Palantir launches Chain Reaction AI infrastructure platform with CenterPoint and NVIDIA

Introduction & Market Context

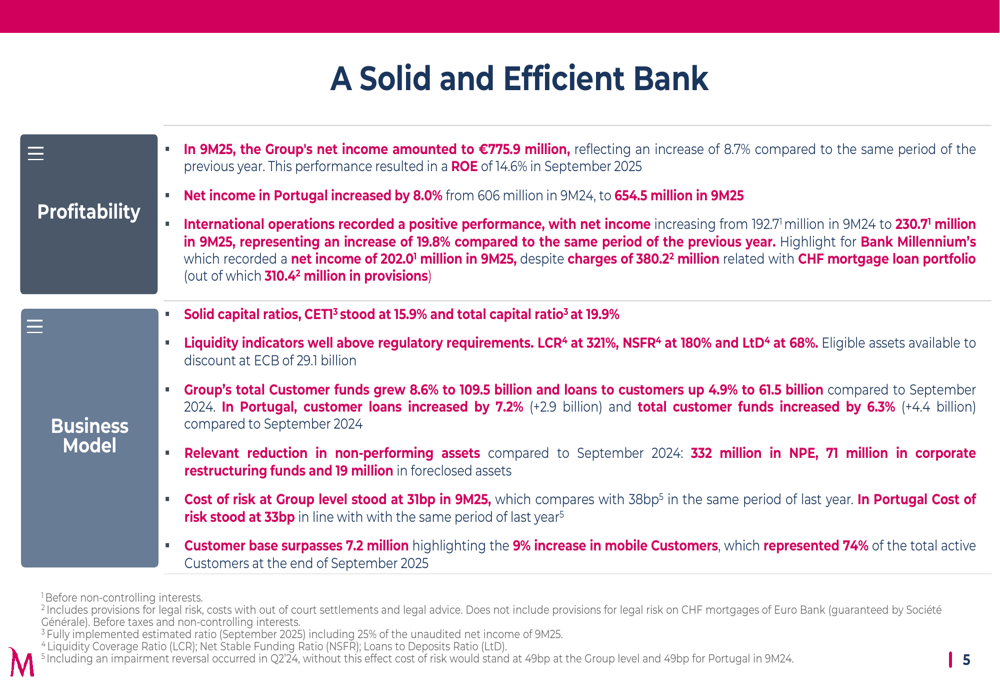

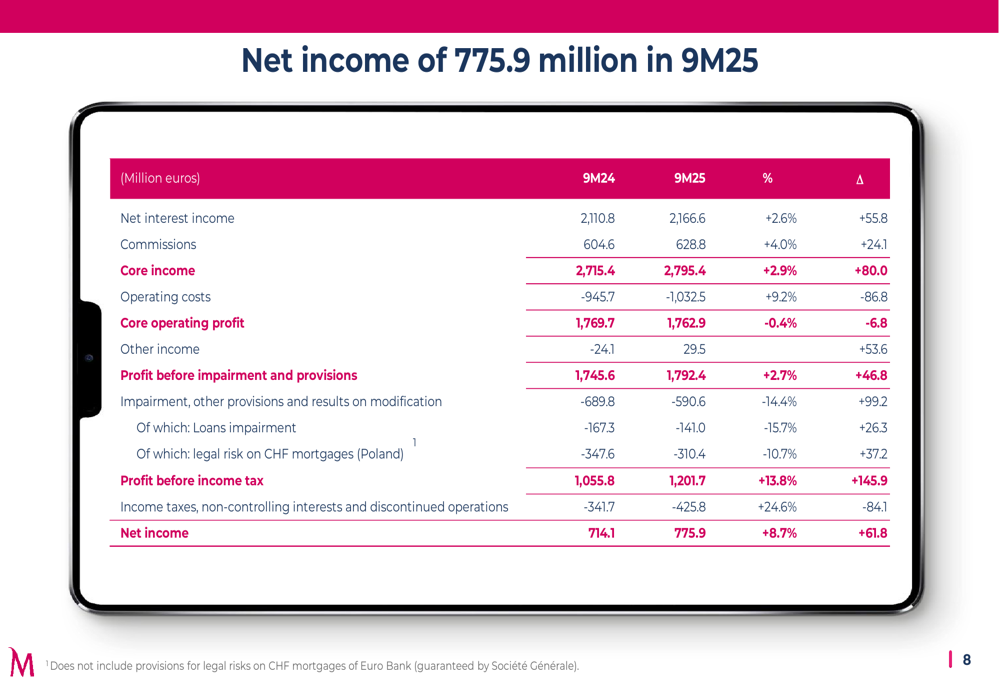

Banco Comercial Português (BCP) reported strong financial results for the first nine months of 2025, with net income reaching €775.9 million, an 8.7% increase compared to the same period in 2024. The bank's stock reacted positively to the earnings announcement, rising 1.74% to €0.784, though it has since retreated 3.19% to close at €0.759 as of October 30, 2025.

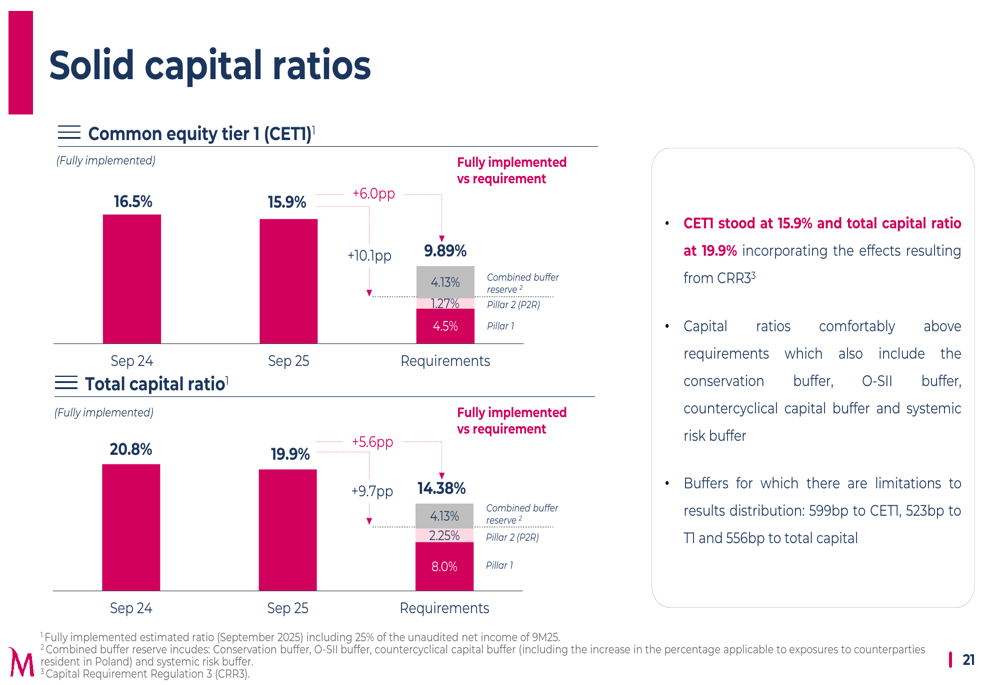

The bank maintained a solid capital position with a Common Equity Tier 1 (CET1) ratio of 15.9%, well above the regulatory requirement of 9.89%. This performance comes amid ongoing digital transformation efforts that have significantly increased mobile banking adoption and transactions.

As shown in the following key performance highlights, BCP achieved a return on equity (ROE) of 14.6% while continuing to improve asset quality:

Quarterly Performance Highlights

BCP's core income grew by 2.9% year-over-year to €2,795.4 million, driven by a 2.6% increase in net interest income to €2,166.6 million and a 4.0% rise in commissions to €628.8 million. Operating costs increased by 9.2% to €1,032.5 million, resulting in a cost-to-income ratio of 37%.

The detailed income statement shows improvement across most metrics, with profit before income tax rising 13.8% to €1,201.7 million. Impairment and provisions decreased by 14.4% to €590.6 million, contributing significantly to the bottom-line growth:

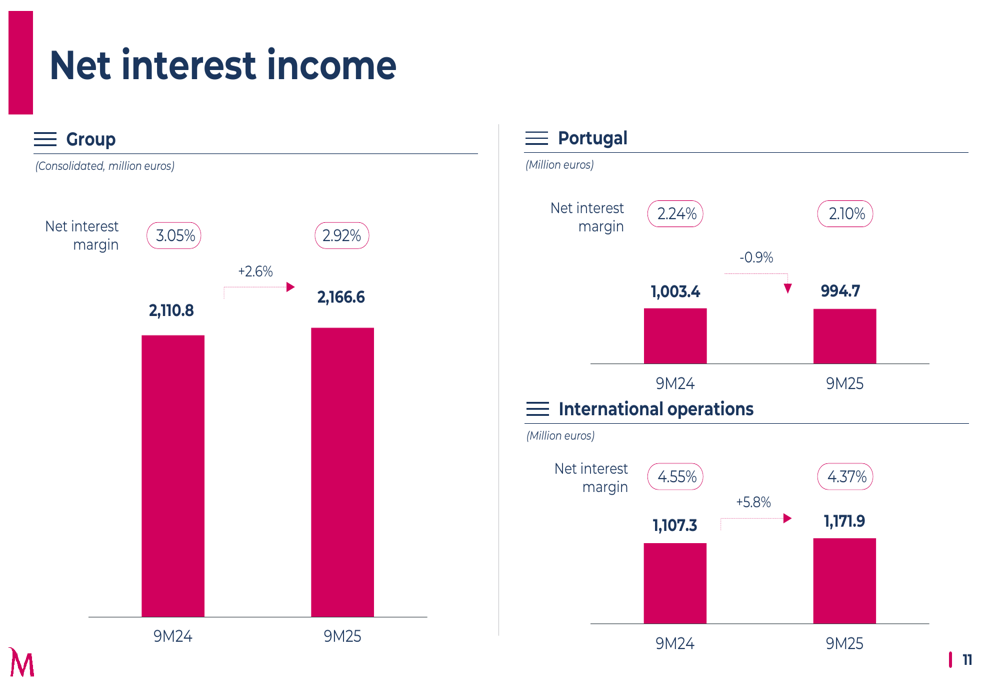

Net interest income performance varied by region, with the international operations growing by 5.8% to €1,171.9 million, offsetting a slight 0.9% decline in Portugal to €994.7 million. The group's net interest margin decreased slightly from 3.05% to 2.92%:

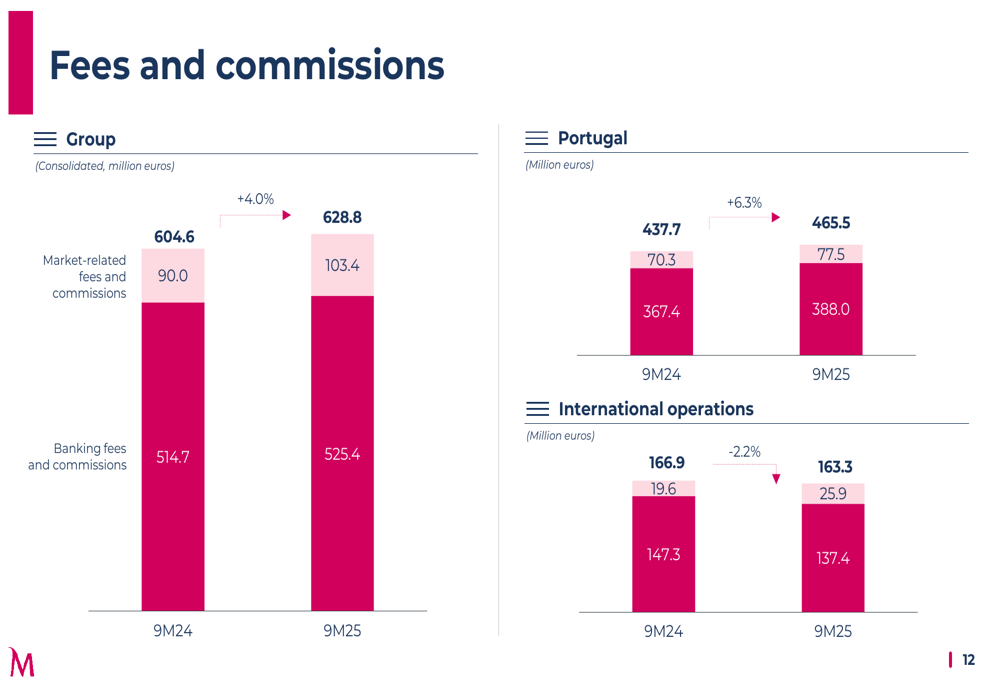

Fees and commissions showed strong growth in Portugal, increasing by 6.3% to €465.5 million, while international operations saw a 2.2% decrease to €163.3 million:

Digital Banking Transformation

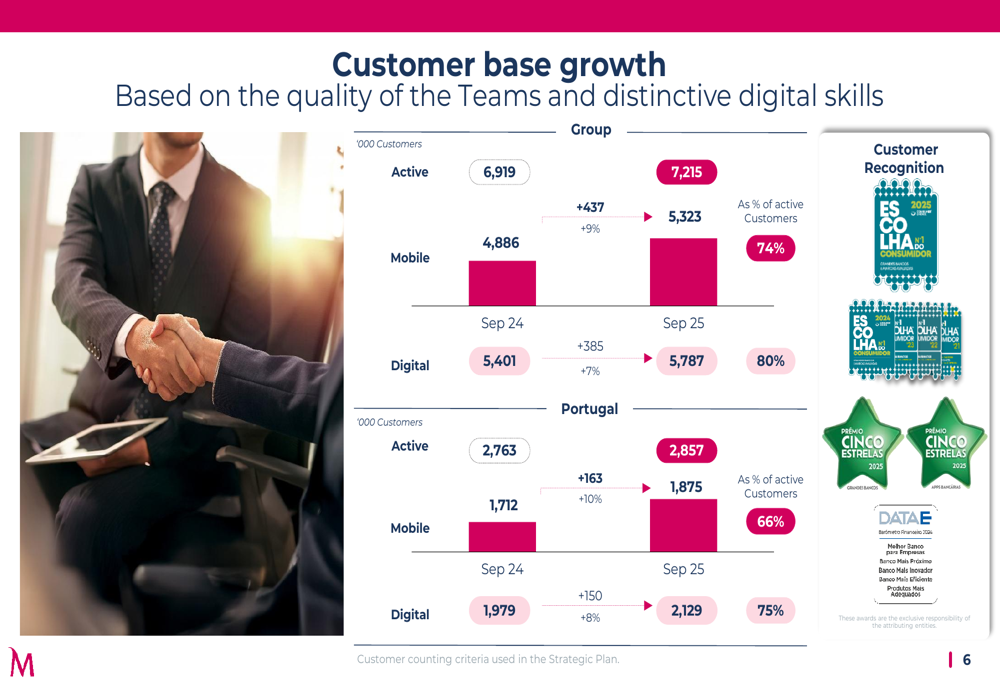

BCP's digital transformation continues to accelerate, with mobile customers increasing by 9% year-over-year to 5.3 million, now representing 74% of active customers. In Portugal, mobile customers grew by 10% to 1.9 million, accounting for 66% of active customers:

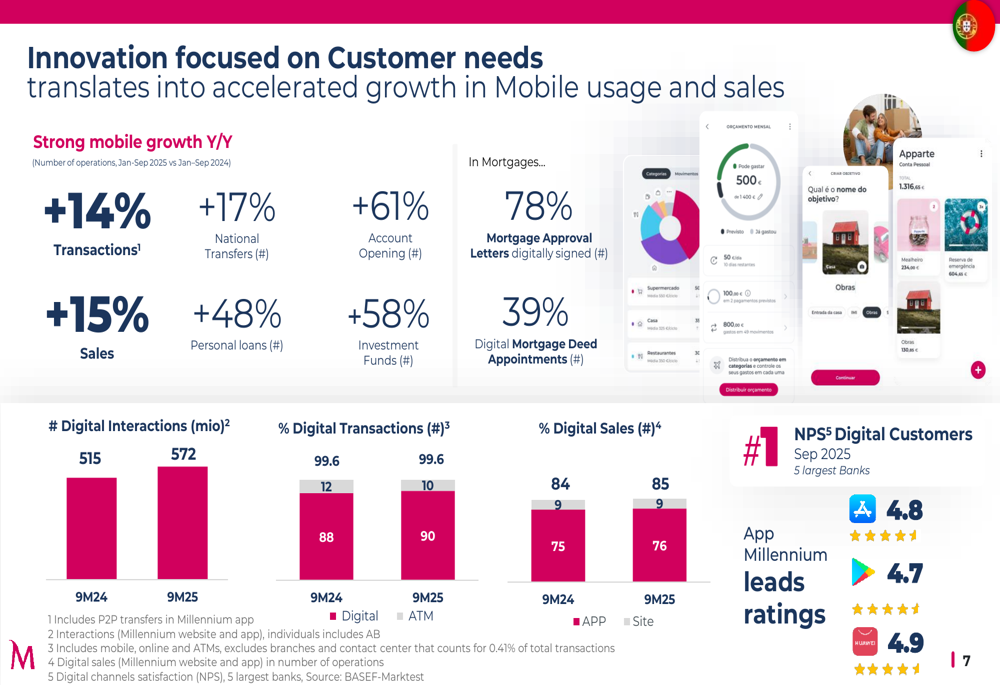

The bank reported impressive growth in mobile banking transactions and sales. Year-over-year, mobile transactions increased by 14%, national transfers by 17%, and account openings by 61%. Personal loans and investment funds through mobile channels grew by 48% and 58% respectively:

Capital Position and Asset Quality

BCP maintained a strong capital position with a CET1 ratio of 15.9% and a total capital ratio of 19.9%, both significantly above regulatory requirements. These capital buffers provide the bank with financial flexibility and stability:

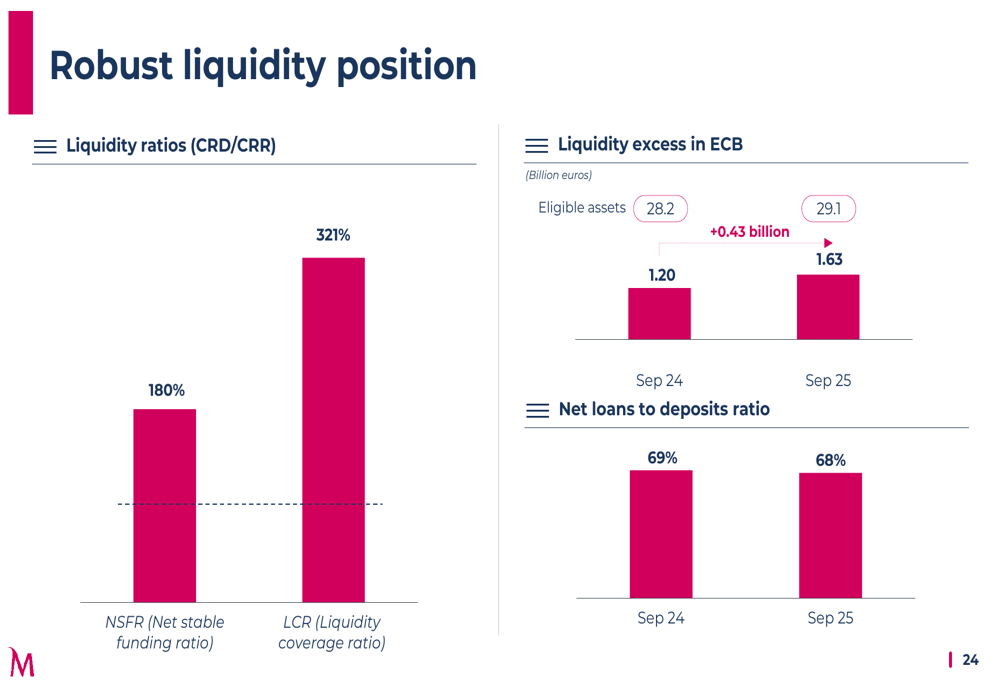

The bank's liquidity position remains robust, with a Liquidity Coverage Ratio (LCR) of 321% and a Net Stable Funding Ratio (NSFR) of 180%, well above regulatory minimums. The bank has €29.1 billion in eligible assets with the European Central Bank:

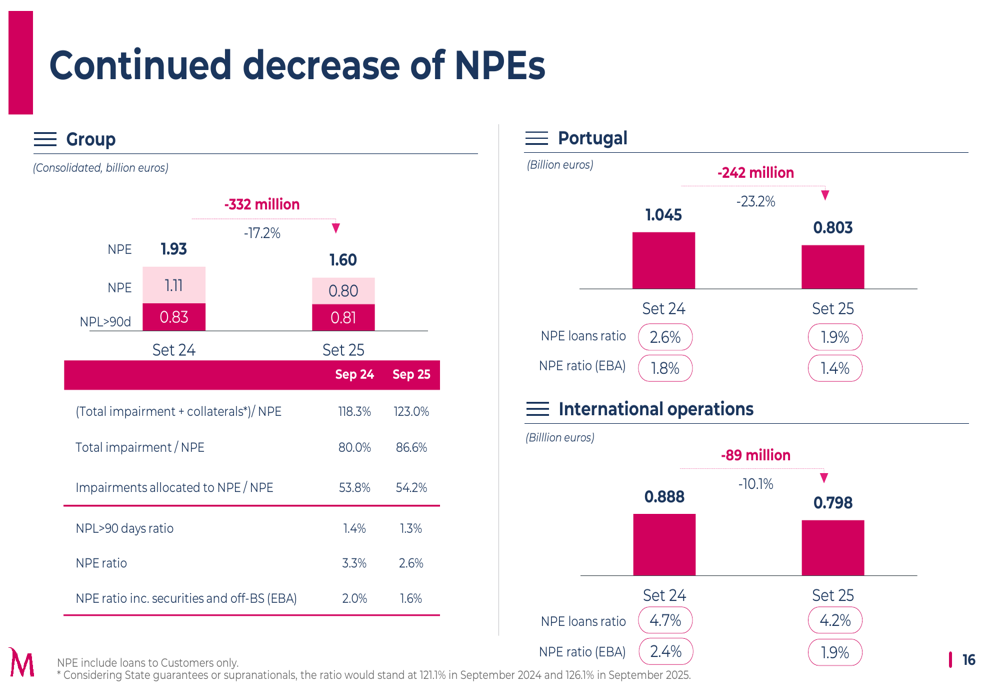

Asset quality continued to improve, with non-performing exposures (NPEs) decreasing by 17.2% year-over-year to €1.60 billion. In Portugal, NPEs declined by 23.2% to €0.803 billion, resulting in an NPE ratio of 1.4% (EBA definition):

Regional Performance

Portugal

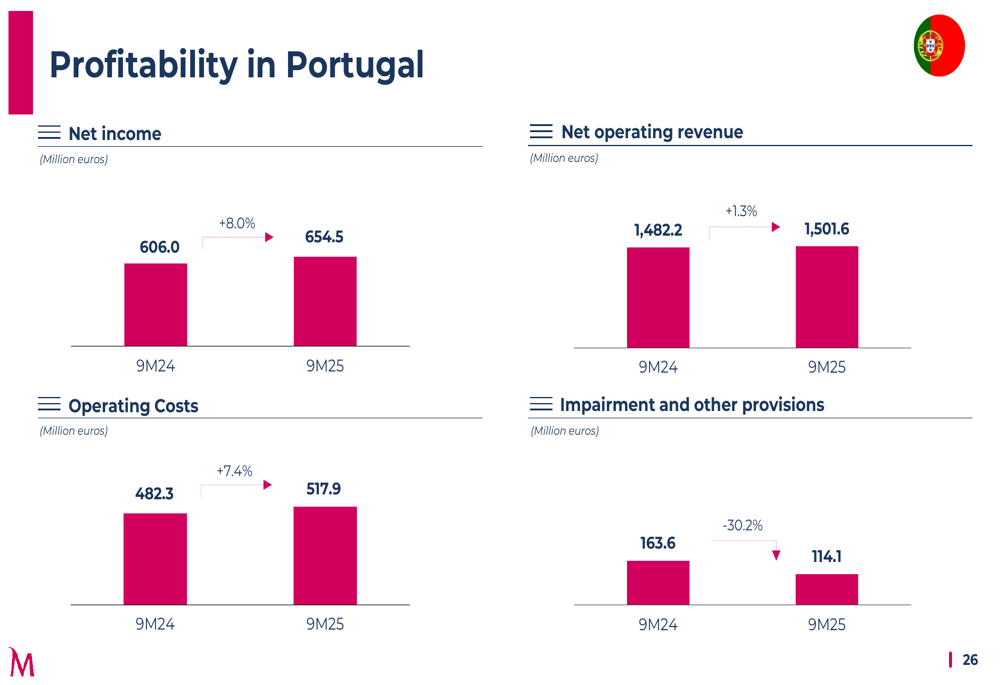

The Portuguese operation delivered strong results with net income increasing by 8.0% to €654.5 million. Net operating revenue grew by 1.3% to €1,501.6 million, while impairment and provisions decreased significantly by 30.2% to €114.1 million:

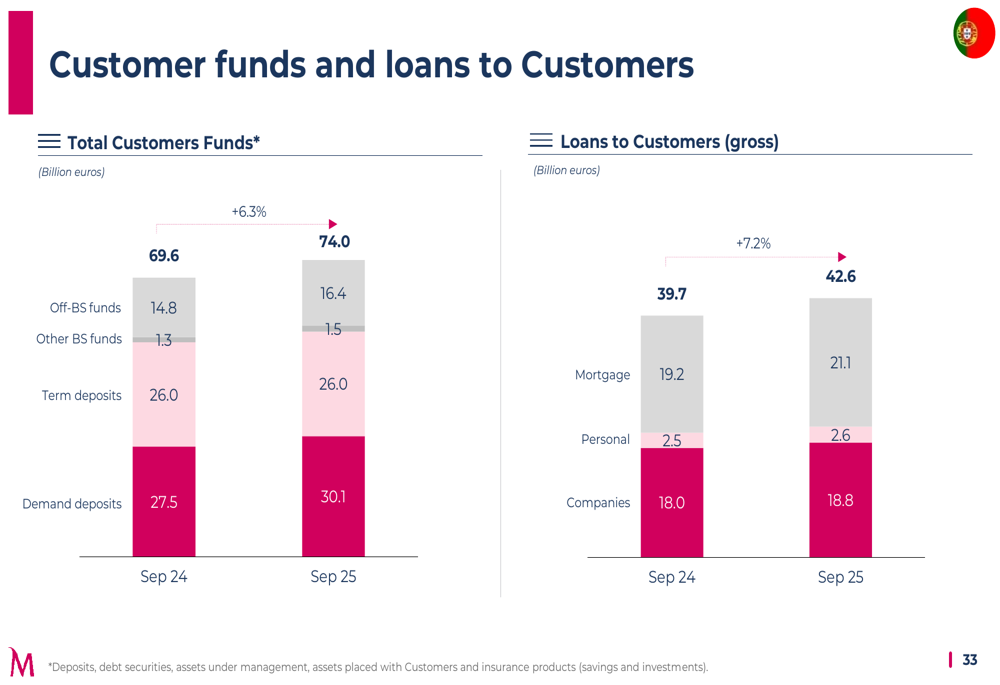

Customer funds in Portugal grew by 6.3% to €74.0 billion, while loans to customers increased by 7.2% to €42.6 billion. Performing loans showed even stronger growth of 8.0%, reaching €41.8 billion, with the mortgage loan portfolio expanding by €1.9 billion:

International Operations

International operations contributed €121.5 million to the group's net income, a 12.4% increase compared to the previous year. Bank Millennium in Poland was the largest contributor, followed by operations in Mozambique and other markets.

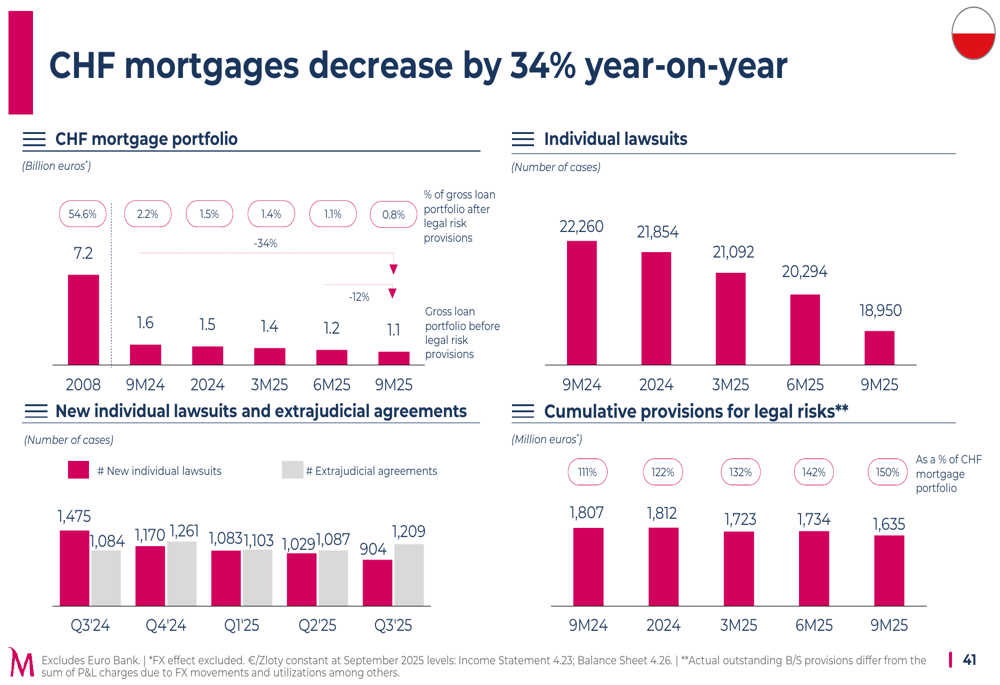

Bank Millennium reported a 2.2% increase in net income to €554.4 million, with net operating revenue growing by 7.8% to €1,220.2 million. The bank continues to manage its Swiss franc mortgage portfolio, which has decreased by 34% to €1.1 billion:

Millennium bim in Mozambique faced challenges, with net income declining by 58.9% to €25.4 million despite a 4.9% increase in net operating revenue to €200.2 million. The bank maintained growth in customer funds (+5.7%) and loans (+3.9%).

Forward-Looking Statements

Looking ahead, BCP aims to achieve a business volume target of €190 billion, up from the current €171 billion (combined customer funds and loans). The bank plans to expand its client base to 8 million from the current 7.2 million while maintaining a cost-to-income ratio below 40%.

The bank's strategic focus remains on digital transformation, operational efficiency, and maintaining strong capital and liquidity positions. BCP expects continued growth in mobile banking adoption and transactions, which should support fee income growth and customer acquisition.

The ongoing reduction in non-performing assets remains a priority, with the bank targeting further improvements in asset quality metrics. In Poland, the continued management of the Swiss franc mortgage portfolio will be crucial for risk mitigation.

Overall, BCP's 9M 2025 results demonstrate the bank's resilience and ability to generate sustainable growth despite challenging market conditions. The strong capital position, improving asset quality, and digital transformation progress position the bank well for continued success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.