Intel stock spikes after report of possible US government stake

Baker Hughes Co (NASDAQ:BKR) reported strong second-quarter 2025 results on July 23, highlighting continued margin expansion and strategic portfolio optimization despite challenges in traditional energy markets. The company’s shares traded at $40.00 in after-hours trading, up 0.38% following the earnings release.

Quarterly Performance Highlights

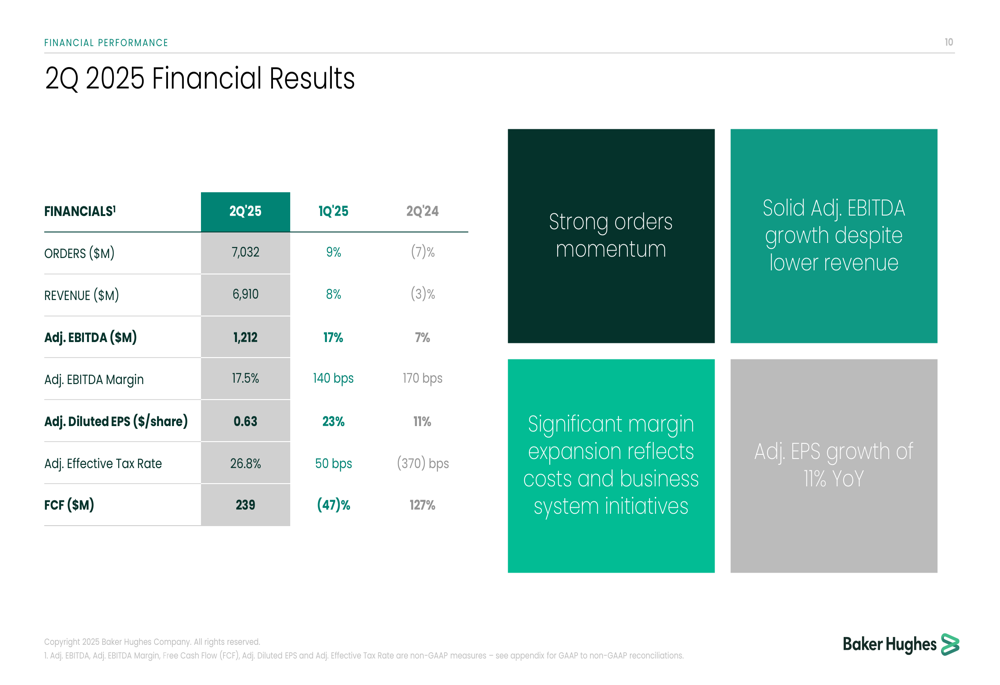

Baker Hughes delivered robust financial results for Q2 2025, marking the tenth consecutive quarter of meeting or exceeding EBITDA guidance. The company reported revenue of $6.91 billion, adjusted EBITDA of $1.21 billion, and adjusted EBITDA margin of 17.5%, representing a 170 basis point improvement year-over-year.

"We’ve now met or exceeded EBITDA guidance for the 10th consecutive quarter," said Lorenzo Simonelli, Chairman and CEO of Baker Hughes, highlighting the company’s consistent execution amid market volatility.

As shown in the following financial results summary:

The company reported orders of $7.03 billion, up 9% sequentially but down 7% year-over-year. Adjusted diluted EPS reached $0.63, representing 11% growth compared to the same period last year. Free cash flow was $239 million, up 127% year-over-year despite a 47% sequential decline.

Baker Hughes returned $423 million to shareholders during the quarter, including $227 million in dividends and $196 million in share repurchases, underscoring its commitment to shareholder returns.

Strategic Portfolio Optimization

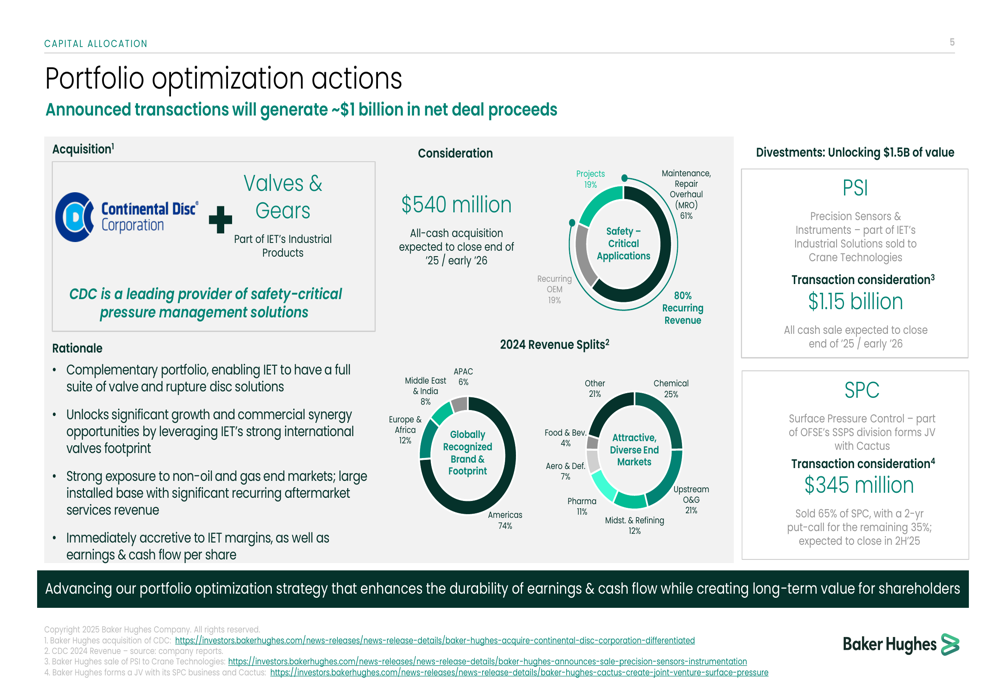

A cornerstone of Baker Hughes’ strategy is its portfolio optimization initiative, which the company expects will generate approximately $1 billion in net deal proceeds. The initiative includes both strategic acquisitions and divestments designed to enhance the company’s competitive positioning in high-growth markets.

The company’s portfolio transformation is illustrated in the following slide:

On the acquisition front, Baker Hughes announced the purchase of Continental Disc Corporation (CDC), a provider of safety-critical pressure management solutions, for $540 million in an all-cash transaction expected to close by the end of 2025 or early 2026.

Simultaneously, the company is divesting non-core assets, including the sale of Precision Sensors & Instruments (PSI) to Crane Technologies for $1.15 billion and the sale of 65% of its Surface Pressure Control (SPC) business as part of a joint venture with Cactus (NYSE:WHD) for $345 million.

"Our portfolio optimization strategy focuses on unlocking value through the sale of non-core assets and reinvesting in core growth opportunities with higher returns," explained Ahmed Moghal, Executive Vice President and CFO. "This approach enhances our earnings quality and cash flow while creating long-term value for shareholders."

Segment Performance

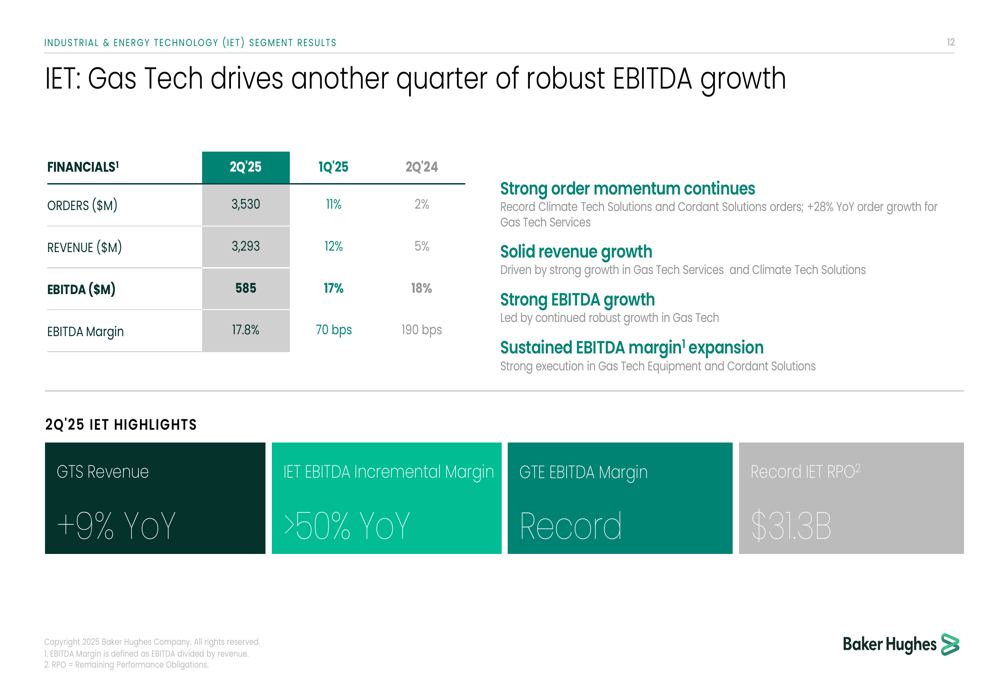

Baker Hughes’ Industrial & Energy Technology (IET) segment delivered particularly strong results, with orders of $3.53 billion, revenue of $3.29 billion, and EBITDA of $585 million. The segment’s EBITDA margin expanded by 190 basis points year-over-year to 17.8%.

The following slide details the IET segment’s performance:

The Gas Technology Services (GTS) business within IET saw revenue growth of 9% year-over-year, while the segment as a whole achieved an incremental EBITDA margin exceeding 50% compared to the previous year. The company also reported record IET remaining performance obligations (RPO) of $31.3 billion.

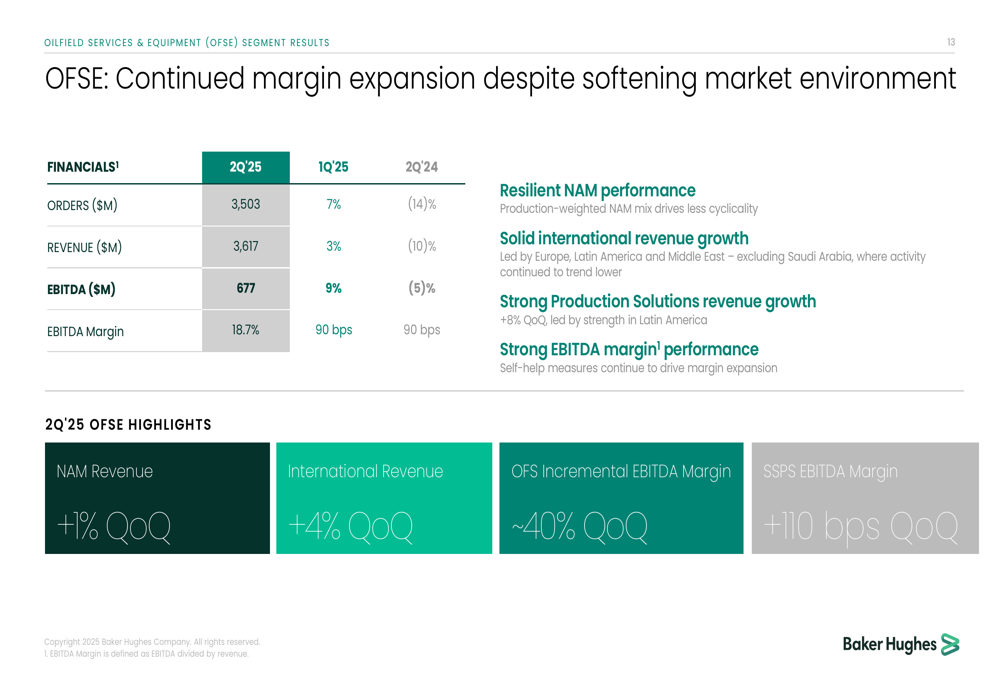

Meanwhile, the Oilfield Services & Equipment (OFSE) segment demonstrated resilience in a challenging market environment, with continued margin expansion despite softening demand:

OFSE reported orders of $3.50 billion, revenue of $3.62 billion, and EBITDA of $677 million, with an EBITDA margin of 18.7% – representing a 90 basis point improvement both sequentially and year-over-year. North American revenue increased 1% quarter-over-quarter, while international revenue grew 4% sequentially.

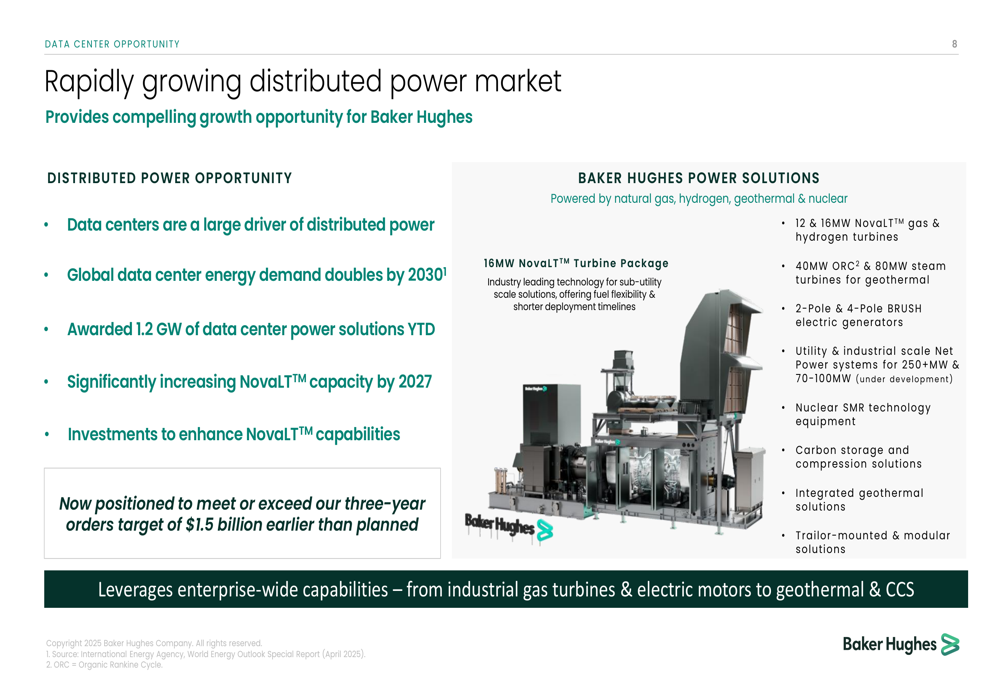

Data Center Opportunity (SO:FTCE11B) Emerges as Growth Driver

A significant bright spot in Baker Hughes’ strategy is its growing focus on the data center market, which the company identifies as a major growth opportunity amid the energy transition. Global data center energy demand is projected to double by 2030, creating substantial opportunities for Baker Hughes’ power solutions.

The company’s data center strategy is outlined in the following slide:

Baker Hughes has already been awarded 1.2 GW of data center power solutions year-to-date, including agreements to supply 30 NovaLT™ turbines delivering almost 500 MW of power to data centers in the U.S. The company is significantly increasing its NovaLT™ capacity by 2027 and now expects to meet or exceed its three-year orders target of $1.5 billion earlier than planned.

"Data centers represent a compelling growth opportunity for Baker Hughes as we leverage our expertise in distributed power solutions," noted Simonelli. "Our NovaLT™ turbines are well-positioned to address the increasing power demands of this rapidly expanding market."

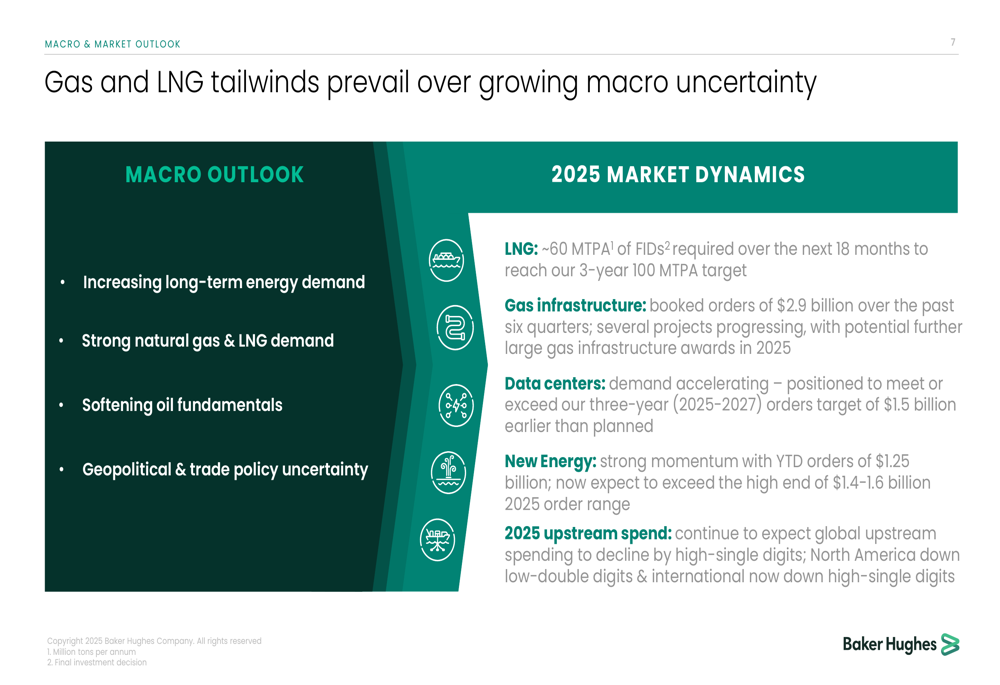

Market Outlook and Guidance

Baker Hughes provided a mixed outlook for the remainder of 2025, noting that gas and LNG tailwinds prevail over growing macroeconomic uncertainty. The company highlighted strong natural gas and LNG demand but acknowledged softening oil fundamentals and geopolitical uncertainties.

The company’s market perspective is summarized in this outlook slide:

For the third quarter of 2025, Baker Hughes expects revenue between $6.45 billion and $7.15 billion and adjusted EBITDA between $1.10 billion and $1.28 billion. For the full year 2025, the company projects revenue of $26.5 billion to $27.7 billion and adjusted EBITDA of $4.45 billion to $4.9 billion.

The company maintained its estimate of a $100 million to $200 million potential net impact to consolidated 2025 EBITDA from tariffs, based on currently announced rates with no further trade policy escalation.

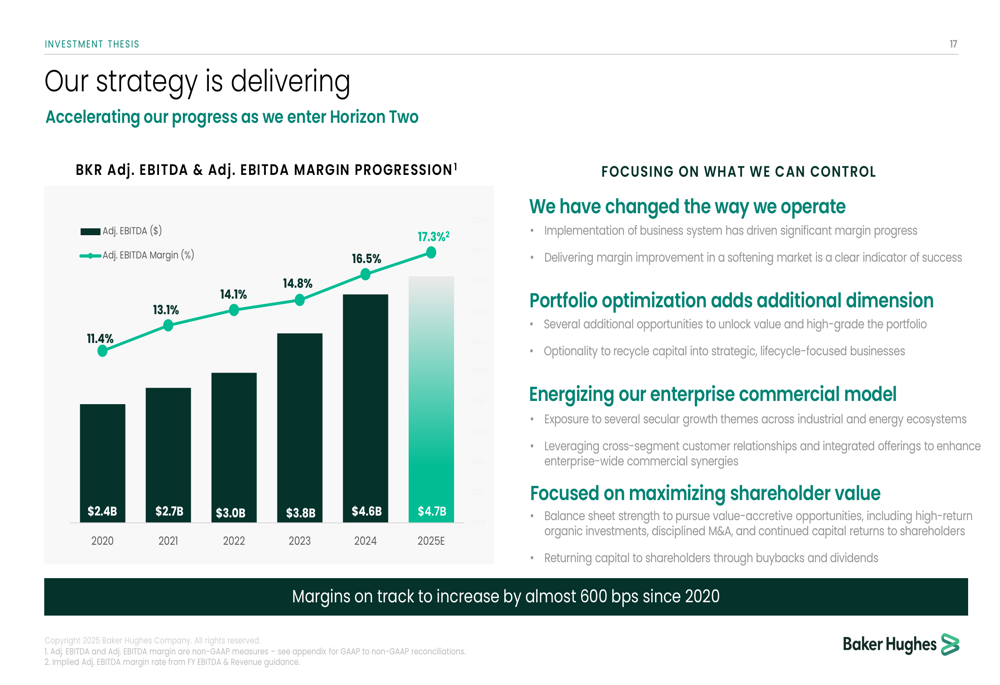

Long-Term Investment Thesis

Baker Hughes emphasized that its strategy is delivering results as the company enters what it calls "Horizon Two" of its transformation journey. Since 2020, adjusted EBITDA has nearly doubled from $2.4 billion to a projected $4.7 billion in 2025, while adjusted EBITDA margins have expanded by almost 600 basis points from 11.4% to 17.3%.

The company’s long-term performance trajectory is illustrated in this investment thesis slide:

"We remain focused on what we can control – optimizing our portfolio, energizing our enterprise commercial model, and maximizing shareholder value," said Simonelli. "Our strategy is delivering results, and we’re well-positioned to continue this momentum despite market challenges."

With a robust balance sheet featuring a net debt to LTM adjusted EBITDA ratio of just 0.6x and liquidity of $6.1 billion, Baker Hughes appears well-positioned to navigate market uncertainties while continuing to invest in growth opportunities and return capital to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.