Stryker shares tumble despite strong Q2 results and raised guidance

Introduction & Market Context

Beazer Homes USA Inc (NYSE:BZH) released its second quarter fiscal 2025 earnings presentation on May 1, revealing modest revenue growth but significant profit declines amid persistent housing market challenges. The homebuilder reported a 3.2% increase in homebuilding revenue to $556 million, while net income plummeted 67.4% year-over-year to $12.8 million.

The stock traded up 2.51% to $20.02 in after-hours trading following the release, suggesting investors may have found some positives in the company’s forward guidance and strategic initiatives despite the profit decline. This comes after a challenging first quarter when Beazer missed earnings expectations substantially.

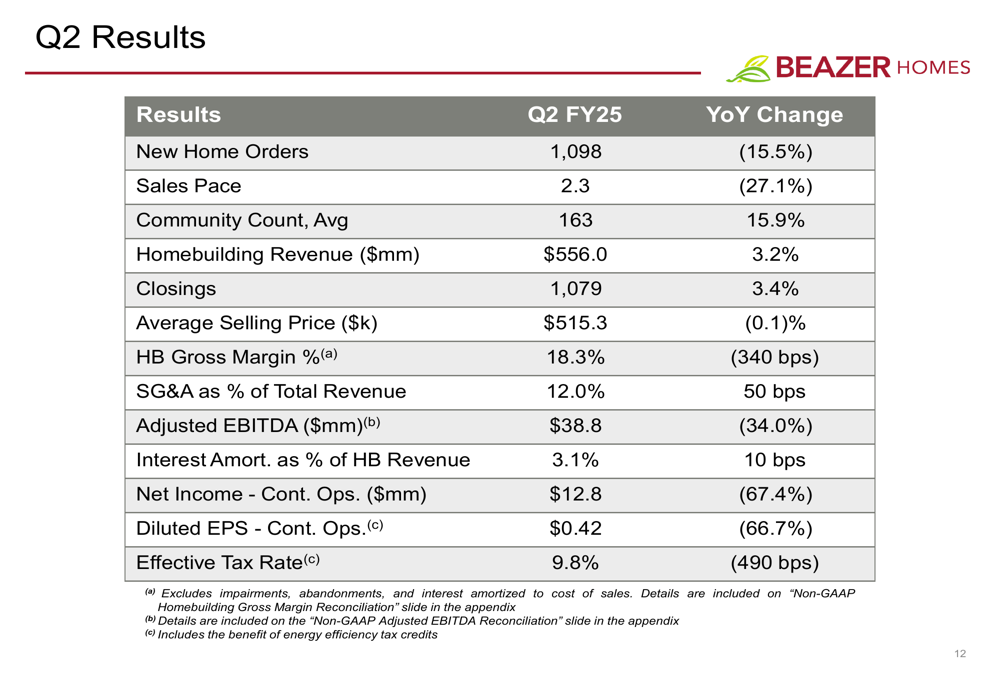

As shown in the following quarterly results summary, Beazer faced significant headwinds in profitability metrics despite modest top-line growth:

Quarterly Performance Highlights

Beazer’s Q2 results painted a mixed picture of the company’s performance. While closings increased 3.4% to 1,079 homes and community count grew 15.9% to an average of 163 active communities, new home orders declined 15.5% to 1,098. More concerning was the 27.1% drop in sales pace to 2.3 homes per community per month, indicating weakening demand.

The company’s profitability metrics showed substantial deterioration, with homebuilding gross margin falling 340 basis points to 18.3% and SG&A as a percentage of total revenue increasing 50 basis points to 12.0%. This margin compression, combined with lower sales volume, resulted in adjusted EBITDA declining 34.0% to $38.8 million and diluted EPS falling 66.7% to $0.42.

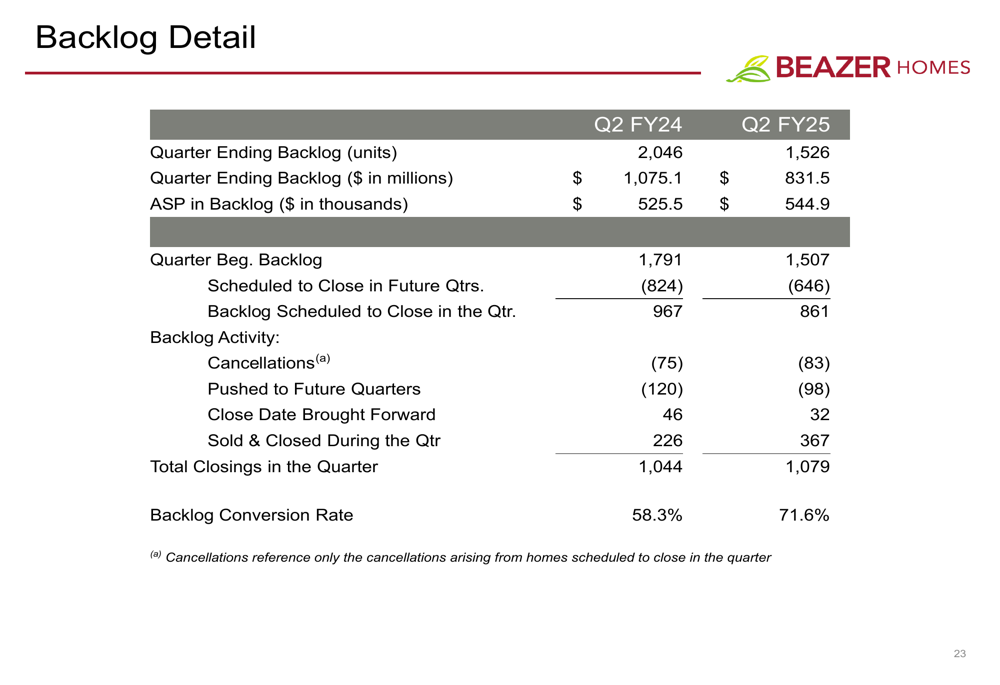

Beazer’s backlog also showed significant weakness compared to the prior year. As illustrated in the backlog detail slide:

The quarter-ending backlog units decreased from 2,046 to 1,526, while the dollar value fell from $1,075.1 million to $831.5 million. However, the average selling price in backlog increased 3.7% to $544,900, potentially providing some margin support in future quarters.

Strategic Initiatives

Despite current market challenges, Beazer outlined ambitious multi-year goals aimed at driving long-term growth and shareholder value. The company is focusing on three key strategic priorities through fiscal year 2027:

The updated capital allocation framework emphasizes community count expansion, balance sheet deleveraging, and share repurchases. Beazer repurchased $20 million of stock during Q2, bringing total repurchases to $42 million over the past three years.

Chairman and CEO Allan P. Merrill highlighted the company’s commitment to growth while maintaining financial discipline: "We’re optimistic about longer-term housing fundamentals while remaining committed to deleveraging our balance sheet into the low 30s to better align with peers."

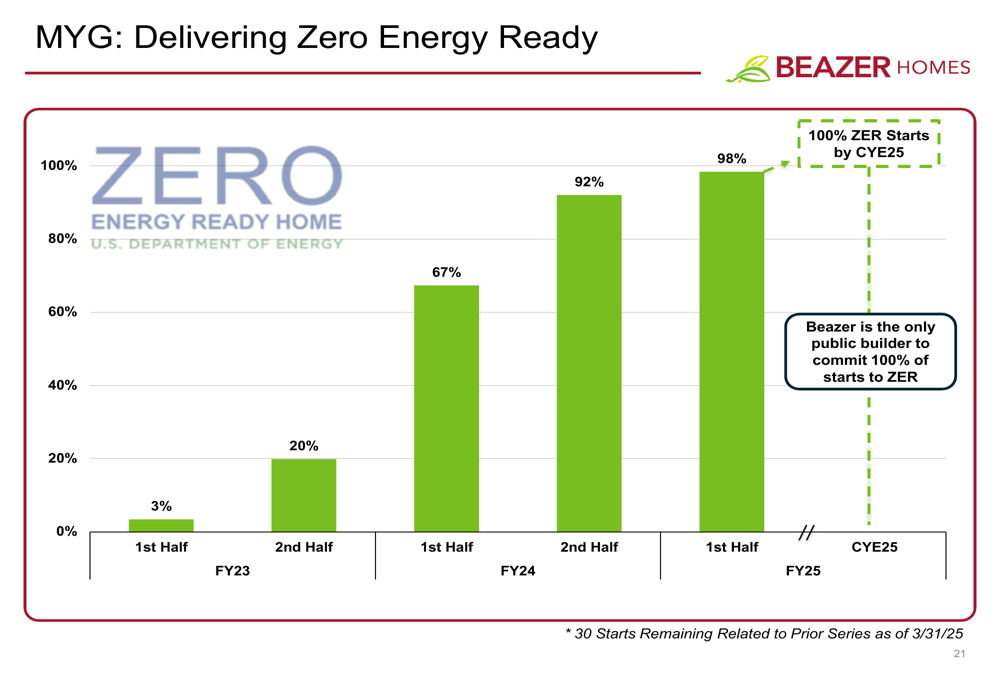

The company continues to differentiate itself through its Zero Energy Ready homes initiative, which has reached 98% of starts in the first half of FY25. Beazer claims to be the only public builder to commit 100% of its starts to this energy-efficient standard.

Forward-Looking Statements

For the third quarter of fiscal 2025, Beazer provided a relatively optimistic outlook, expecting new home orders to increase 5-10% and closings to range between 1,050-1,100 units. The company anticipates the average selling price to be approximately $525,000 with adjusted homebuilding gross margin improving slightly and diluted EPS exceeding $0.40.

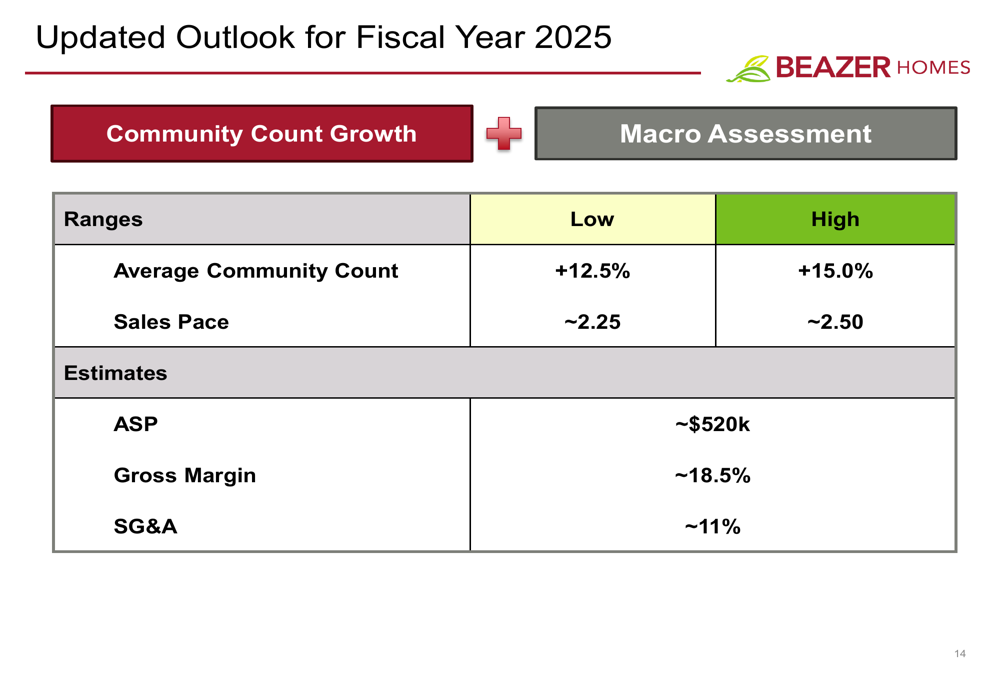

Looking at the full fiscal year 2025, Beazer updated its outlook based on community count growth and macroeconomic assessment:

The company expects average community count growth between 12.5% and 15.0%, with sales pace ranging from approximately 2.25 to 2.50 homes per community per month. Average selling price is projected at approximately $520,000, with gross margin around 18.5% and SG&A at approximately 11% of revenue.

Financial Position

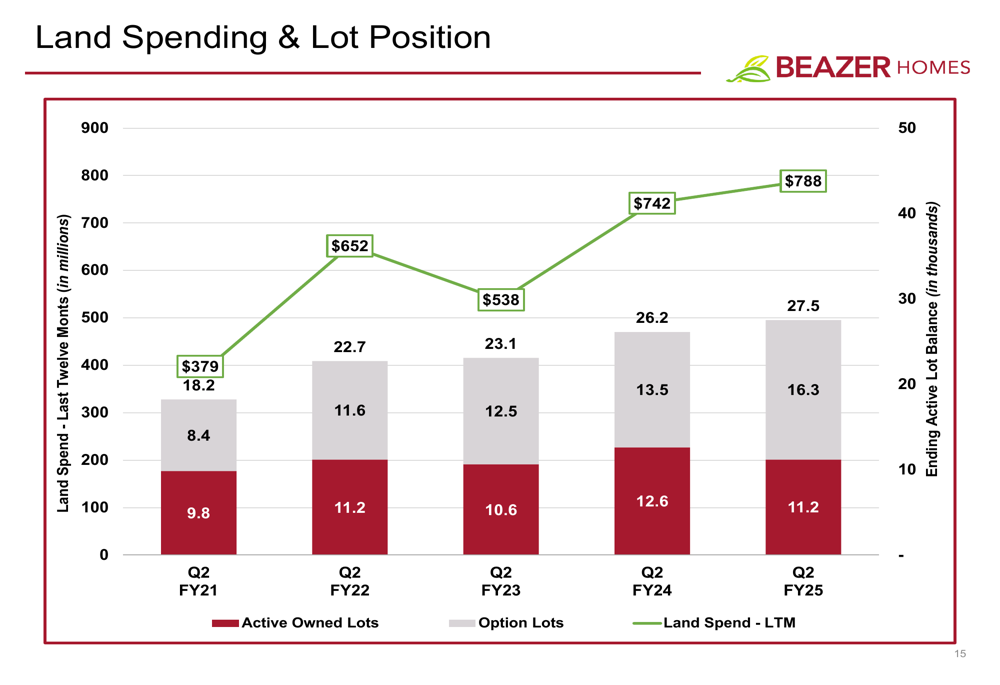

Beazer’s land investment strategy continues to support future growth, with land spending increasing to $788 million for the last twelve months ending Q2 FY25, up from $742 million in the comparable prior period. The company has shifted its lot acquisition strategy toward options, with option lots increasing to 16,300 from 13,500 a year ago.

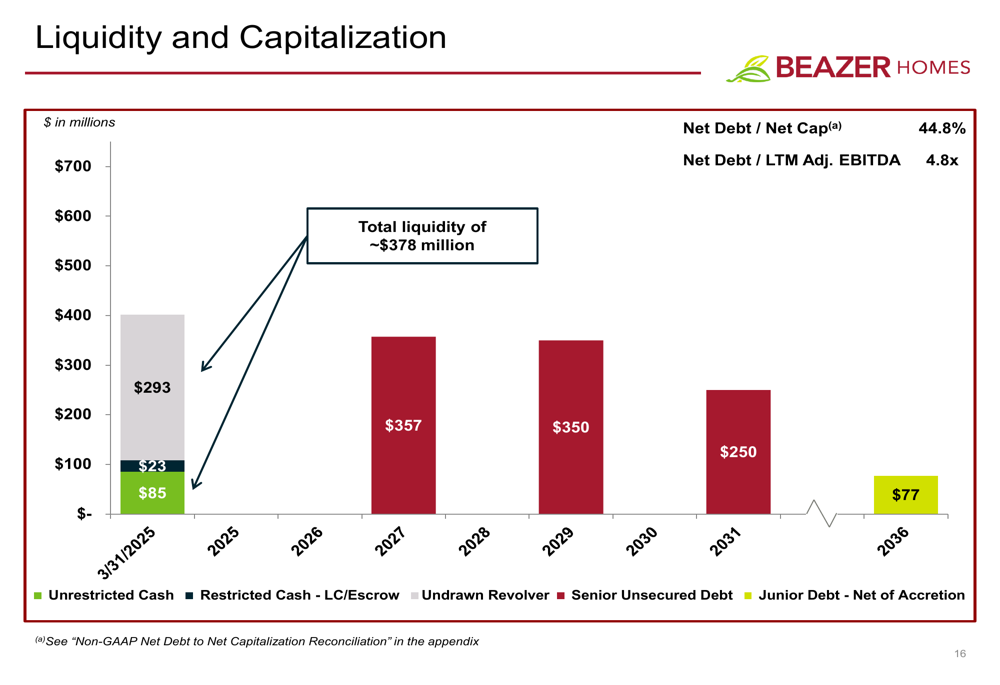

The company’s liquidity position remains solid with approximately $378 million in total liquidity as of March 31, 2025. However, leverage metrics have increased, with net debt to net capitalization at 44.8% and net debt to LTM adjusted EBITDA at 4.8x.

Beazer aims to reduce its net debt to net capitalization ratio to the low 30% range by fiscal year-end 2027, primarily through retained earnings and profitability improvement.

Conclusion

Beazer Homes’ Q2 FY25 results reflect the ongoing challenges in the housing market, with affordability constraints and higher mortgage rates continuing to pressure demand and margins. While the company has made progress on community count growth and its Zero Energy Ready homes initiative, the significant declines in orders, margins, and profitability highlight the difficult operating environment.

Management remains focused on its long-term strategic goals while navigating near-term headwinds. Investors will be watching closely to see if Beazer can deliver on its Q3 expectations and make progress toward its multi-year targets in a housing market that continues to face affordability challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.