Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

Banco BPM (BIT:BAMI) presented its first half 2025 results on August 5, revealing a strong financial performance with net income exceeding €1.2 billion, representing 62% of its full-year guidance. The Italian banking group’s shares have performed well in recent months, with the stock trading at €2.571 after a 26% year-to-date gain, according to recent market data.

The results demonstrate significant progress in the bank’s strategic transformation from a traditional lending-focused institution to a more diversified financial services provider, with the recently completed Anima acquisition playing a central role in this shift.

Executive Summary

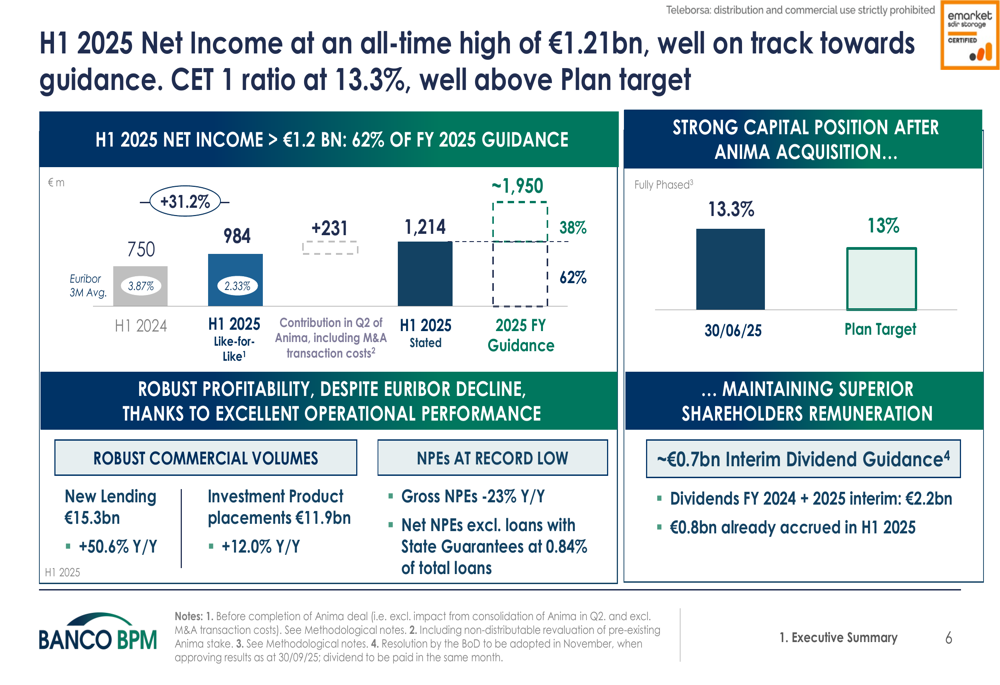

Banco BPM reported H1 2025 stated net income of €1.214 billion, a substantial 62% increase from €750 million in H1 2024. On a like-for-like basis (excluding Anima’s contribution), net income still grew impressively by 31.2% to €984 million.

The bank’s performance was driven by strong commercial volumes, with new lending up 50.6% year-over-year to €15.3 billion and investment product placements increasing 12.0% to €11.9 billion. Asset quality continued to improve, with gross non-performing exposures (NPEs) down 23% year-over-year.

As shown in the following chart of key performance metrics and guidance:

The bank has raised its full-year 2025 guidance to approximately €1.95 billion, representing a 38% increase from the H1 2025 stated results. This improved outlook reflects both organic growth and the successful integration of Anima, which is already contributing significantly to the group’s profitability.

Strategic Initiatives

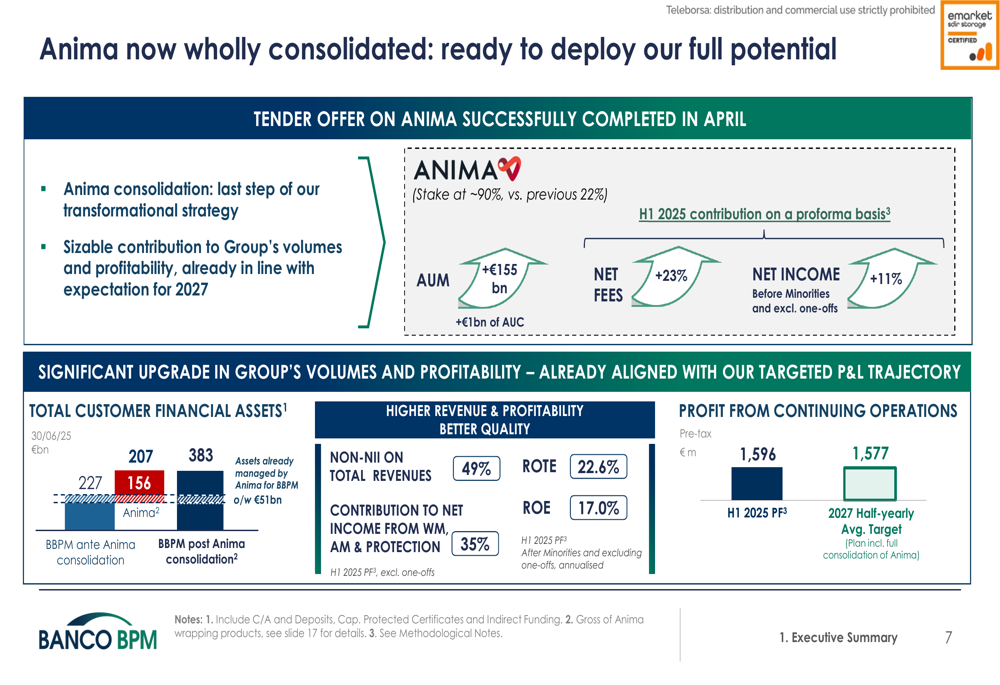

The successful completion of the tender offer for Anima in April 2025 represents a milestone in Banco BPM’s transformational strategy. The bank increased its stake from 22% to approximately 90%, consolidating Anima’s results starting from Q2 2025.

This acquisition has dramatically expanded the group’s asset management capabilities, as illustrated in the following slide:

The Anima consolidation has increased Banco BPM’s total customer financial assets from €207 billion to €383 billion and is already contributing to the group’s profitability, with a positive impact of 11% on net income before minorities and excluding one-offs.

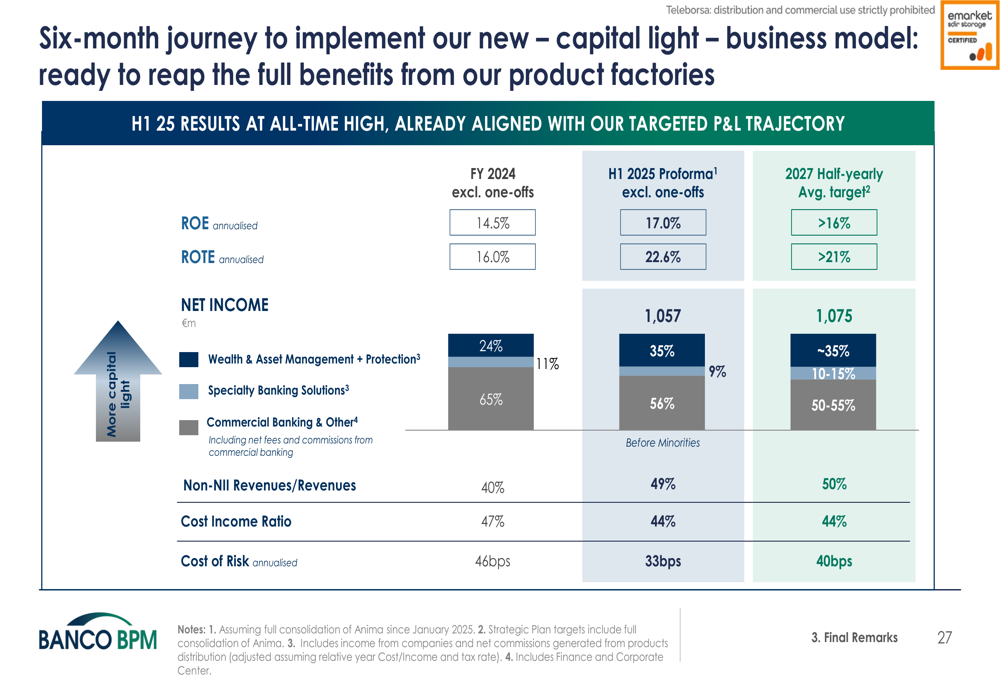

CEO Giuseppe’s strategic vision, as mentioned in the Q1 earnings call, is being realized: "We are transforming a bank which was two-thirds led by commercial activity to a bank which will be led 50% by commission coming from product factory." The H1 results confirm this transition, with non-interest income now representing 47% of total revenue, up from 38% a year earlier.

The bank’s transformational journey is progressing according to plan, with initiatives in life insurance, property and casualty insurance, and asset management all contributing to the shift toward a more capital-light business model:

Detailed Financial Analysis

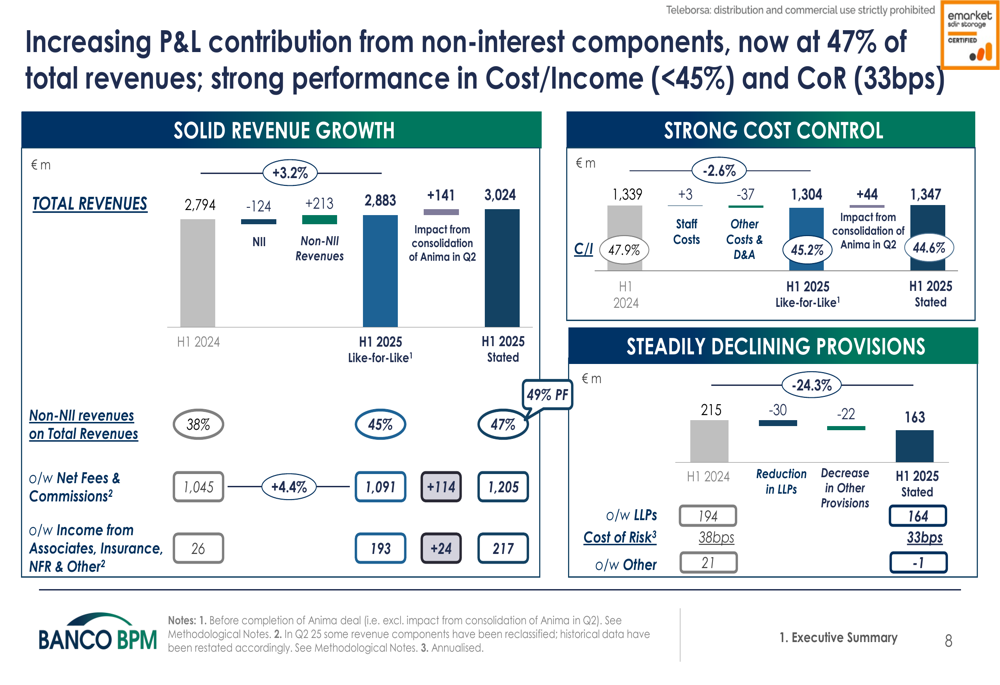

Banco BPM’s total revenue increased by 3.2% year-over-year on a like-for-like basis, reaching €2.883 billion, and further to €3.024 billion when including Anima’s contribution. This growth came despite a decline in net interest income, highlighting the success of the bank’s strategy to diversify revenue streams.

The following chart illustrates the changing composition of the bank’s revenue and its strong cost control:

Operating costs remained well-controlled, with the cost-to-income ratio improving from 47.9% to 44.6%. This efficiency improvement, combined with lower loan loss provisions (cost of risk decreased from 38bps to 33bps), has significantly boosted profitability.

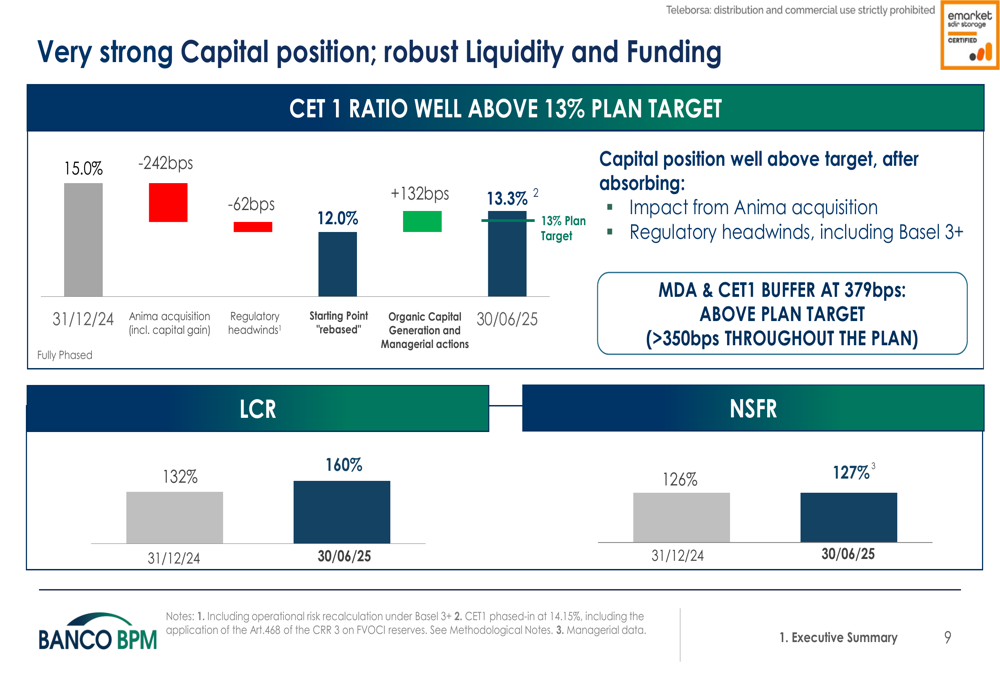

The bank’s capital position remains robust despite the impact of the Anima acquisition. The CET1 ratio stands at 13.3%, well above the 13% target, with the acquisition having a 242 basis point impact that was partially offset by 132 basis points of organic capital generation:

Liquidity metrics also remain strong, with the Liquidity Coverage Ratio (LCR) increasing from 132% to 160% and the Net Stable Funding Ratio (NSFR) improving slightly from 126% to 127%.

Forward-Looking Statements

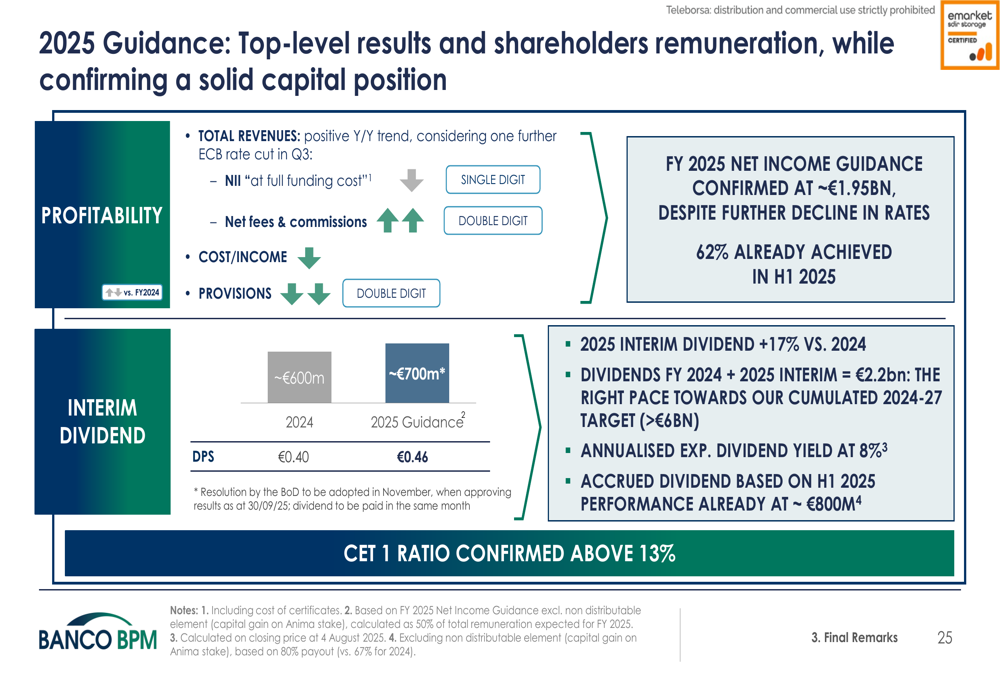

Banco BPM has confirmed its positive outlook for the remainder of 2025, with guidance pointing to continued revenue growth, improved cost efficiency, and lower provisions. The bank has also announced an attractive dividend policy, with the 2025 interim dividend expected to increase by 17% compared to 2024, representing an annualized yield of 8%.

As shown in the following guidance summary:

The bank has already accrued approximately €800 million in dividends based on H1 2025 performance, demonstrating its commitment to shareholder returns while maintaining a strong capital position.

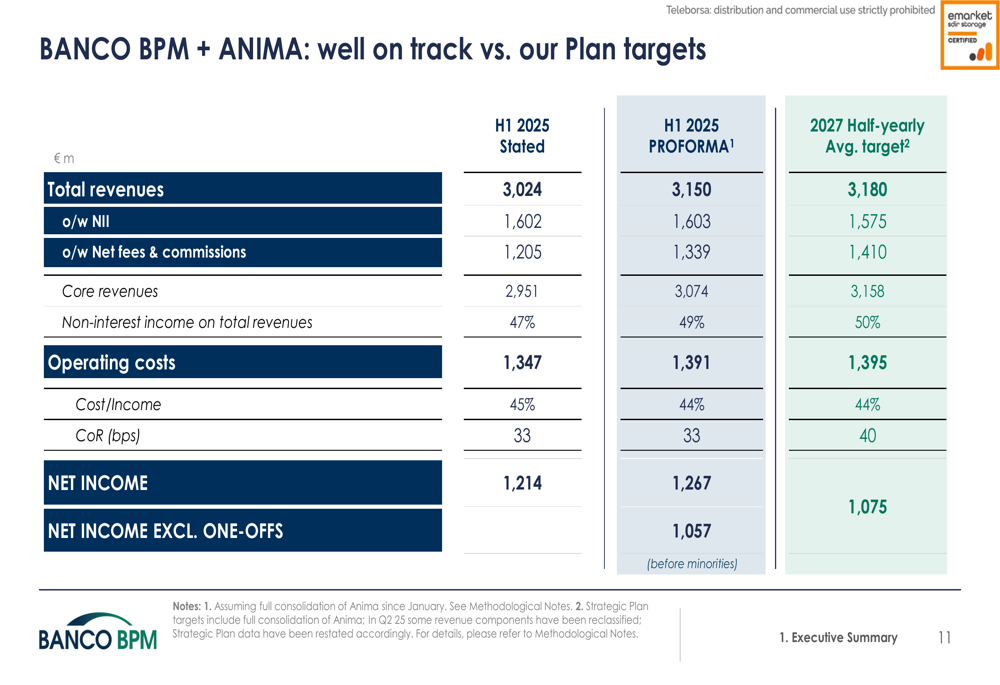

Looking further ahead, Banco BPM appears well on track to meet its 2027 targets, with many metrics already approaching the half-yearly average targets:

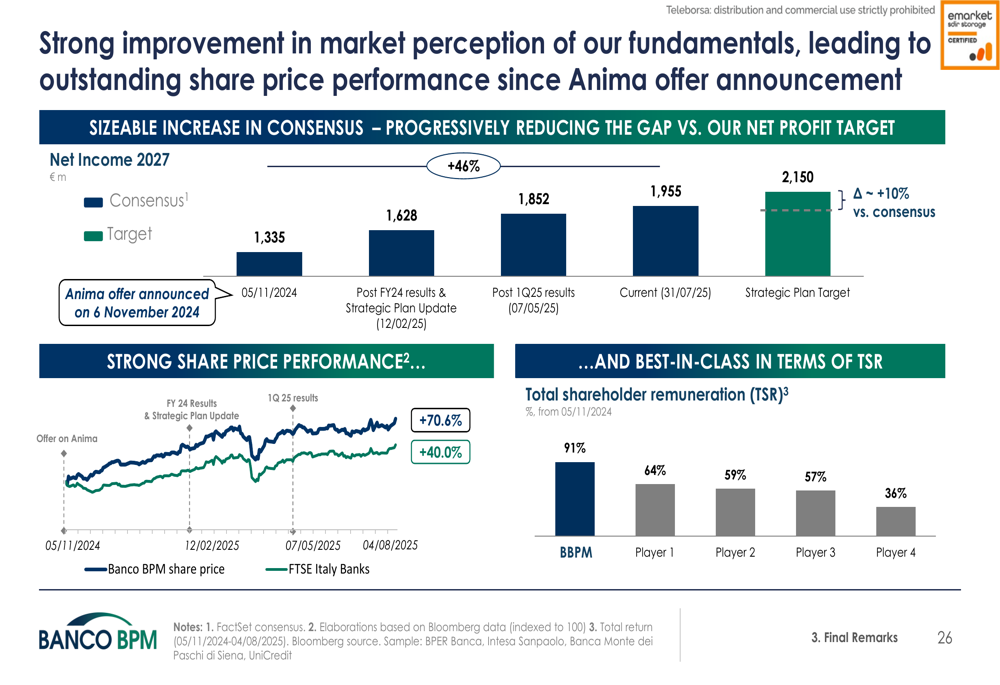

Market perception of the bank has improved significantly since the Anima acquisition announcement, with analyst consensus progressively reducing the gap versus the bank’s net profit target and the share price outperforming the market:

In conclusion, Banco BPM’s H1 2025 results demonstrate strong execution of its strategic transformation, with the Anima acquisition accelerating the shift toward a more diversified, fee-based business model. While challenges remain, including the potential impact of interest rate fluctuations and economic uncertainty in Italy and Europe, the bank appears well-positioned to continue its positive trajectory toward achieving its 2027 strategic objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.