Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

Beazer Homes USA Inc (NYSE:BZH) presented its third-quarter fiscal 2025 results on July 31, revealing a company navigating a challenging housing market while maintaining focus on its long-term growth strategy. The homebuilder reported mixed results, with declining orders and closings offset by community count growth and continued progress on strategic initiatives.

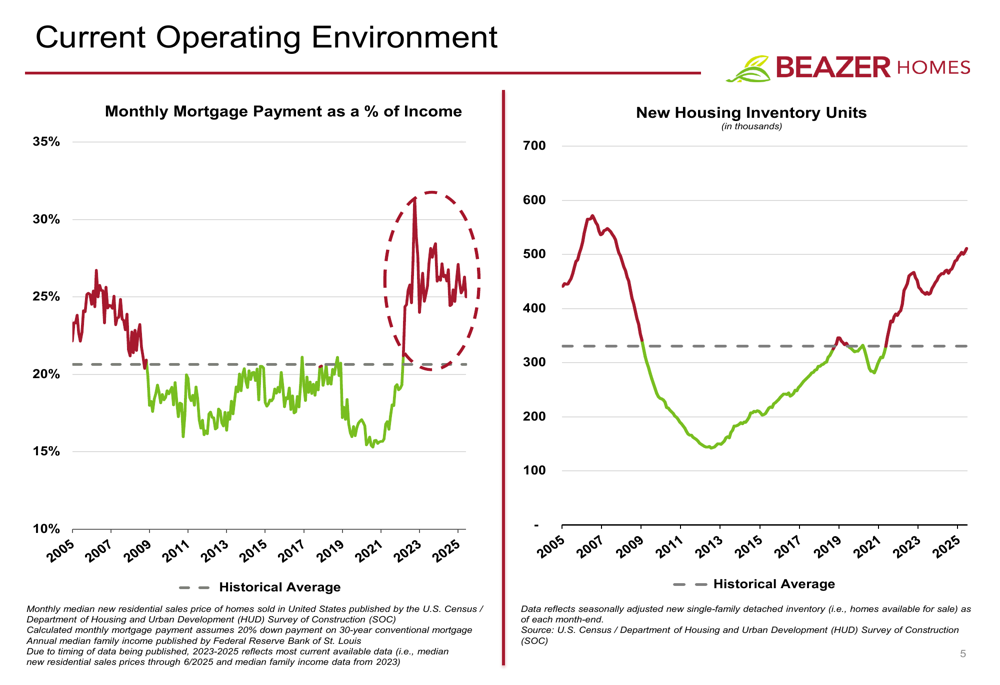

The current operating environment presents significant challenges for homebuilders, with mortgage affordability stretched beyond historical norms and inventory levels gradually rising from previously low levels.

As shown in the following chart of mortgage affordability and housing inventory trends:

Quarterly Performance Highlights

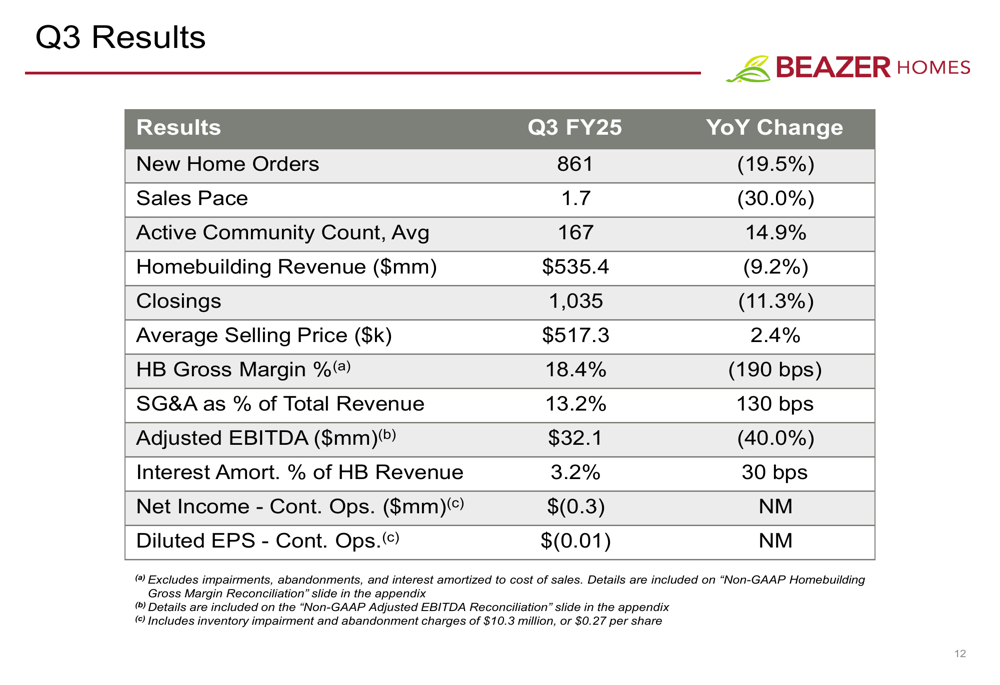

Beazer’s Q3 FY25 results reflected the difficult market conditions, with several key metrics declining year-over-year. New home orders fell 19.5% to 861, while the sales pace dropped 30% to 1.7 homes per community per month. Homebuilding revenue decreased 9.2% to $535.4 million, with closings down 11.3% to 1,035 homes.

Despite these challenges, the company highlighted several positive developments, including community count growth, book value per share growth, and gross margin increases. Beazer also continued its share repurchase program, buying back over $12 million of stock during the quarter and bringing the year-to-date total to $33 million.

The comprehensive Q3 results are detailed in the following table:

The company’s average selling price increased 2.4% to $517,300, providing some offset to the decline in closing volume. However, homebuilding gross margin decreased 190 basis points to 18.4%, while SG&A as a percentage of total revenue increased 130 basis points to 13.2%. Adjusted EBITDA fell 40% to $32.1 million.

Notably, Beazer recorded inventory impairment and abandonment charges of $10.3 million ($0.27 per share), resulting in a net loss from continuing operations of $0.3 million or $0.01 per diluted share. This contrasts with the earnings article reporting an EPS of $0.88, suggesting the article referenced non-GAAP adjusted figures that excluded these impairment charges.

Strategic Initiatives

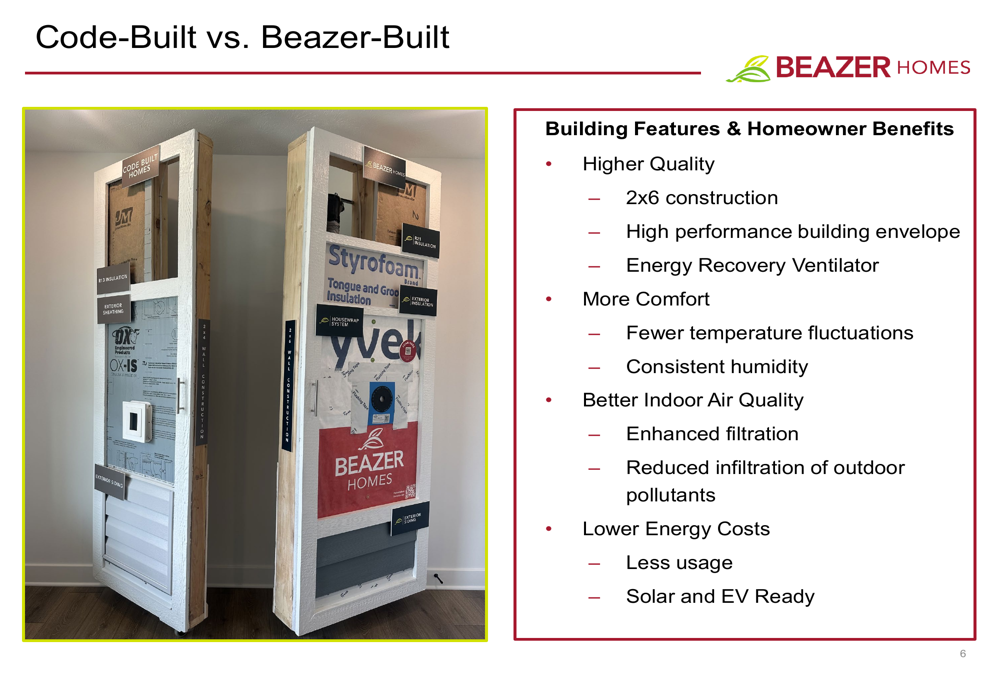

Beazer continues to differentiate itself through its focus on energy-efficient construction and quality. The company positions itself as "America’s #1 Energy-Efficient Homebuilder" and highlights the superior construction methods used in its homes compared to industry standards.

The following image illustrates Beazer’s construction quality differentiation:

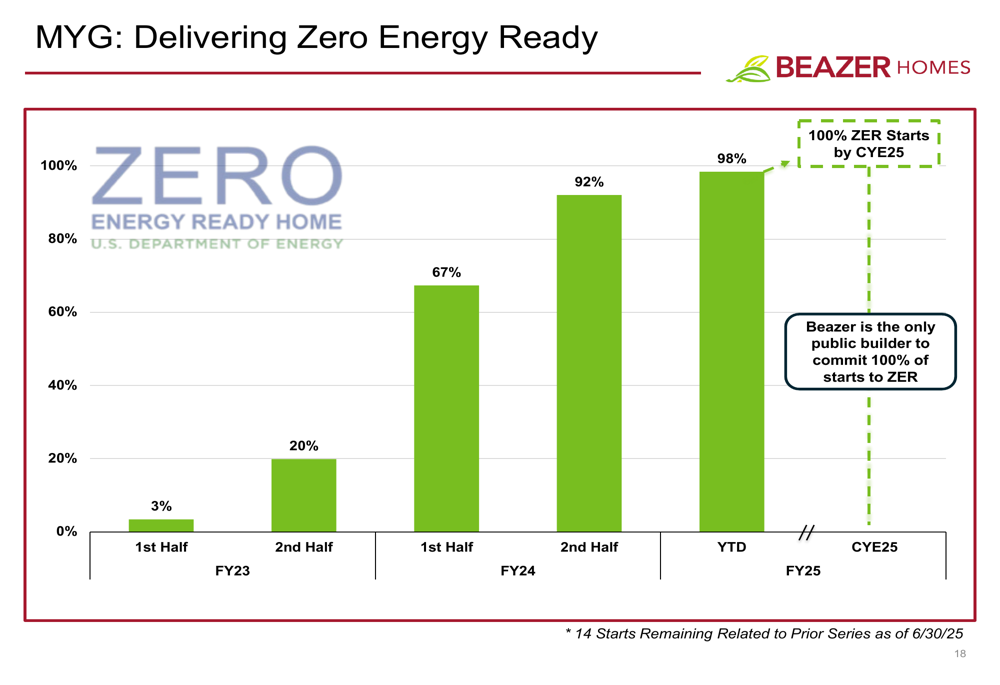

A cornerstone of Beazer’s strategy is its commitment to Zero Energy Ready (ZER) homes. The company has made remarkable progress in this area, increasing the percentage of ZER starts from just 3% in the first half of FY23 to 98% in YTD FY25, with a goal of reaching 100% by calendar year-end 2025.

As shown in this chart tracking the company’s progress toward 100% Zero Energy Ready homes:

Beazer claims to be the only public homebuilder committed to making 100% of its homes Zero Energy Ready, which provides a clear differentiation point in the competitive landscape.

Forward-Looking Statements

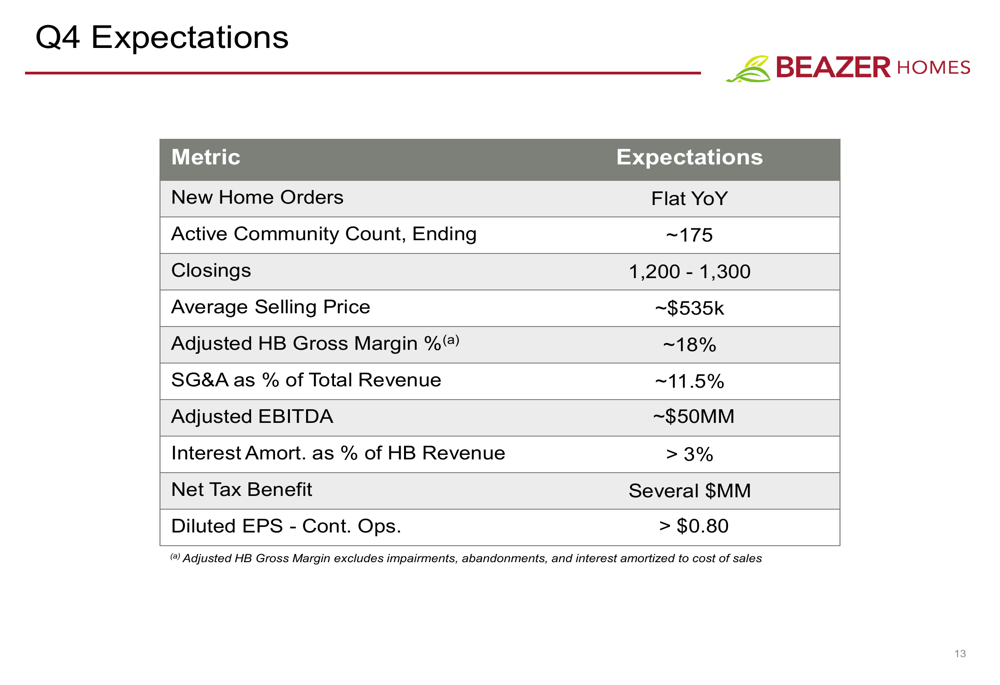

For the fourth quarter of fiscal 2025, Beazer expects new home orders to be flat year-over-year, with closings projected between 1,200 and 1,300 units at an average selling price of approximately $535,000. The company anticipates an adjusted homebuilding gross margin of about 18% and SG&A as a percentage of total revenue of approximately 11.5%.

The detailed Q4 expectations are outlined in the following table:

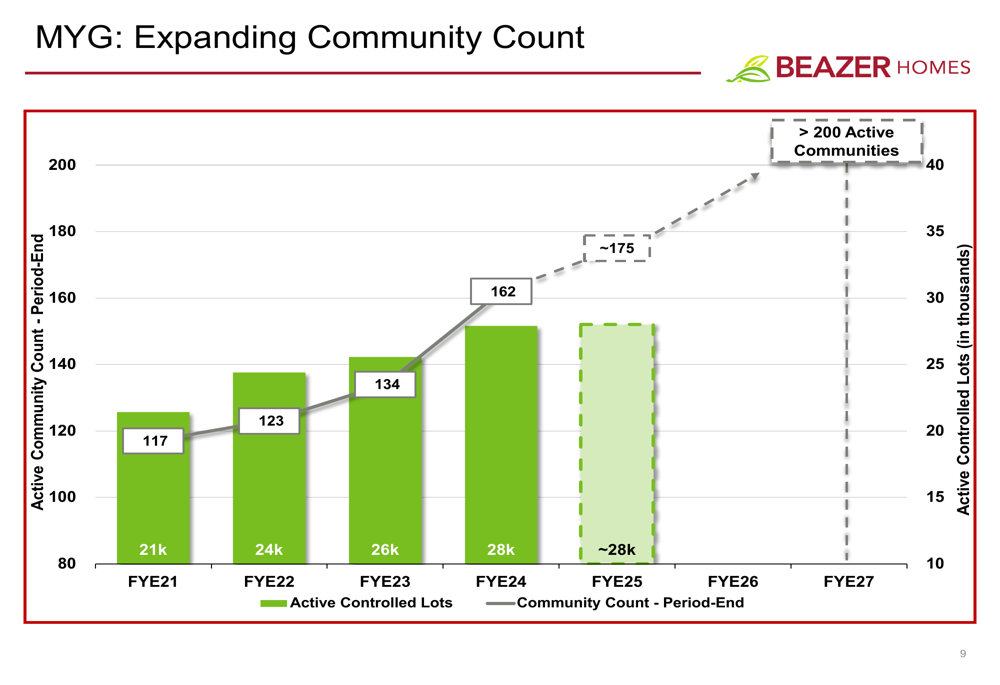

Looking beyond the current fiscal year, Beazer has established multi-year goals through fiscal 2027, including expanding its community count to over 200, reducing net debt to net capitalization to the low 30% range, and achieving double-digit compound annual growth in book value per share.

The company’s community count expansion strategy is illustrated in this chart:

Competitive Industry Position

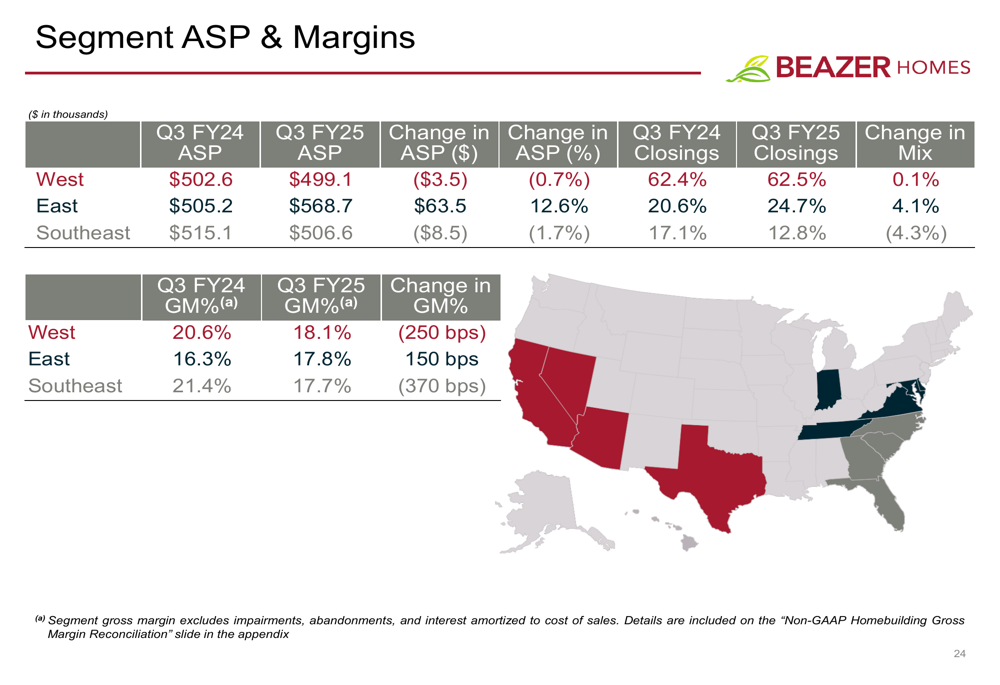

Beazer’s regional performance varied significantly across its operating areas. The following table provides a breakdown of average selling prices and margins by segment:

The East region showed the strongest performance with price increases, while the West and Southeast regions experienced price declines. This regional variation reflects different market dynamics and competitive pressures across the country.

Beazer is actively managing its land portfolio to enhance returns on capital through asset structuring and community positioning. The company has increased its percentage of optioned lots to 60% of active controlled lots, up from 55% a year ago, providing greater flexibility in land management.

Balance Sheet and Liquidity

As of June 30, 2025, Beazer reported total liquidity of approximately $292 million, including $83 million in unrestricted cash. The company’s net debt to net capitalization ratio stood at 46.6%, with a goal of reducing this to the low 30% range by fiscal 2027.

Land spend for fiscal 2025 is expected to be between $700 million and $750 million, supporting the company’s community count growth strategy. Beazer’s focus on increasing the percentage of optioned lots versus owned lots provides greater flexibility in managing capital allocation.

In conclusion, while Beazer Homes faces near-term challenges from the difficult housing market, the company continues to execute on its long-term strategy of community count growth, balance sheet improvement, and differentiation through energy-efficient construction. The stock closed at $23.42 following the earnings release, showing a modest 0.34% increase in the aftermarket session, suggesting investors are balancing the mixed quarterly results against the company’s longer-term strategic positioning.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.