Street Calls of the Week

Introduction & Market Context

Banc of California (NYSE:BANC) released its second quarter 2025 earnings presentation on July 24, showing significant year-over-year improvement in adjusted performance metrics despite flat reported earnings per share. The regional bank, which has a market capitalization of approximately $2.29 billion based on recent trading, continues to navigate a challenging economic environment while implementing strategic initiatives to enhance shareholder value.

The bank’s stock closed at $15.26 on July 23, 2025, up 1.26% from the previous close, and has traded between $11.52 and $18.08 over the past 52 weeks. Following its Q1 2025 earnings release, which showed an EPS beat but revenue miss, the stock had experienced some volatility.

Quarterly Performance Highlights

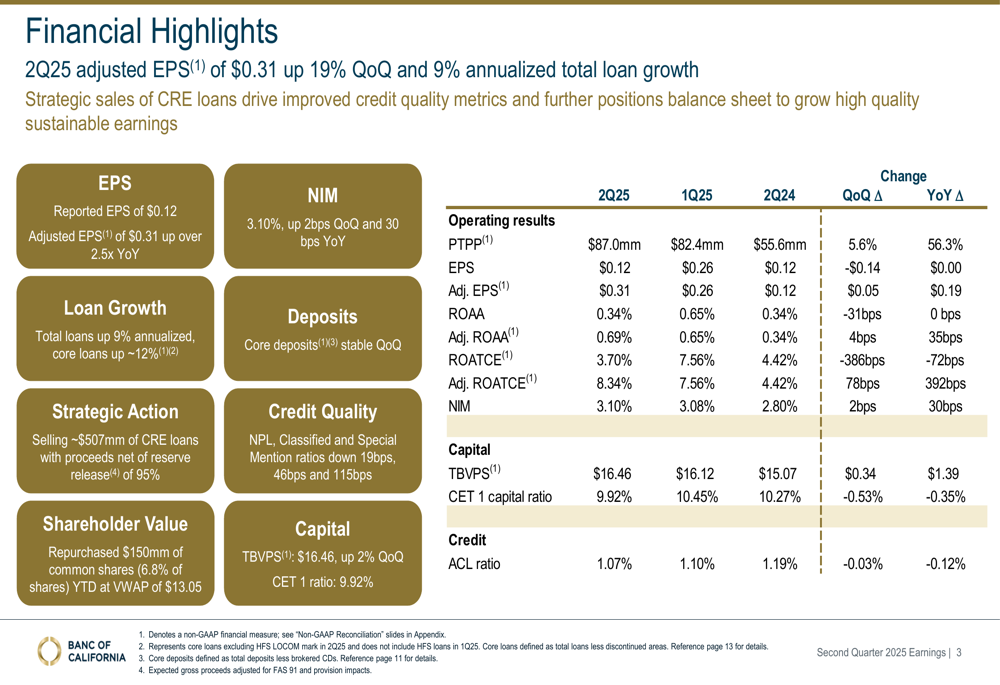

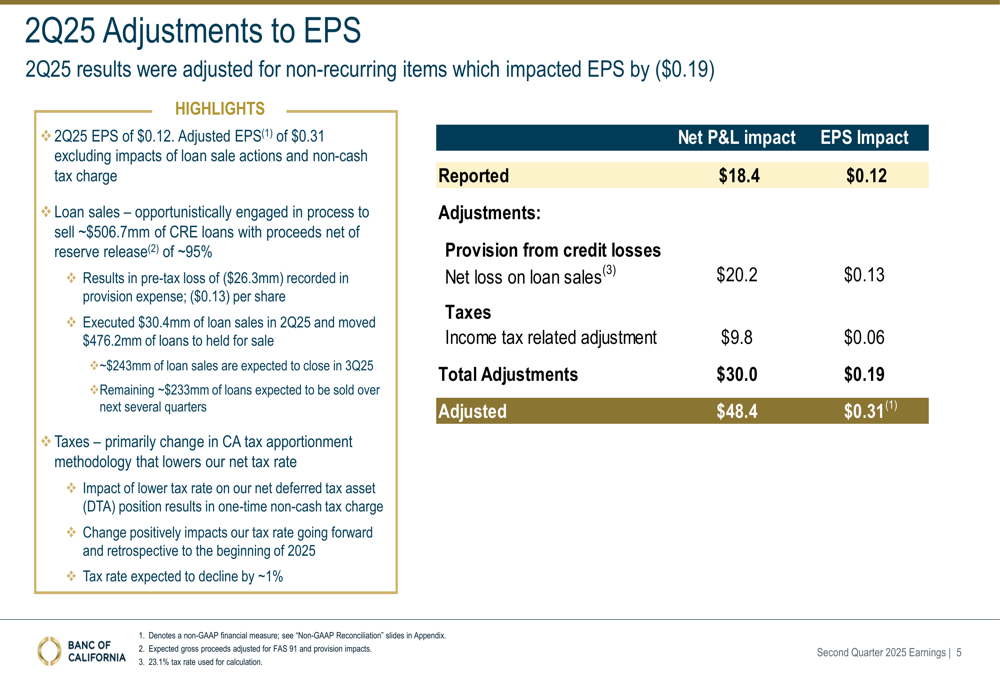

Banc of California reported Q2 2025 adjusted earnings per share of $0.31, representing a 158% increase from $0.12 in the same quarter last year and a 19% improvement from $0.26 in Q1 2025. However, reported EPS remained flat year-over-year at $0.12, primarily due to a pre-tax loss of $26.3 million related to strategic loan sales.

As shown in the following financial highlights chart, the bank demonstrated improvement across several key metrics:

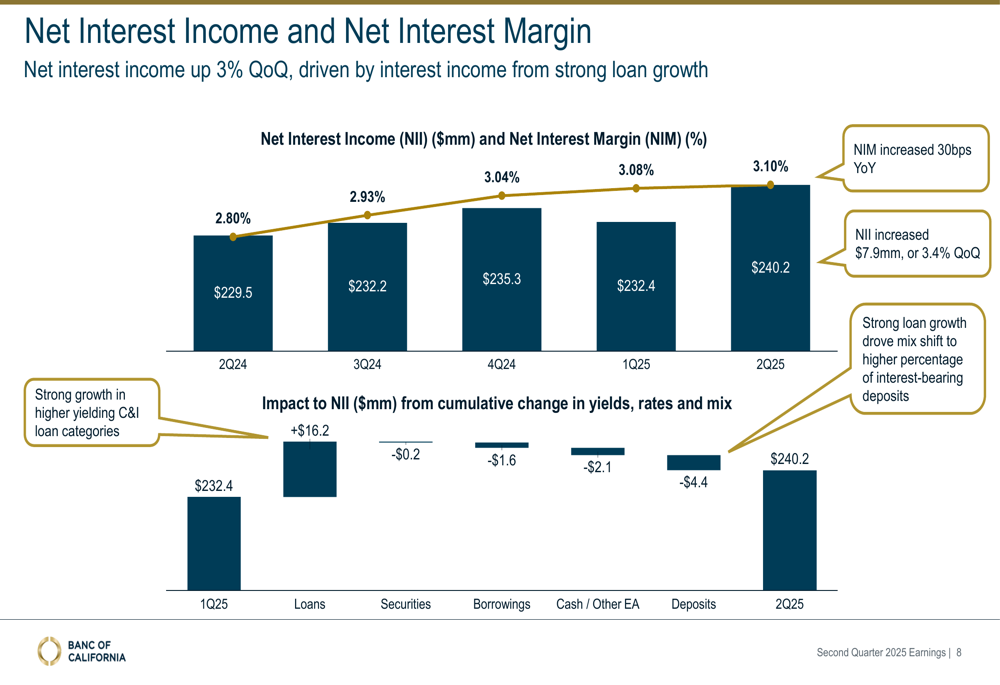

The bank’s net interest margin (NIM) expanded to 3.10%, up 2 basis points quarter-over-quarter and 30 basis points year-over-year. This improvement contributed to pre-tax pre-provision (PTPP) income of $87.0 million, compared to $82.4 million in Q1 2025 and $55.6 million in Q2 2024.

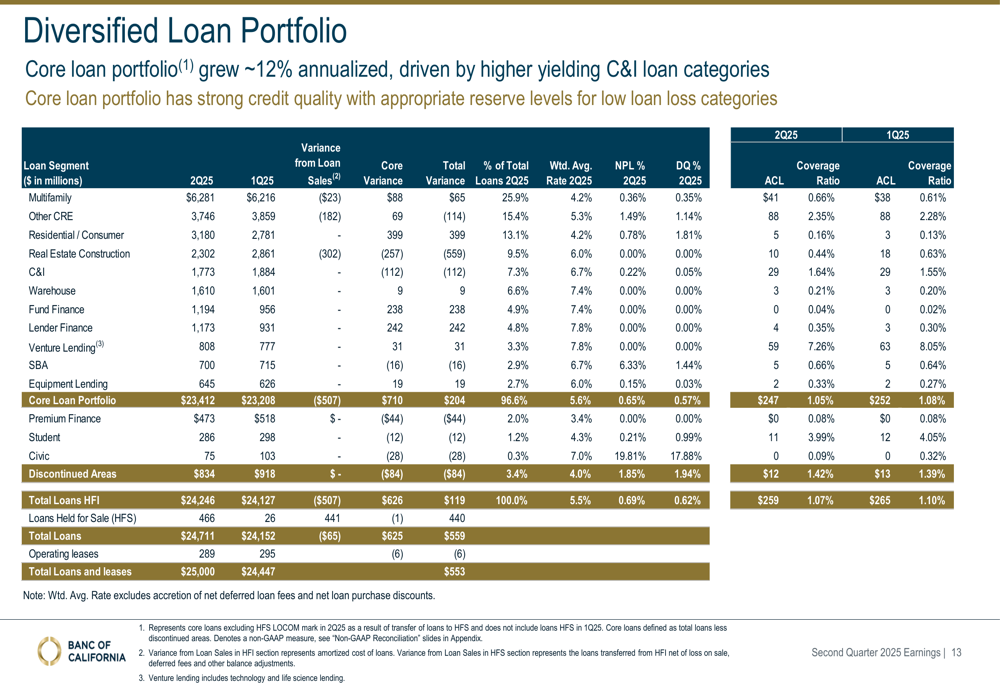

Total (EPA:TTEF) loans increased at an annualized rate of 9%, with core loans growing at approximately 12%, driven by higher-yielding commercial and industrial loan categories. Core deposits remained stable quarter-over-quarter.

Detailed Financial Analysis

The difference between reported and adjusted earnings is primarily attributable to strategic loan sales and related provisions, as detailed in the following breakdown:

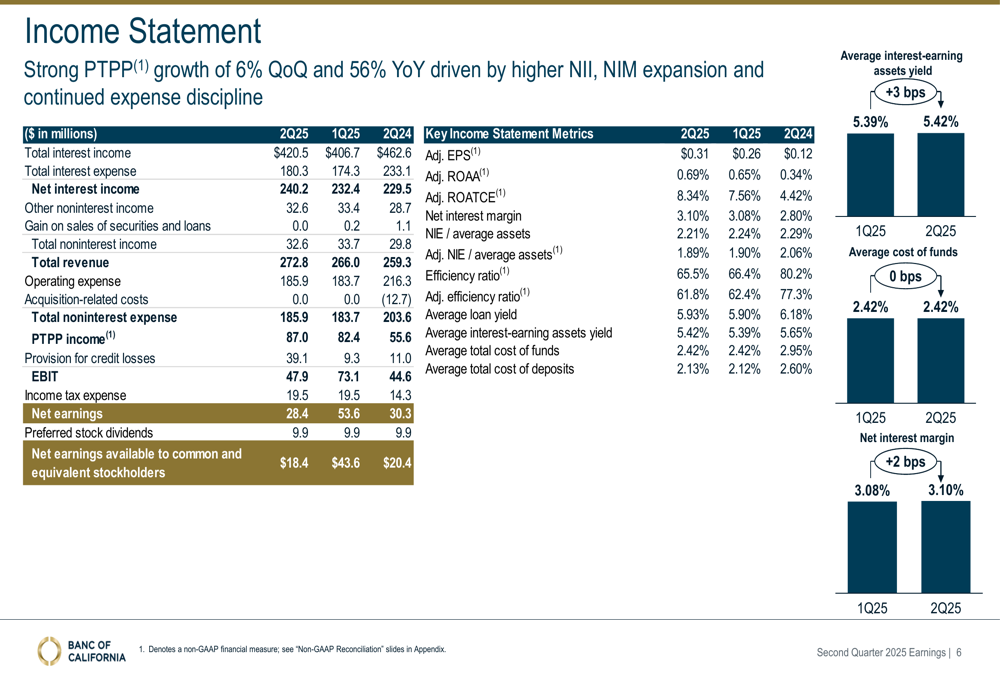

The bank’s income statement shows strong PTPP growth and increased net interest income, with total revenue reaching $272.8 million in Q2 2025 compared to $266.0 million in Q1 2025 and $259.3 million in Q2 2024.

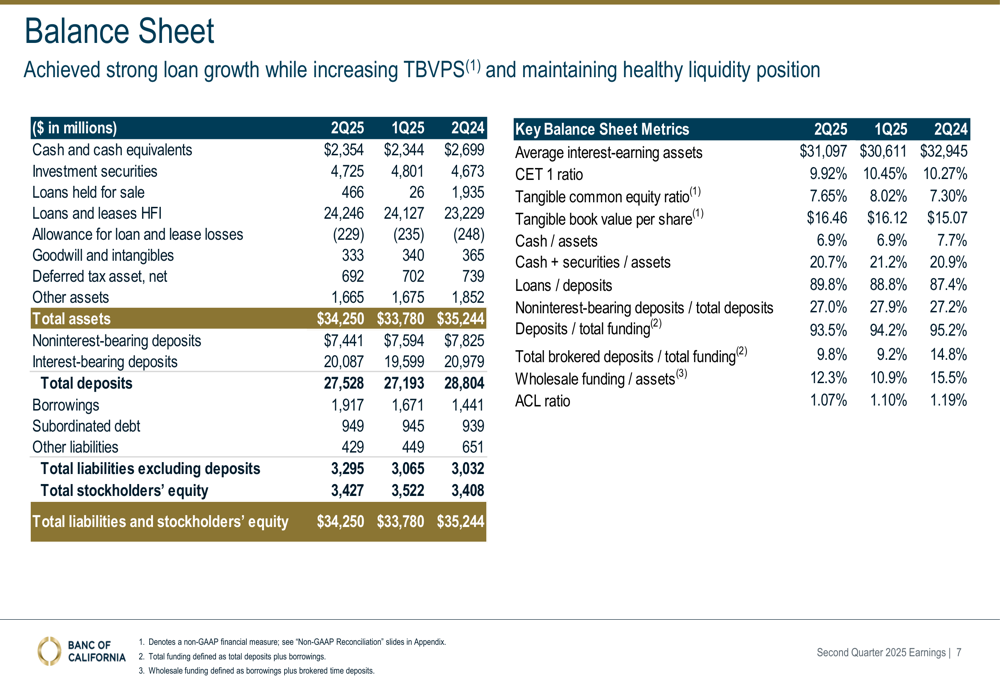

On the balance sheet side, total assets stood at $34.25 billion as of June 30, 2025, up from $33.78 billion at the end of Q1 2025 but down from $35.24 billion a year ago. Tangible book value per share increased to $16.46, representing 2% growth quarter-over-quarter and 9.2% year-over-year.

The bank’s net interest income and margin have shown consistent improvement over the past year, as illustrated in the following chart:

Strategic Initiatives

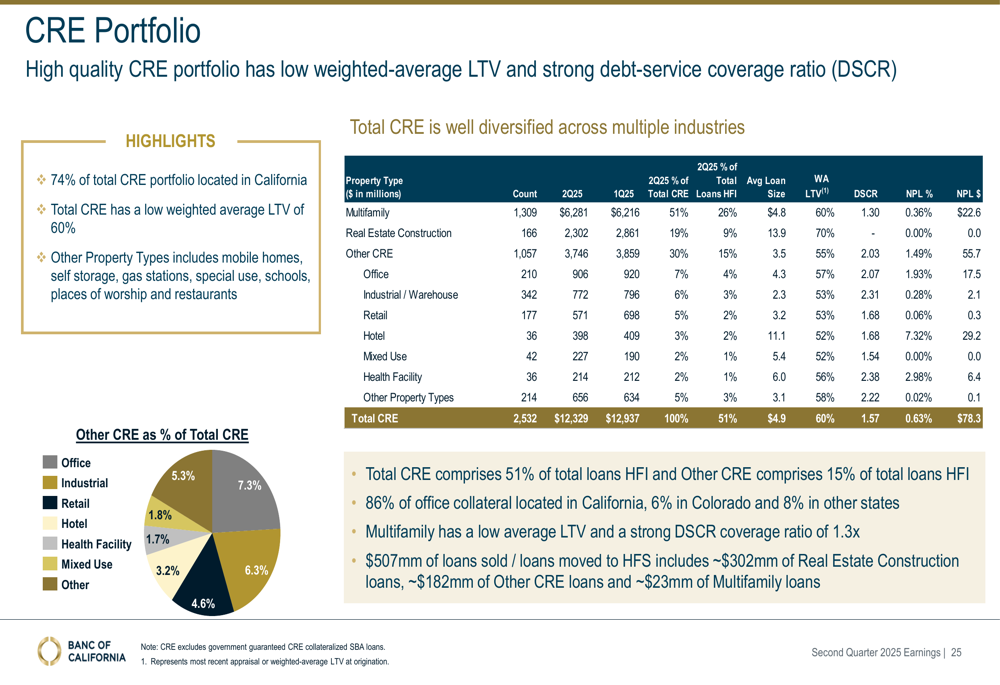

A key strategic action during the quarter was the sale of approximately $507 million of commercial real estate loans, with proceeds net of reserve release at 95%. This move contributed to improvements in credit quality metrics, with nonperforming loans, classified loans, and special mention ratios declining by 19 basis points, 46 basis points, and 115 basis points, respectively.

The bank has maintained a diversified loan portfolio with strong credit quality and appropriate reserve levels, particularly for low loan loss categories:

Banc of California has also been active in returning capital to shareholders, repurchasing $150 million of common shares year-to-date, representing approximately 6.8% of outstanding shares at an average price of $13.05. The CET1 capital ratio stood at 9.92% at quarter-end, down from 10.45% in Q1 2025 but still well above regulatory requirements.

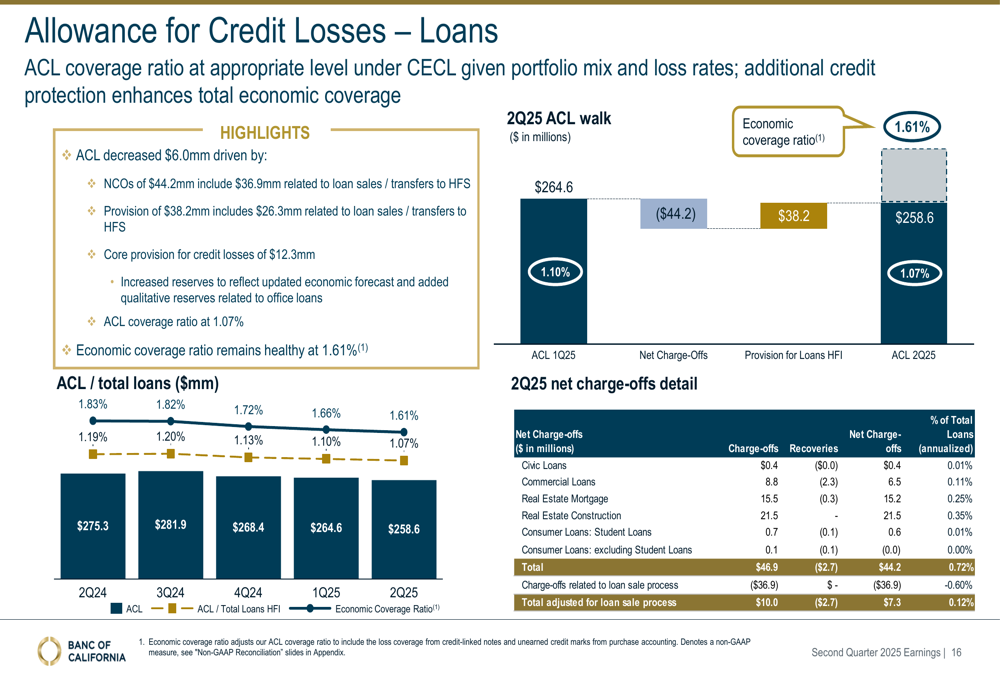

The bank’s allowance for credit losses (ACL) coverage ratio was 1.07%, which management described as appropriate given the portfolio mix and loss rates:

Forward-Looking Statements

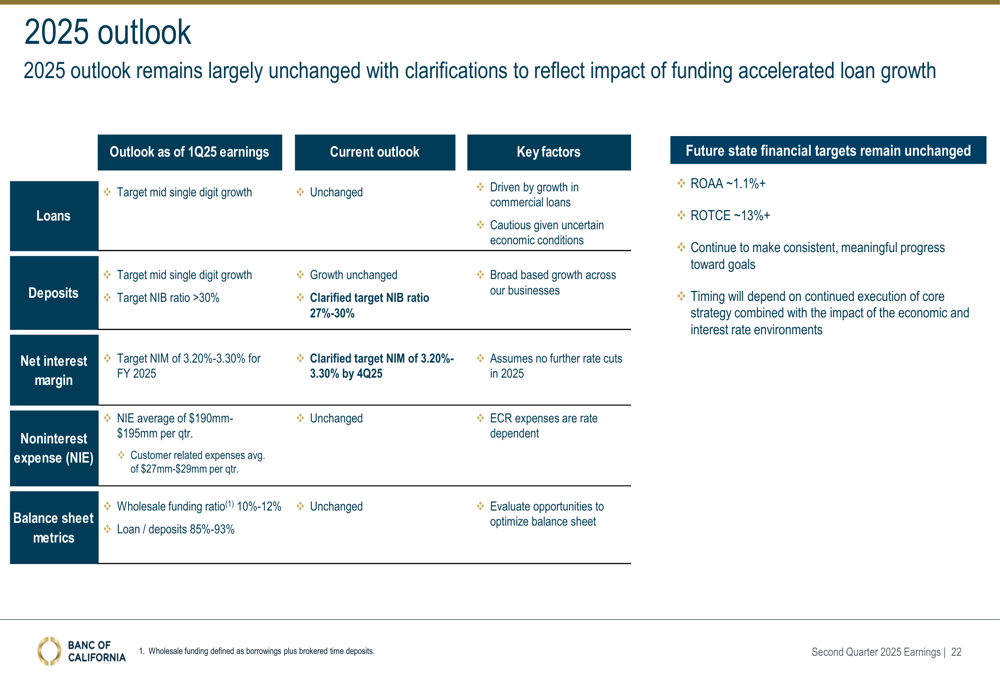

Looking ahead, Banc of California maintained most of its 2025 outlook targets while clarifying others. The bank continues to target mid-single-digit loan growth but noted caution given uncertain economic conditions. For deposits, it clarified its target for non-interest-bearing deposits to 27-30% of total deposits.

The bank expects its net interest margin to reach 3.20-3.30% by Q4 2025, assuming no further rate cuts this year. Longer-term financial targets remain unchanged, with goals of achieving a return on average assets of approximately 1.1% or higher and a return on tangible common equity of 13% or higher.

The bank’s commercial real estate portfolio, which has been an area of focus for investors in the regional banking sector, remains well-diversified across multiple industries with low weighted-average loan-to-value ratios and strong debt service coverage:

Management emphasized that the timing of achieving its long-term financial targets will depend on continued execution of core strategy combined with the impact of the economic and interest rate environments. The bank’s approach appears to balance growth initiatives with prudent risk management in an uncertain economic climate.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.