Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Banco de Chile (NYSE:BCH) presented its first quarter 2025 earnings results on May 7, revealing a 14.2% increase in net income despite falling short of revenue expectations. The bank’s stock closed at $143 on May 8, down 1.65% from the previous close, reflecting investor concerns over the revenue miss despite the earnings beat.

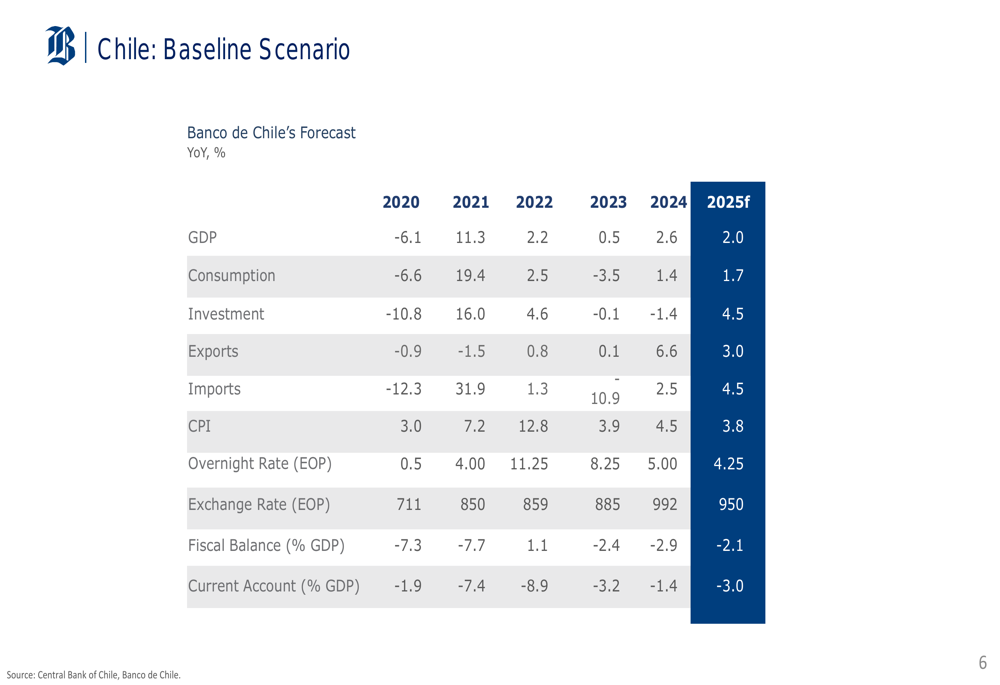

The presentation highlighted Chile’s economic environment, with GDP growth forecasted at 2.0% for 2025 and inflation expected to converge to 3.8% by year-end. The bank operates in a context of gradually declining interest rates, with the overnight rate projected to reach 4.25% by the end of 2025.

As shown in the following economic forecast chart, Chile’s economy is expected to maintain moderate growth despite global uncertainties:

Quarterly Performance Highlights

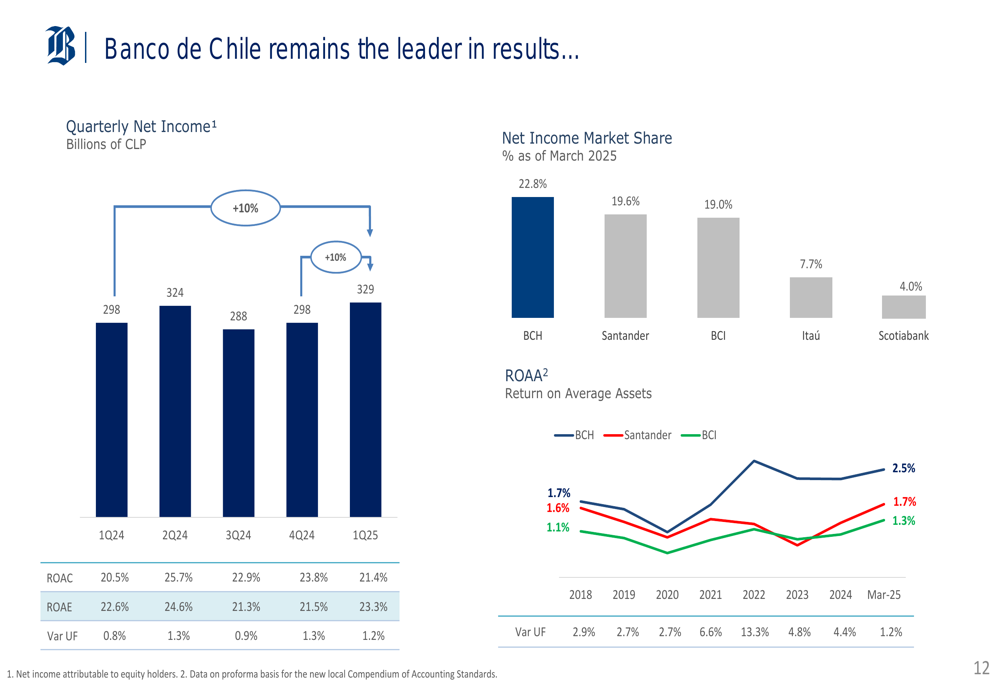

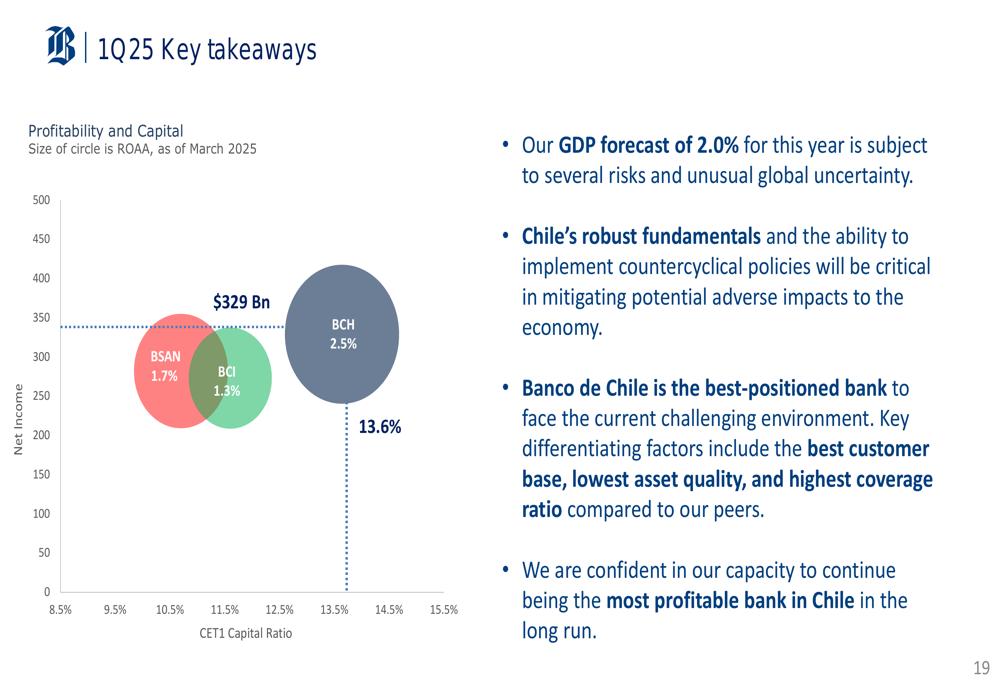

Banco de Chile reported net income of 329 billion CLP for Q1 2025, up from 288 billion CLP in Q1 2024, representing a 14.2% year-over-year increase. However, total revenue reached 779 billion CLP, falling short of analyst expectations of 797.9 billion CLP. This mixed performance contributed to the stock’s decline despite the earnings beat, with EPS of 3.26 exceeding the forecast of 2.83.

The bank’s quarterly performance demonstrates consistent growth in profitability metrics, with return on average assets reaching 1.7% in March 2025, outperforming major competitors Santander (BME:SAN) (1.3%) and BCI (1.5%).

The following chart illustrates the bank’s quarterly net income growth and market share position:

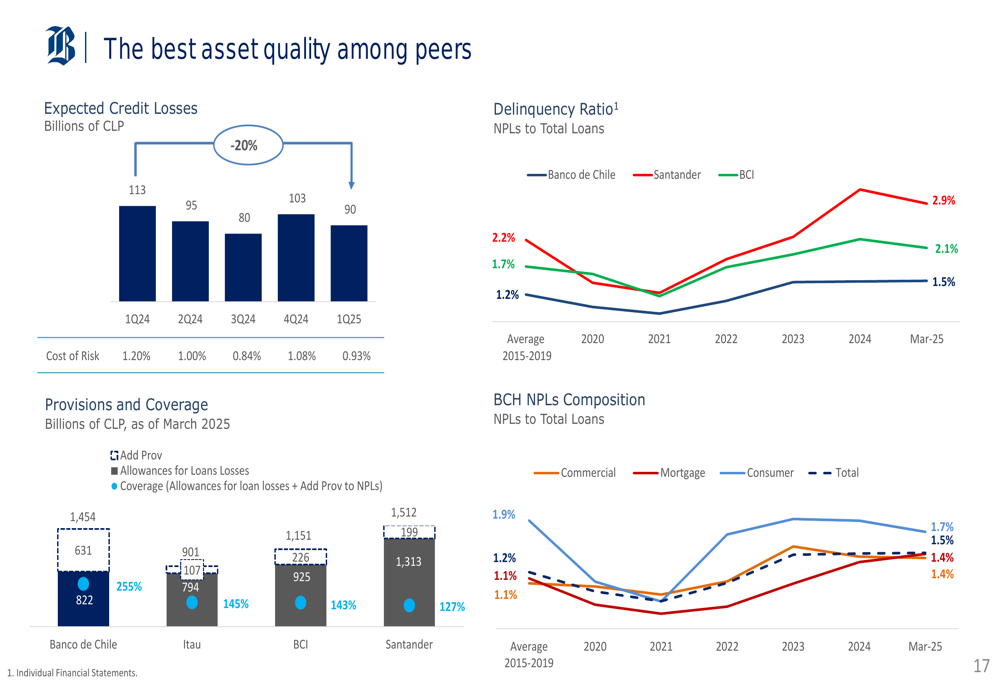

Asset quality showed significant improvement, with expected credit losses decreasing by 20% year-over-year from 113 billion CLP in Q1 2024 to 90 billion CLP in Q1 2025. The bank maintained a delinquency ratio of 1.5% as of March 2025, reflecting strong risk management practices.

The following asset quality comparison highlights the bank’s performance in this area:

Competitive Industry Position

Banco de Chile maintains a leading position in several key metrics within the Chilean banking sector. The bank holds the largest market share in net income at 22.8%, followed by Santander (19.6%) and BCI (19.0%). It also leads in profitability metrics, with a net interest margin of 4.7% compared to Santander’s 4.0% and BCI’s 3.7%.

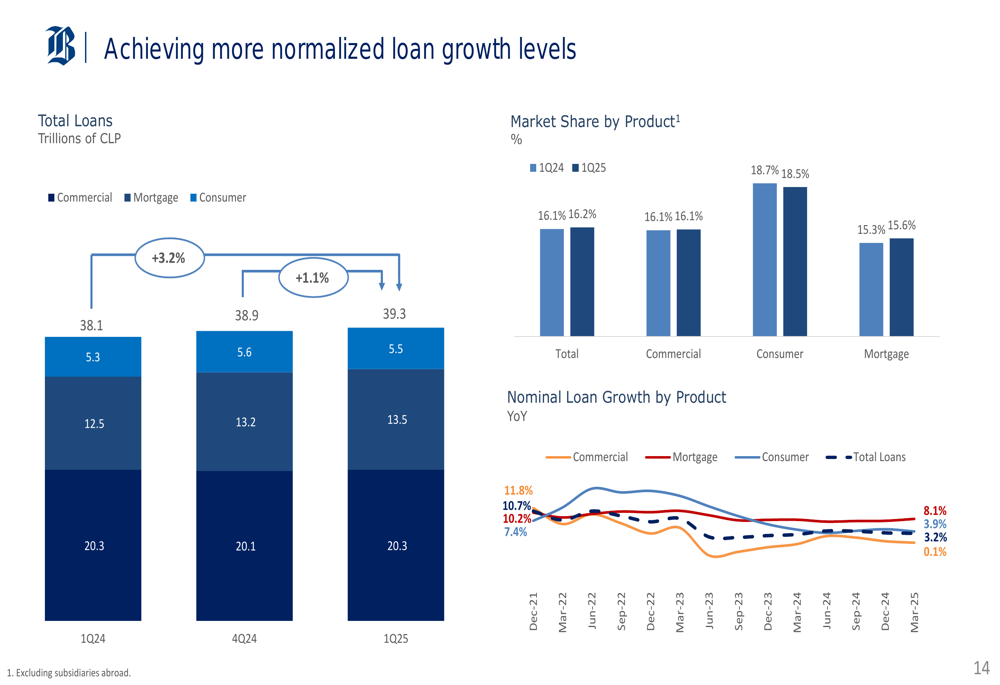

The bank’s loan portfolio reached 39.3 trillion CLP in Q1 2025, up from 38.1 trillion CLP in Q1 2024. Market share by product segment shows strength across categories, with total loans at 16.2%, commercial loans at 16.1%, consumer loans at 18.5%, and mortgage loans at 15.6%.

The following chart details the bank’s loan growth and market share by product:

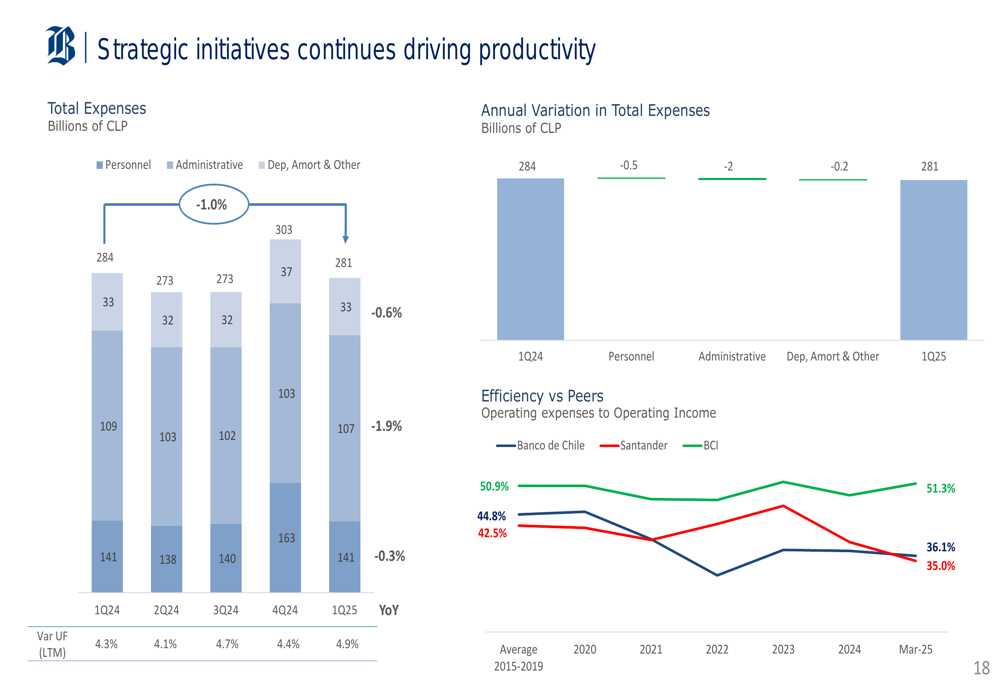

Banco de Chile also demonstrates superior operational efficiency, with a cost-to-income ratio of 36.1%, well below its target of ≤42%. Total (EPA:TTEF) expenses decreased by approximately 1% year-over-year, reflecting effective cost management initiatives.

The expense analysis below shows the bank’s cost structure and trends:

Strategic Initiatives

The presentation highlighted several strategic initiatives aimed at enhancing the bank’s competitive position and operational efficiency. These include the implementation of AI tools, with the adoption of AI Copilot Chat, and digital enhancements that have boosted retail current account originations by 35%.

The bank has also introduced new products, including more flexible personal banking options and new foreign exchange bank accounts for businesses in GBP, Yen, and Yuan. Digital FAN accounts showed 21% year-over-year growth, demonstrating the success of the bank’s digital transformation efforts.

Cost optimization remains a priority, with the bank centralizing functions to improve efficiency. These initiatives support Banco de Chile’s strategic pillars and mid-term targets, which include maintaining top positions in return on average capital and reserves, market share, net promoter score, and corporate reputation.

Forward-Looking Statements

Banco de Chile maintains a positive outlook for 2025, projecting continued profitability despite economic challenges. The bank expects Chile’s GDP to grow by 2.0% in 2025, with inflation converging to 3.8% and the overnight interest rate stabilizing around 4.25% by year-end.

The following key takeaways summarize the bank’s position and outlook:

Management emphasized the bank’s robust fundamentals and its position as the most profitable bank in Chile, which they believe will enable it to navigate economic uncertainties effectively. The bank aims to maintain its leadership in demand deposits and strengthen its position in commercial and consumer lending.

Despite the positive outlook presented in the slides, investors should note the revenue shortfall in Q1 2025 and the subsequent stock price decline. While Banco de Chile continues to deliver strong profitability, market expectations regarding revenue growth may present challenges in the coming quarters as the bank executes its strategic initiatives in a moderately growing economic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.