Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

BetMakers Technology Group Ltd (ASX:BET) released its Q4 FY25 update on July 22, 2025, showcasing significant improvements in financial performance as the company’s transformation strategy continues to deliver results. The global racing technology solutions provider saw its stock trading at $0.1 on July 21, down 4.76% ahead of the quarterly update, with shares having traded in a 52-week range of $0.076 to $0.135.

The company positions itself as the global market leader for racing technology solutions, with an extensive network spanning over 30 countries and partnerships with more than 230 racing organizations worldwide.

Quarterly Performance Highlights

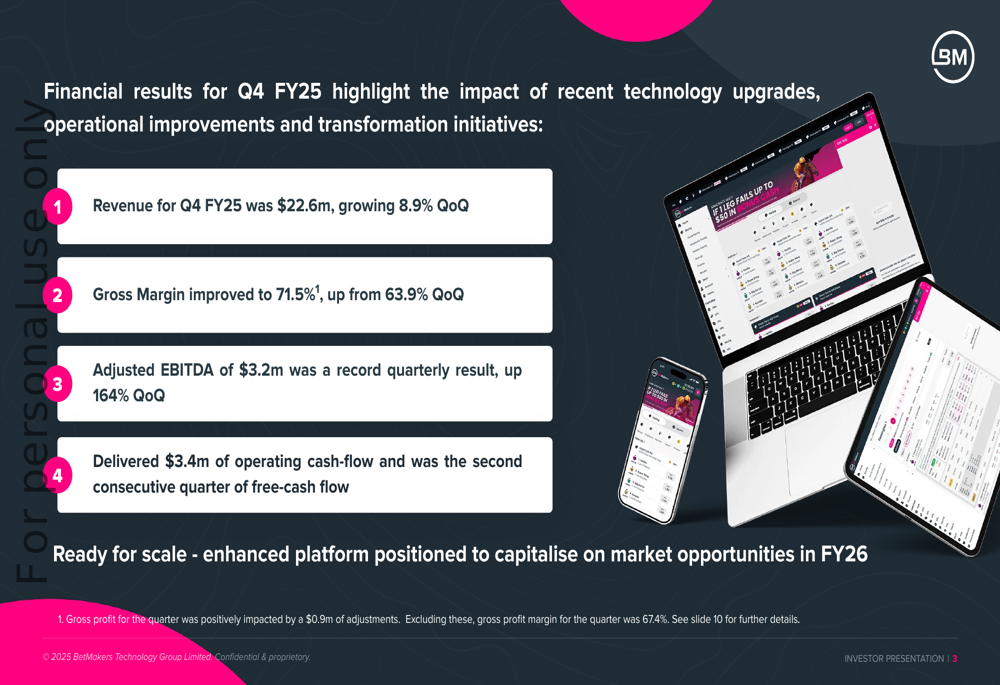

BetMakers reported Q4 FY25 revenue of $22.6 million, representing an 8.9% increase quarter-over-quarter. More impressively, the company achieved a record quarterly Adjusted EBITDA of $3.2 million, up 164% from the previous quarter. This marks a significant milestone in the company’s journey toward sustainable profitability.

As shown in the following chart of quarterly financial results:

Gross margin improved substantially to 71.5%, up from 63.9% in the previous quarter. However, it’s worth noting that this figure includes a $0.9 million positive adjustment; excluding this impact, the adjusted gross margin would be 67.4%, which still represents a notable improvement over previous quarters.

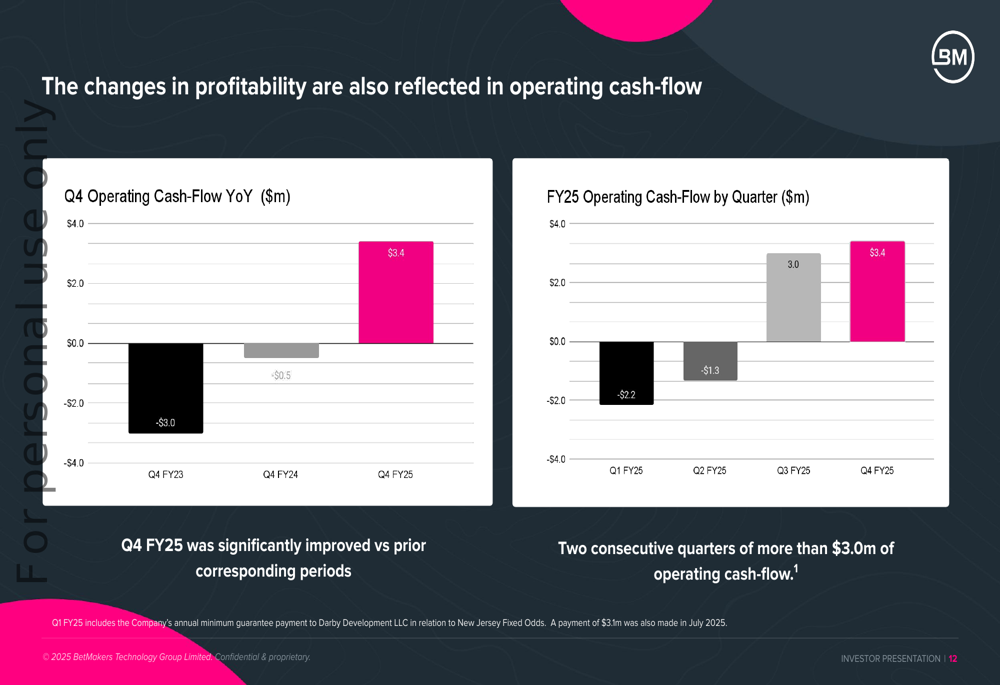

The company also delivered $3.4 million in operating cash flow, marking the second consecutive quarter of positive free cash flow. This trend demonstrates BetMakers’ improving financial health and operational efficiency.

Financial Transformation Journey

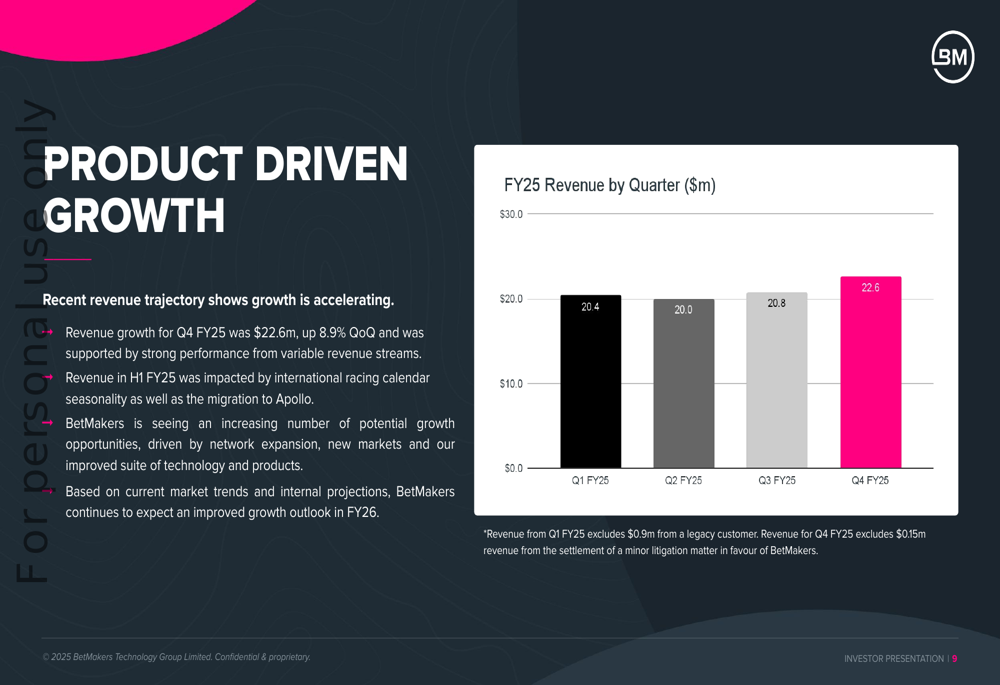

BetMakers’ quarterly results reflect a remarkable financial transformation over the past two years. The company has steadily improved its revenue performance throughout FY25, with quarterly revenue increasing from $20.4 million in Q1 to $22.6 million in Q4.

The following chart illustrates this consistent revenue growth pattern:

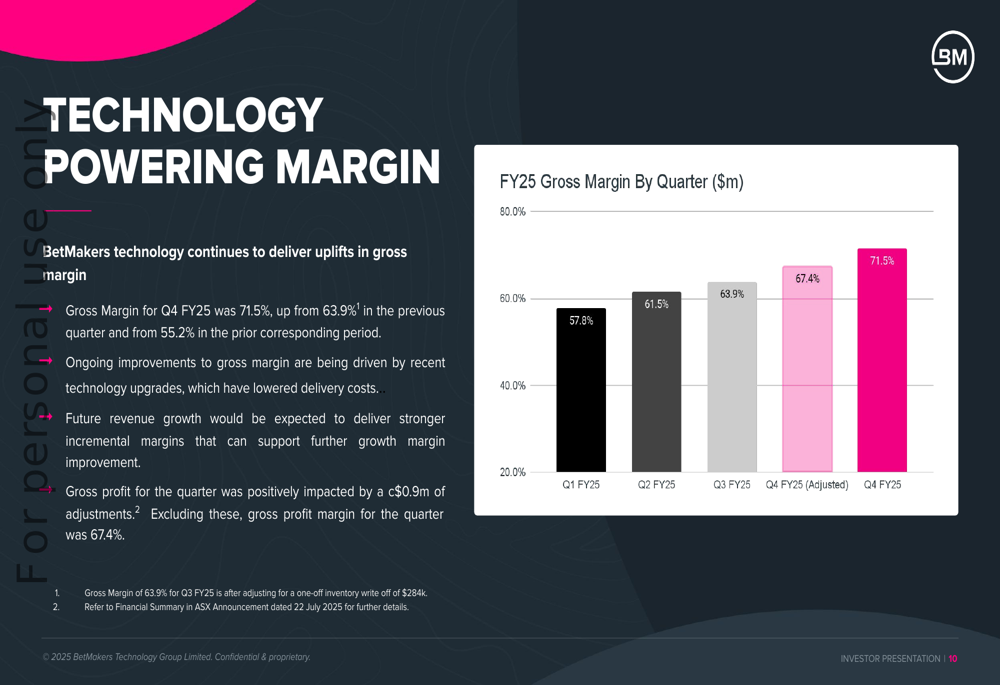

Even more impressive has been the company’s margin expansion. Gross margins have improved sequentially each quarter, from 57.8% in Q1 FY25 to 71.5% in Q4 FY25. This improvement reflects the company’s focus on technology-driven efficiency and scale.

The margin improvement trajectory is clearly visible in this chart:

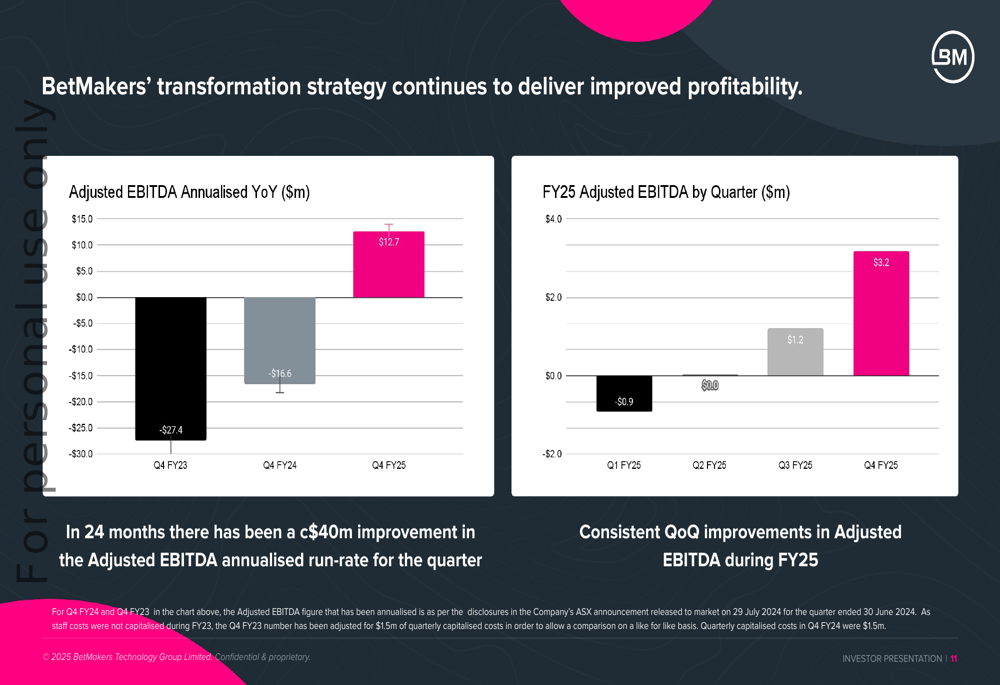

Perhaps the most dramatic aspect of BetMakers’ transformation is the turnaround in profitability. The company has achieved a remarkable improvement in its Adjusted EBITDA, moving from an annualized rate of -$27.4 million in Q4 FY23 to $12.7 million in Q4 FY25 – representing approximately $40 million in improvement over 24 months.

The quarterly progression of Adjusted EBITDA throughout FY25 shows this acceleration toward profitability:

This profitability improvement has translated into positive operating cash flow, with the company generating $3.4 million in Q4 FY25, compared to -$0.5 million in Q4 FY24 and -$3.0 million in Q4 FY23.

The following chart demonstrates this cash flow transformation:

Competitive Industry Position

BetMakers has established a differentiated position in the global racing technology market through its comprehensive product portfolio. The company claims that no global competitor offers a full-service horse racing product offering for both Tote and Fixed Odds betting.

The company’s competitive advantage is built on six core platform components: Integrations and Relationships, Regulations and Integrity, Content and Data, Proprietary & Innovative Technology, Network Effects, and a Modular Platform.

BetMakers’ extensive global network includes 65+ online wagering operators, 45+ regulatory licenses, 30+ active countries, and 230+ racing partners. This global footprint provides a strong foundation for future growth and expansion.

The company’s product portfolio comparison against peers demonstrates its comprehensive offering:

Strategic Initiatives

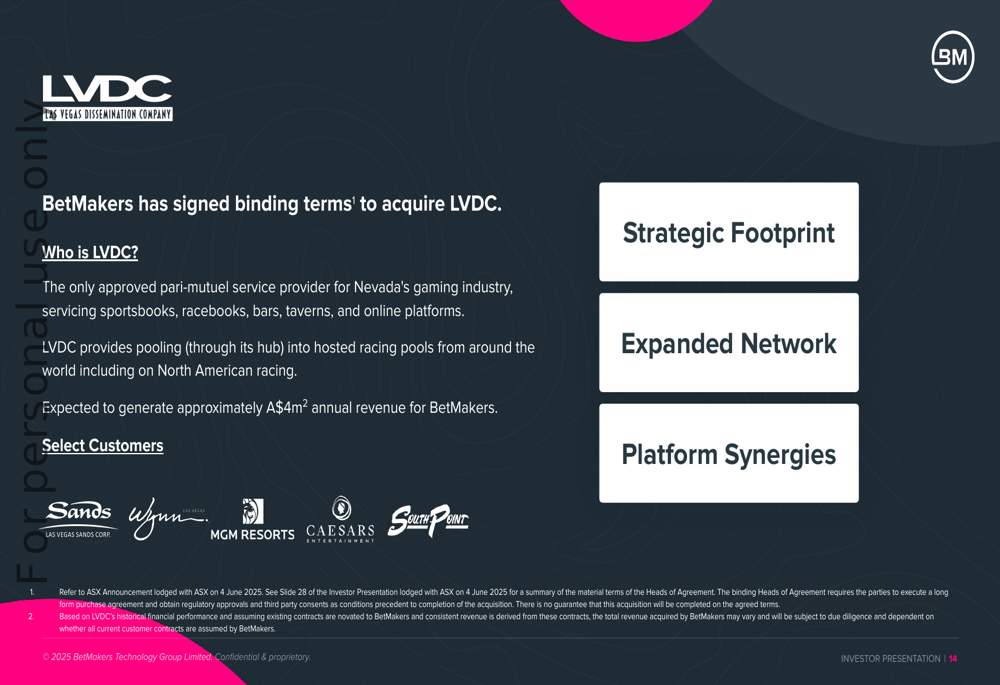

A key strategic development highlighted in the presentation is BetMakers’ acquisition of Las Vegas Dissemination Company (LVDC), the only approved pari-mutuel service provider for Nevada’s gaming industry. This acquisition is expected to generate approximately A$4 million in revenue and strengthen BetMakers’ presence in the critical US market.

The LVDC acquisition brings relationships with major casino operators including Las Vegas Sands (NYSE:LVS) Corp., Wynn Resorts (NASDAQ:WYNN), MGM Resorts (NYSE:MGM), Caesars (NASDAQ:CZR) Entertainment, and South Point. These relationships provide significant opportunities for cross-selling and upselling BetMakers’ broader product portfolio.

The strategic rationale and benefits of the LVDC acquisition are outlined here:

BetMakers expects the LVDC transaction to be cash flow positive within 12 months, with opportunities to monetize these customer relationships and the Las Vegas footprint through content expansion and product synergies.

Forward-Looking Statements

Looking ahead, BetMakers describes itself as "Ready for scale - enhanced platform positioned to capitalise on market opportunities in FY26." The company sees significant opportunities to upgrade existing clients along its value chain, potentially increasing revenue per client as they adopt more of BetMakers’ services.

Recent contract wins in major global markets are expected to provide additional growth opportunities. The company also anticipates that the LVDC acquisition will strengthen its US market position and provide a platform for further expansion in this key region.

With two consecutive quarters of positive operating cash flow and a record quarterly Adjusted EBITDA result, BetMakers appears well-positioned to continue its financial transformation and capitalize on its global market position in racing technology solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.