Futures slip, bank earnings ahead, Powell to speak - what’s moving markets

Introduction & Market Context

Axalta Coating Systems Ltd (NYSE:AXTA) presented its second quarter 2025 financial results on July 30, showing operational resilience amid challenging market conditions. The coatings manufacturer achieved record Adjusted EBITDA and Adjusted Diluted EPS despite experiencing a 3% year-over-year decline in net sales, as the company continues to navigate a complex global economic environment.

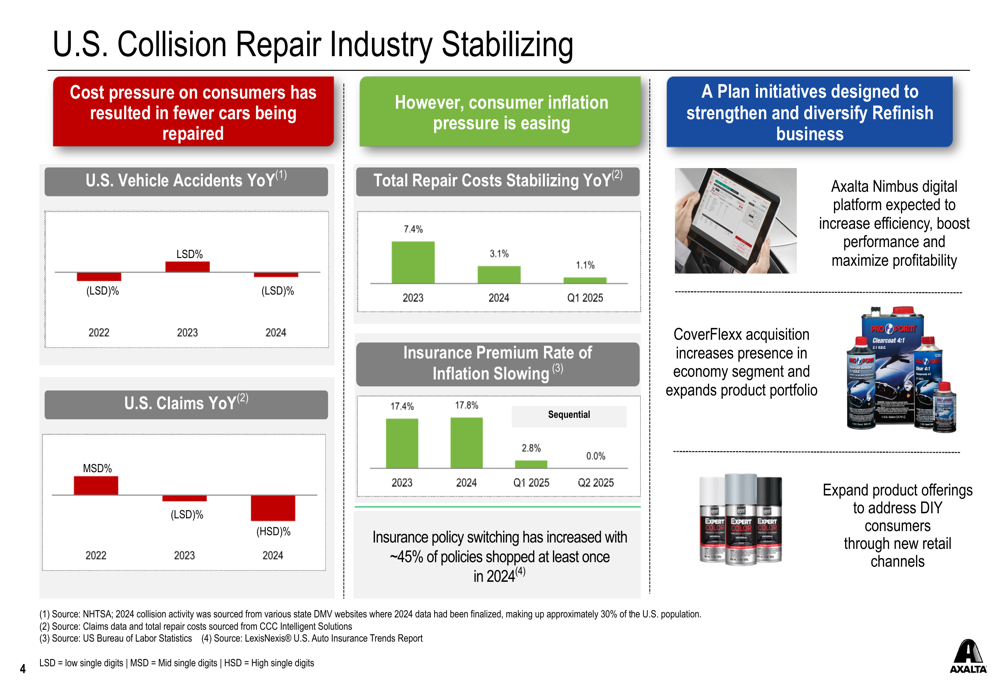

The presentation highlighted stabilization in the U.S. collision repair industry, with consumer inflation pressure easing and insurance premium inflation slowing significantly. However, Axalta noted that cost pressures on consumers have resulted in fewer cars being repaired, creating headwinds for its refinish business.

As shown in the following chart detailing the collision repair industry trends:

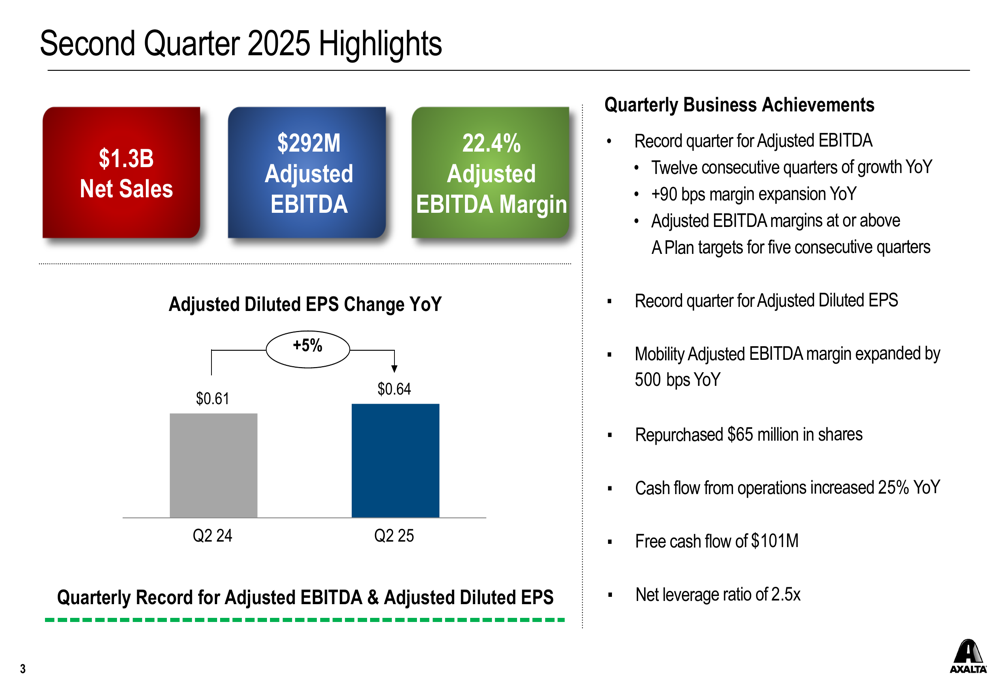

Quarterly Performance Highlights

Axalta reported Q2 2025 net sales of $1.3 billion, down 3% compared to the same period last year. Despite this decline, the company achieved record quarterly Adjusted EBITDA of $292 million, slightly up from $291 million in Q2 2024. The Adjusted EBITDA margin expanded by 90 basis points to 22.4%, marking the twelfth consecutive quarter of year-over-year growth.

Adjusted Diluted EPS increased 5% to $0.64 compared to $0.61 in the prior year period. The company also reported strong cash generation with operating cash flow up 25% to $142 million and free cash flow of $101 million, a 6% increase year-over-year.

The following slide summarizes Axalta’s key financial results for the quarter:

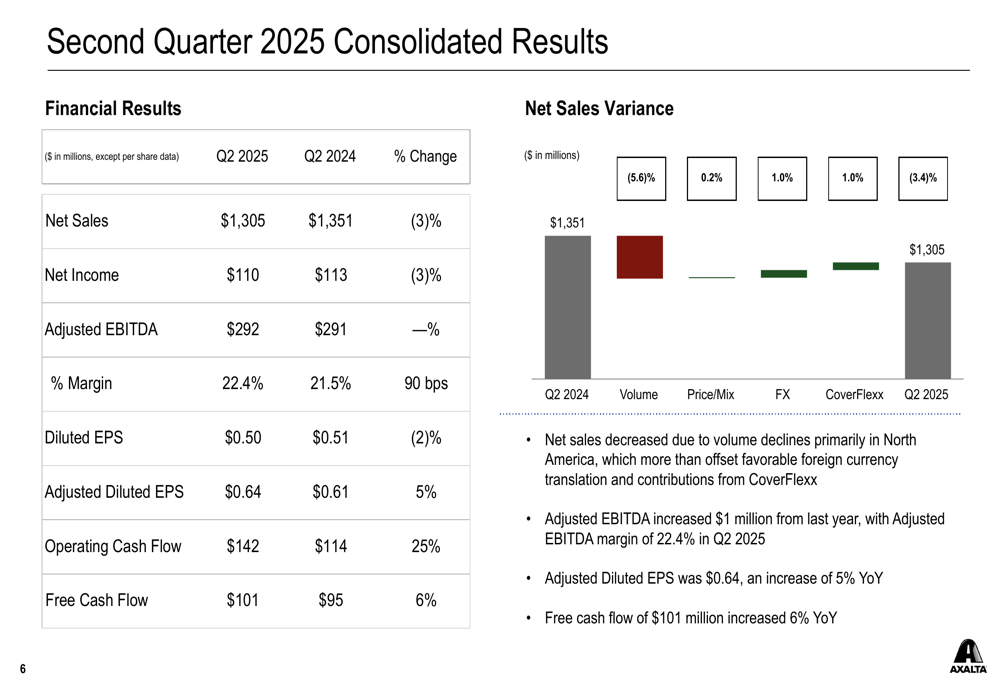

A closer look at the consolidated financial results reveals that volume declines, primarily in North America, were the main driver of the sales decrease, partially offset by favorable foreign currency translation and contributions from the CoverFlexx acquisition:

Segment Analysis

Axalta’s performance showed a stark contrast between its two main business segments. The Performance Coatings segment, which includes Refinish and Industrial businesses, reported a 6% decline in net sales to $836 million. Adjusted EBITDA for this segment fell 10% to $200 million, with margins contracting by 120 basis points to 23.8%.

The decline in Performance Coatings was primarily driven by lower repair activity in North America for the Refinish business and volume weakness in the Industrial business. These headwinds were partially offset by favorable foreign currency translation and the contribution from the CoverFlexx acquisition.

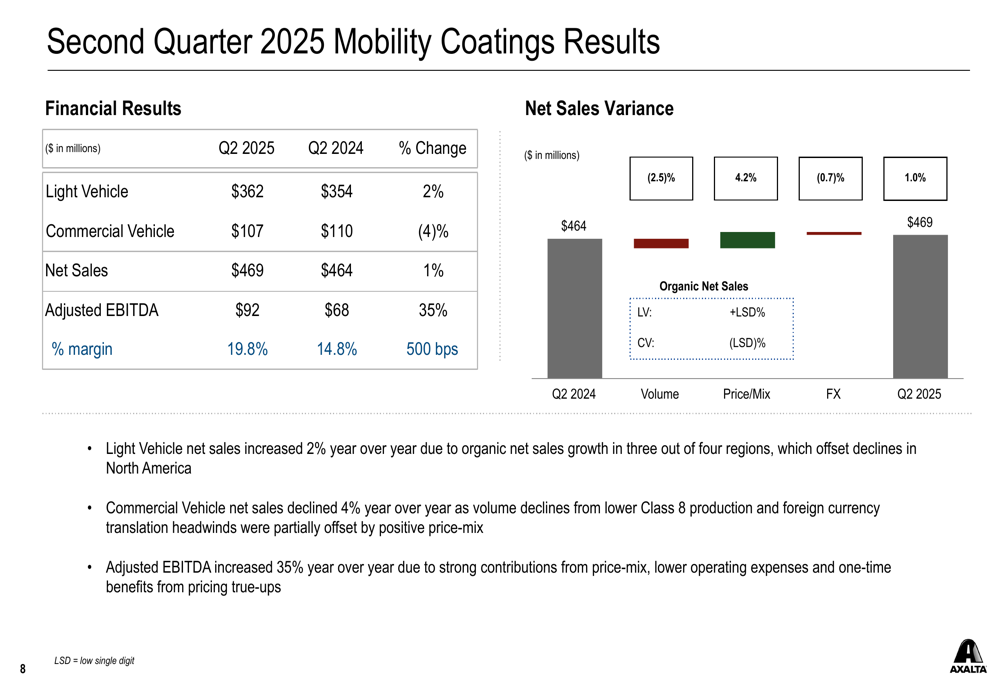

In contrast, the Mobility Coatings segment, which includes Light Vehicle and Commercial Vehicle businesses, showed strong performance with a 1% increase in net sales to $469 million. More impressively, Adjusted EBITDA for this segment surged 35% to $92 million, with margins expanding by 500 basis points to 19.8%. This improvement was driven by strong price-mix contributions, lower operating expenses, and one-time benefits from pricing true-ups.

The following chart illustrates the Mobility Coatings segment’s impressive results:

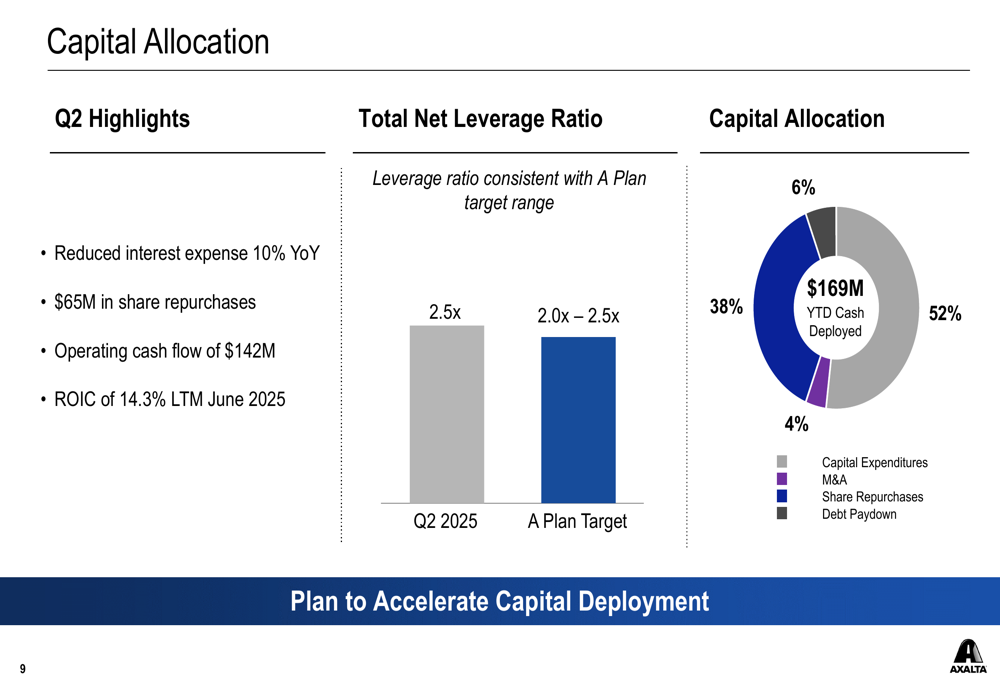

Capital Allocation and Strategic Initiatives

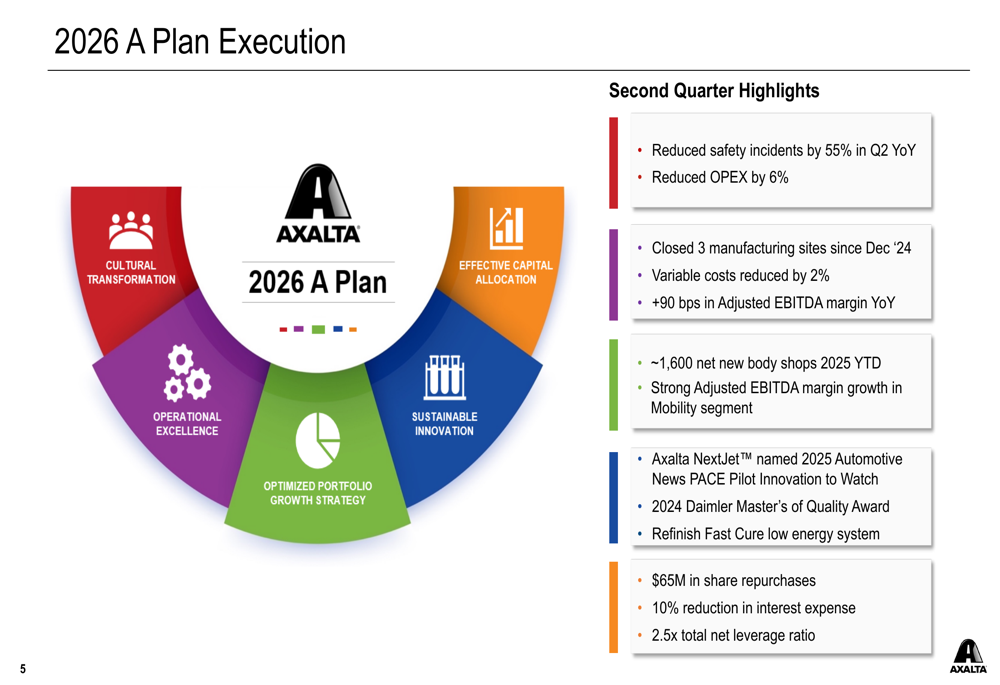

Axalta continued to execute its "A Plan" strategy, focusing on cultural transformation, effective capital allocation, sustainable innovation, optimized portfolio growth, and operational excellence. The company reduced safety incidents by 55% year-over-year, decreased operating expenses by 6%, and closed three manufacturing sites since December 2024.

The company’s capital allocation strategy in Q2 included $65 million in share repurchases and a 10% reduction in interest expense year-over-year. Axalta maintained a total net leverage ratio of 2.5x, consistent with its A Plan target range of 2.0x-2.5x.

As shown in the following capital allocation breakdown:

Axalta’s strategic initiatives are centered around its "A Plan" execution, which has delivered tangible results across multiple areas:

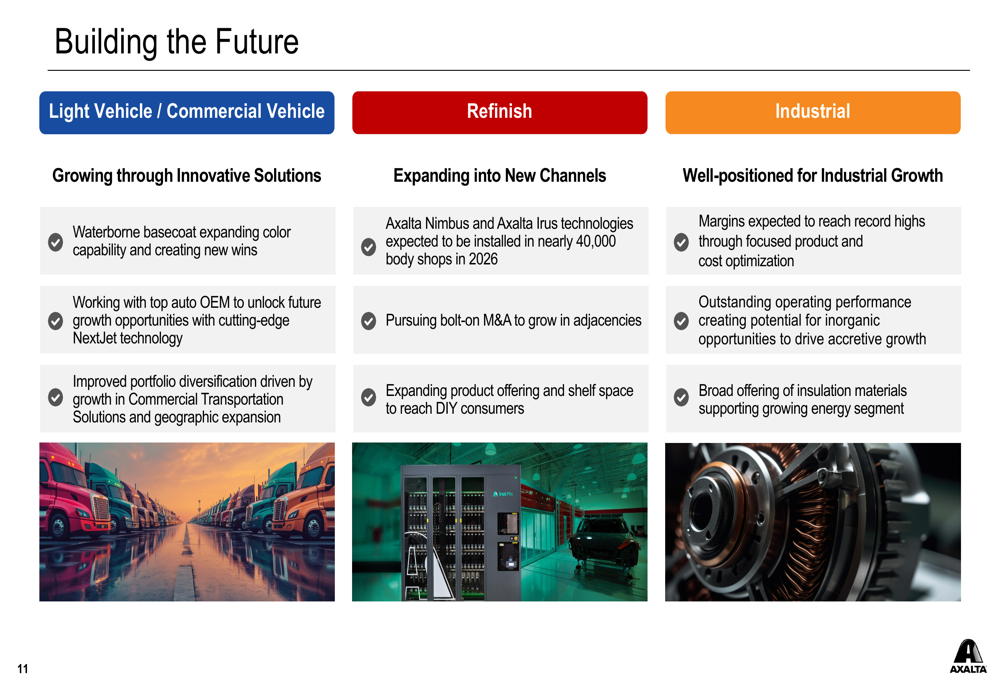

Looking ahead, the company outlined its growth strategy across its three main segments, focusing on waterborne basecoat expansion and NextJet technology for its automotive business, digital platforms for Refinish, and margin improvement for Industrial:

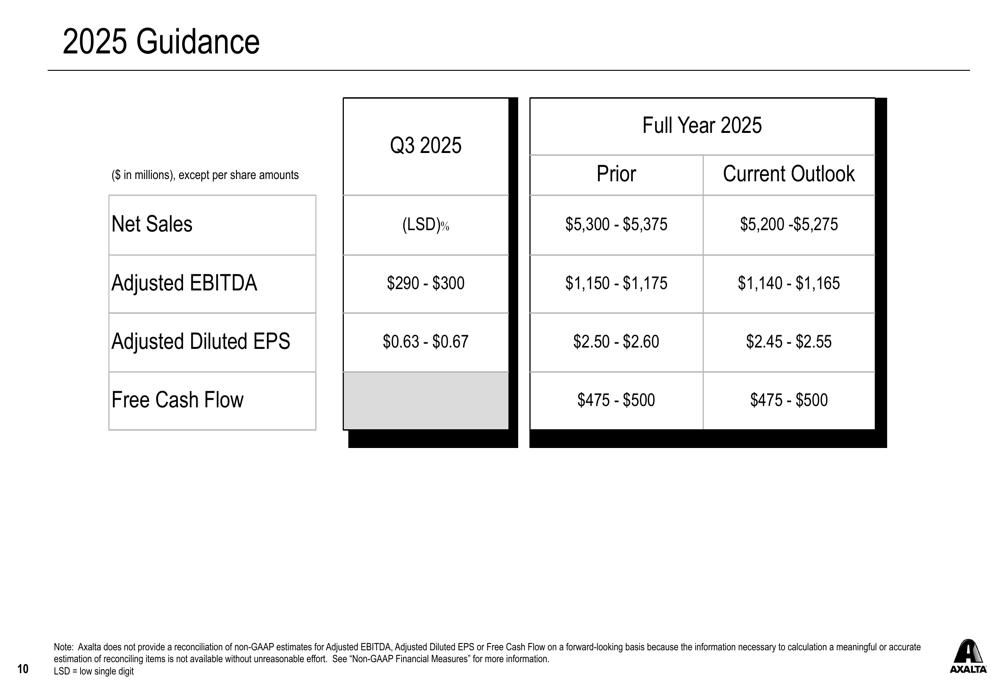

Guidance and Outlook

Despite the operational achievements in Q2, Axalta revised its full-year 2025 guidance downward. The company now expects net sales of $5,200-$5,275 million, down from the previous guidance of $5,300-$5,375 million. Adjusted EBITDA is projected to be $1,140-$1,165 million, slightly lower than the prior guidance of $1,150-$1,175 million. Adjusted Diluted EPS is now expected to be $2.45-$2.55, compared to the previous range of $2.50-$2.60.

For Q3 2025, Axalta projects a low-single-digit percentage decline in net sales, with Adjusted EBITDA between $290-$300 million and Adjusted Diluted EPS between $0.63-$0.67.

The company’s updated guidance reflects ongoing challenges in the market environment, including geopolitical volatility, heightened trade tensions, and low global industrial activity. However, Axalta maintained its free cash flow guidance of $475-$500 million for the full year.

The following slide details the company’s updated guidance:

Axalta’s modeling assumptions for the full year include continued net body shop wins and resilient pricing in Refinish, business wins in Latin America and Asia Pacific for Light Vehicle and Commercial Vehicle segments, and $30-$40 million of incremental cost savings from its 2024 Transformation Initiative. The company also expects $25 million lower interest expense year-over-year.

Despite the reduced guidance, Axalta’s focus on operational efficiency and strategic initiatives positions the company to navigate the challenging market environment while continuing to deliver margin improvements and strong cash flow generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.