TSX jumps amid Fed rate cut hopes, ongoing U.S. government shutdown

Introduction & Market Context

Bank Handlowy w Warszawie SA (WSE:BHW), operating under the Citi Handlowy brand in Poland, presented its first quarter 2025 financial results on May 8, 2025, showcasing solid performance amid a challenging economic environment. The bank reported strong profitability metrics and loan growth despite some revenue pressure, outperforming the broader Polish banking sector in several key areas.

The presentation comes as Poland’s economy is projected to grow between 2.9% and 4.3% through 2026, with the National Bank of Poland expected to gradually reduce its reference rate from the current 5.75% to 3.50% by the end of 2026.

Quarterly Performance Highlights

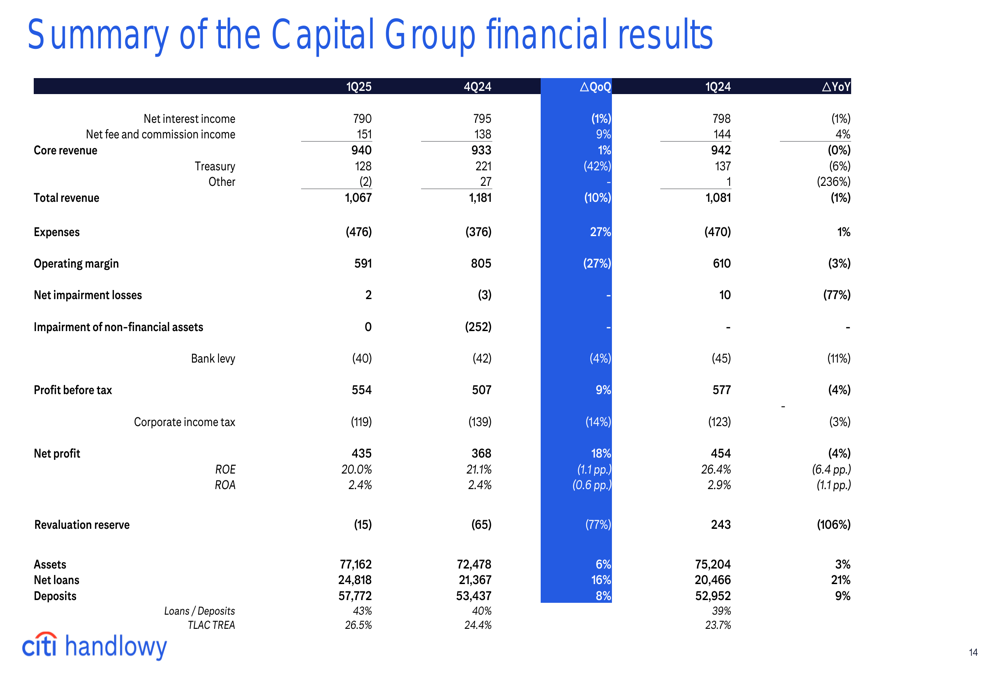

Bank Handlowy reported a net profit of PLN 435 million for Q1 2025, achieving a return on equity (ROE) of 20.0%. Total (EPA:TTEF) revenue reached PLN 1,067 million, with the bank’s loan portfolio expanding by 12% year-over-year and deposits growing by 9%.

As shown in the following comprehensive financial summary:

The bank maintained a strong capital position with a TLAC TREA ratio of 26.5%, providing ample buffer for continued growth and regulatory compliance.

Detailed Financial Analysis

Revenue and Interest Income

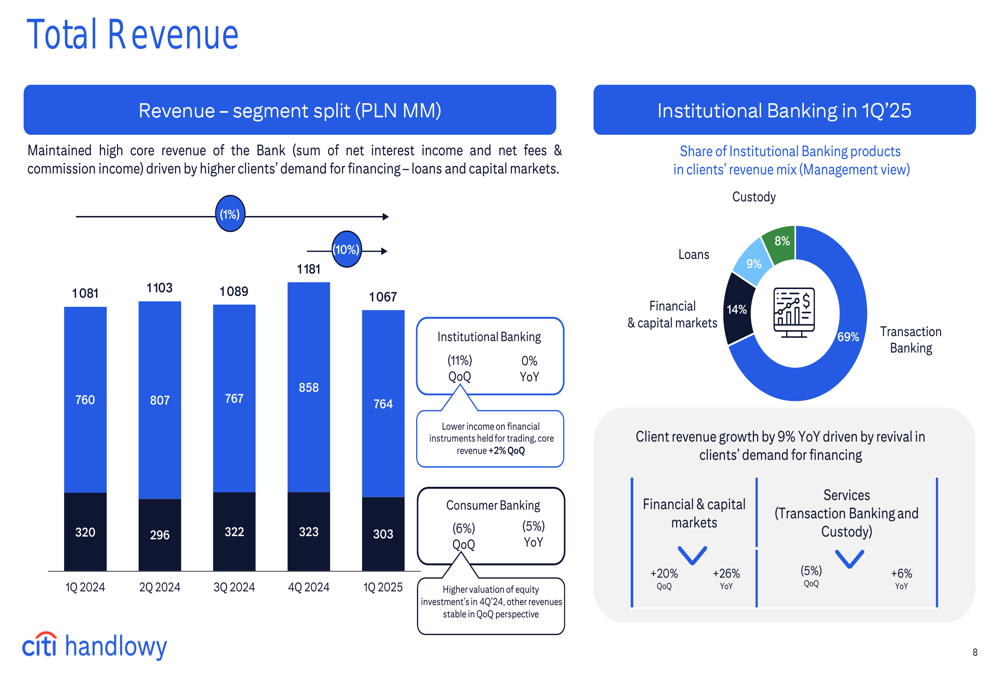

Total revenue slightly decreased to PLN 1,067 million from PLN 1,081 million in Q1 2024. The revenue mix shows divergent performance across business segments, with Institutional Banking experiencing some pressure while Consumer Banking remained relatively stable.

The following chart illustrates the revenue breakdown by segment:

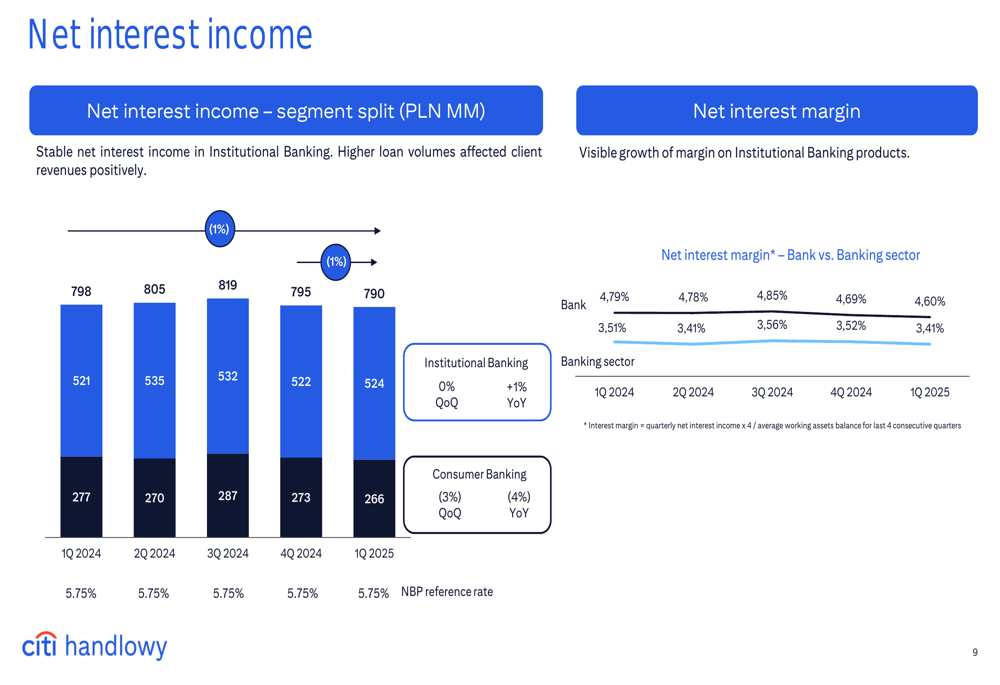

Net interest income, which accounts for the largest portion of the bank’s revenue, remained relatively stable at PLN 790 million compared to PLN 798 million in the same period last year. Notably, Bank Handlowy maintained a net interest margin of 4.60%, significantly outperforming the banking sector average of 3.41%, though showing a slight decline from 4.79% in Q1 2024.

The following chart demonstrates the bank’s consistent margin premium over the sector average:

Fee and Commission Income

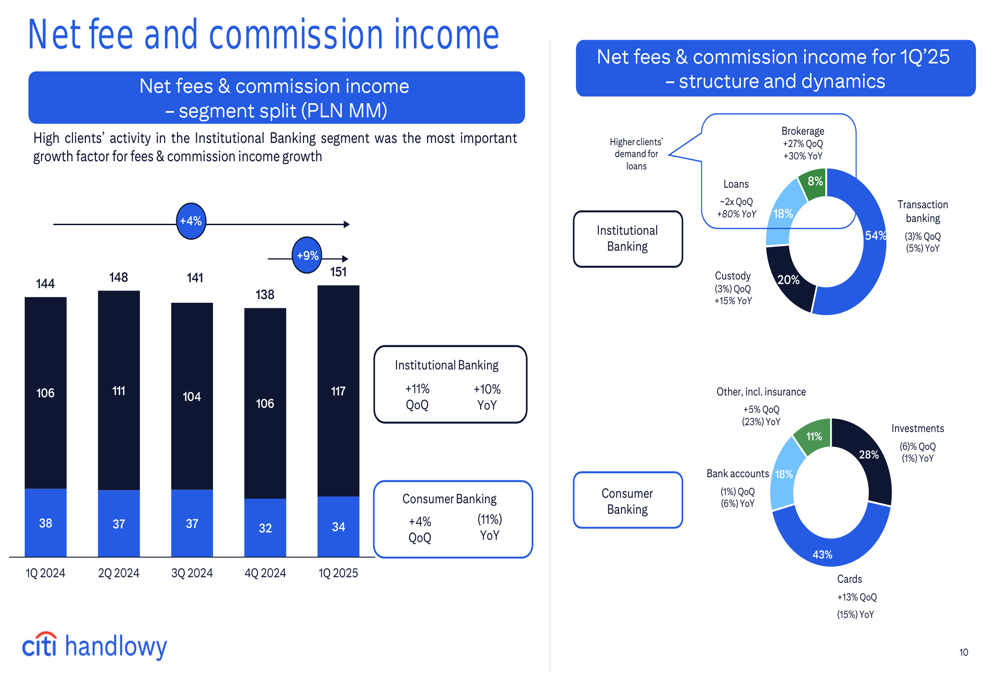

Net fee and commission income increased to PLN 151 million from PLN 144 million in Q1 2024, representing a 4.9% year-over-year growth. This improvement was primarily driven by Institutional Banking, which saw an 11% quarter-on-quarter and 10% year-on-year increase in fee income.

The following breakdown shows the composition and dynamics of fee income:

Expenses and Cost Management

Operating expenses increased marginally by 1% to PLN 476 million in Q1 2025. The bank maintained disciplined cost management despite inflationary pressures in the Polish economy.

Business Segment Performance

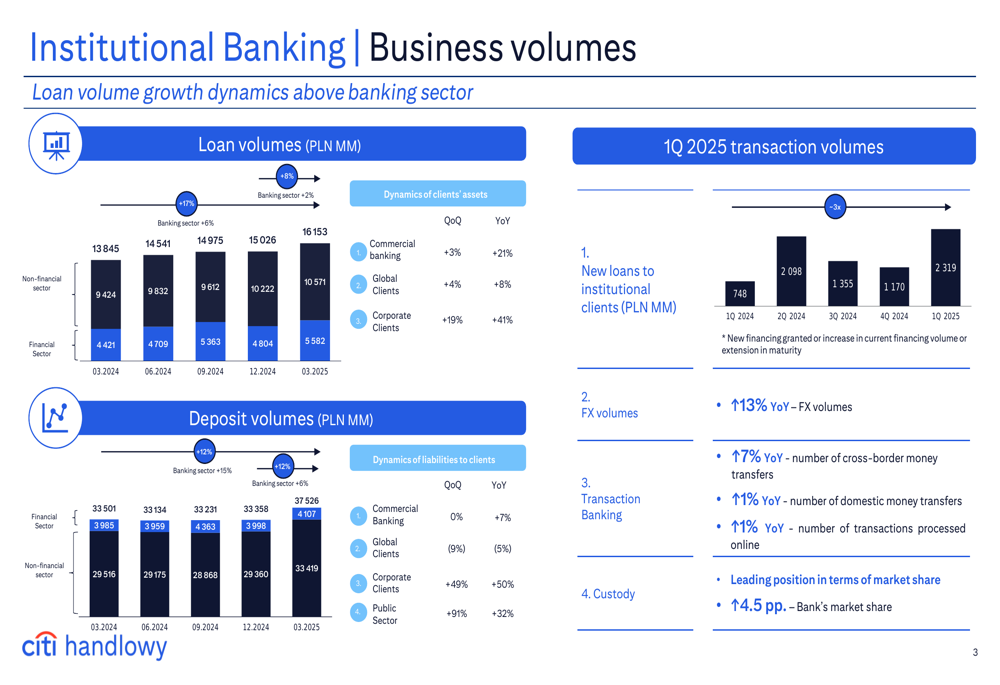

Institutional Banking

The Institutional Banking segment demonstrated strong loan growth of 8% quarter-on-quarter, despite experiencing an 11% revenue decline in the same period. The segment saw significant growth in financial markets turnover (+63% QoQ) and transaction banking (+6% QoQ).

The following chart details the business volumes across different client segments:

Bank Handlowy also highlighted several key transactions in the quarter, including syndicated loans for Elemental (EUR 252 million), InPost (PLN 4.2 billion), and W Holding (PLN 1.77 billion/EUR 101 million). In capital markets, the bank participated in Diagnostyka+’s IPO (PLN 1.7 billion) and CCC (WA:CCCP) Group’s share issuance (PLN 1.5 billion).

Consumer Banking

The Consumer Banking segment delivered stable revenue quarter-on-quarter, with deposits growing by 1% QoQ. The segment showed particular strength in FX operations (+16% QoQ) and wealth management (+30% QoQ).

FX volumes grew by 14% year-over-year, with 64% of FX volumes processed via CitiKantor. The number of transactions in CitiKantor increased by 20% year-over-year, reaching record high levels.

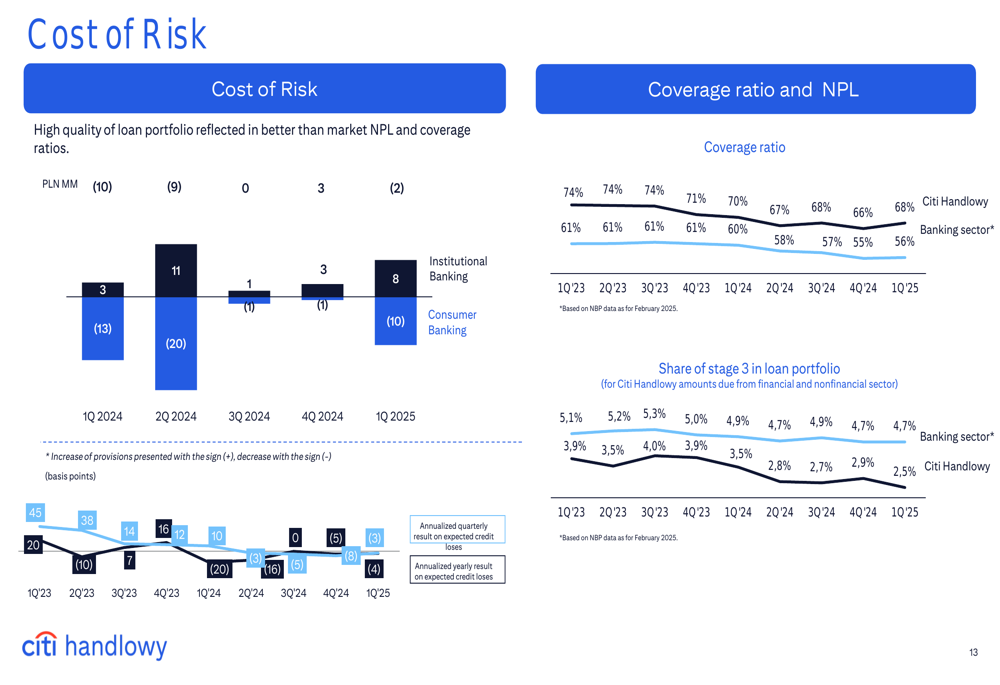

Capital Position and Risk Management

Bank Handlowy maintained a strong capital position with a TLAC TREA ratio of 26.5%. The cost of risk remained well-controlled, particularly in the Institutional Banking segment.

The following chart illustrates the cost of risk trends:

The bank’s coverage ratio stood at 68% for Stage 3 loans, significantly higher than the banking sector average of 55%. The share of Stage 3 loans in the bank’s portfolio was 2.5%, below the sector average of 3.9%.

Forward-Looking Statements

Looking ahead, Bank Handlowy is positioned to benefit from the projected growth in the Polish economy. GDP growth is forecast between 2.9% and 4.3% through 2026, with investments expected to grow between 3.5% and 4.8%.

The bank’s strategy appears focused on maintaining its premium position in transaction banking and custody services, while continuing to grow its loan portfolio and wealth management offerings. With its strong capital position and controlled risk profile, Bank Handlowy seems well-positioned to navigate the anticipated gradual reduction in Polish interest rates over the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.