S&P, Nasdaq edge higher with gold spike, FOMC minutes in focus

Introduction & Market Context

Banca Mediolanum (BIT:BMED) reported its H1 2025 results on July 31, showing resilient performance amid a challenging interest rate environment. The Italian financial services group saw its stock rise 1.11% to €15.32 following the presentation, continuing its strong performance that has seen the share price trade near its 52-week high of €15.55.

The H1 results build upon the momentum seen in Q1, when the bank reported a 10% year-over-year increase in net income. The company’s diversified business model has proven effective in navigating the current economic landscape, with strong growth in managed assets and commission income offsetting the expected decline in net interest income.

Executive Summary

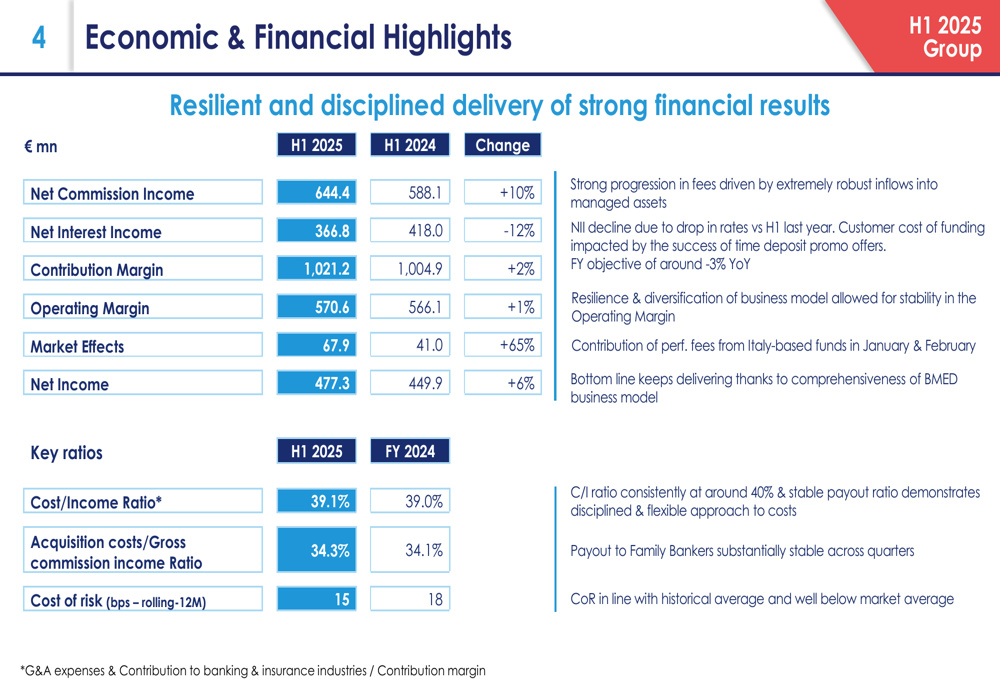

Banca Mediolanum delivered a solid financial performance in the first half of 2025, with net income rising 6% year-over-year to €477.3 million, compared to €449.9 million in H1 2024. This growth was primarily driven by a 10% increase in net commission income to €644.4 million and a 47% surge in net inflows into managed assets, reaching €4.54 billion.

As shown in the following economic and financial highlights chart, the bank’s contribution margin increased by 2% to €1,021.2 million, while operating margin grew 1% to €570.6 million, demonstrating the resilience of Banca Mediolanum’s business model despite a 12% decline in net interest income:

The bank’s customer base continued to expand, reaching nearly 2 million customers as of June 30, 2025, a 3% increase from December 2024. The Family Banker network also grew by 3% to 6,604 advisors, with particularly strong growth in Private Bankers and Wealth Advisors, which increased by 8% to 980.

Detailed Financial Analysis

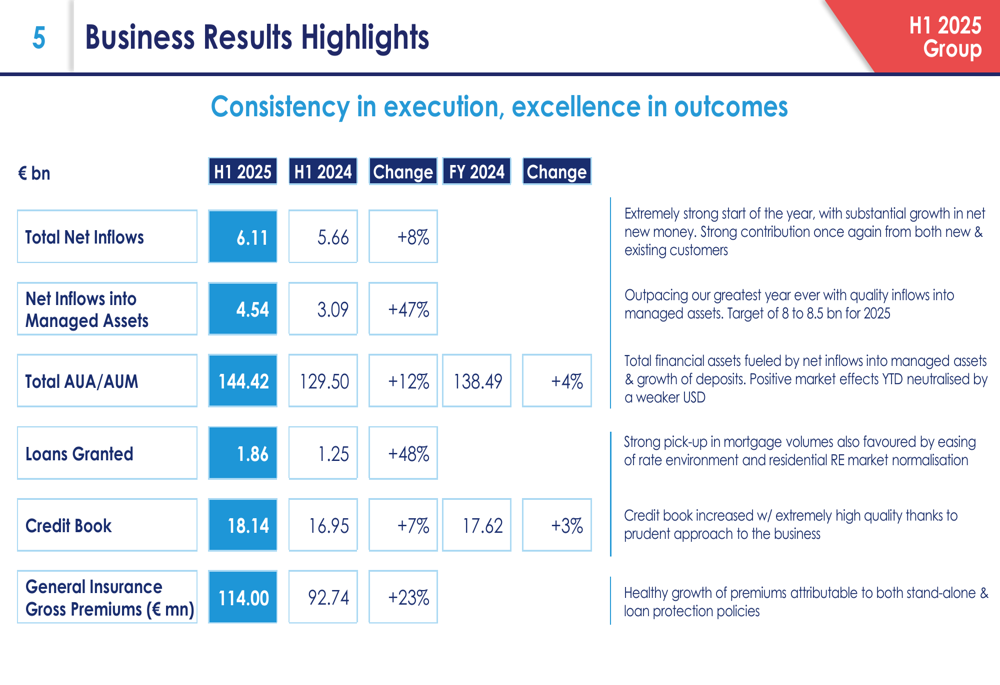

Banca Mediolanum’s business results showed strong momentum across key metrics in H1 2025. Total (EPA:TTEF) net inflows increased by 8% to €6.11 billion, while net inflows into managed assets surged by 47% to €4.54 billion. Total assets under administration and management grew by 12% year-over-year to €144.42 billion.

The following business results highlights chart illustrates the bank’s strong performance across various business lines:

The bank’s growth was supported by several resilience drivers, including a 3% increase in bank customers to nearly 2 million and a 3% growth in Family Bankers to 6,604. Notably, the number of Private Bankers and Wealth Advisors increased by 8% to 980, with their assets under management growing by 8% to €46.58 billion.

Despite the challenging interest rate environment, Banca Mediolanum maintained a stable cost/income ratio of 39.1%, compared to 39.0% at the end of 2024. The acquisition costs to gross commission income ratio remained virtually unchanged at 34.3%, indicating disciplined cost management.

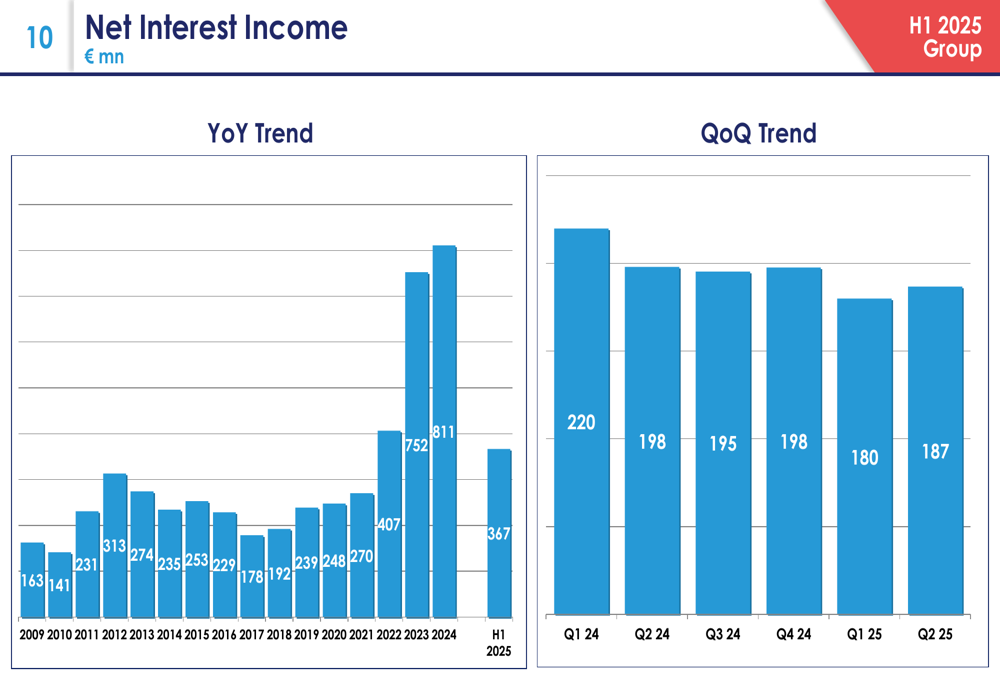

The bank’s net interest income showed a declining trend, as expected in the current rate environment. The following chart illustrates the net interest income trend both year-over-year and quarter-over-quarter:

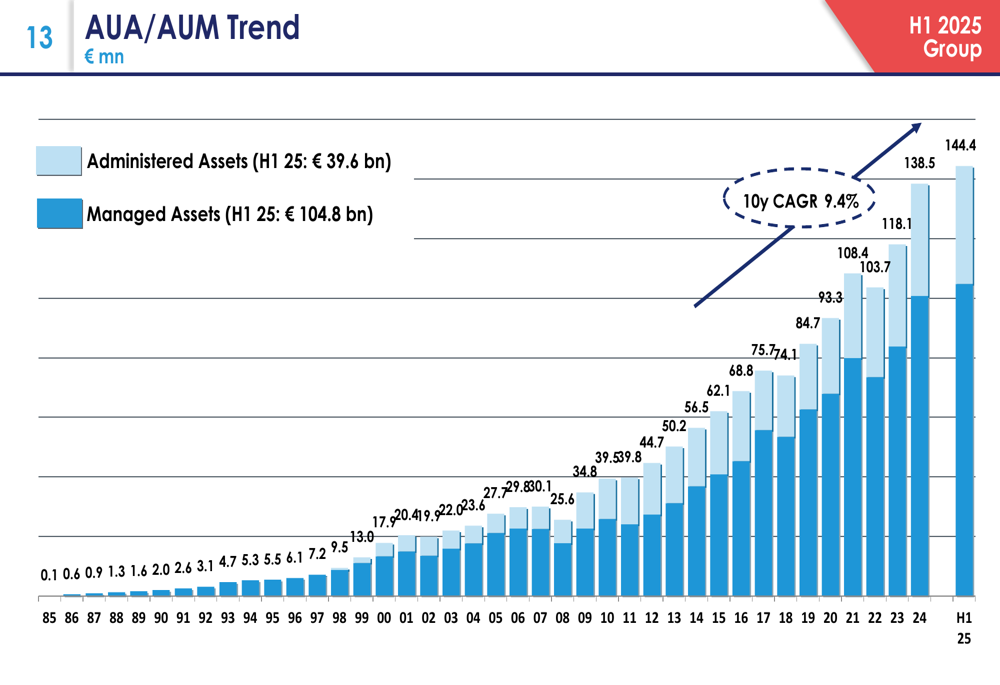

On the asset side, Banca Mediolanum’s total assets under administration and management have shown consistent growth over the years, with a 10-year CAGR of 9.4%. The following chart shows this impressive long-term growth trajectory:

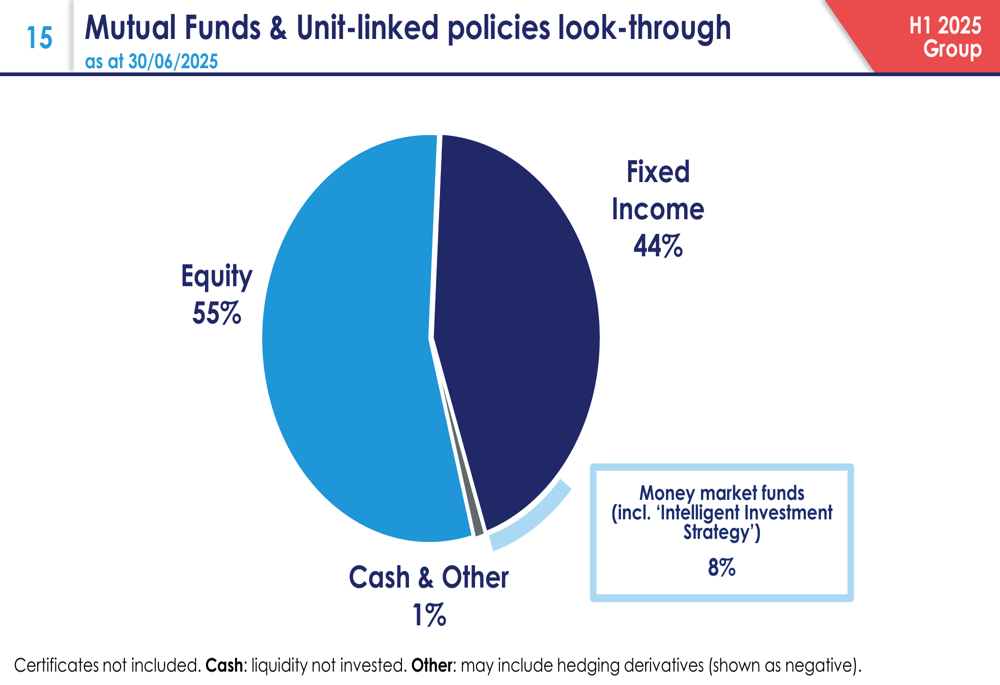

The bank’s asset allocation in mutual funds and unit-linked policies as of June 30, 2025, shows a balanced approach with 55% in equity, 44% in fixed income, and 1% in cash and other investments:

Strategic Initiatives & Growth Drivers

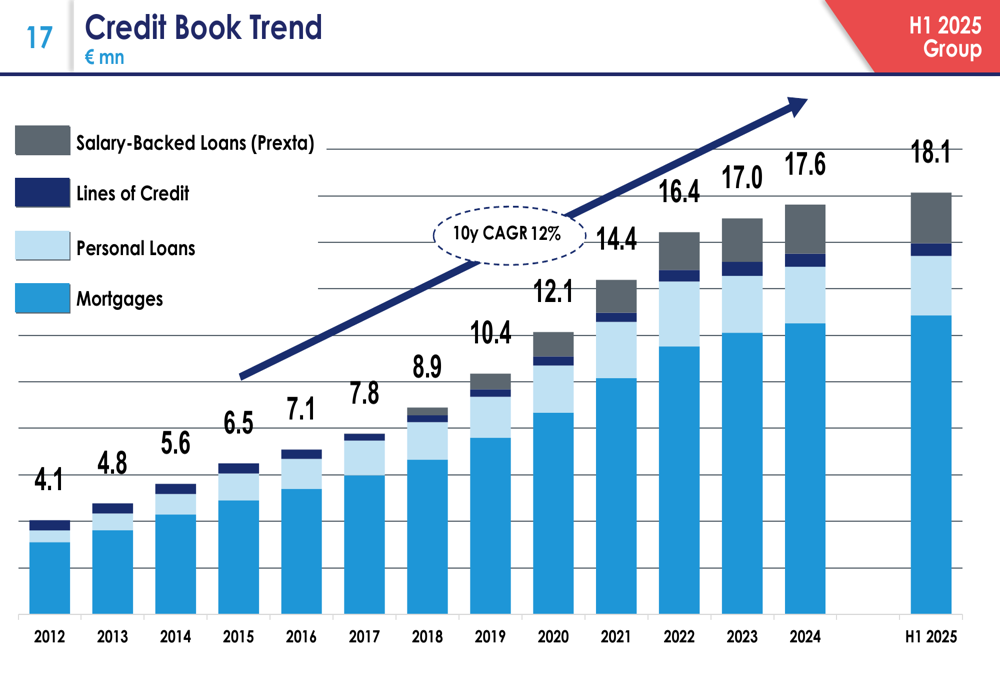

Banca Mediolanum’s credit business showed strong growth in H1 2025, with loans granted increasing by 48% year-over-year to €1.86 billion. This growth was particularly strong in mortgages, which increased by 48% to €1.01 billion, benefiting from the easing rate environment and normalization of the residential real estate market.

The bank’s credit book has shown consistent growth over the years, with a 10-year CAGR of 12%. The following chart illustrates this growth trend:

In Italy, Banca Mediolanum maintained its leading position among financial advisor networks, ranking first by net inflows into managed assets and advisory fees with €3.92 billion in H1 2025, according to Assoreti data.

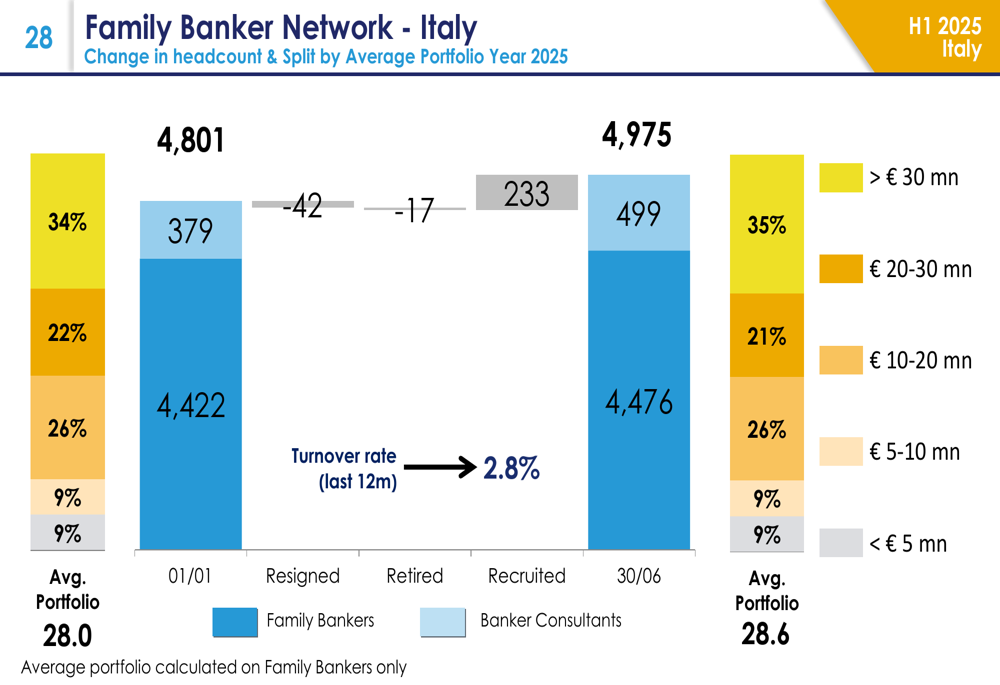

The bank’s Family Banker network in Italy continued to expand, reaching 4,975 advisors as of June 2025, up from 4,801 at the end of 2024. The network maintained a low turnover rate of 2.8%, indicating high advisor satisfaction and stability.

As shown in the following chart, the distribution of Family Bankers by portfolio size demonstrates the network’s strength and maturity:

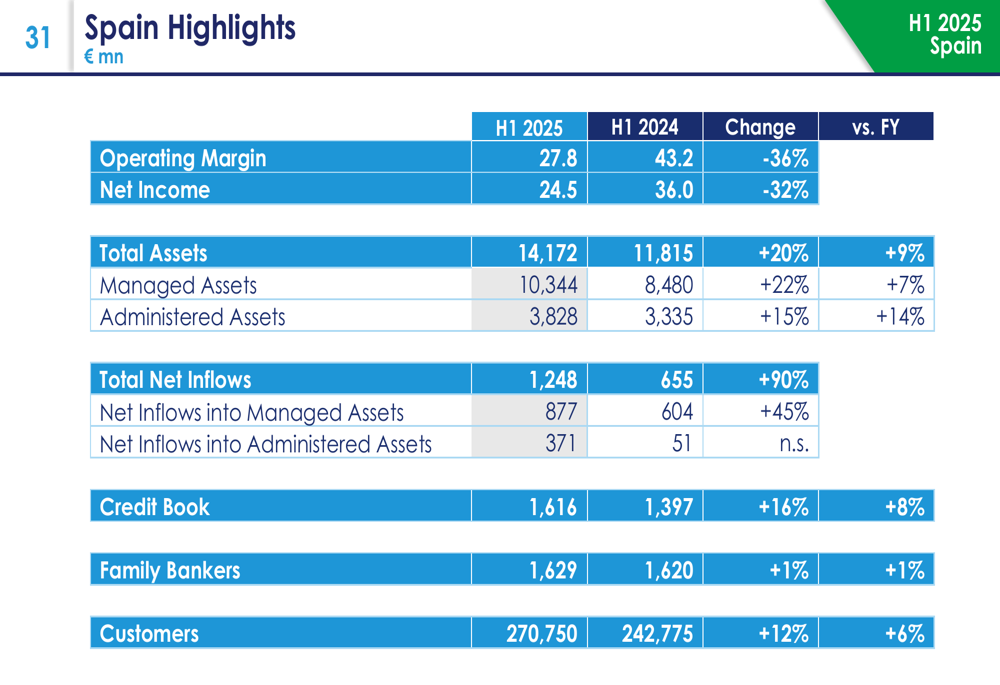

In Spain, Banca Mediolanum achieved impressive growth, with total net inflows increasing by 90% year-over-year to €1.25 billion. The Spanish operations now serve over 270,750 customers, a 12% increase from H1 2024, and manage €14.17 billion in total assets, up 20% year-over-year.

Capital Position & Balance Sheet Strength

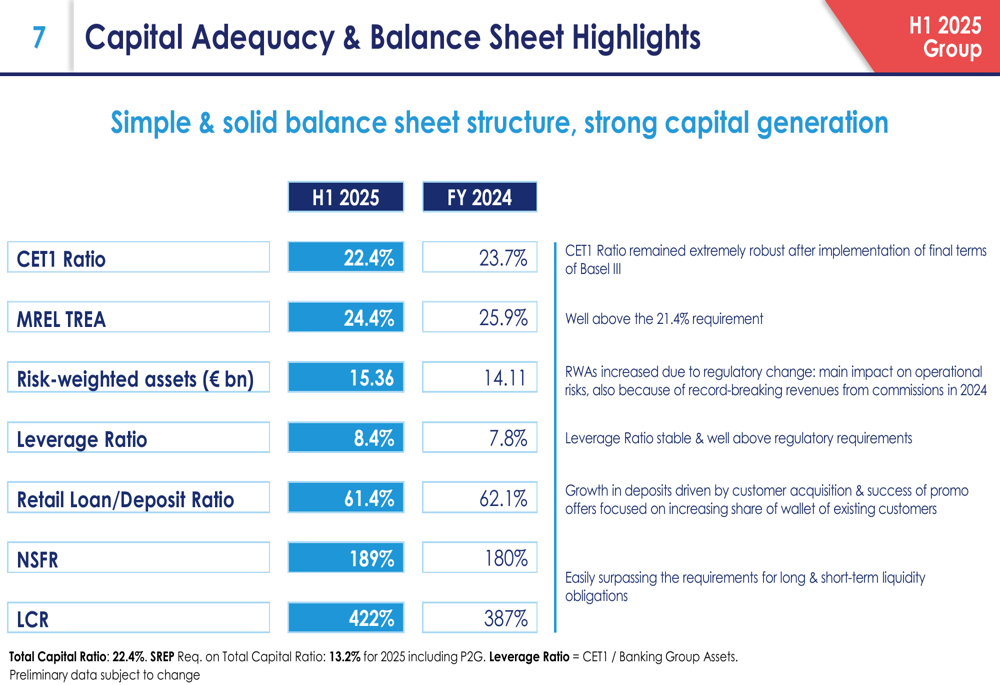

Banca Mediolanum maintained a strong capital position, with a CET1 ratio of 22.4% as of June 30, 2025, well above regulatory requirements despite a slight decrease from 23.7% at the end of 2024. The bank’s leverage ratio improved to 8.4% from 7.8% at the end of 2024.

The following capital adequacy and balance sheet highlights demonstrate the bank’s solid financial foundation:

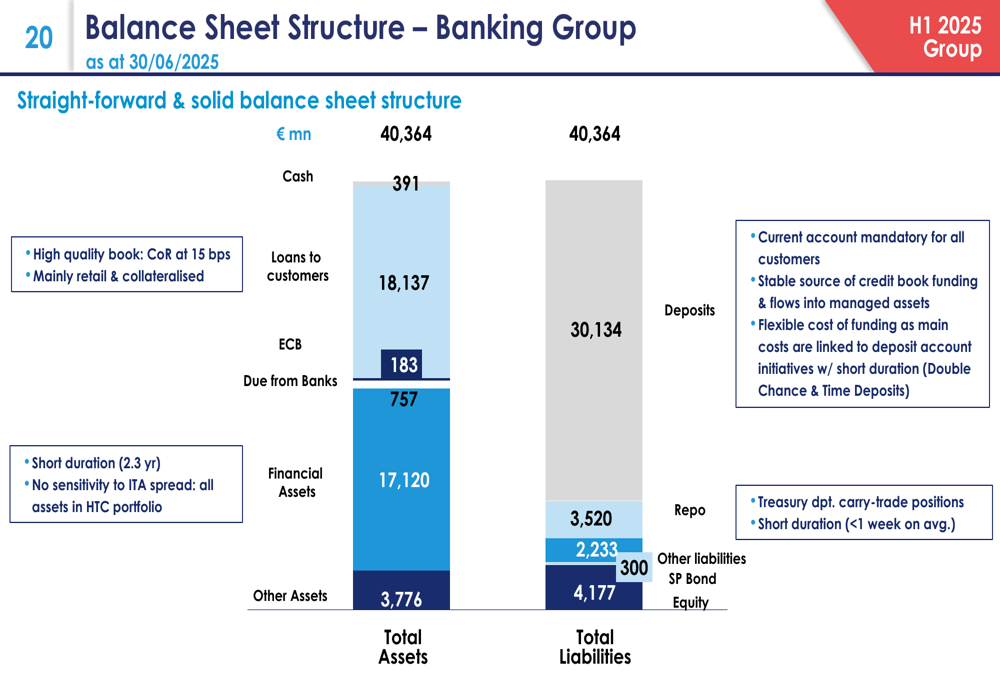

The bank’s balance sheet structure remains simple and solid, with total assets of €40.36 billion as of June 30, 2025. Customer loans represent 45% of total assets, while financial assets account for 42%. On the liability side, customer deposits make up 75% of total liabilities, providing a stable funding base.

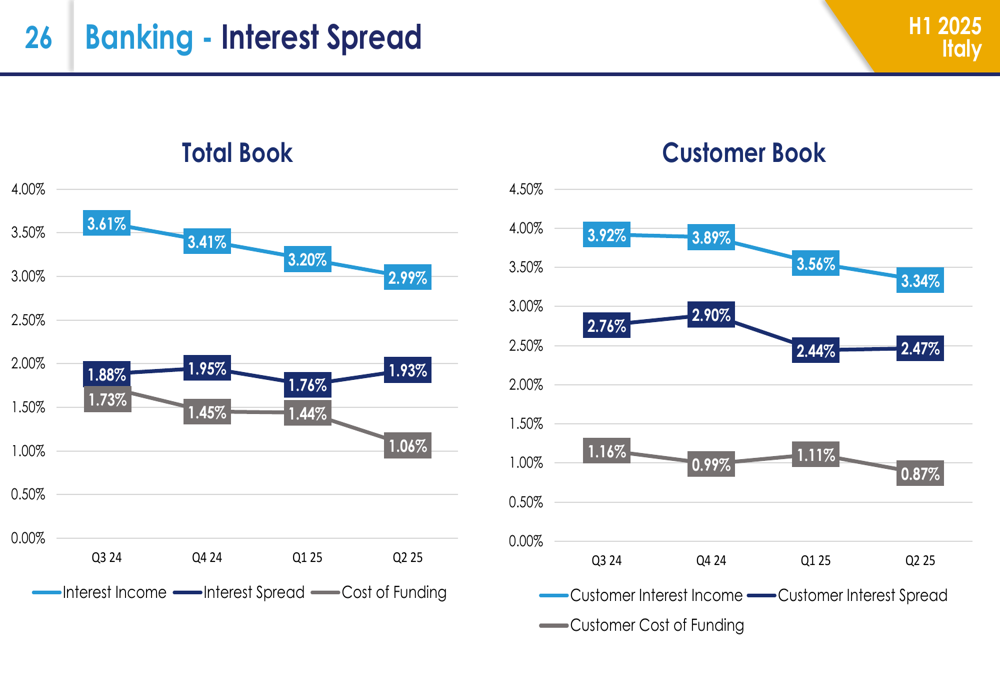

The bank’s interest spread in Italy has stabilized in recent quarters, as shown in the following chart, which illustrates the trends in interest income, interest spread, and funding costs:

Forward-Looking Statements

Looking ahead, Banca Mediolanum expects net inflows into managed assets to reach between €8 billion and €8.5 billion for the full year 2025, building on the strong performance in the first half. The bank anticipates that its contribution margin for the full year will be around 3% lower than in 2024, primarily due to the expected continued decline in net interest income.

The bank remains focused on maintaining its cost/income ratio at around 40% and keeping its cost of risk below 20 basis points. The growth of the Private Banker and Wealth Advisor segments will continue to be a strategic priority, as will the expansion in the Spanish market.

During the Q1 earnings call, CEO Massimo Doris emphasized the importance of maintaining close customer relationships during challenging times, stating, "These are times when staying in close contact with customers and staying true to our strategic direction really makes a difference." The H1 results demonstrate that this approach continues to yield positive results for Banca Mediolanum.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.