BHP, Rio Tinto shares rise as peer Vale posts smaller-than-feared Q2 profit drop

Introduction & Market Context

Bausch + Lomb (NYSE:BLCO) reported mixed first quarter 2025 results, with revenue growth offset by earnings pressure from a voluntary recall of its enVista intraocular lens products. The company’s shares were down 5.32% in premarket trading to $12.99, reflecting investor concerns about the recall’s impact on full-year profitability despite raised revenue guidance.

The eye health company delivered 5% constant currency revenue growth in Q1, but faced headwinds from the recall, U.S. generics performance, and foreign exchange impacts. The results come after a strong fourth quarter 2024, when the company exceeded analyst expectations and reported robust organic growth.

Quarterly Performance Highlights

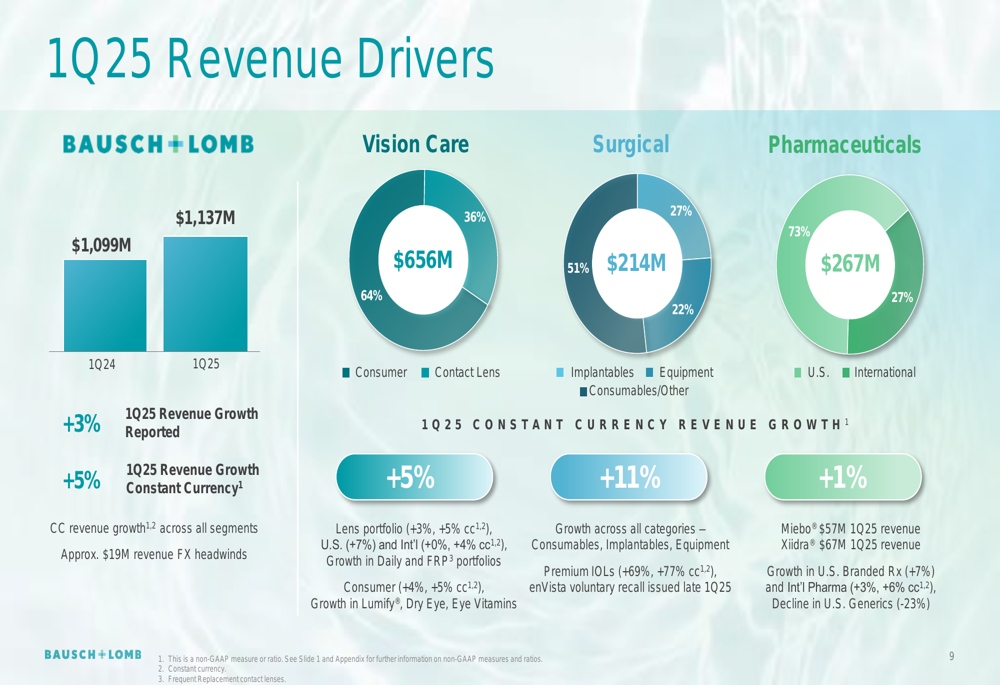

Bausch + Lomb reported total revenue of $1,137 million in Q1 2025, up from $1,099 million in Q1 2024, representing 5% growth on a constant currency basis. The company achieved organic revenue growth of 11% compared to the previous year, demonstrating strong underlying performance across its core business segments.

As shown in the following chart detailing growth across segments and franchises:

The company saw growth across all three of its main segments, with Vision Care up 5%, Surgical up 11%, and Pharmaceuticals up 1% on a constant currency basis. Several key franchises delivered impressive growth, including Blink (+84%), enVista (+69%), Infuse (+42%), Ultra (+13%), Artelac (+12%), and Lumify (+9%).

However, profitability metrics showed significant pressure. Adjusted EBITDA fell to $98 million in Q1 2025 from $180 million in Q1 2024, while adjusted EPS dropped to -$0.15 from $0.07 in the prior year period.

The following slide provides a detailed breakdown of the company’s Q1 2025 P&L performance:

Impact of enVista Recall

A significant factor affecting Q1 results was the voluntary recall of certain enVista intraocular lens (IOL) products. The company completed an investigation that determined the issue stemmed from raw material used in specific lots delivered by a different vendor. The recall had a one-time impact of -$16 million on Q1 results.

Bausch + Lomb has implemented enhanced inspection protocols for IOLs and more explicit standards for third-party vendors. The company has returned to full production of all enVista platform IOLs and expects to return to full market supply in the U.S. in the coming weeks.

The following slide details the company’s approach to returning enVista products to market:

Updated Guidance

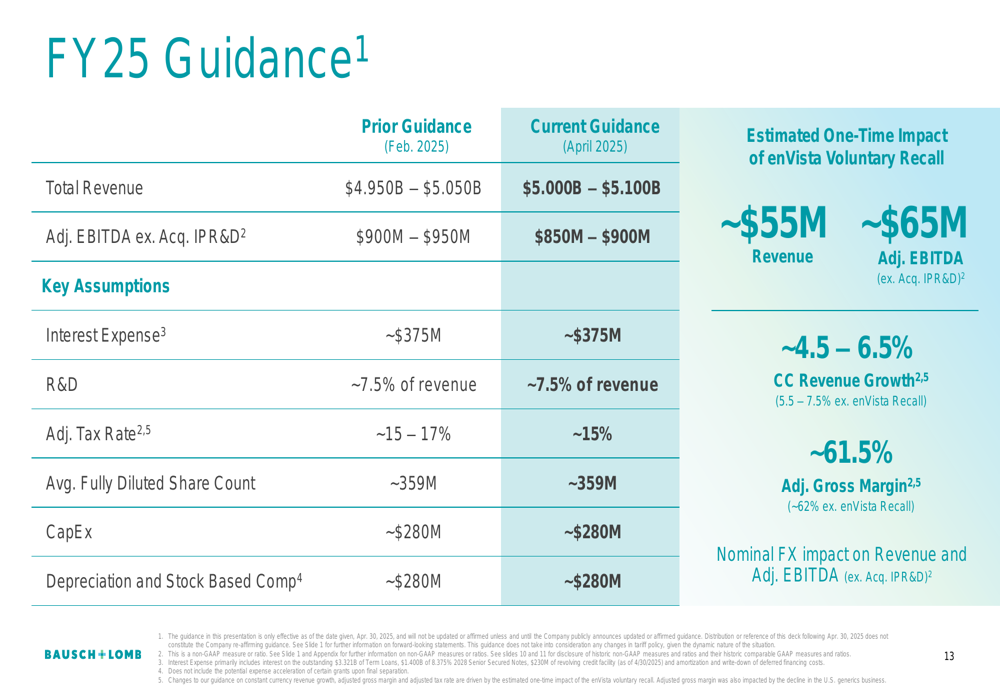

Despite the challenges from the enVista recall, Bausch + Lomb raised its full-year 2025 revenue guidance while lowering its adjusted EBITDA outlook. The company now expects total revenue of $5.000-$5.100 billion, up from the previous guidance of $4.950-$5.050 billion. However, adjusted EBITDA guidance was reduced to $850-$900 million from the prior $900-$950 million.

The following slide outlines the updated FY25 guidance:

The company provided a clear bridge explaining the changes to its guidance, highlighting how the enVista recall and foreign exchange impacts affected both revenue and EBITDA projections:

The estimated one-time impact of the enVista voluntary recall is expected to be approximately $55-$65 million for both revenue and adjusted EBITDA. This is partially offset by favorable foreign exchange impacts of approximately $100 million for revenue and $20 million for adjusted EBITDA.

Growth Drivers

Despite the challenges, Bausch + Lomb continues to see strong performance in several key growth drivers. The company’s dry eye portfolio, including Miebo and Xiidra, showed impressive results. Miebo generated $57 million in Q1 2025 revenue, while Xiidra contributed $67 million.

The following chart illustrates the strong growth in the company’s dry eye franchise:

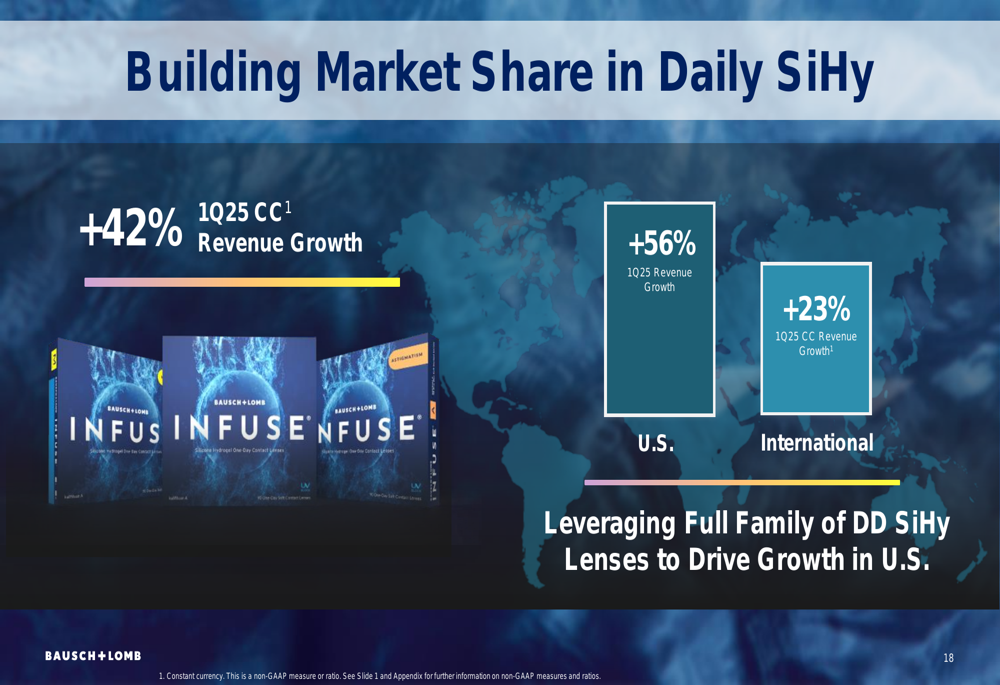

In the contact lens segment, the company’s Infuse daily silicone hydrogel lenses delivered 42% constant currency revenue growth in Q1 2025, with 56% growth in the U.S. and 23% growth internationally. This performance highlights the company’s success in building market share in the premium daily disposable contact lens category.

The following slide showcases the growth in the daily silicone hydrogel lens segment:

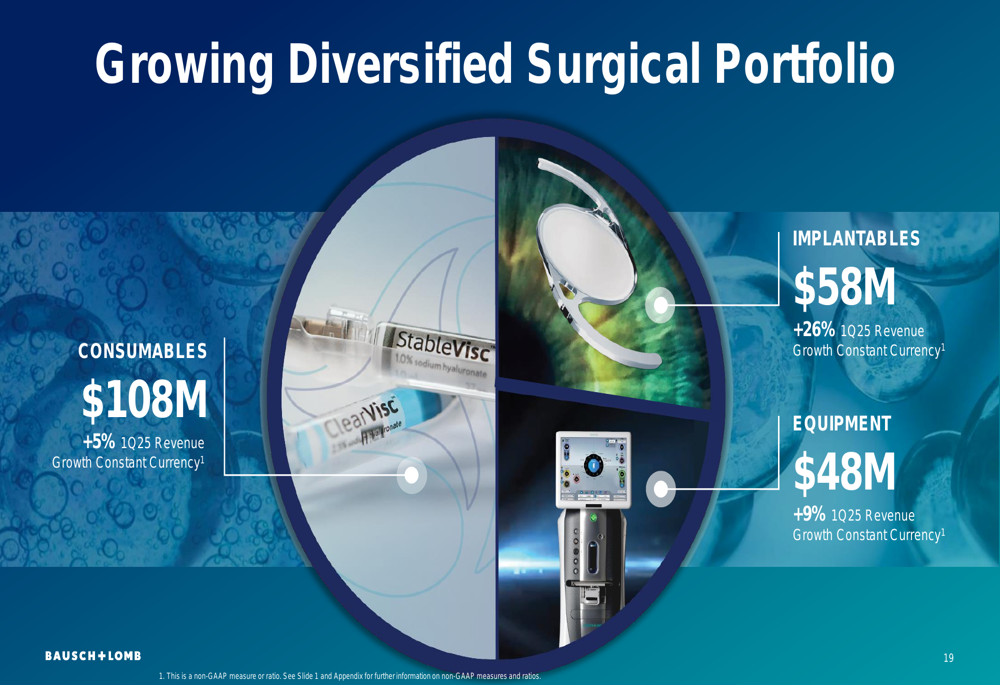

The surgical business also showed strong growth across its diversified portfolio, with implantables growing 26%, equipment up 9%, and consumables increasing 5% on a constant currency basis in Q1 2025.

As illustrated in this slide on the surgical portfolio:

Strategic Initiatives

Bausch + Lomb outlined its strategic focus on three core priorities: growing revenue at or above market, building selling and operational excellence, and prioritizing pipeline innovation. The company is also implementing strategies to manage tariff policies, including strategic inventory stocking, leveraging its global manufacturing footprint, and evaluating strategic pricing opportunities.

The following slide details the company’s strategic priorities:

The company’s global network, consisting of 23 manufacturing plants, 59 distribution facilities, and 160+ contract manufacturing organizations, provides flexibility to adapt to changing trade policies and supply chain challenges.

Pipeline and Innovation

Bausch + Lomb continues to advance its pipeline across multiple categories to drive future growth. Key pipeline assets include a biomimetic contact lens, next-generation Lumify, Elios MIGS treatment for glaucoma, and novel therapeutics for dry eye disease, glaucoma, and ocular surface pain.

The company is targeting end-of-year U.S. approval for its Elios next-generation MIGS treatment and initiating clinical studies across several innovative products.

The following slide provides an overview of the company’s pipeline initiatives:

Forward-Looking Statements

Despite the near-term challenges from the enVista recall, Bausch + Lomb remains confident in its ability to deliver constant currency revenue growth of approximately 4.5-6.5% for the full year 2025. The company expects to maintain an adjusted gross margin of around 61.5% and continues to invest in research and development at approximately 7.5% of revenue.

Key assumptions for 2025 include interest expense of approximately $375 million, an adjusted tax rate of around 15%, average fully diluted share count of approximately 359 million, capital expenditures of approximately $280 million, and depreciation and stock-based compensation of approximately $280 million.

The company’s focus on executing its strategic priorities, returning enVista to market, managing tariff policies, and advancing its pipeline positions it to overcome the current challenges and drive long-term growth in the eye health market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.