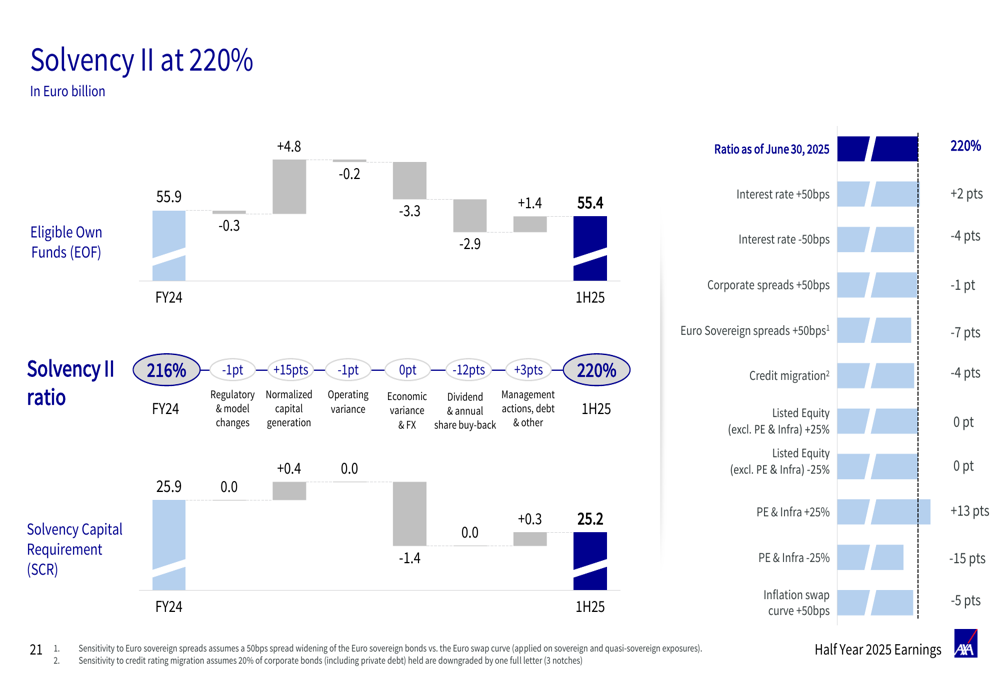

AXA's balance sheet remains strong, with a Solvency II ratio of 220%:

The Solvency II ratio improved from 216% to 220%, with Eligible Own Funds of €55.4 billion and a Solvency Capital Requirement of €25.2 billion. This strong capital position provides the company with flexibility for strategic investments and shareholder returns.

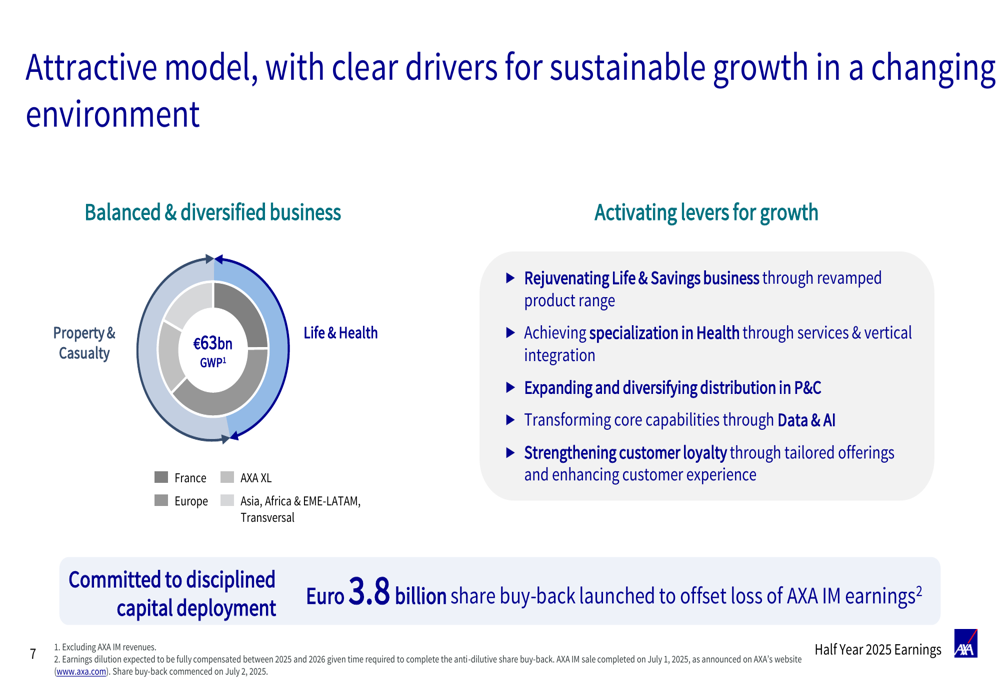

However, the presentation also reveals that shareholders' equity decreased from €49.9 billion to €45.5 billion, while debt gearing increased from 20.6% to 23.4%. The company has launched a €3.8 billion share buyback program to offset the loss of AXA Investment Managers earnings.

Forward-Looking Statements

AXA remains confident in achieving the targets outlined in its "Unlock the Future" strategic plan. The company is focusing on several growth levers:

These include rejuvenating the Life & Savings business through a revamped product range, achieving specialization in Health through services and vertical integration, expanding and diversifying distribution in P&C, transforming core capabilities through Data & AI, and strengthening customer loyalty through tailored offerings and enhanced customer experience.

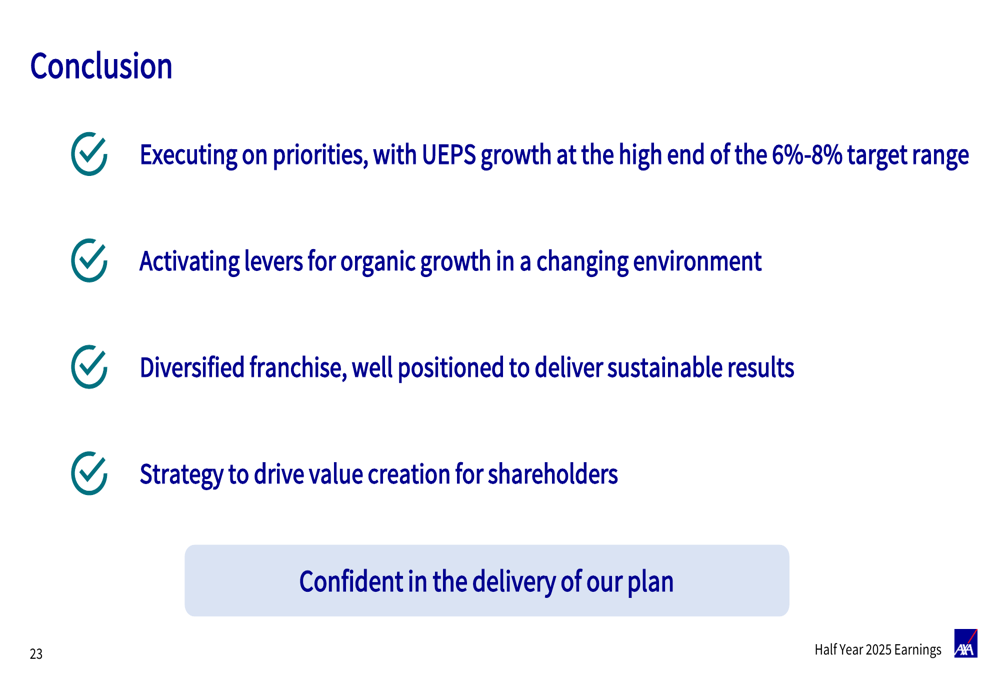

In its conclusion, AXA emphasized its execution on priorities:

The company highlighted that it is executing on its priorities, with UEPS growth at the high end of its 6-8% target range. AXA believes its diversified franchise is well-positioned to deliver sustainable results, with a strategy focused on driving value creation for shareholders.

Deputy CEO Frederic de Courtois reinforced the company's strategic focus during the earnings call, stating: "We are insurance, only insurance and again only insurance," while emphasizing that "Our priority goal with our plan is organic growth." He also expressed confidence in the transformative potential of data and AI, noting, "We are fully convinced that [data and AI] will have a very strong impact on our businesses."

Despite the positive messaging, investors appear concerned about the EPS miss and potential challenges ahead, including integration risks with the Prima acquisition, softening in the UK motor market, and potential volatility in financial markets that could affect asset valuations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.