AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

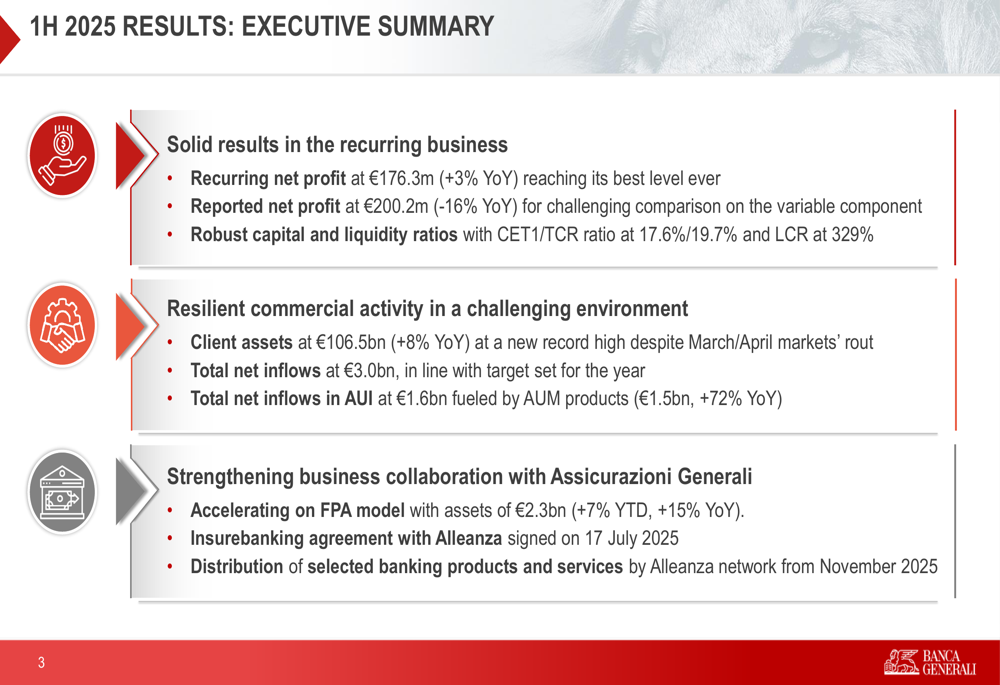

Banca Generali (BIT:BGN) released its first half 2025 financial results on July 29, showing resilience in its core business despite headwinds in variable fee income. The stock traded up 0.68% following the presentation, reflecting investor confidence in the company’s underlying performance.

The Italian wealth manager reported a 16% year-over-year decline in reported net profit to €200.2 million, primarily due to lower variable components. However, recurring net profit increased by 3% to €176.3 million, highlighting the stability of the company’s core business amid challenging market conditions.

Executive Summary

Banca Generali’s first half results demonstrated solid performance in recurring business segments while facing pressure on variable fee income. The company achieved robust commercial activity with total client assets reaching €106.5 billion, up 8% year-over-year, and total net inflows of €3.0 billion.

As shown in the following executive summary from the company’s presentation, Banca Generali maintained strong capital and liquidity positions while advancing its strategic collaboration with Assicurazioni Generali:

The company’s recurring net profit growth of 3% year-over-year demonstrates the resilience of its core business model, even as the reported net profit declined 16% due to a 66% drop in variable net profit components.

Quarterly Performance Highlights

Banca Generali’s quarterly results reveal a tale of two quarters, with a stronger Q1 followed by a more challenging Q2. Net profit decreased from €110.3 million in Q1 to €89.9 million in Q2, while recurring net profit remained more stable, increasing slightly from €87.0 million to €89.4 million.

The following chart illustrates the evolution of the company’s net profit components:

Net financial income showed positive momentum, reaching €177.0 million for the first half, a 6% increase year-over-year. This growth was supported by higher total deposits and contribution from the extended perimeter, including the integration of Intermonte.

Total (EPA:TTEF) gross fees decreased by 3% year-over-year to €592.7 million, with recurring fees accounting for 93% of the total (compared to 85% in 1H 2024). The decline was primarily driven by a 55% drop in variable fees to €42.5 million, reflecting challenging financial market conditions compared to the previous year.

Detailed Financial Analysis

Banca Generali’s investment fees reached €473.4 million in the first half, up 7% year-over-year despite the sharp financial markets correction in March/April 2025. Management fees increased by 7% to €447 million, in line with average asset expansion.

The company maintained a stable total payout ratio of 53.1%, broadly in line with the previous year and long-term guidance. Fee expenses on net interest income decreased by 32% year-over-year to €4.7 million, reflecting the trend in interest rates.

Operating costs increased to €164.4 million, with core operating costs rising 8.4% year-over-year to €133.8 million. This increase included higher personnel and IT expenditures associated with the insurebanking initiative and AI integration project.

The following summary table provides a comprehensive overview of Banca Generali’s financial performance for the first half of 2025:

Strategic Initiatives

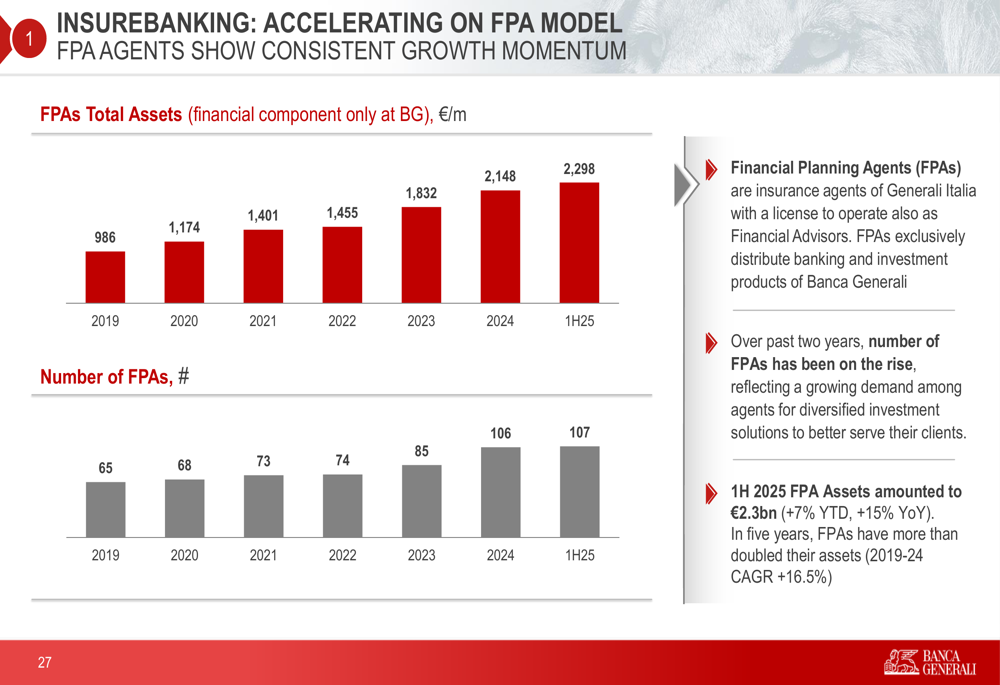

A key focus of Banca Generali’s presentation was its strategic "insurebanking" partnership with Generali Italia. This initiative aims to leverage synergies between banking and insurance services, targeting a significant untapped market potential in Italy.

The following slide illustrates the market opportunity that Banca Generali is pursuing with its insurebanking strategy:

The partnership, formalized with an agreement signed on July 17, 2025, includes three collaboration models: accelerating the Financial Planning Agents (FPA) model, direct insurebanking through Alleanza Assicurazioni, and FA/Agent collaboration.

The FPA model has shown strong growth, with assets increasing to €2.3 billion (+7% YTD, +15% YoY) and the number of agents growing steadily. The direct insurebanking agreement with Alleanza will enable the distribution of selected banking products and services through Alleanza’s network starting from November 2025.

Forward-Looking Statements

Despite current market challenges, Banca Generali’s management confirmed its targets for 2025, including net inflows of €6.0 billion and an average net interest margin of 200 basis points. The company expects management fee margins to range between 140-142 basis points in the second half of 2025.

The Board of Directors has approved the 2026-2028 Strategic Plan on a stand-alone basis, although the company noted that some business opportunities are currently "on stand-by" due to the ongoing exchange tender offer from Mediobanca (OTC:MDIBY).

As shown in the closing remarks slide, Banca Generali remains committed to delivering long-term value through its core business and strategic initiatives:

The company’s capital position remains strong with a Total Capital Ratio of 19.7%, despite the impact from CRR3 introduction (-3.8 percentage points) and the first-time integration of Intermonte (-2.1 percentage points). Liquidity ratios also remain well above regulatory requirements, with a Liquidity Coverage Ratio of 329%.

Analyst Perspectives

Following the Q1 2025 results announced earlier this year, Banca Generali’s stock had seen positive momentum, with the price increasing by 1.42% after that announcement. The company’s market capitalization stood at approximately $7.3 billion, with impressive revenue growth of 24.45% over the twelve months prior to Q1 reporting.

The first half results confirm the trends observed in Q1, with strong recurring business performance offsetting weakness in variable fees. The strategic focus on insurebanking represents a significant growth opportunity, though execution risks remain, particularly in the context of the unresolved Mediobanca offer.

Investors will likely focus on the company’s ability to maintain its recurring profit growth while navigating market volatility and advancing its strategic initiatives. The confirmed 2025 targets provide a clear roadmap for the remainder of the year, though the broader market environment and the resolution of the Mediobanca offer will be key factors influencing the company’s performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.