Gold prices dip as hawkish Fed minutes weigh ahead of Jackson Hole

Introduction & Market Context

Banco BPM (BIT:BAMI) presented its first quarter 2025 results on May 7, showcasing record-breaking performance with net income surpassing the €500 million mark for the first time in the bank’s history. The Italian lender reported significant progress toward its strategic goals while completing the acquisition of asset manager Anima, a key strategic move to diversify its business model.

The strong quarterly performance comes amid Banco BPM’s continued support for the Italian economy, with growth in core customer loans and a focus on sustainable financing initiatives. The bank’s shares have performed exceptionally well over the past year, delivering nearly 95% returns to investors according to historical data.

Quarterly Performance Highlights

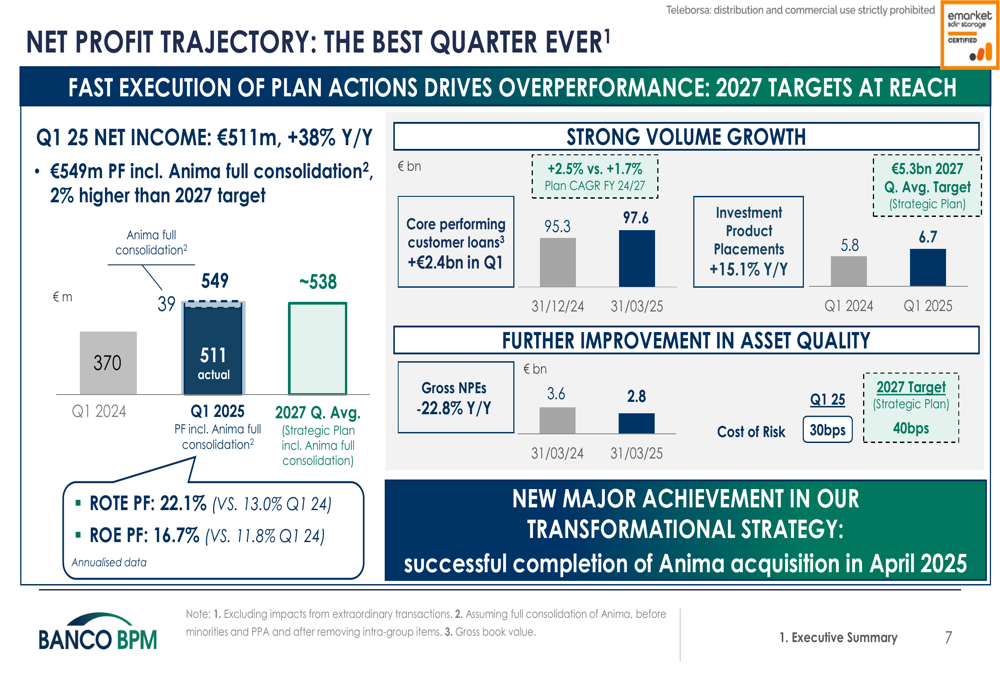

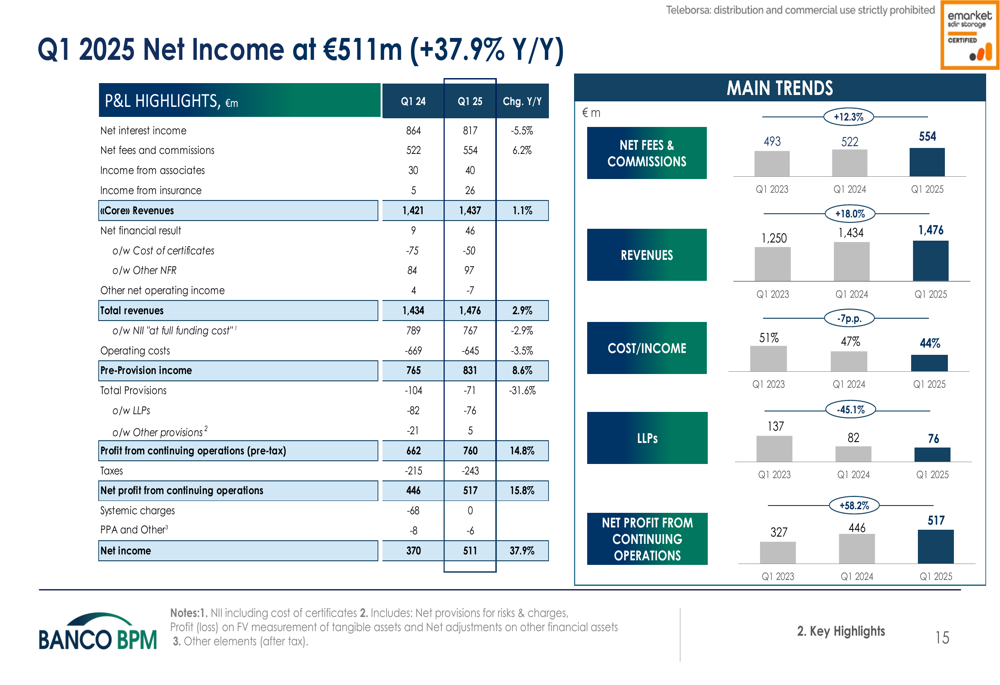

Banco BPM reported Q1 2025 net income of €511 million, representing a 38% year-over-year increase and marking the best quarterly result in the bank’s history. The performance was driven by strong commercial results, with core performing customer loans growing 2.5% quarter-over-quarter and investment product placements increasing 15.1% year-over-year.

As shown in the following chart highlighting the bank’s net profit trajectory:

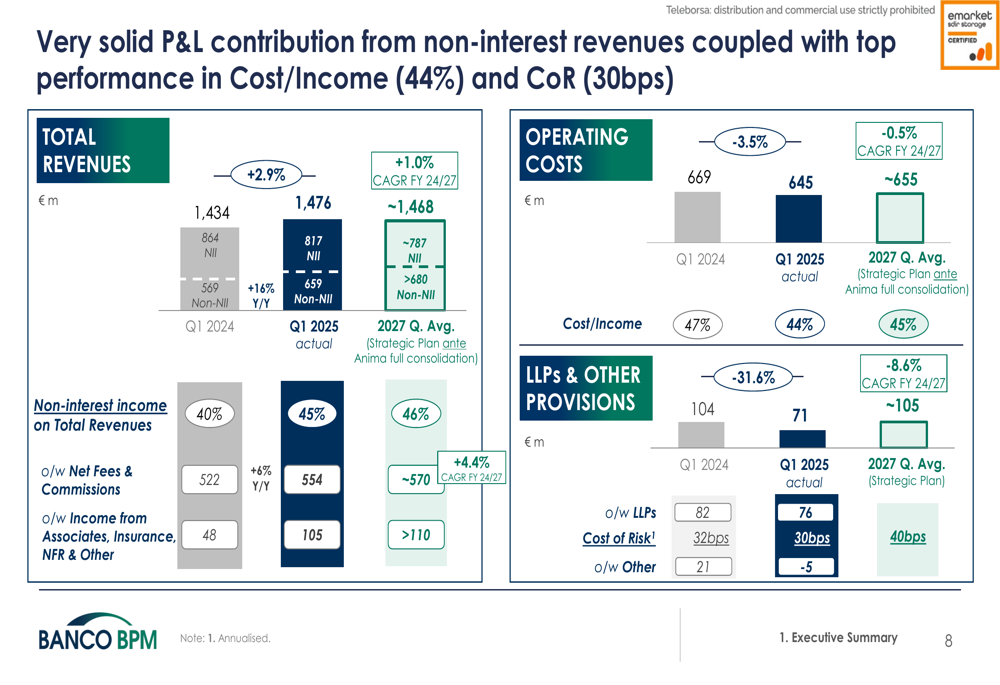

Total (EPA:TTEF) revenues reached €1,476 million, up 2.9% compared to the same period last year, while operating costs decreased by 3.5% to €645 million. This combination resulted in an impressive cost-to-income ratio of 44%, demonstrating the bank’s operational efficiency. Loan loss provisions and other provisions decreased significantly by 31.6% to €71 million, with the cost of risk at a low 30 basis points.

The following slide illustrates the solid P&L contribution and cost/income performance:

The bank’s profitability metrics were equally impressive, with return on equity (ROE) at 16.7% and return on tangible equity (ROTE) at 22.1% when including the full consolidation of Anima. Profit from continuing operations before tax reached €827 million in Q1 2025 on a pro-forma basis, already exceeding the €788 million quarterly target for 2027.

Strategic Initiatives

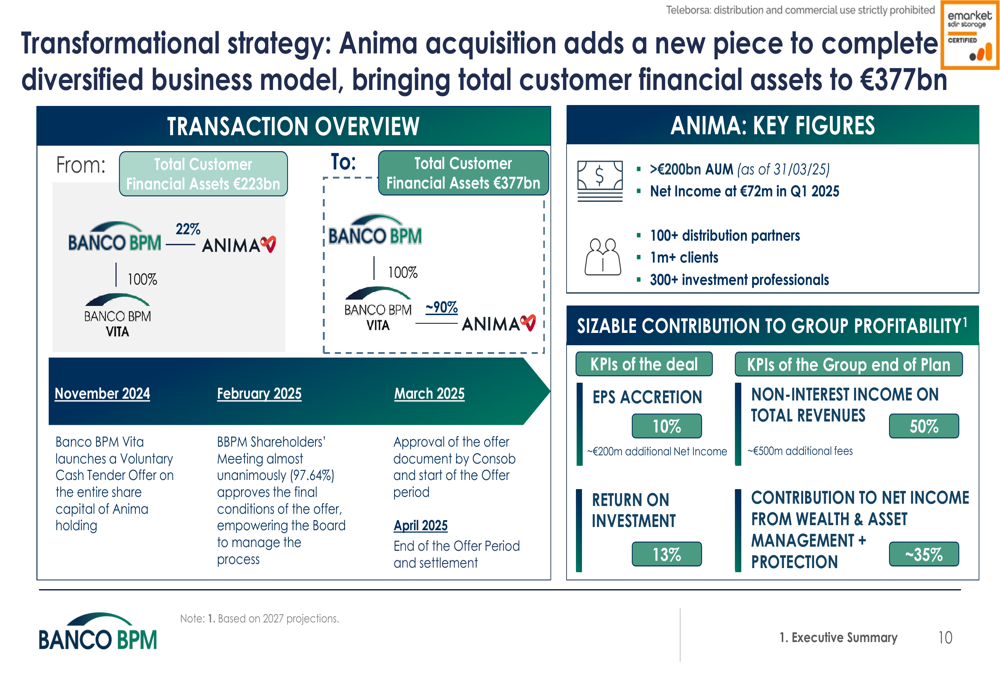

The most significant strategic development in the quarter was the successful completion of the Anima acquisition in April 2025. This acquisition represents a key milestone in Banco BPM’s strategy to diversify its business model and strengthen its asset management capabilities.

The following slide provides an overview of the Anima acquisition and its strategic importance:

With this acquisition, Banco BPM’s total customer financial assets increased to €377 billion. Anima brings significant scale to the group with over €200 billion in assets under management, more than 100 distribution partners, over 1 million clients, and 300+ investment professionals. The deal is expected to deliver 10% EPS accretion and a 13% return on investment.

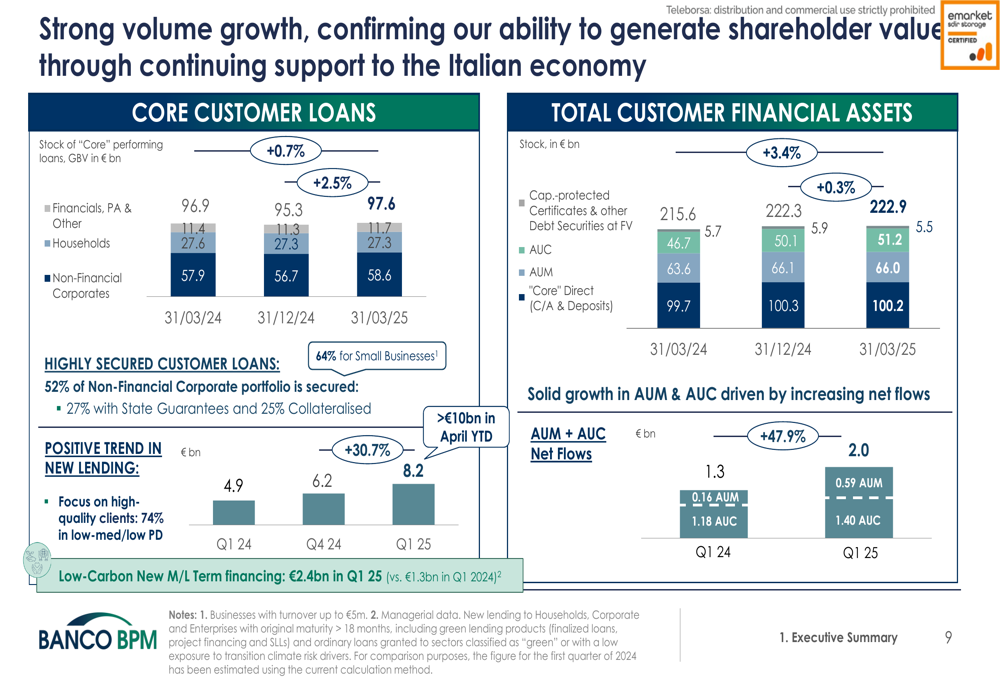

The bank also highlighted strong volume growth in its core business, supporting the Italian economy with increased lending activity. Low-carbon new medium/long-term financing reached €2.4 billion in Q1 2025, underscoring the bank’s commitment to sustainable finance.

As illustrated in this slide on volume growth and customer loans:

Asset Quality and Capital Position

Banco BPM continued to improve its asset quality, with gross non-performing exposures (NPEs) decreasing by 22.8% year-over-year and 3.5% quarter-over-quarter. Net bad loans, excluding state-guaranteed loans, were reported as "close to zero," reflecting the bank’s successful efforts to clean up its balance sheet.

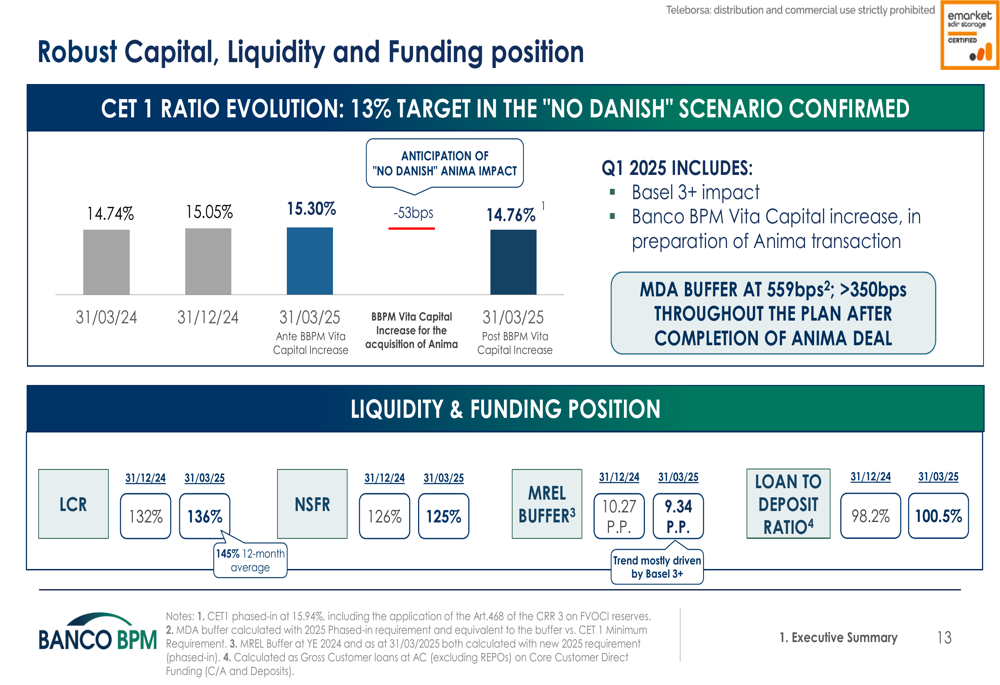

The bank’s capital position remained robust, with the CET1 ratio increasing to 15.30% as of March 31, 2025, up from 14.74% a year earlier. The management buffer above minimum distributable amount (MDA) requirements stood at a comfortable 559 basis points, which the bank expects to maintain above 350 basis points throughout its strategic plan even after the completion of the Anima deal.

The following slide details the bank’s capital, liquidity, and funding position:

Forward-Looking Statements

Based on the strong Q1 2025 performance, Banco BPM upgraded its full-year 2025 net income guidance from approximately €1.7 billion to approximately €1.95 billion. The bank remains confident in achieving its 2027 net income target of €2.15 billion, with Q1 2025 pro-forma results (including Anima) already tracking 2% higher than the 2027 quarterly target.

The bank expects the Anima acquisition to start contributing to its P&L from Q2 2025 onward, with a potential contribution of €39 million already identified for Q1 if fully consolidated. Management confirmed its CET1 ratio target of 13% in the "no Danish" scenario, indicating strong capital generation capacity even while pursuing strategic acquisitions.

The income statement highlights for Q1 2025 are presented in the following slide:

Banco BPM’s Q1 2025 results demonstrate significant progress toward its strategic goals, with record-breaking profitability, improved asset quality, and a strengthened business model following the Anima acquisition. The upgraded guidance for 2025 suggests continued momentum as the bank advances toward its 2027 targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.