Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Introduction & Market Context

Axon Enterprise Inc (NASDAQ:AXON) presented its Q2 2025 investor slides on August 4, 2025, showcasing strong financial performance and an expanding product ecosystem. The company’s stock closed at $742.47 and rose 0.62% in after-hours trading following the presentation, approaching its 52-week high of $830.21.

The public safety technology provider continues to build on its momentum from Q1 2025, when it reported $604 million in revenue with a 31% year-over-year increase. The latest presentation reveals further acceleration in Q2, positioning Axon as a dominant player in the law enforcement technology sector with growing influence in adjacent markets.

Executive Summary

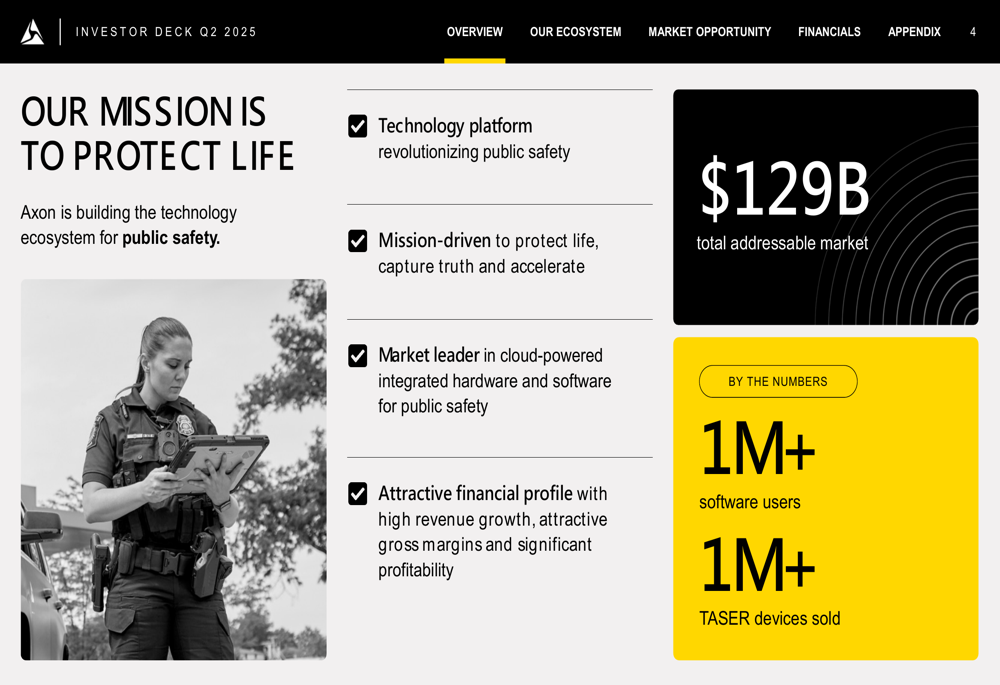

Axon’s mission-driven approach centers on protecting life through its expanding technology ecosystem for public safety. The company has set an ambitious "moonshot" goal to cut gun-related deaths between police and the public by 50% by 2033.

As shown in the following slide highlighting Axon’s mission and key metrics, the company has built a substantial business around this purpose:

The presentation reveals impressive financial metrics, including $2.1 billion in 2024 annual revenue, $1.2 billion in annual recurring revenue, and a 25% adjusted EBITDA margin. With future contracted bookings of $10.7 billion and 124% net revenue retention, Axon demonstrates both current strength and future growth potential.

Financial Performance Highlights

Axon reported Q2 2025 revenue of $669 million, representing continued growth from the $604 million reported in Q1. The Q2 revenue breaks down to $292 million from Connected Devices and $376 million from Software (ETR:SOWGn) & Services, highlighting the company’s successful transition toward higher-margin software offerings.

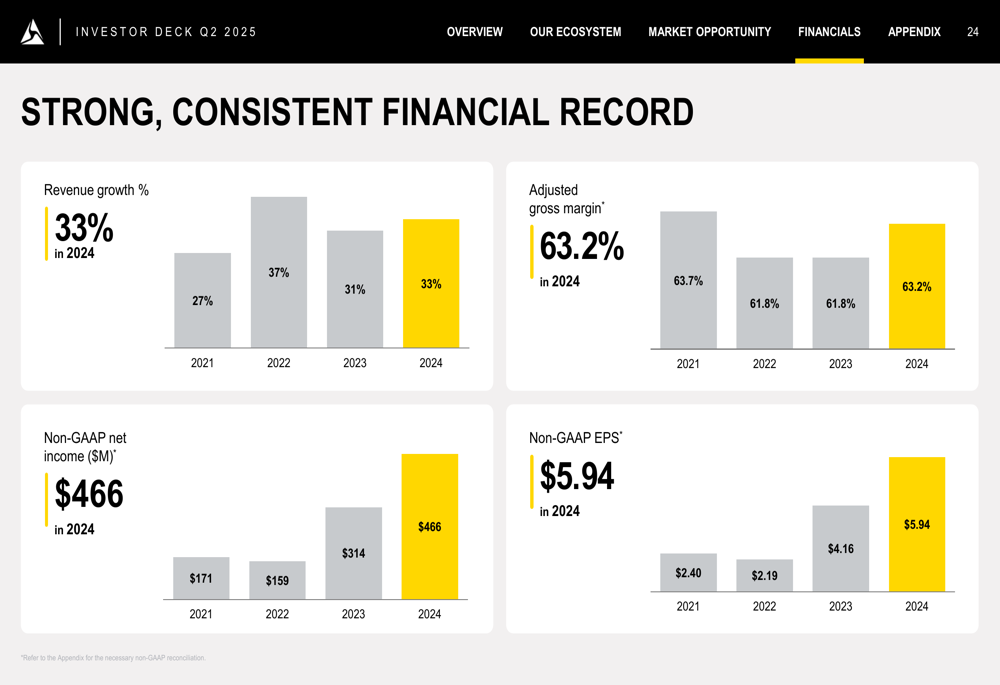

The company’s financial results demonstrate consistent performance across key metrics, as illustrated in this comprehensive financial overview:

Axon’s 2024 performance showed 33% revenue growth with an adjusted gross margin of 63.2%. Non-GAAP net income reached $466 million with earnings per share of $5.94. This strong performance has continued into 2025, with Q1 earnings per share of $1.41 exceeding analyst expectations of $1.30.

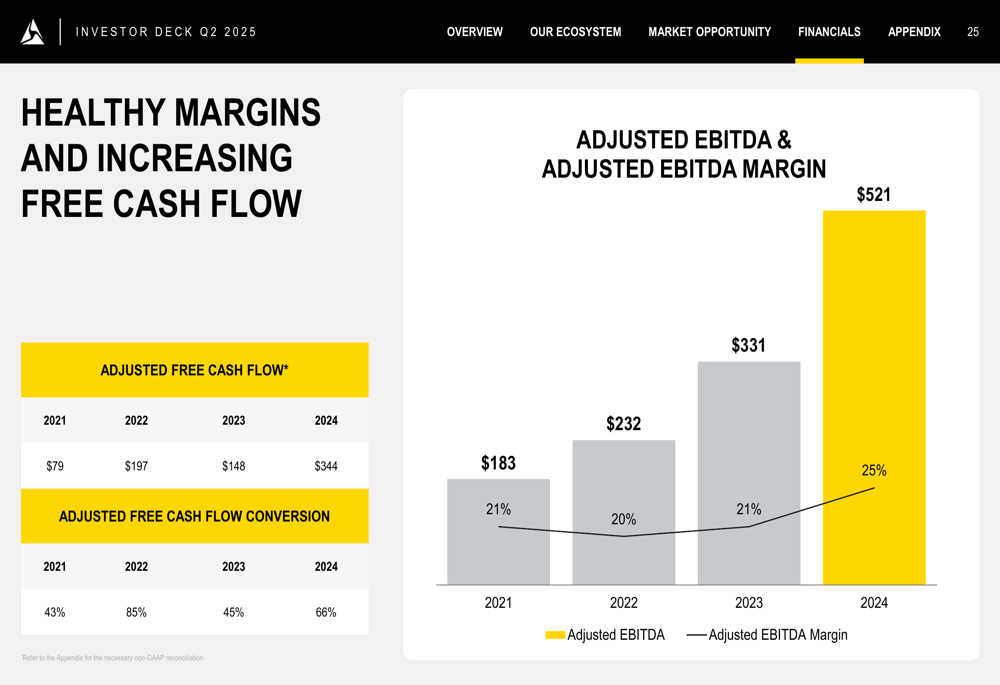

The company’s cash generation capabilities have also improved, with adjusted free cash flow reaching $344 million in 2024, representing a 66% conversion rate:

Product Ecosystem and Growth Strategy

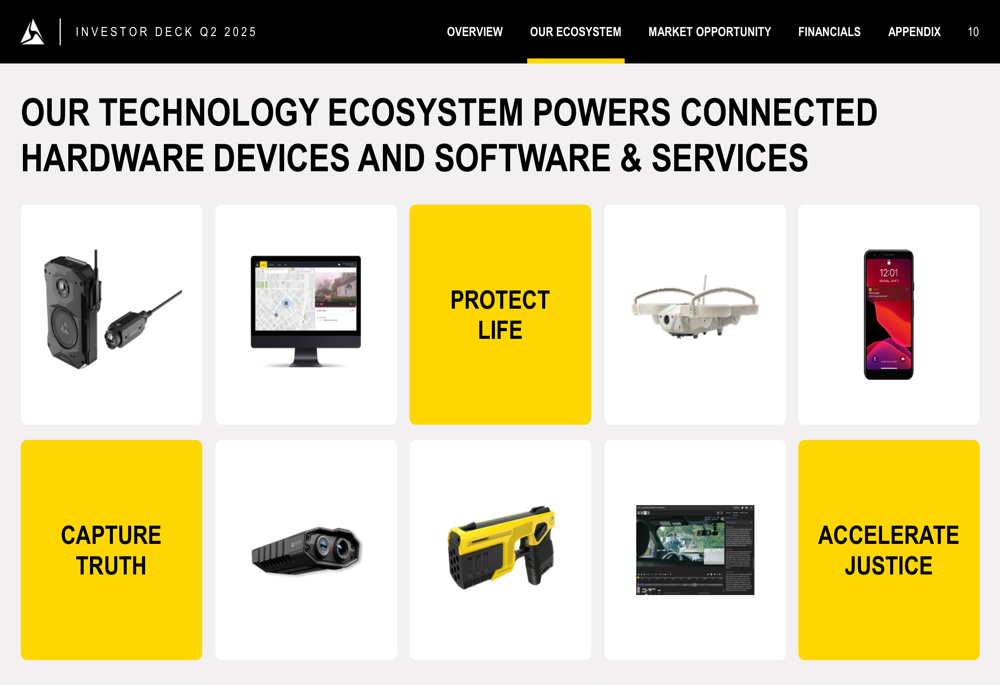

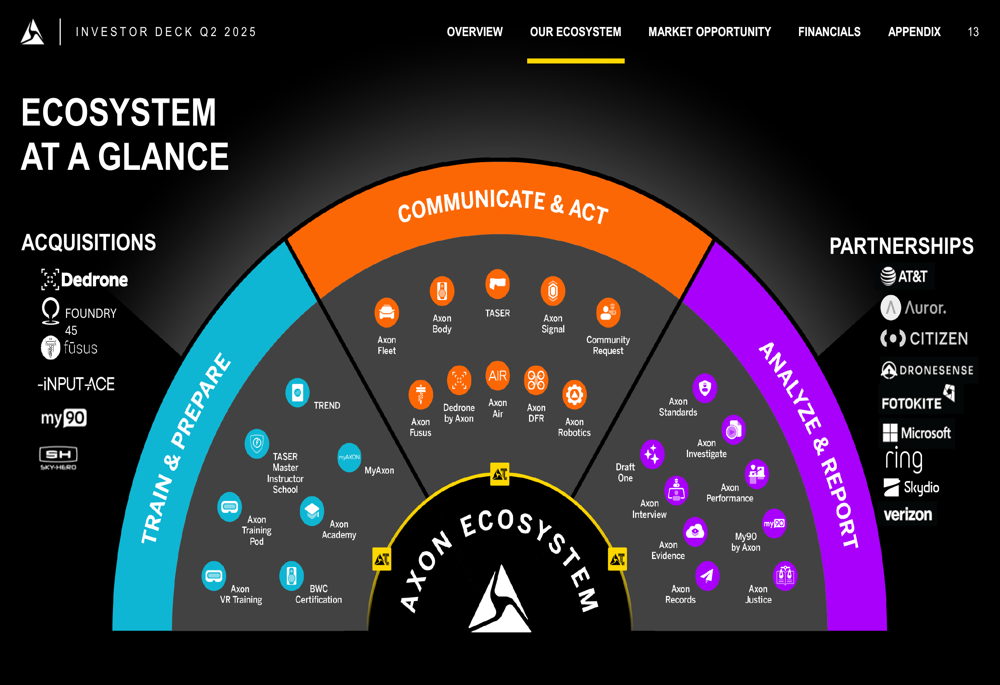

Axon’s comprehensive technology ecosystem spans hardware devices and software services designed to work together seamlessly. The ecosystem includes TASER devices for de-escalation, connected video and sensors for evidence capture, and drones for situational awareness, all supported by cloud software for evidence management and real-time operations.

The following visualization illustrates how these products interconnect within Axon’s ecosystem:

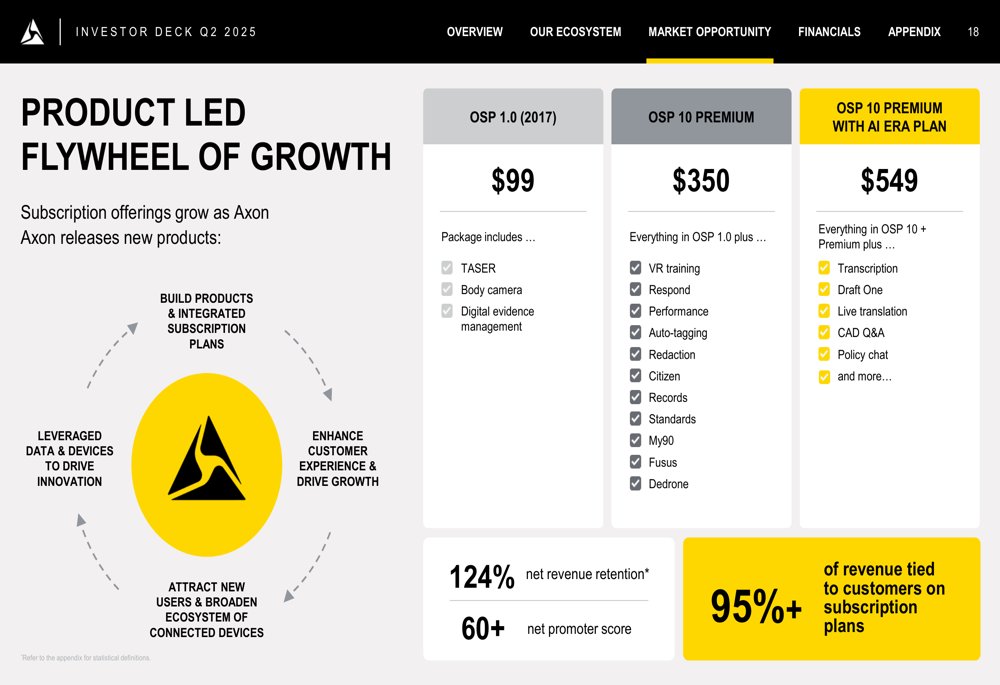

The company’s growth strategy follows a product-led flywheel approach, where new products drive subscription adoption, which in turn funds further innovation. Axon’s Officer Safety Plan (OSP) subscription bundles have been particularly successful, with monthly prices ranging from $99 to $549 depending on the feature set:

This subscription model has proven highly effective, with 95% of revenue now coming from customers on subscription plans and a net revenue retention rate of 124%, indicating strong customer satisfaction and upselling success.

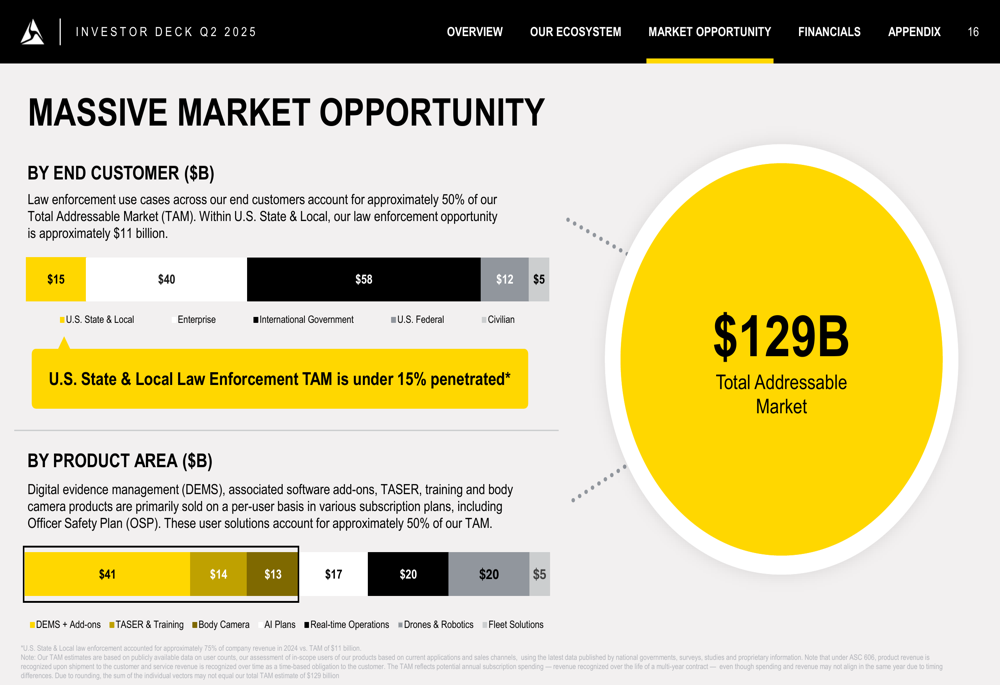

Market Opportunity (SO:FTCE11B) and Expansion

Axon identifies a total addressable market of $129 billion, with its current penetration in the U.S. State & Local Law Enforcement market under 15%. The company is pursuing multiple growth vectors, including international expansion, federal contracts, enterprise safety, and civilian markets.

The breakdown of this market opportunity is detailed in the following chart:

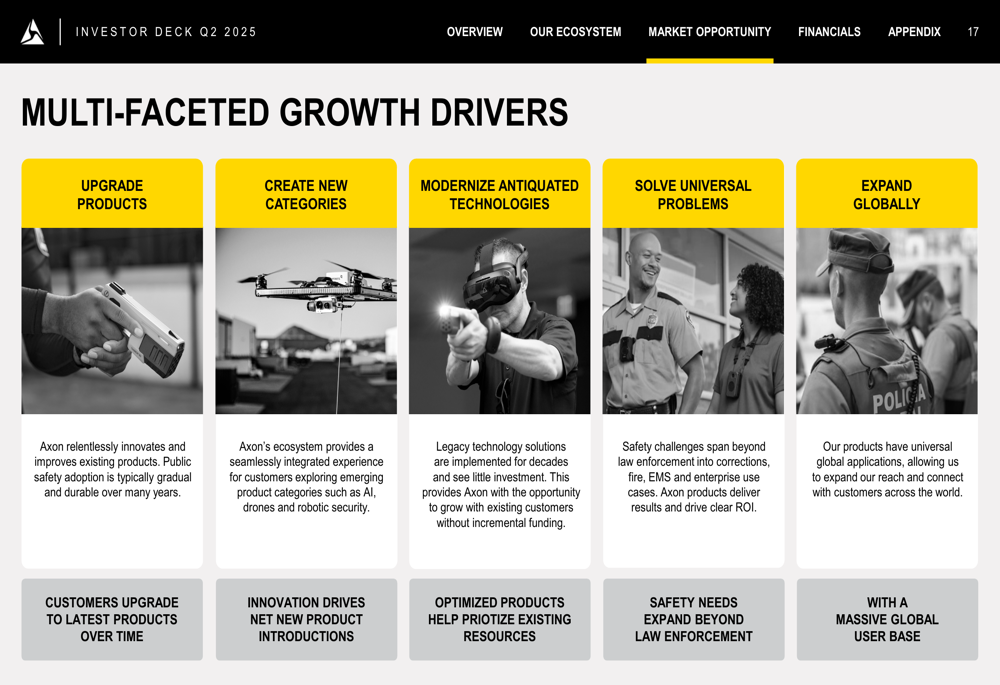

To capture this opportunity, Axon is pursuing a multi-faceted growth strategy that includes upgrading existing products, creating new categories, modernizing antiquated technologies, solving universal problems, and expanding globally:

The company has strengthened its ecosystem through strategic acquisitions and partnerships. Recent acquisitions include Dedrone and Fusus, while partnerships with companies like AT&T (NYSE:T) and Aurora enhance Axon’s capabilities and market reach:

Forward Guidance and Outlook

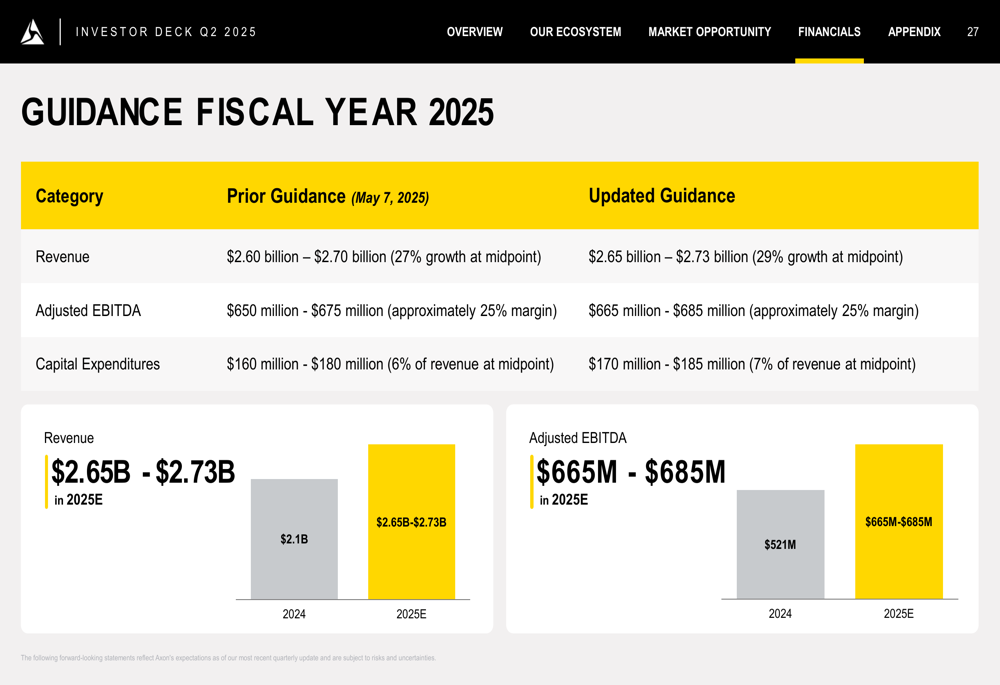

Looking ahead, Axon provided guidance for fiscal year 2025, projecting revenue between $2.65 billion and $2.73 billion, representing 29% growth at the midpoint. The company expects to maintain its adjusted EBITDA margin at approximately 25%, with capital expenditures of $170-185 million (7% of revenue).

The detailed guidance is presented in the following slide:

This guidance aligns with statements made during the Q1 earnings call, where management projected annual revenue between $2.6 billion and $2.7 billion, representing 27% growth at the midpoint.

CEO Rick Smith has articulated a vision where "violence and crime rarely occur because it is simply so unappealing and so well deterred," while President Josh Isner emphasized the company’s commitment to innovation and execution capability.

As Axon continues to invest in AI capabilities and new product development, the company appears well-positioned to maintain its growth trajectory while pursuing its mission of protecting life through technology. However, potential challenges include tariff impacts that could affect EBITDA margins, ongoing R&D investments that may strain resources, and execution risks as the company expands into new sectors and geographies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.