Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Balco Group AB (STO:BALCO) reported mixed results in its Q2 2025 presentation, revealing a record-high order intake that contrasted sharply with declining sales and profitability. The Nordic balcony solutions specialist, which has seen its stock price decline by 0.75% to 26.30 SEK on July 14, continues to face profitability challenges despite growing market activity in key regions.

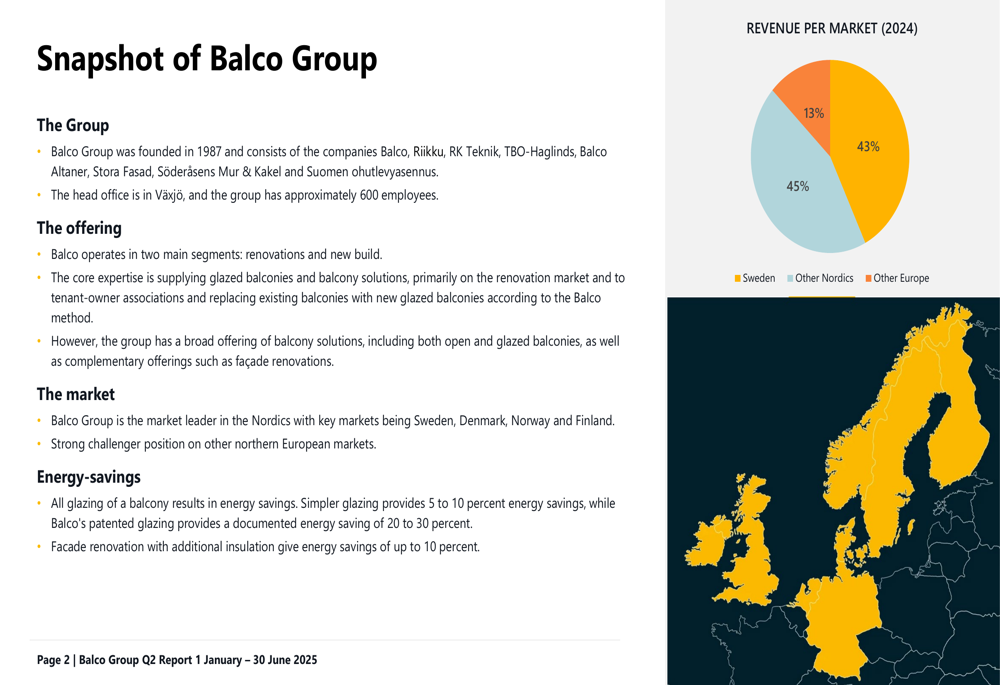

The company, founded in 1987 and headquartered in Växjö, Sweden, maintains its position as the market leader in the Nordics with approximately 600 employees. Balco specializes in glazed balconies for both renovation and new build projects, with operations primarily focused in Sweden, Denmark, Norway, and Finland.

As shown in the following revenue distribution chart, Sweden remains Balco’s largest market, accounting for 45% of revenue, followed by other Nordic countries at 43% and other European markets at 13%:

Quarterly Performance Highlights

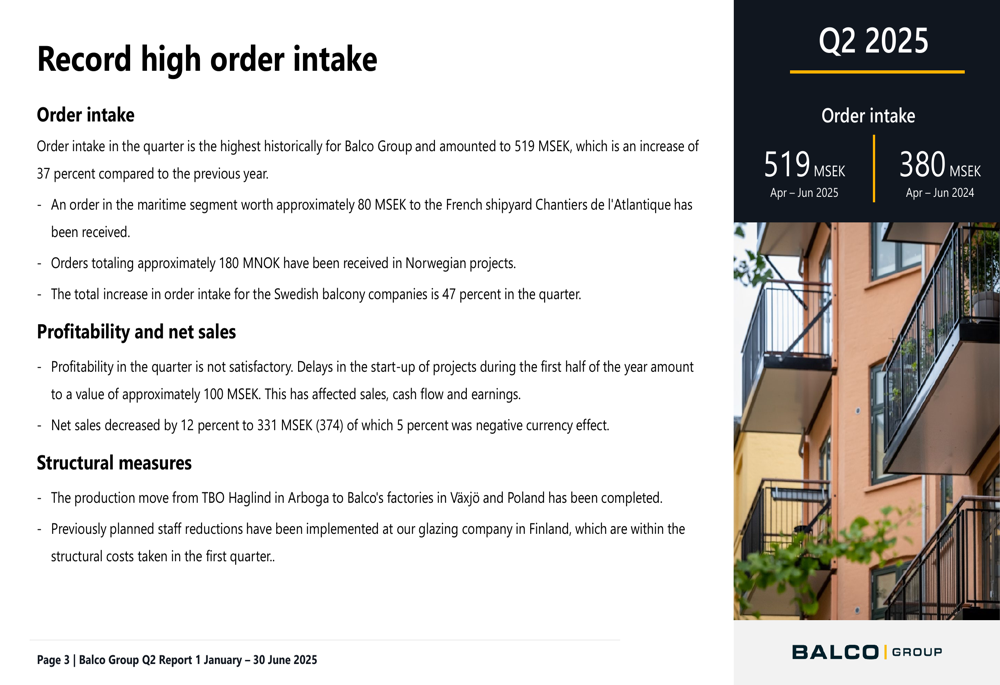

Balco’s Q2 2025 was characterized by a stark contrast between robust order intake and weakening financial performance. The company reported a record order intake of 519 MSEK, representing a 37% increase compared to Q2 2024 (380 MSEK). This growth was driven by significant orders including an 80 MSEK maritime segment order from Chantiers de l’Atlantique and 180 MNOK in Norwegian projects. Swedish balcony companies particularly excelled with a 47% increase in order intake.

However, this order strength did not translate to current financial performance. Net sales decreased by 12% to 331 MSEK (compared to 374 MSEK in Q2 2024), with a 5% negative currency effect. Adjusted operating result (EBITA) fell to 6 MSEK from 19 MSEK in the previous year, resulting in a margin contraction from 5.0% to just 1.9%. The company attributed this disappointing profitability to delayed projects worth approximately 100 MSEK.

The following chart illustrates these key performance metrics, highlighting the divergence between order intake growth and financial results:

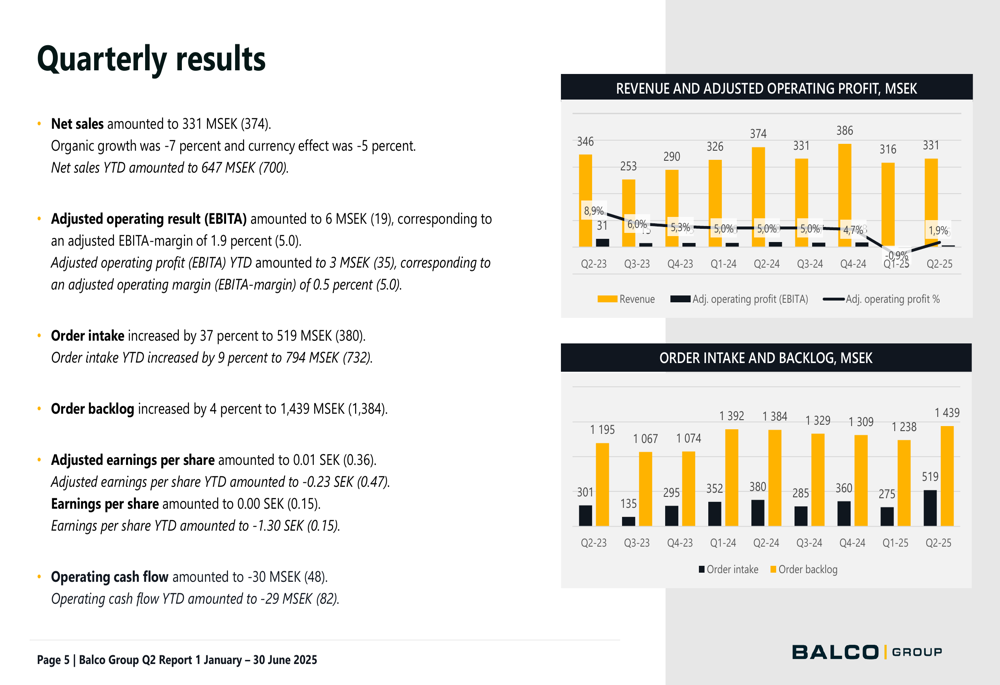

A more comprehensive view of Balco’s quarterly performance shows the company’s revenue and profitability trends alongside the growing order backlog:

Segment Analysis

Balco operates through two main segments: Renovation and New Build, with the former representing the majority of the company’s business.

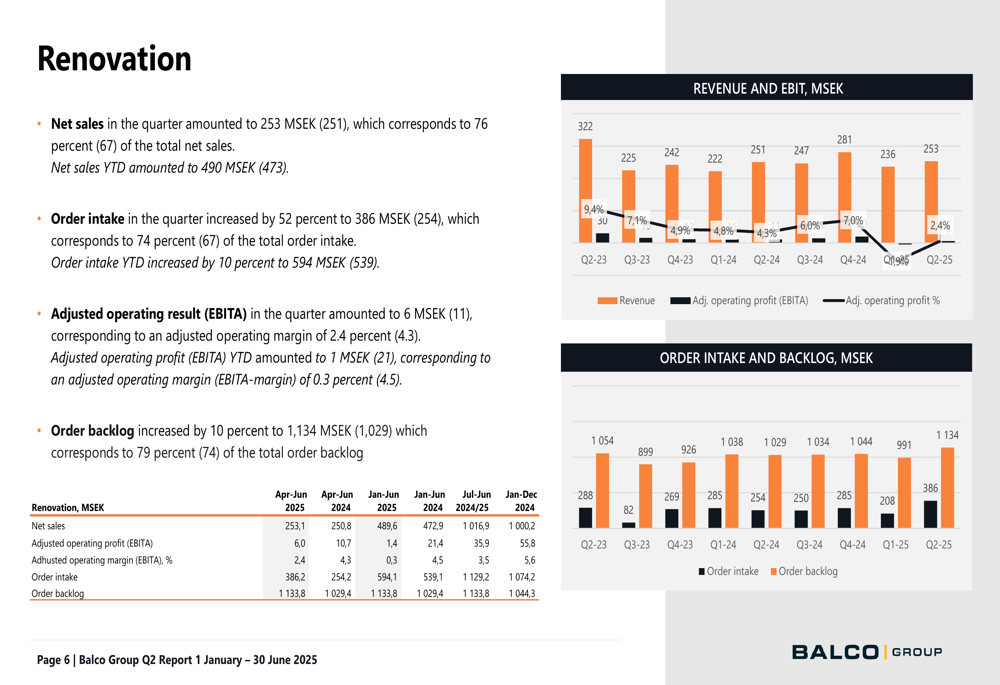

The Renovation segment, accounting for 76% of total net sales, reported stable revenue of 253 MSEK (251 MSEK in Q2 2024). However, profitability declined significantly with adjusted EBITA falling to 6 MSEK from 11 MSEK, resulting in a margin reduction from 4.3% to 2.4%. The segment’s order intake showed remarkable growth of 52% to 386 MSEK, representing 74% of total orders. This growth contributed to a 10% increase in the segment’s order backlog, which reached 1,134 MSEK.

The following chart details the Renovation segment’s performance metrics:

The New Build segment, representing 24% of total sales, experienced a more pronounced decline with net sales falling to 78 MSEK from 123 MSEK in Q2 2024. Adjusted EBITA dropped to just 1 MSEK from 7 MSEK, with margins contracting from 5.5% to 0.8%. Despite these challenges, order intake increased by 6% to 133 MSEK, though the segment’s order backlog decreased to 305 MSEK from 355 MSEK.

Financial Position

Balco’s financial position shows increasing strain, with equity amounting to 753 MSEK (798 MSEK) and an equity/assets ratio of 45% (47%). More concerning is the significant increase in leverage, with interest-bearing net debt including leasing debt to adjusted EBITDA rising to 5.6 times from 3.3 times a year earlier.

The company disclosed that it has obtained a waiver with its bank that is valid until the end of the year, suggesting potential covenant issues. The banking agreement with Danske Bank (CSE:DANSKE) remains valid until March 31, 2028. Operating cash flow was negative at -30 MSEK, compared to a positive 48 MSEK in Q2 2024.

This deterioration in financial metrics follows the challenging first quarter of 2025, when Balco reported a negative adjusted EBITA and saw its stock price drop by 12.77%.

Market Context & Outlook

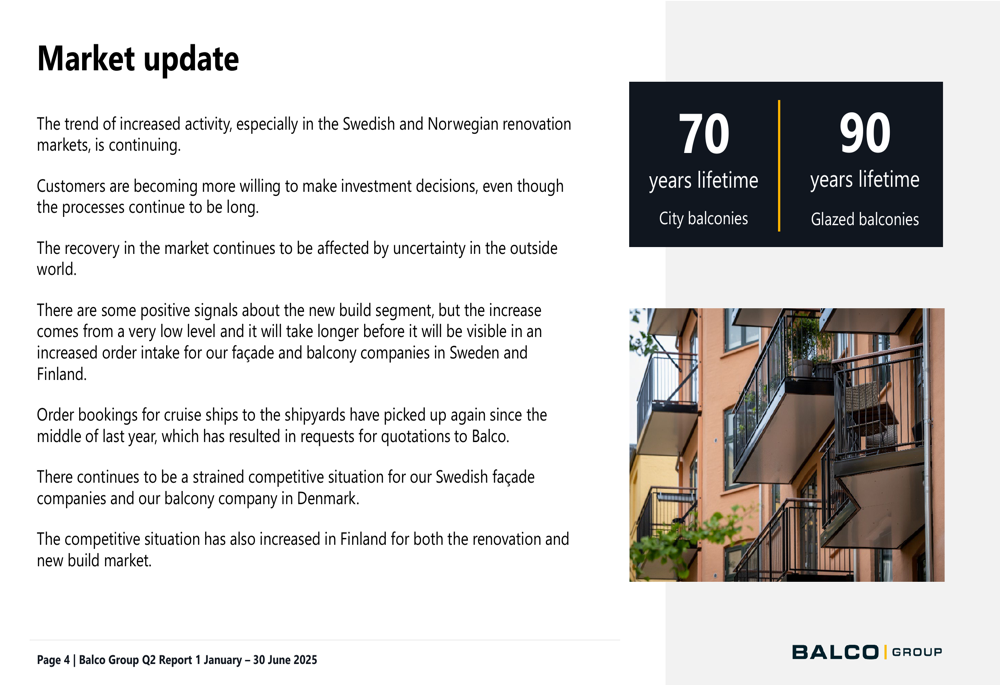

Despite current financial challenges, Balco’s management expressed cautious optimism about market conditions. The company noted increased activity in the Swedish and Norwegian renovation markets, with customers becoming more willing to make investment decisions, though decision processes remain lengthy.

The presentation highlighted positive signals in the new build segment, particularly noting that order bookings for cruise ships have picked up since mid-2024. However, the company faces a strained competitive environment in several key markets, including its Swedish façade companies, Danish balcony operations, and both renovation and new build segments in Finland.

Balco continues to emphasize its product durability as a key differentiator, noting that its City Balconies have a 70-year lifetime while its Glazed balconies last up to 90 years. The company also highlights the energy efficiency of its solutions, with its patented glazing providing 20-30% energy savings.

As shown in this market update slide, Balco maintains a strong position despite competitive pressures:

Forward-Looking Statements

Looking ahead, Balco’s management indicated that upcoming quarters will continue to be affected in terms of sales and earnings as the company focuses on profitability and cost savings. The company has completed production moves from TBO Haglind and implemented staff reductions in Finland as part of its structural measures.

Management emphasized the company’s strong market position, high quality products, and long durability as foundations for future growth. The cautiously optimistic outlook for renovation projects contrasts with expectations of a longer recovery period for the new build segment.

This forward-looking perspective comes after a challenging first half of 2025, with year-to-date adjusted EBITA at just 3 MSEK compared to 35 MSEK in the same period last year, and a margin of only 0.5% versus 5.0% previously.

Balco’s mixed Q2 results reflect a company in transition, with strong order momentum providing hope for future recovery while current financial performance remains under pressure. Investors will likely focus on whether the growing order backlog can translate into improved profitability in coming quarters, and whether the company can address its increasing debt levels without further equity dilution.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.