Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Axactor SE (OB:ACR) presented its second quarter 2025 results on August 14, continuing the positive momentum seen in Q1. The debt collection company’s stock closed at €8.54 prior to the presentation, representing a significant rise from the €5.50 reported after Q1 results, indicating strong investor confidence in the company’s strategic direction.

The presentation highlighted Axactor’s continued focus on operational efficiency, 3PC (Third-Party Collection) growth, and financial stability through successful refinancing activities. These efforts come amid a challenging but stabilizing European debt collection market, with the company showing particular strength in its Norwegian and Spanish operations.

Quarterly Performance Highlights

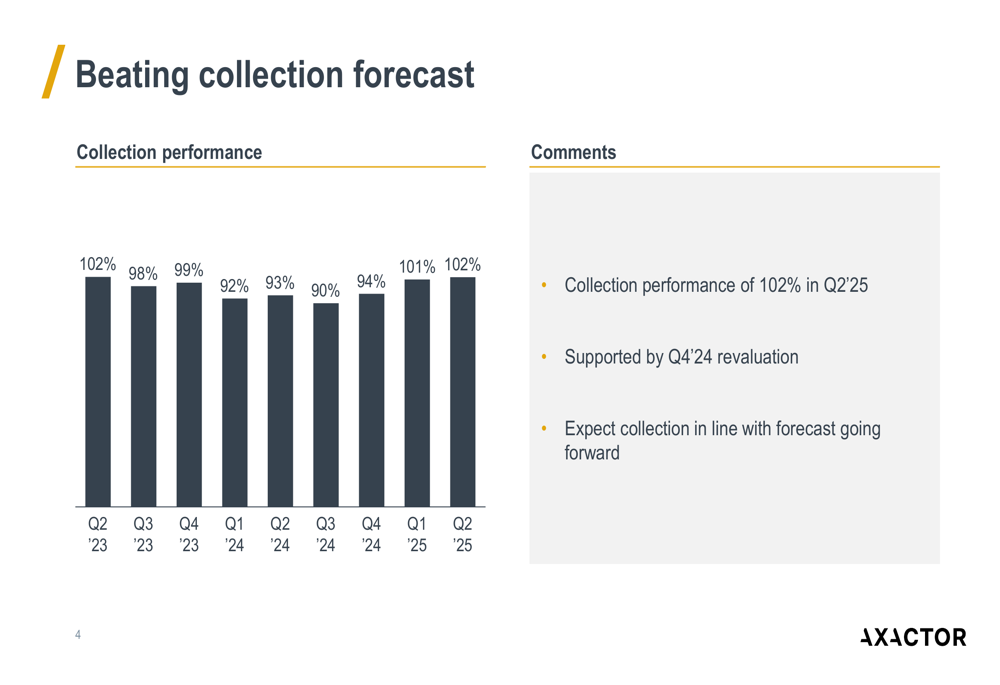

Axactor reported a collection performance of 102% in Q2 2025, exceeding forecasts for the second consecutive quarter after achieving 101% in Q1. This performance was supported by the Q4 2024 revaluation and demonstrates the company’s operational efficiency.

As shown in the following chart of quarterly collection performance:

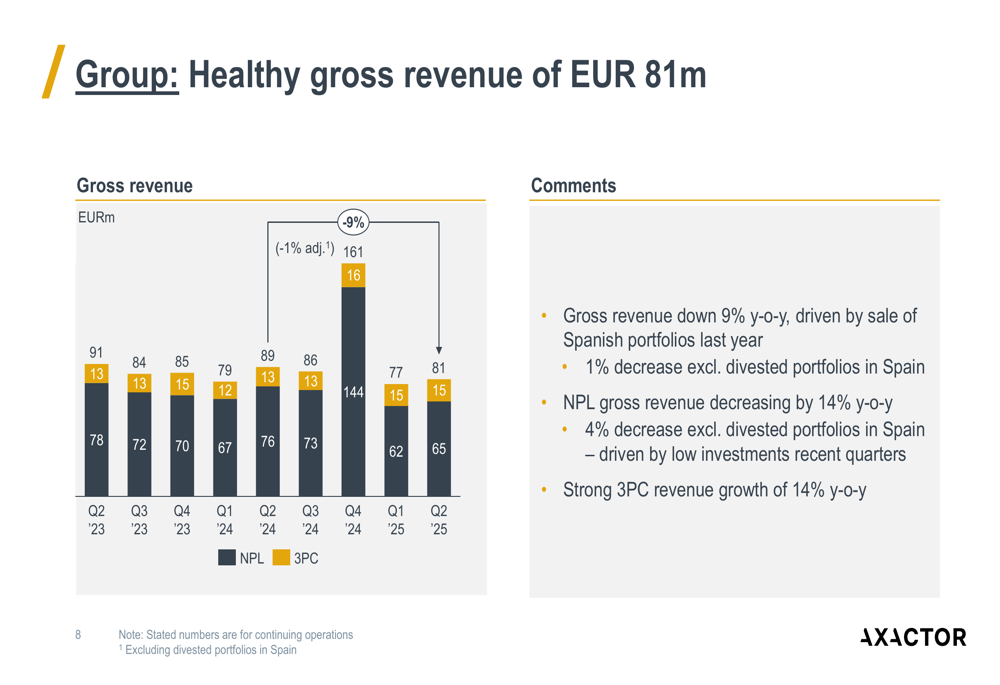

The company maintained healthy gross revenue of €81 million, which represents a modest 1% year-over-year decrease excluding divested portfolios in Spain. The 3PC segment continued its strong growth trajectory with a 14% year-over-year increase in revenue, offsetting the 14% decline in NPL (Non-Performing Loans) gross revenue.

The revenue breakdown by segment is illustrated in this chart:

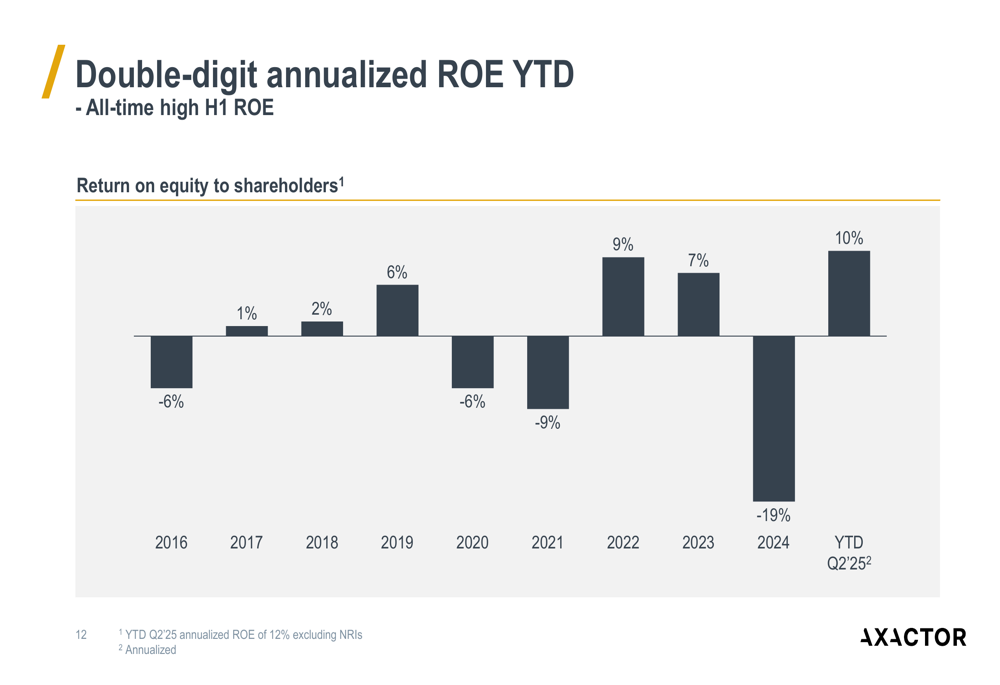

Axactor achieved an annualized return on equity to shareholders of 8% (12% excluding non-recurring items), with year-to-date return on equity reaching 10% (12% excluding NRIs). This represents a significant improvement from the -19% ROE recorded in 2024 and marks an all-time high for first-half performance.

The historical ROE trend is depicted in the following chart:

Strategic Initiatives

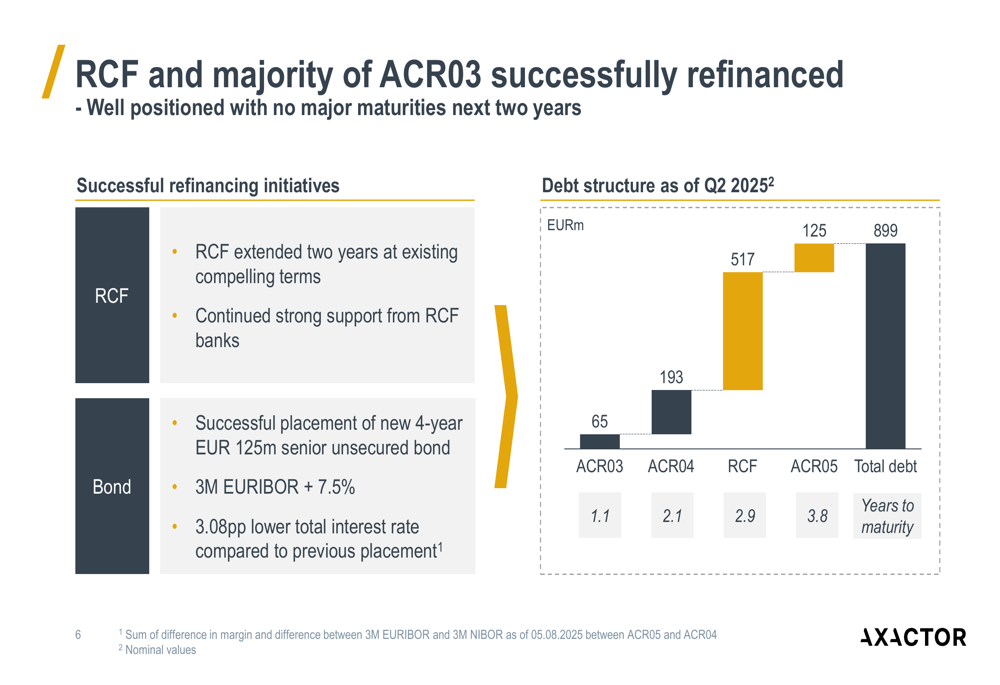

A key achievement during the quarter was the successful refinancing of Axactor’s Revolving Credit Facility (RCF) and the majority of its ACR03 bond. The company placed the new ACR05 bond at more than three percentage points lower total interest rate compared to ACR04, significantly improving its cost of capital.

The current debt structure and maturity profile is illustrated below:

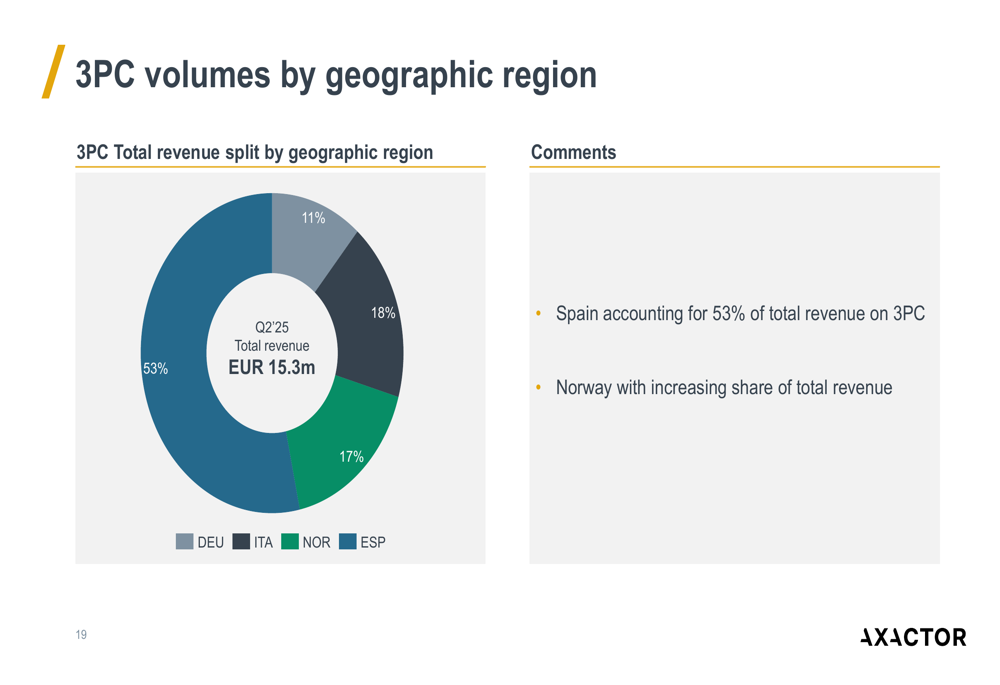

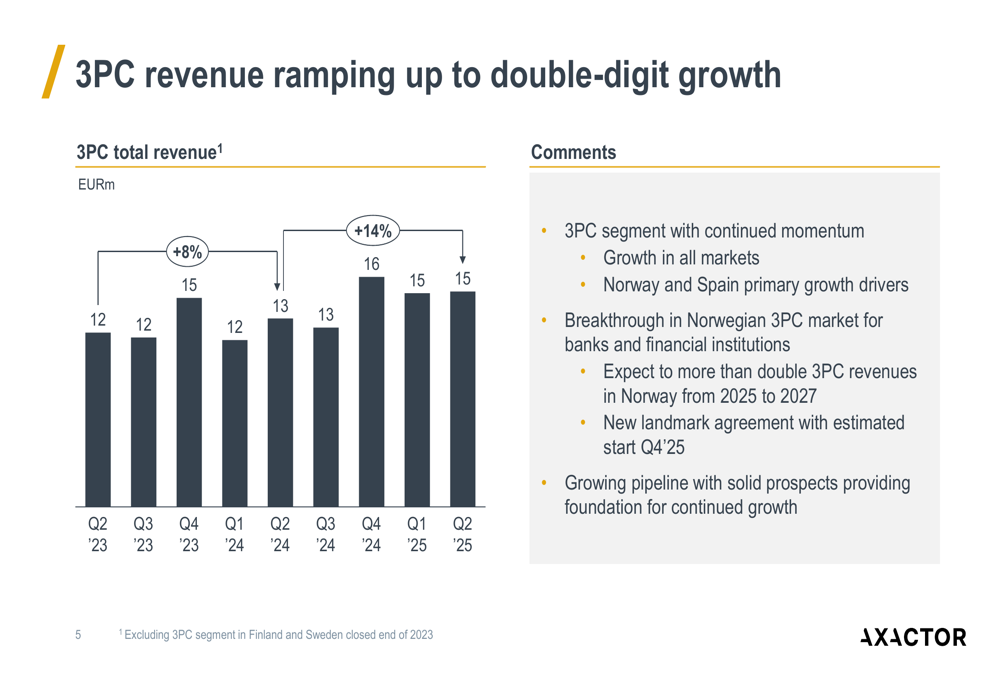

Axactor’s 3PC business continues to gain momentum, with growth in all markets and Norway and Spain serving as primary drivers. The company reported a breakthrough in the Norwegian 3PC market and expects to more than double 3PC revenues in Norway from 2025 to 2027.

The geographic distribution of 3PC revenue shows Spain’s dominance and Norway’s growing importance:

The 3PC segment’s consistent revenue growth is evident in this quarterly trend:

Detailed Financial Analysis

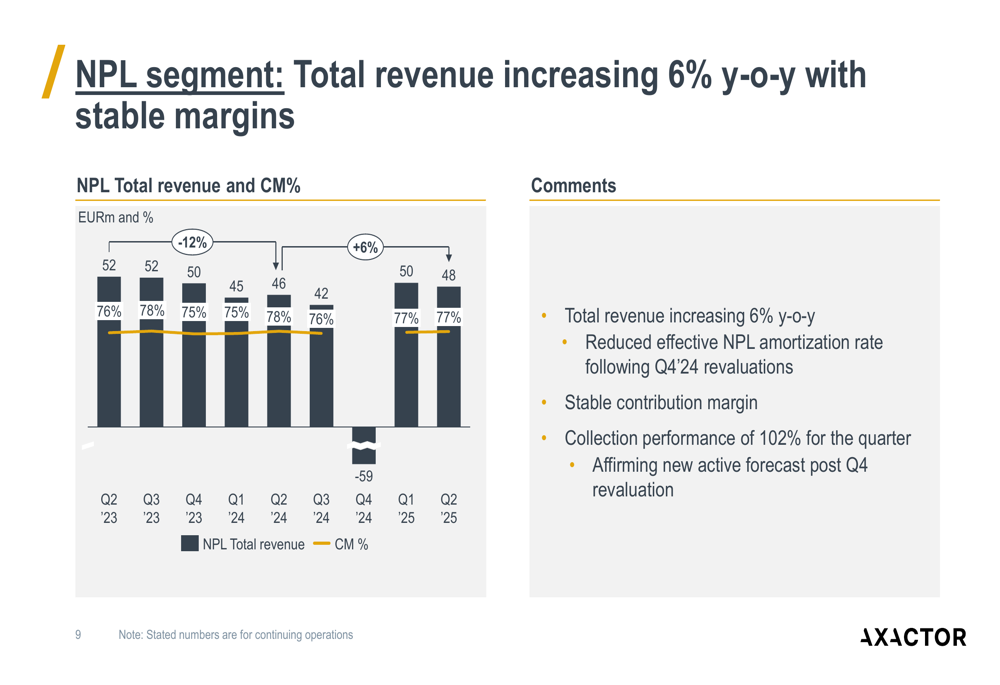

The NPL segment showed resilience with a 6% year-over-year increase in total revenue and stable contribution margins around 77%. This performance was supported by reduced amortization rates following portfolio revaluations and the strong collection performance.

NPL segment performance metrics are shown here:

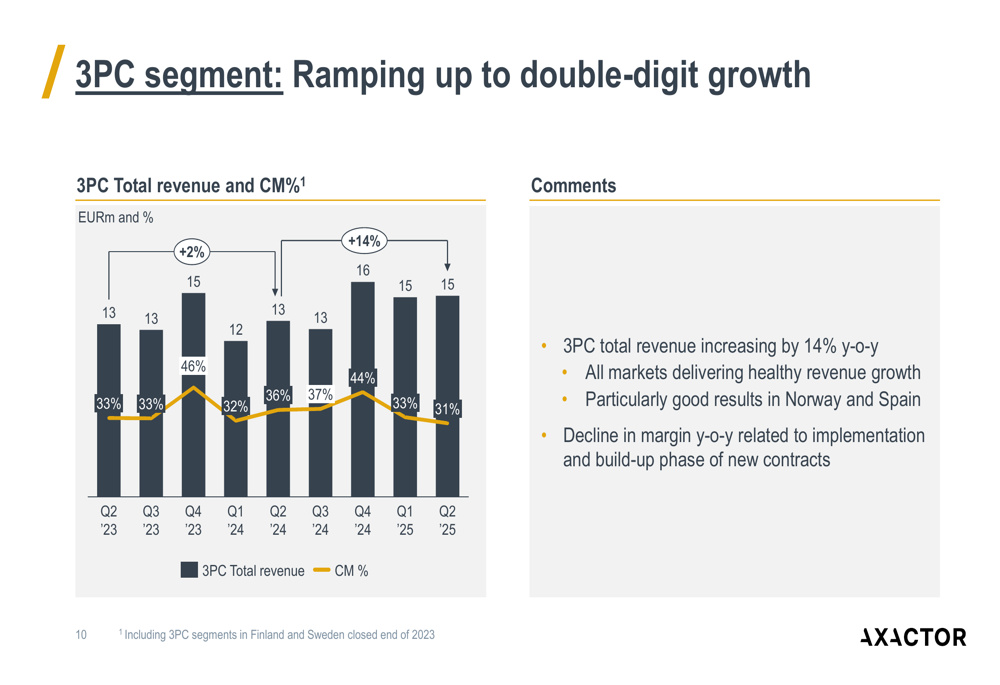

Meanwhile, the 3PC segment continued its double-digit growth trajectory, though margins declined year-over-year due to implementation costs. Total 3PC revenue reached €15 million in Q2 2025, up from €13 million in Q2 2024.

3PC segment performance is illustrated in this chart:

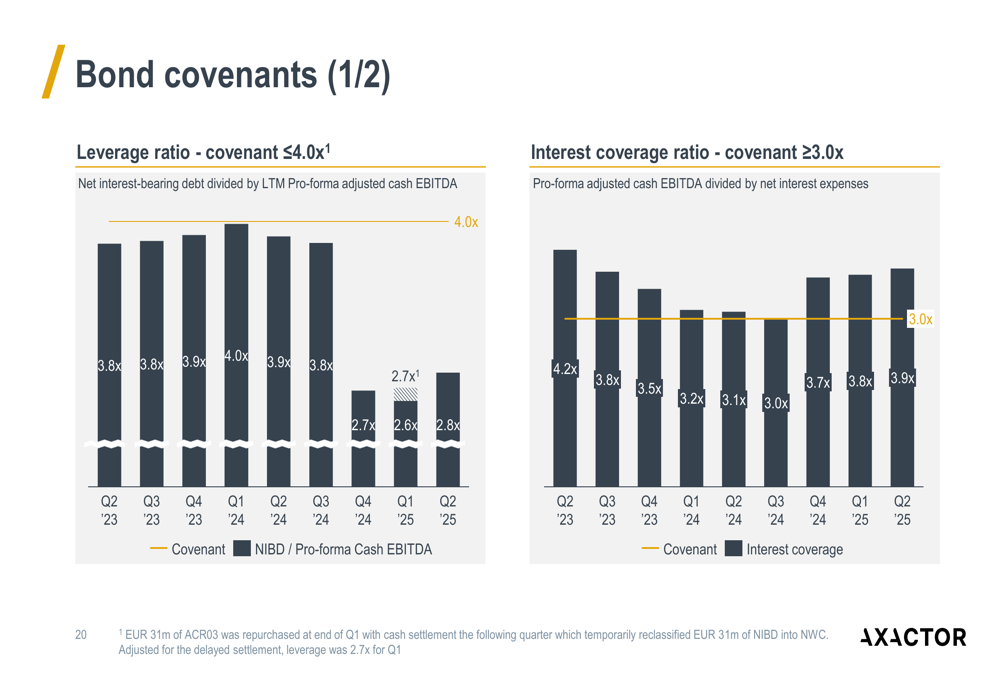

Axactor’s financial health has improved significantly, with the leverage ratio declining to 2.8x in Q2 2025 from near-covenant levels of 4.0x in early 2024. Similarly, the interest coverage ratio strengthened to 3.9x, well above the covenant requirement of 3.0x.

The company’s performance against bond covenants is shown below:

Forward-Looking Statements

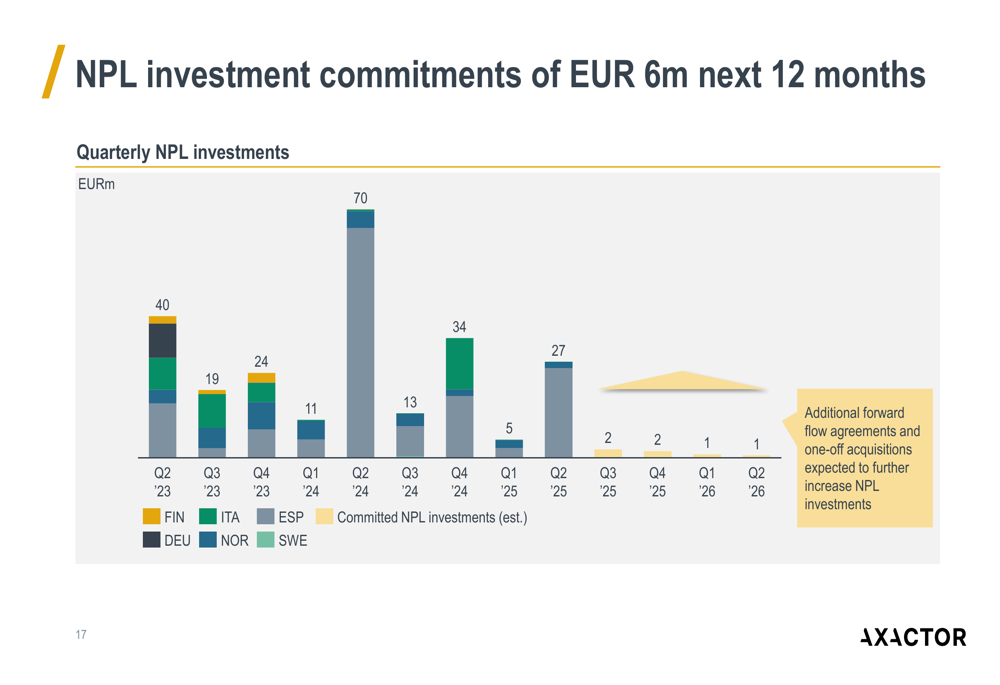

Looking ahead, Axactor expects collection performance to remain around 100%, maintaining the strong trajectory established in recent quarters. The company is shifting its strategic focus to accretive NPL investments, though committed investments for the remainder of 2025 appear modest at €2 million for Q3 and €1 million for Q4.

The NPL investment outlook is depicted in this chart:

Axactor anticipates cost reductions following its IT infrastructure migration, with quarterly OPEX expected to decrease by approximately €800,000. This aligns with the cost control focus mentioned in the Q1 earnings report.

The company appears well-positioned with no major debt maturities in the next two years and has secured several large new 3PC agreements that should support continued growth in that segment. The growing pipeline in the 3PC business, particularly in Norway, suggests this will remain a key growth driver for Axactor in the coming years.

While the presentation highlighted strong operational performance, investors should note that the company’s ERC (Estimated Remaining Collections) has declined slightly to €2,320 million in Q2 2025 from €2,563 million in Q2 2023, reflecting the impact of portfolio sales and modest recent NPL investments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.