Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

BioAtla Inc. (NASDAQ:BCAB), a clinical-stage biotech company focused on developing Conditionally Active Biologics (CABs) for cancer treatment, presented its latest corporate update on August 7, 2025. Despite showing promising clinical data across multiple programs, the company continues to face significant financial challenges, with its stock closing at $0.38 and showing minimal movement in premarket trading.

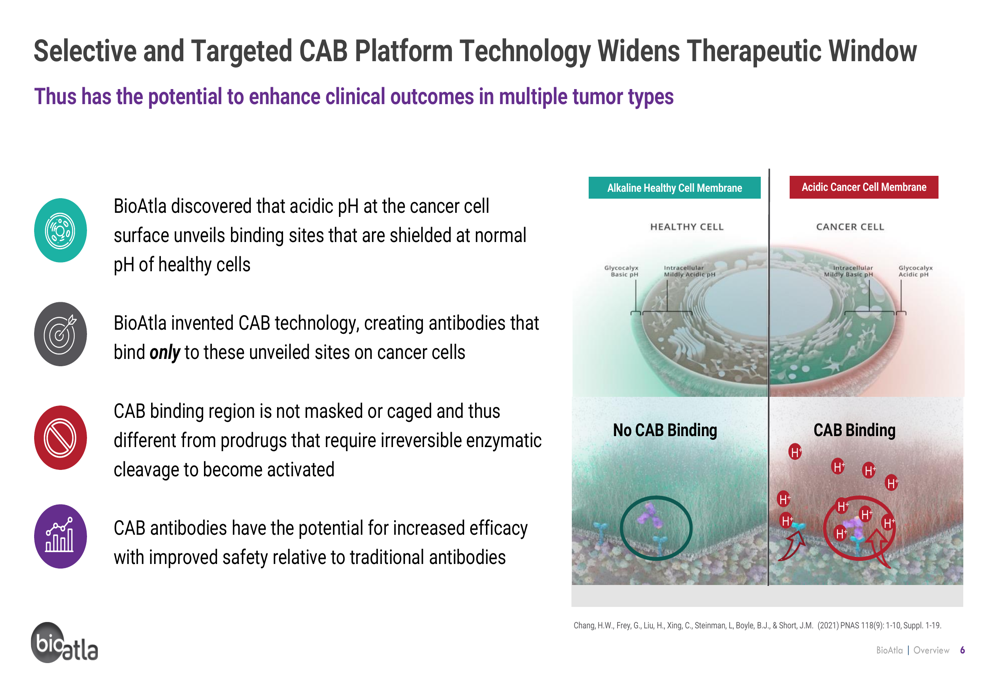

The company’s innovative CAB platform technology differentiates itself through pH-selective binding that targets the acidic tumor microenvironment, potentially improving efficacy while reducing toxicity compared to conventional antibody therapies. With over 500 issued patents, BioAtla’s proprietary technology aims to address limitations of current cancer treatments.

As shown in the following illustration of the CAB platform technology, BioAtla’s approach leverages the acidic environment of cancer cells to enable selective binding:

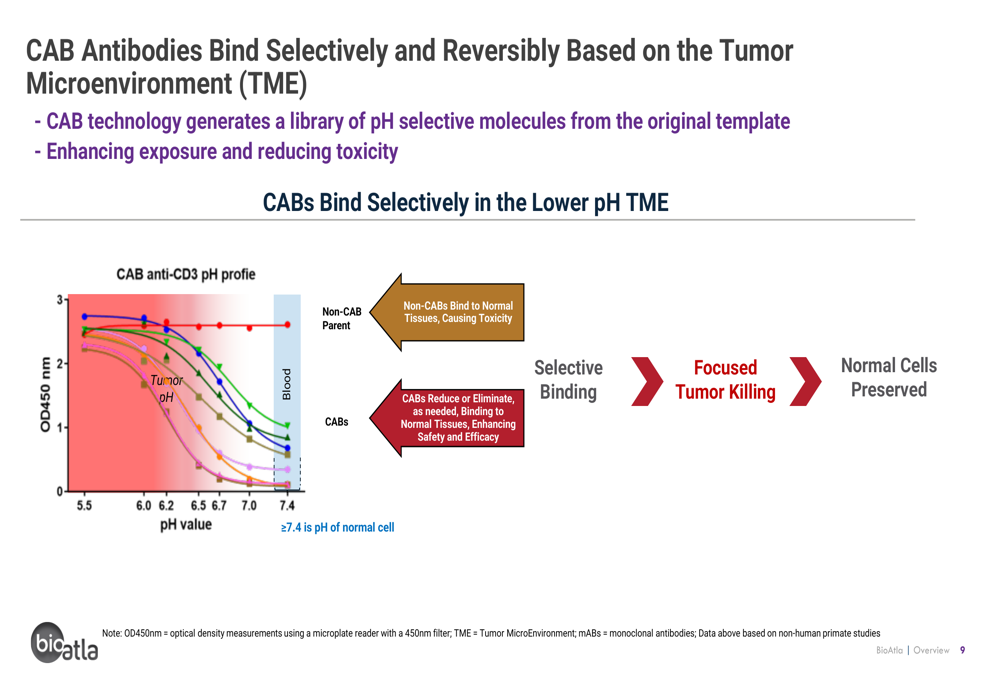

This selective binding mechanism is further demonstrated in the following visualization, showing how CAB antibodies bind selectively and reversibly based on tumor microenvironment pH:

Recent Financial Performance

BioAtla reported better-than-expected financial results in Q1 2025, with an EPS of -$0.26 beating the forecast of -$0.39. This improvement was driven by significant cost reductions, with R&D expenses decreasing to $12.4 million from $18.9 million year-over-year, and G&A expenses slightly declining to $5.3 million from $5.6 million.

Despite these improvements, the company’s stock has plummeted 74.87% over the past six months, with a current market capitalization of just $27.7 million. The disconnect between promising clinical data and market performance highlights investor concerns about the company’s long-term financial sustainability and competitive positioning.

As of March 31, 2025, BioAtla reported cash and cash equivalents of $32.4 million, though the August presentation did not provide an updated cash position, raising questions about the company’s current runway.

Clinical Program Highlights

BioAtla’s presentation highlighted progress across multiple clinical programs, with particular focus on three key candidates: BA3182, Mecbotamab vedotin, and Ozuriftamab vedotin.

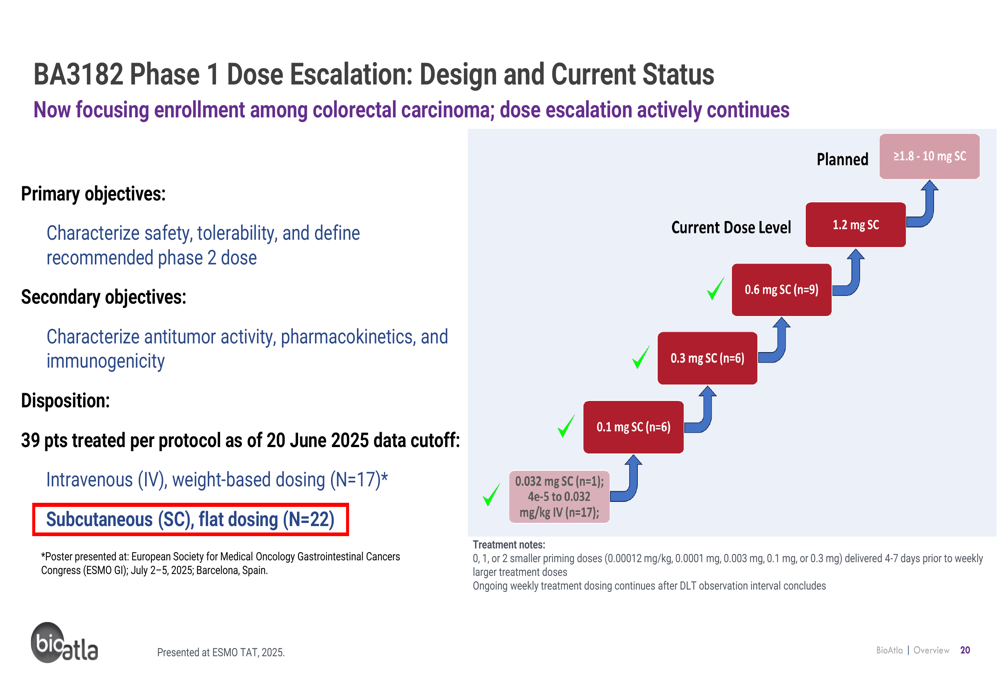

BA3182, a dual conditionally active biologic targeting EpCAM and CD3, is showing promising early results in adenocarcinomas. The Phase 1 dose escalation study has enrolled 39 patients as of June 20, 2025, with generally manageable adverse events and evidence of tumor reduction across multiple cancer types.

The following chart illustrates the BA3182 Phase 1 dose escalation design and current status:

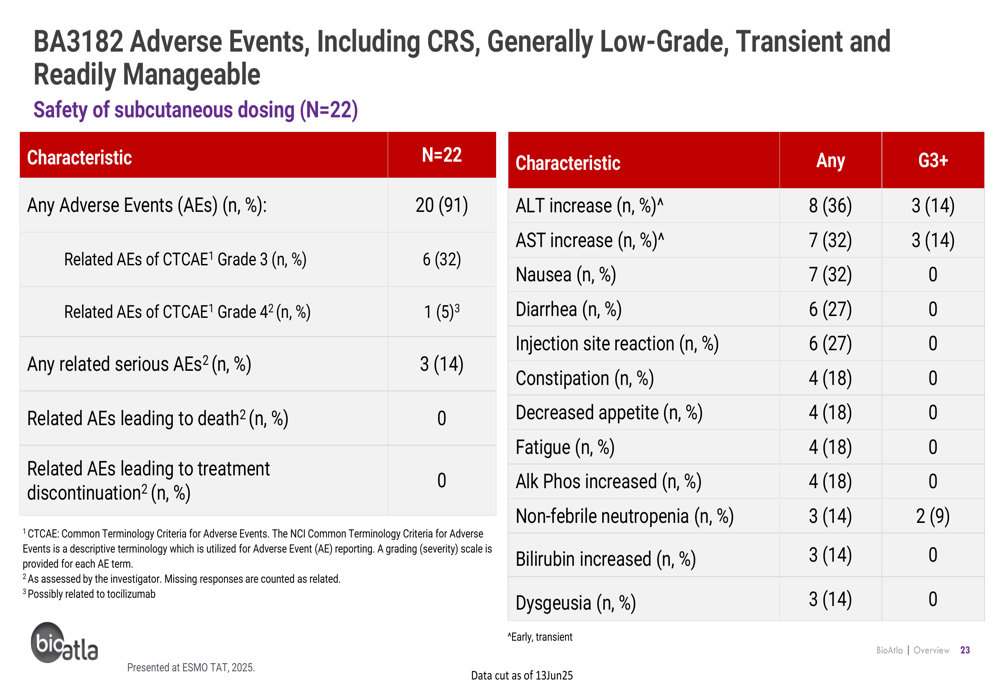

Safety data for BA3182 indicates that related adverse events were generally low-grade, transient, and readily manageable, with no treatment-related deaths reported:

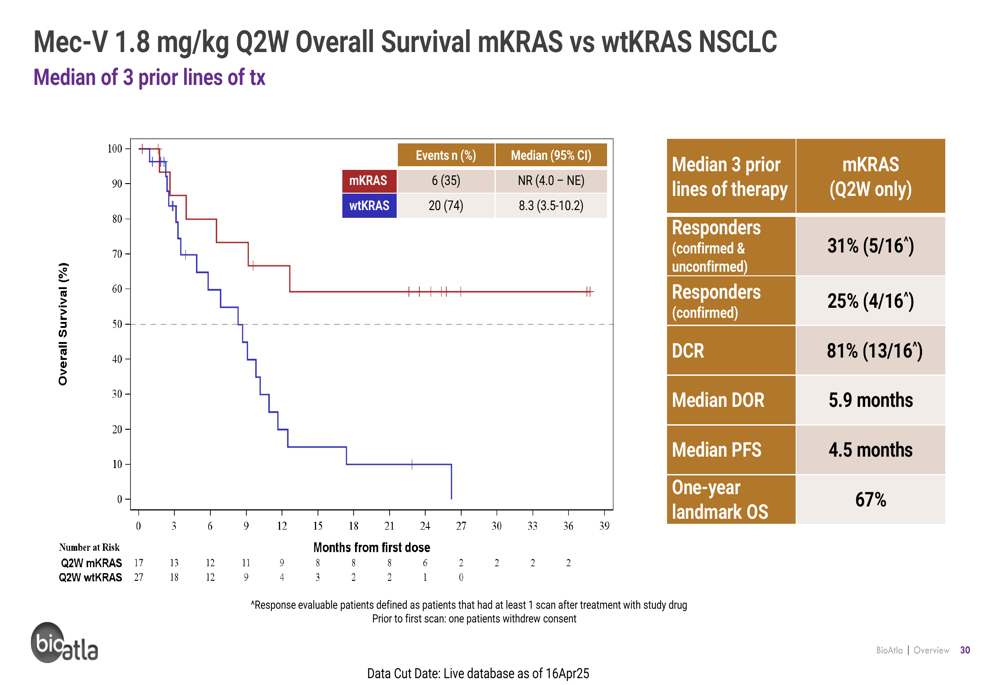

Mecbotamab vedotin (Mec-V), a CAB-AXL-ADC, has demonstrated particularly impressive survival data in mutated KRAS (mKRAS) non-small cell lung cancer (NSCLC). The following Kaplan-Meier curve shows overall survival comparing mKRAS and wild-type KRAS patients:

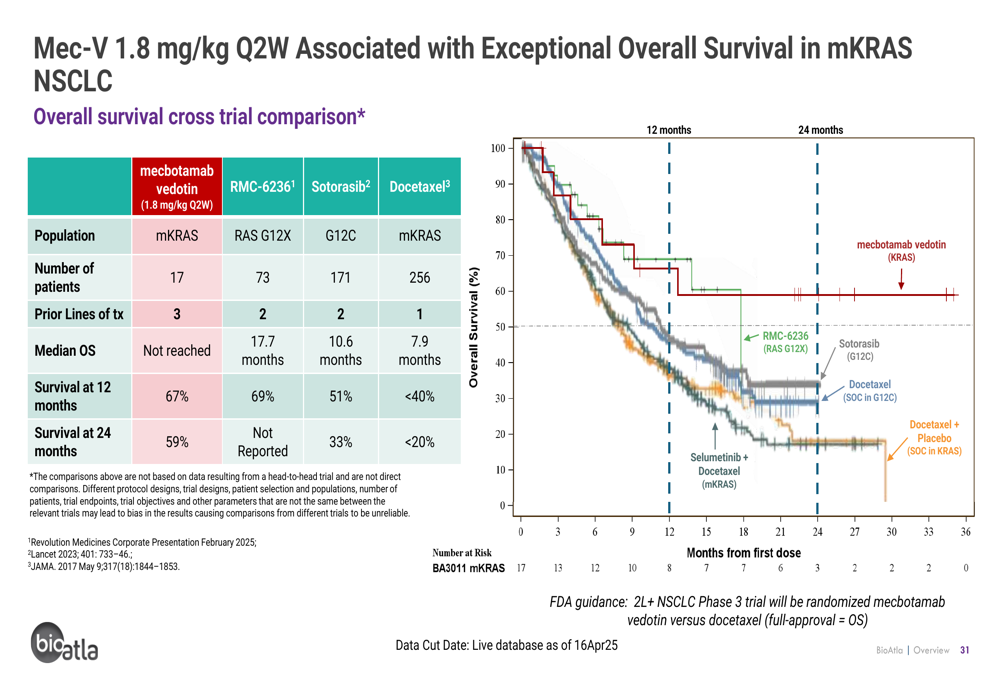

When compared to other treatments for mKRAS NSCLC, Mec-V shows competitive or superior survival rates, as illustrated in this comparative analysis:

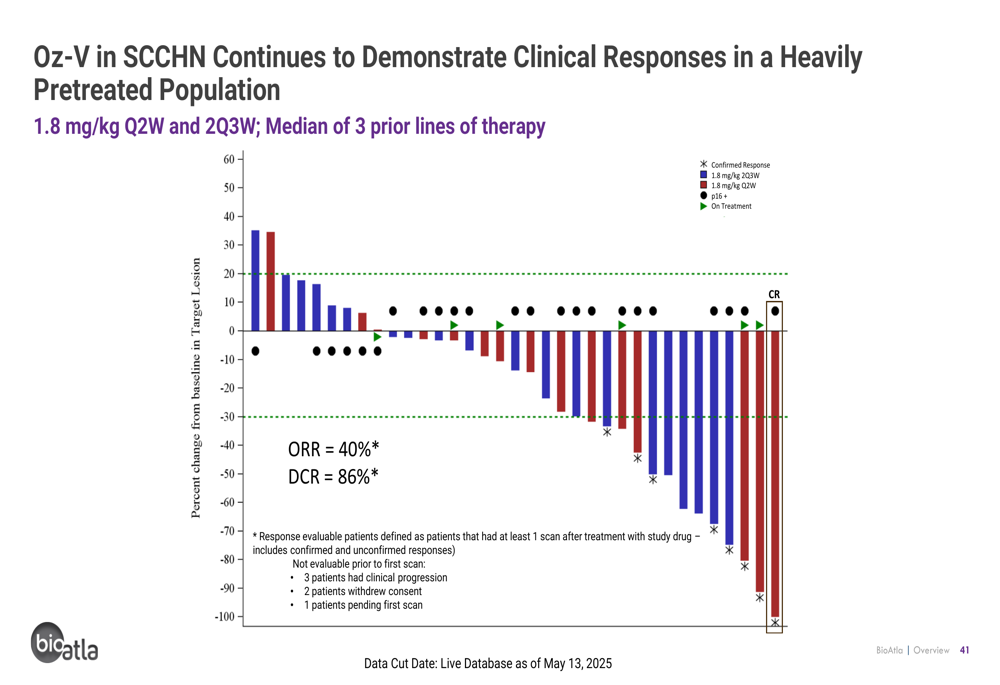

Ozuriftamab vedotin (Oz-V), a CAB-ROR2-ADC targeting HPV-positive oropharyngeal squamous cell carcinoma (OPSCC), has also shown encouraging clinical responses in heavily pretreated patients:

Strategic Initiatives & Future Catalysts

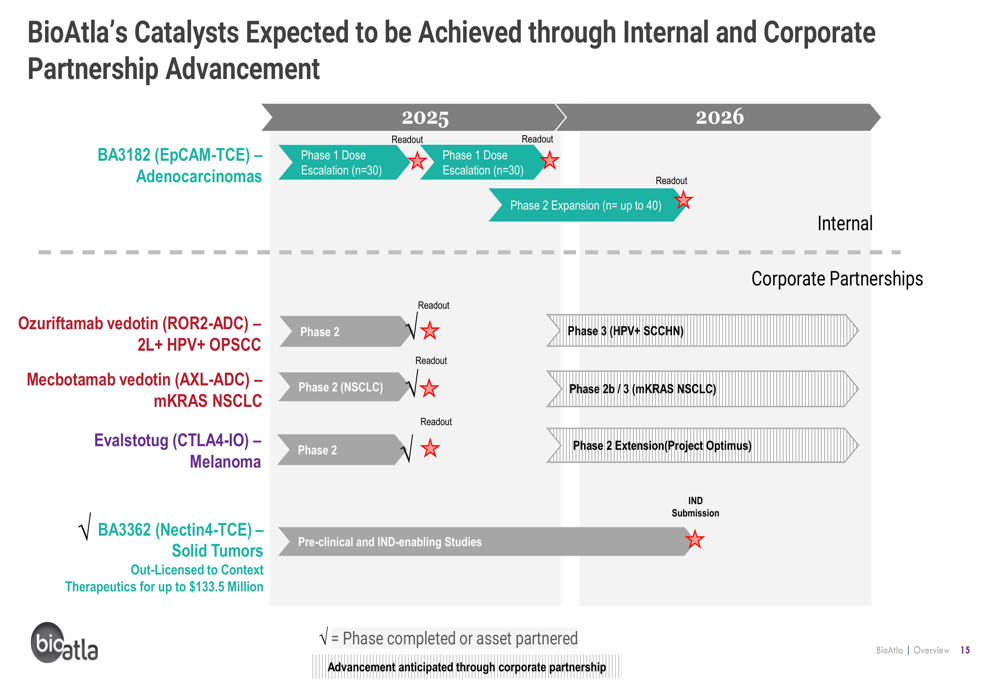

BioAtla’s presentation outlined several upcoming catalysts and milestones across its pipeline, providing a roadmap for potential value-creating events through 2026:

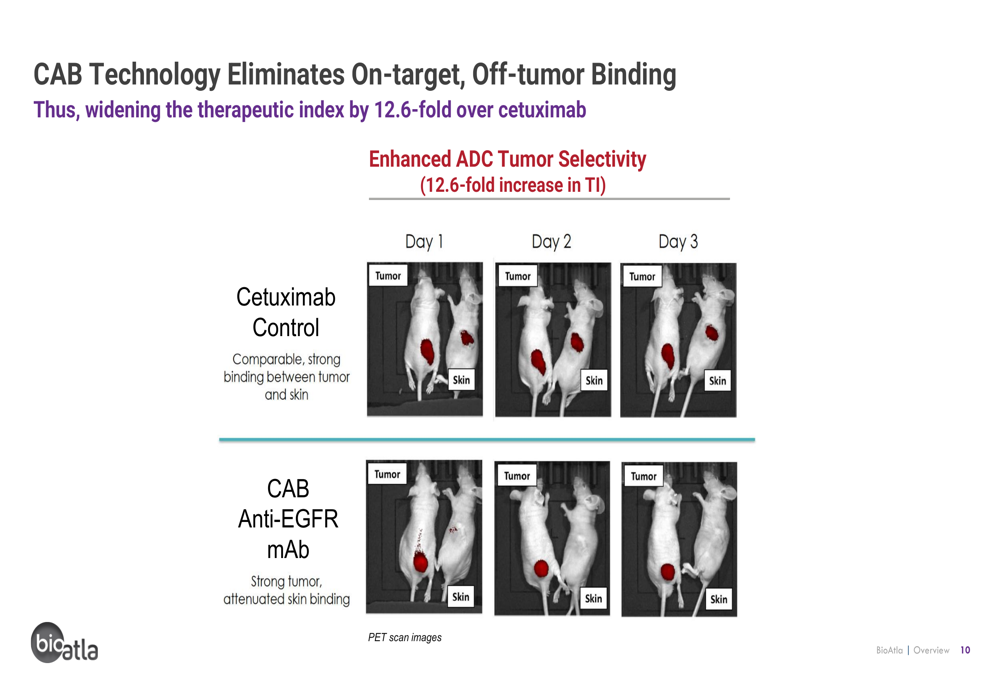

The company is positioning its CAB platform as having key advantages over conventional antibody approaches and prodrugs, including conditional and reversible binding that increases efficacy while improving safety. This technology enables BioAtla to target previously "undruggable" cancer targets due to toxicity concerns.

One compelling demonstration of this advantage is shown in the following PET scan comparison, illustrating how CAB technology eliminates off-tumor binding:

Competitive Positioning & Market Opportunities

BioAtla is targeting significant market opportunities with its lead programs. For Mecbotamab vedotin, the company is focusing on mKRAS NSCLC, which represents approximately 30% of all NSCLC patients. The presentation highlighted competitive response rates compared to other treatments in this indication.

For Ozuriftamab vedotin, BioAtla is positioning the drug as potentially the first approved treatment specifically for HPV+ OPSCC, with an estimated worldwide market value of approximately $1 billion. The company also noted potential expansion into other HPV+ solid tumors, representing a market valued at over $7 billion.

However, as noted in the recent earnings call, BioAtla faces significant competitive pressures, particularly from new KRAS inhibitors entering the market.

Outlook & Challenges

While BioAtla’s clinical data appears promising, the company faces several challenges that may explain its struggling stock performance. Continued net losses and cash burn remain concerns, with the company’s financial outlook suggesting ongoing losses through 2025. Forward EPS forecasts project -$0.23 for Q2 2025 and -$1.13 for FY2025.

During the recent earnings call, CEO Dr. Jay Short emphasized patient outcomes, stating, "We continue to observe multiple patients achieving tumor reduction and tolerating the therapy over many months without progression." Chief Medical (TASE:BLWV) Officer Dr. Eric Sievers added, "Overall survival is the bottom line here," highlighting the company’s focus on meaningful clinical endpoints.

The company’s strategy appears focused on advancing its clinical programs while pursuing cost reduction initiatives and potential partnerships. However, investors will likely need to see more definitive clinical success and a clearer path to commercialization before regaining confidence in BioAtla’s long-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.