S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Banca Mediolanum (BIT:BMED) reported strong first-quarter results on May 8, 2025, with net profit rising 10% year-over-year despite headwinds in net interest income. The Italian financial services group’s shares closed at €13.75, up 2.76% on the day of the presentation, reflecting positive investor reception to the results. The stock is currently trading near its 52-week high of €15.51, having recovered substantially from its 52-week low of €9.3.

Quarterly Performance Highlights

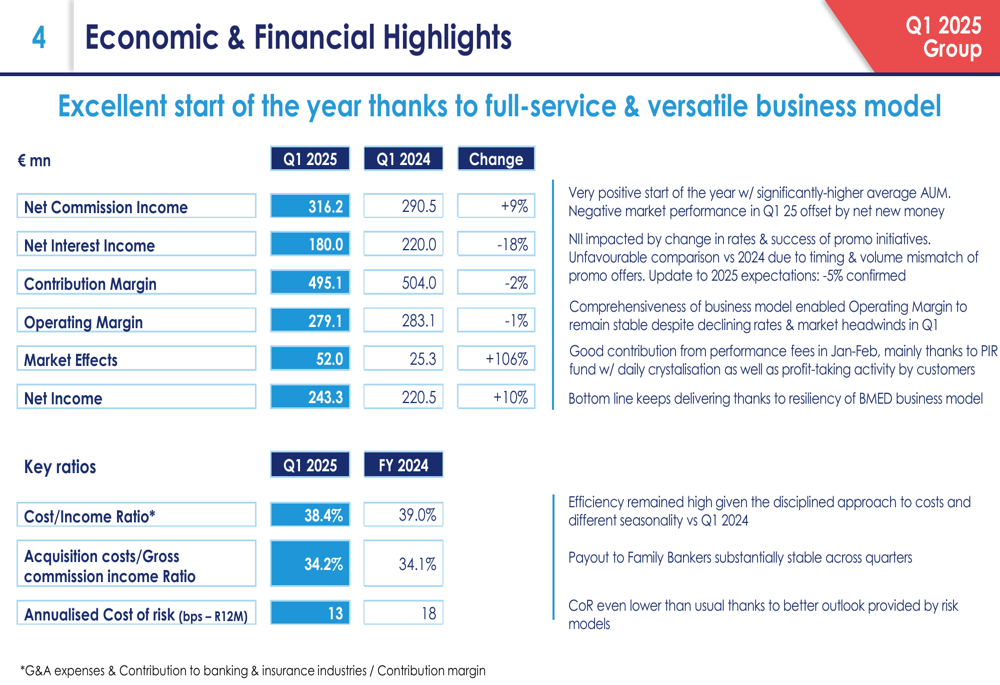

Banca Mediolanum delivered what it described as an "excellent start of the year" in Q1 2025, with net income reaching €243.3 million, a 10% increase from €220.5 million in the same period last year. This growth came despite an 18% decline in net interest income, which was more than offset by strong performance in commission income and market effects.

As shown in the following financial highlights table, net commission income grew 9% to €316.2 million, while market effects more than doubled to €52 million:

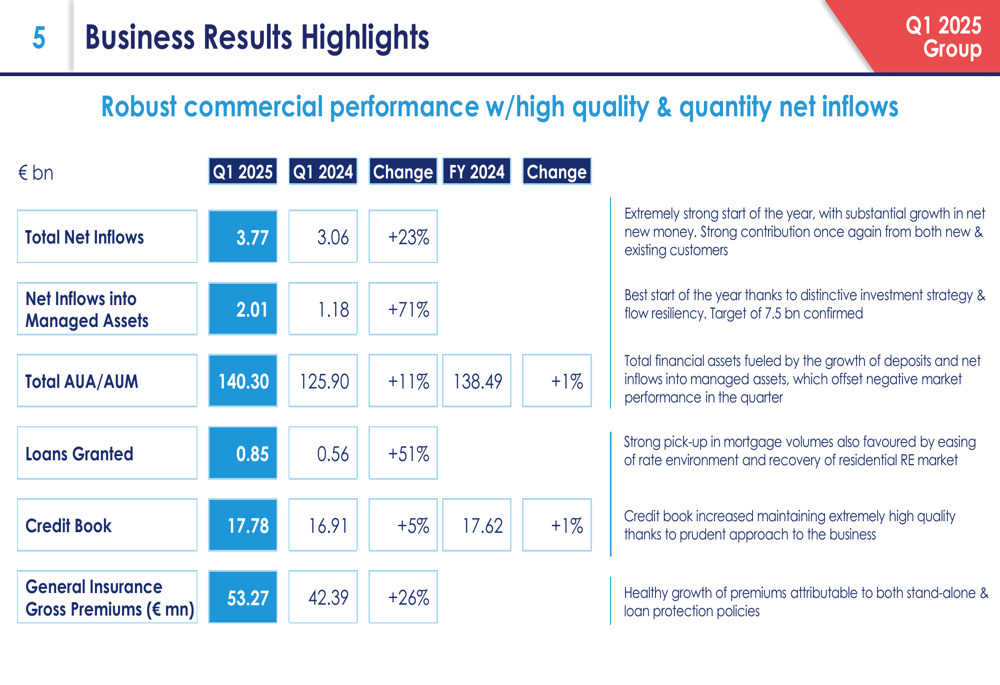

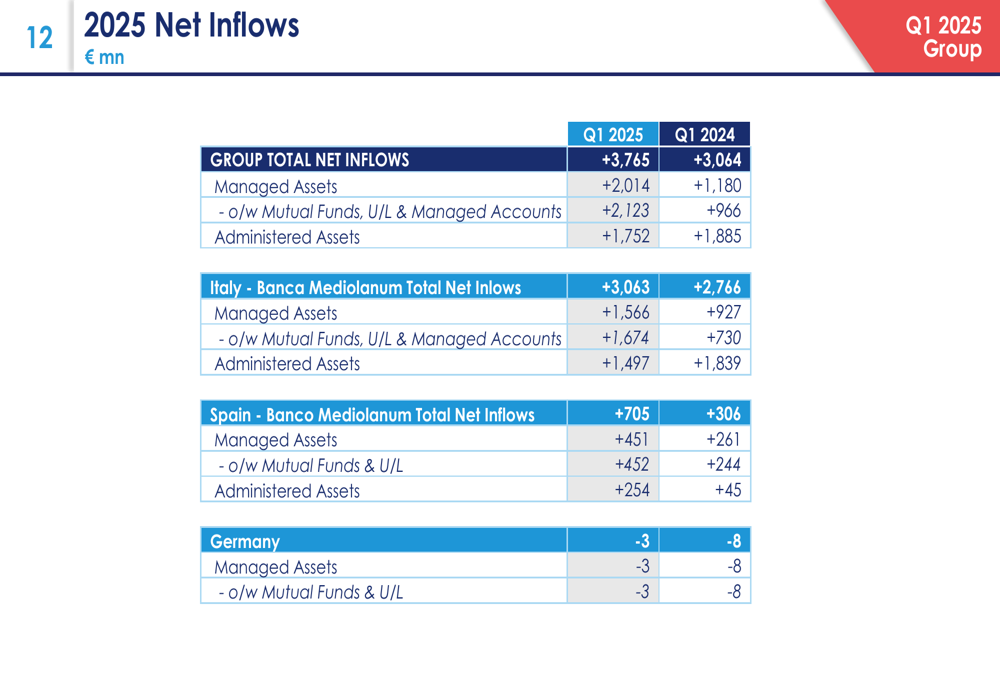

The bank’s business performance was particularly strong in terms of asset gathering, with total net inflows increasing 23% year-over-year to €3.77 billion. Most notably, net inflows into managed assets surged 71% to €2.01 billion, demonstrating the bank’s success in shifting customer assets to higher-margin products.

The following business results highlight the robust commercial performance across various metrics:

Detailed Financial Analysis

The bank’s income statement reveals how Banca Mediolanum has successfully navigated the challenging interest rate environment by growing its fee-based business. Gross commission income increased 12% year-over-year to €546.1 million, helping to offset the 18% decline in net interest income to €180 million.

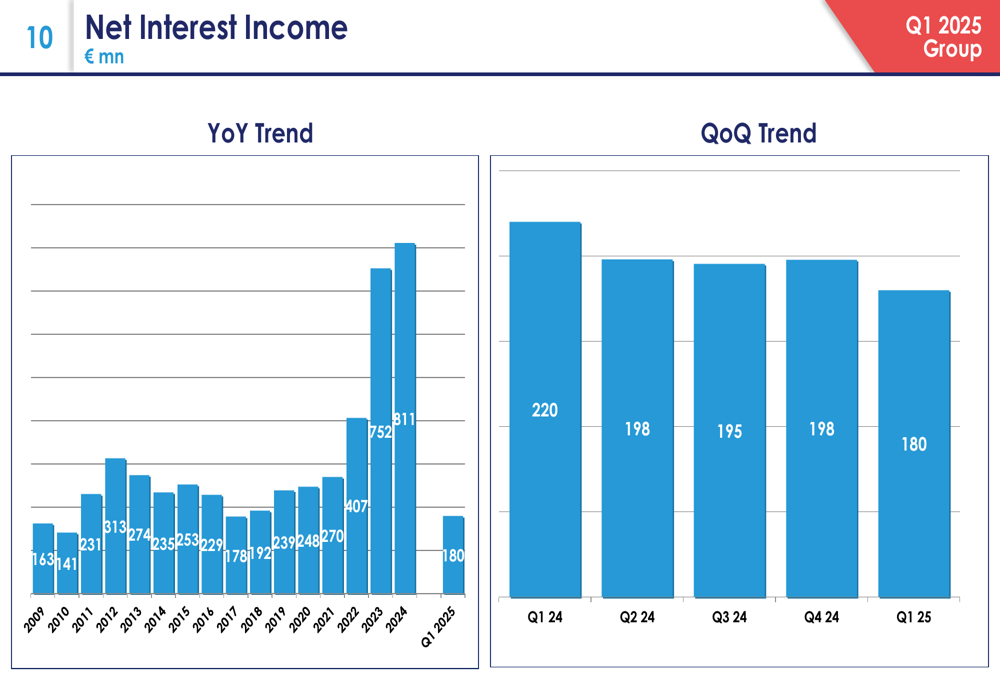

The decline in net interest income follows a pattern seen over recent quarters, as illustrated in the following chart showing both long-term and recent quarterly trends:

Despite higher acquisition costs, which rose 18% to €186.9 million, the bank maintained tight control over overall expenses. The cost/income ratio improved slightly to 38.4% in Q1 2025 from 39.0% at the end of 2024, reflecting the bank’s operational efficiency.

Business Growth Drivers

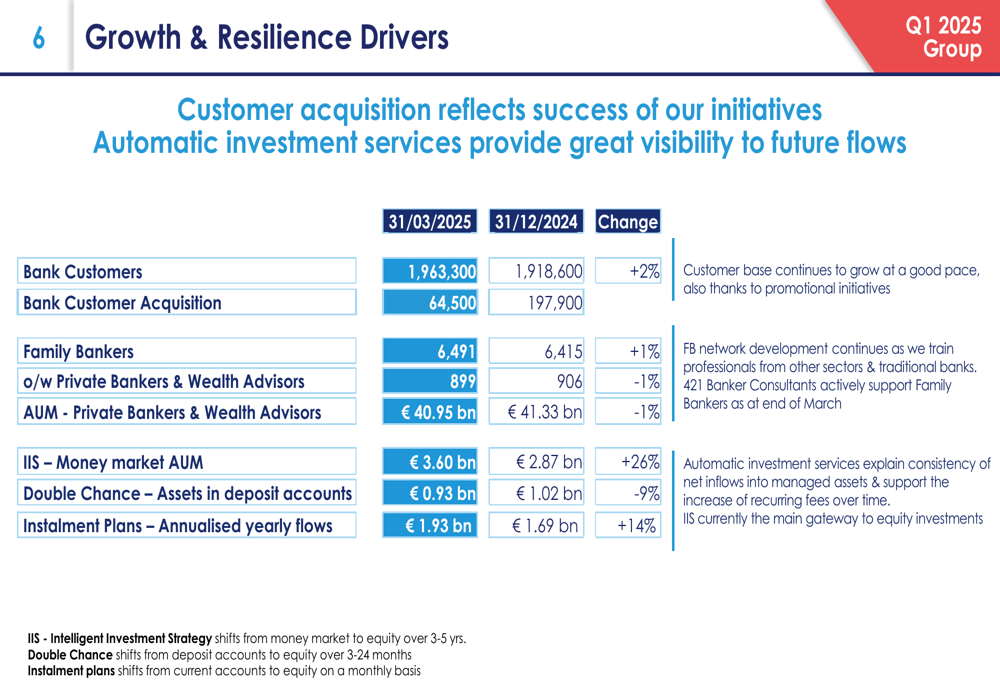

Customer acquisition remained strong in Q1 2025, with Banca Mediolanum adding 64,500 new bank customers, bringing the total to 1,963,300 (up 2% from December 2024). The company’s network of financial advisors, known as Family Bankers, grew to 6,491, a 1% increase from the end of 2024.

The bank’s automatic investment services continued to show strong momentum, with money market assets under management increasing 26% to €3.60 billion, while annualized yearly flows through installment plans grew 14% to €1.93 billion.

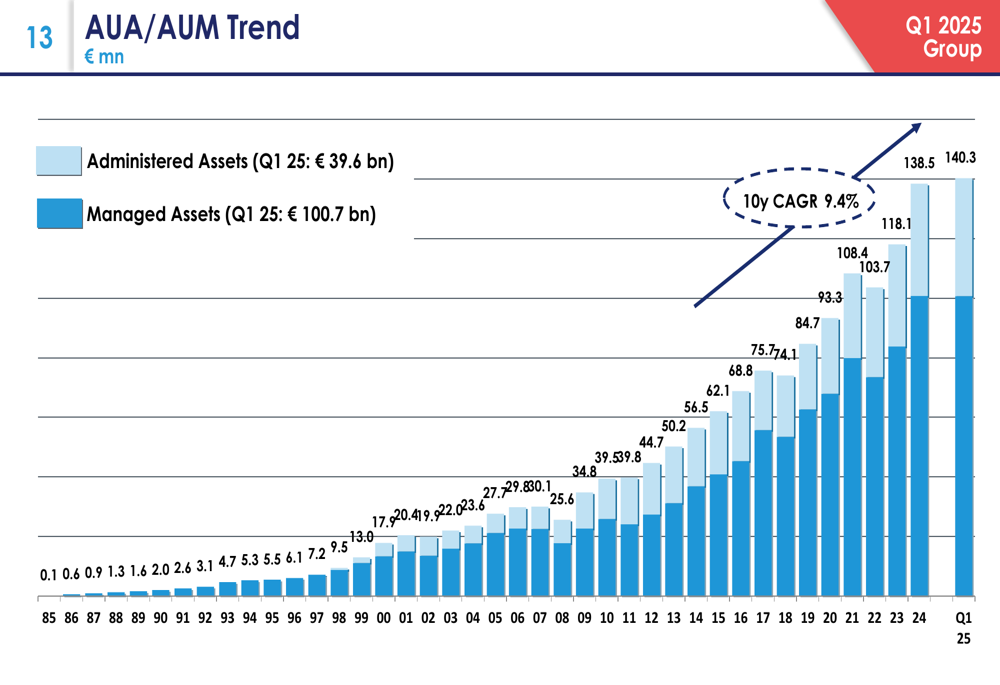

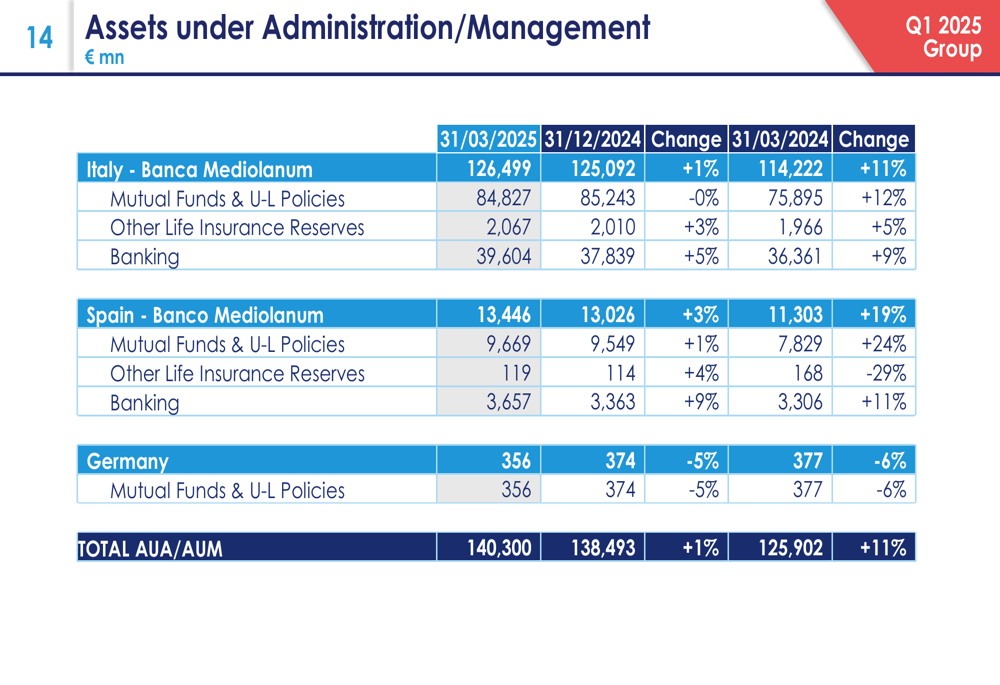

The growth in assets under administration and management has been consistent over time, with a 10-year compound annual growth rate (CAGR) of 9.4%. Total (EPA:TTEF) AUA/AUM reached €140.3 billion at the end of Q1 2025, representing an 11% increase year-over-year and a 1% increase from the end of 2024.

The following chart illustrates this long-term growth trend:

Regional Performance Analysis

Banca Mediolanum’s growth was broad-based across its key markets, with particularly strong performance in Spain. The Spanish operation, Banco Mediolanum, saw total net inflows more than double to €705 million in Q1 2025 compared to €306 million in Q1 2024, with managed assets inflows growing to €451 million.

The following breakdown shows net inflows by region and asset type:

In terms of total assets under administration and management, Italy remains the dominant market with €126.5 billion (up 11% year-over-year), while Spain showed stronger growth at 19% year-over-year, reaching €13.4 billion.

Capital Position and Balance Sheet

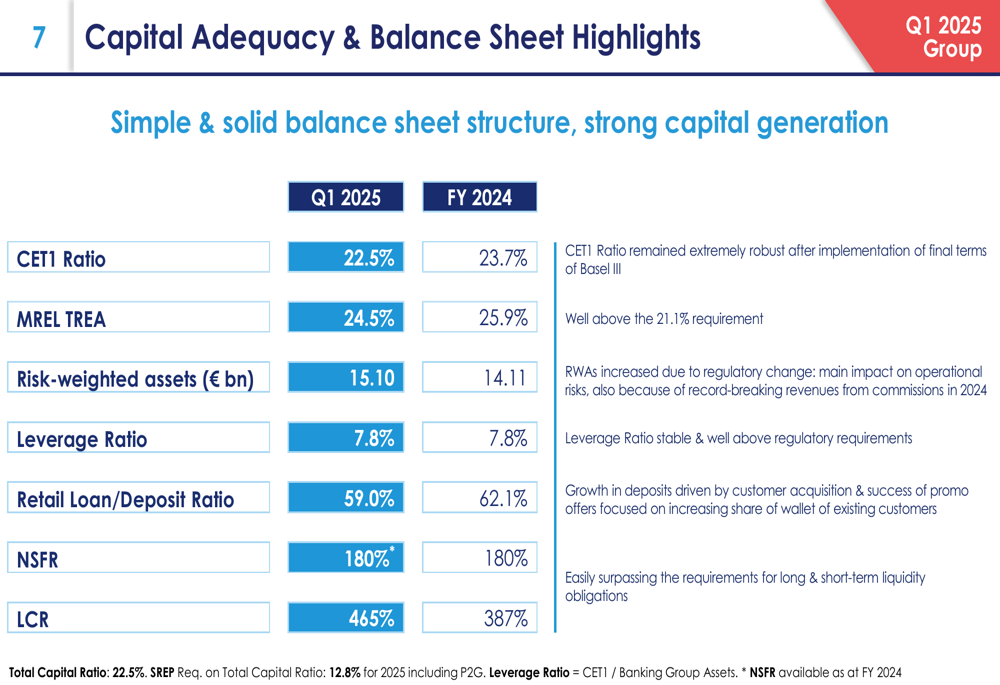

Banca Mediolanum maintained a strong capital position, with a CET1 ratio of 22.5% at the end of Q1 2025, well above regulatory requirements despite a slight decrease from 23.7% at the end of 2024. The bank’s liquidity position improved further, with the Liquidity Coverage Ratio (LCR) increasing to 465% from 387% at the end of 2024.

The following table details the bank’s capital adequacy and balance sheet metrics:

The retail loan-to-deposit ratio decreased to 59.0% from 62.1% at the end of 2024, indicating a conservative approach to lending despite a 5% year-over-year growth in the credit book to €17.78 billion. The bank’s cost of risk improved to 13 basis points from 18 basis points at the end of 2024.

Forward-Looking Statements

While the presentation did not include explicit guidance for the remainder of 2025, the strong start to the year positions Banca Mediolanum well to continue its growth trajectory. The bank’s diversified business model, with its mix of asset management, banking, and insurance services, provides resilience against fluctuations in interest rates.

The continued shift toward managed assets, which generate higher margins through commission income, should help offset the ongoing pressure on net interest income. The strong customer acquisition and growth in automatic investment services also provide visibility for future revenue streams.

Banca Mediolanum’s solid capital position and conservative balance sheet structure give it flexibility to pursue growth opportunities while maintaining financial stability in a potentially volatile market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.