Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

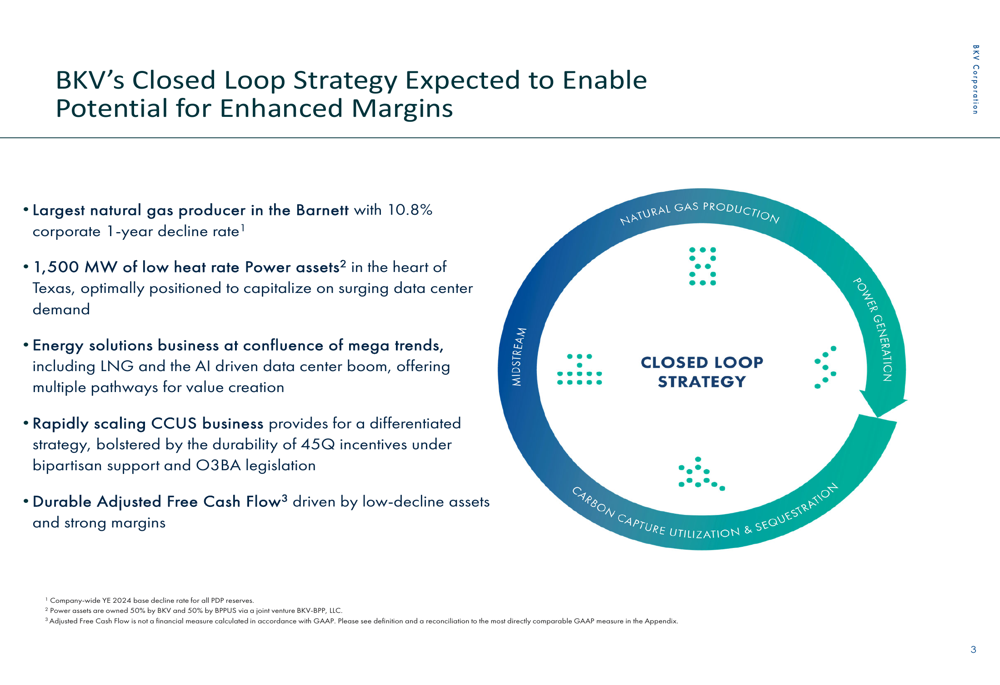

BKV Corporation (NYSE:BKV) presented its Q2 2025 results on August 12, highlighting strong performance across its vertically integrated energy operations. The company, which has seen its stock rise to $20.12 following an 8% surge after Q1 earnings, continues to execute its "Closed Loop Strategy" combining natural gas production, power generation, and carbon capture.

The presentation comes amid growing demand in the ERCOT power market and increasing focus on low-carbon energy solutions. BKV’s strategic positioning in these areas appears to be paying dividends, with particularly strong results from its power joint venture exceeding guidance.

As shown in the following illustration of BKV’s integrated business model:

Quarterly Performance Highlights

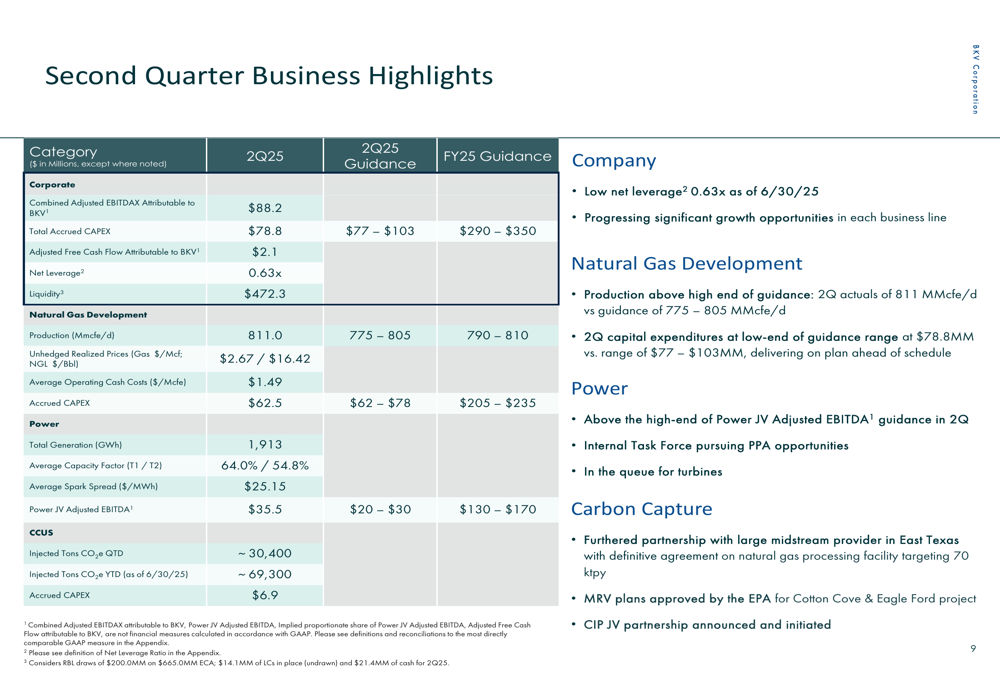

BKV reported solid Q2 2025 results across all business segments. The company achieved a Combined Adjusted EBITDAX of $88.2 million, with total accrued capital expenditures of $78.8 million, within the guided range of $77-103 million.

Natural gas production reached 811 MMcfe/d, exceeding expectations due to strong base decline management and outperformance from new wells. The power segment was particularly impressive, with total generation of 1,913 GWh and Power JV Adjusted EBITDA of $35.5 million, significantly outperforming the guidance range of $20-30 million.

The company’s carbon capture business continues to scale, with approximately 69,300 tons of CO₂ injected year-to-date through its operational projects.

The following summary highlights key Q2 2025 metrics across BKV’s business units:

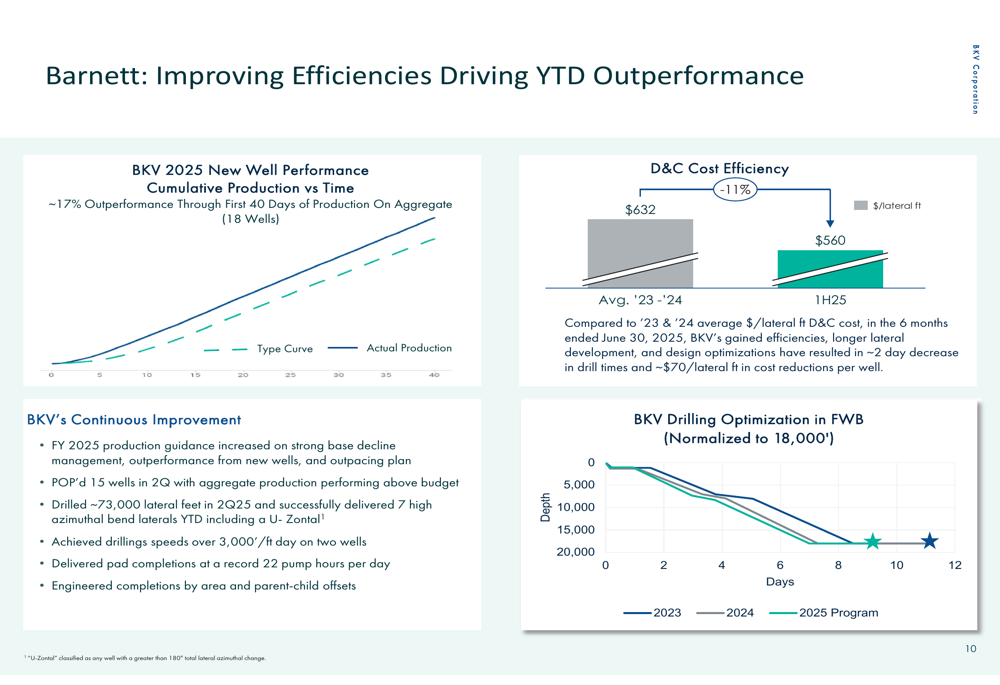

BKV’s Barnett operations have shown notable efficiency improvements, with new well performance outpacing type curves by 17%. Drilling and completion costs have decreased from $632 per lateral foot in 2023-2024 to $560 per lateral foot in the first half of 2025, demonstrating the company’s focus on operational excellence.

As illustrated in this performance chart showing actual production versus type curve expectations:

Strategic Initiatives

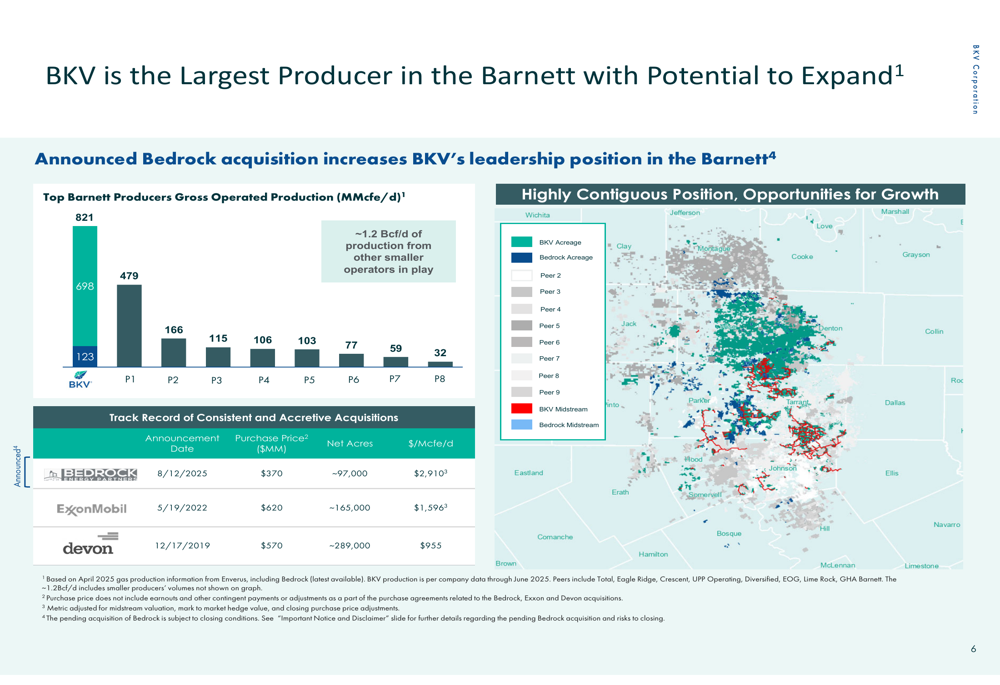

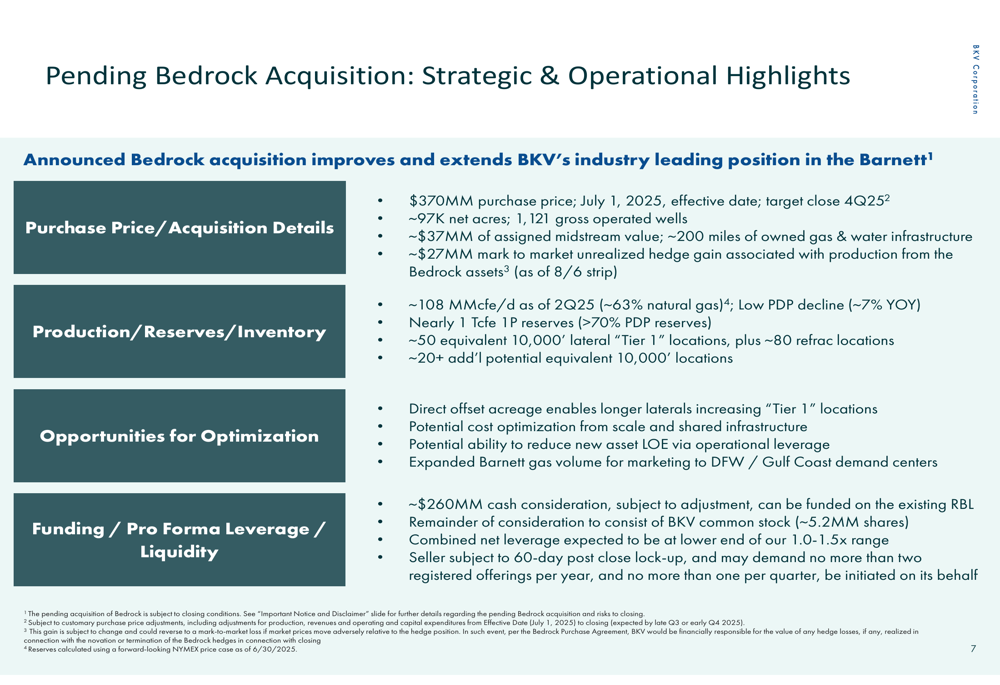

The most significant strategic development announced was BKV’s acquisition of Bedrock Energy Partners for $370 million, further cementing the company’s position as the largest producer in the Barnett. The acquisition adds approximately 97,000 net acres, 1,121 gross operated wells, and production of 108 MMcfe/d as of Q2 2025.

The following chart illustrates BKV’s dominant position in the Barnett region and the impact of the Bedrock acquisition:

The Bedrock acquisition, expected to close in Q4 2025, includes nearly 1 Tcfe of 1P reserves (>70% PDP) and approximately 50 equivalent 10,000’ lateral "Tier 1" locations. The transaction structure involves approximately $260 million in cash consideration with the remainder in BKV common stock.

Key strategic highlights of the acquisition include:

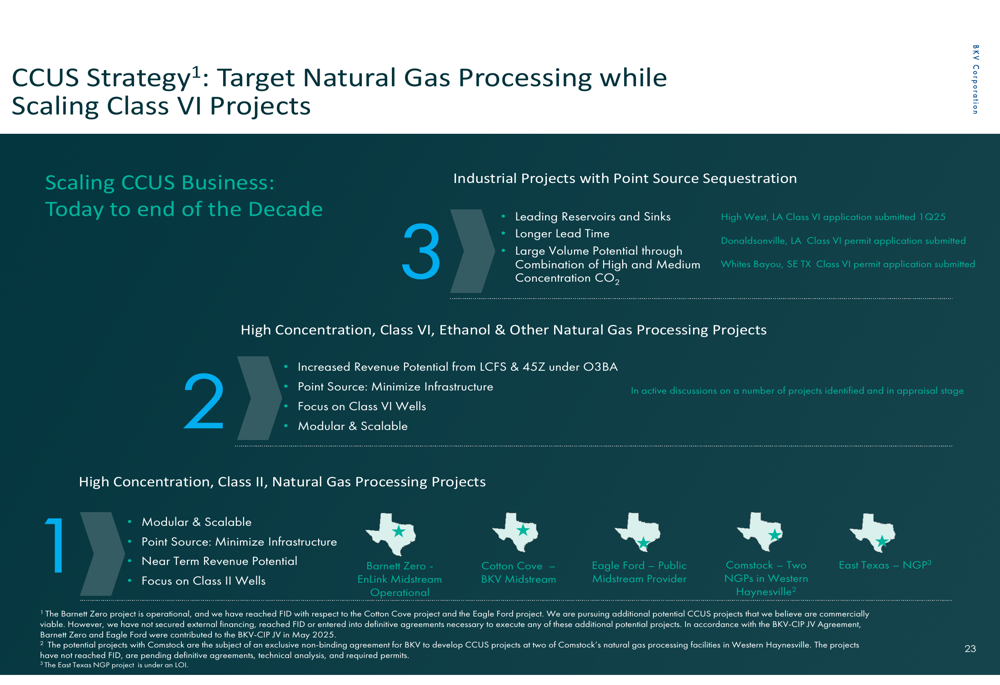

BKV continues to advance its carbon capture utilization and storage (CCUS) business, with multiple projects in development. The company’s flagship Barnett Zero project has been injecting CO₂ since November 2023, and additional projects are planned to scale sequestration volumes to 3.1 million tons by 2028.

The company’s CCUS strategy is illustrated in the following diagram:

Competitive Industry Position

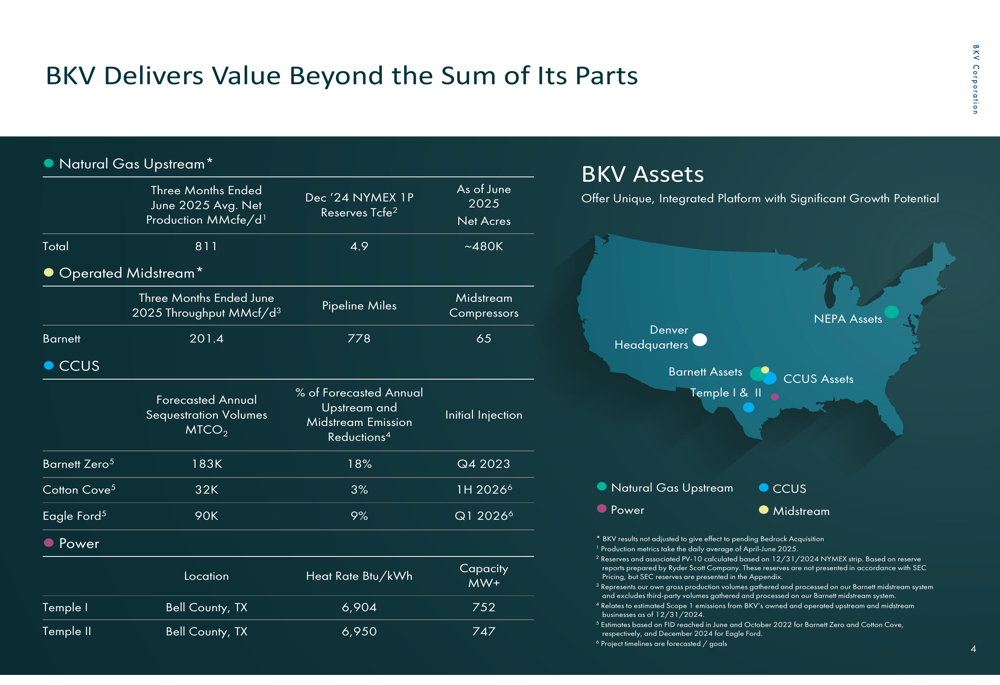

BKV has established itself as the largest producer in the Barnett with 821 MMcfe/d of gross operated production, significantly ahead of its nearest competitors. The company’s inventory strength includes over 500 locations representing more than 15 years of drilling inventory, with 270 pre-Bedrock locations below $3.00/MMBtu breakeven.

The company’s power assets are strategically positioned to benefit from rapid growth in the ERCOT market, where annual energy demand is forecast to grow at an average annual rate of 13.6% from 2025-2031, compared to historical growth of 3.1% from 2014-2024. This growth is being driven in part by data center development in Temple, Texas, where BKV’s power plants are located.

The following slide illustrates BKV’s comprehensive asset portfolio and geographic footprint:

The company’s power joint venture with Banpu Power US is particularly well-positioned to capitalize on growing demand from data centers and industrial users in the Temple, Texas area. Several major projects are underway, including Meta (NASDAQ:META)’s 900,000 sq. ft data center with 152 MW capacity and Rowan Moriah’s 300 MW capacity data center.

Forward-Looking Statements

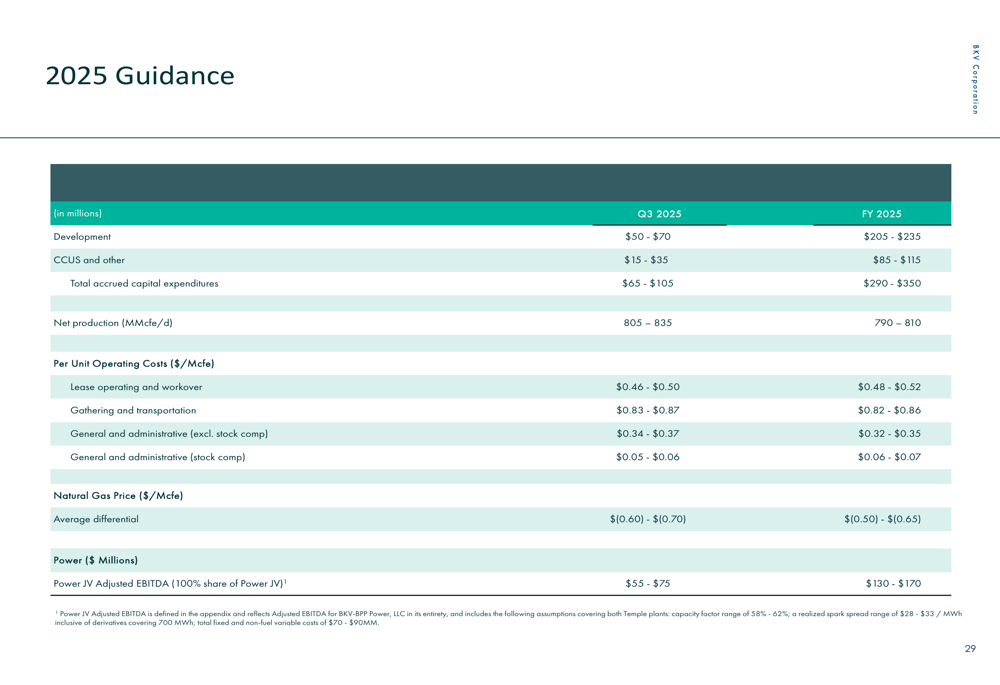

BKV provided detailed guidance for the remainder of 2025, maintaining its disciplined approach to capital allocation while pursuing growth opportunities. For full-year 2025, the company expects:

- Total (EPA:TTEF) accrued capital expenditures of $290-350 million

- Net production of 790-810 MMcfe/d

- Lease operating and workover costs of $0.48-0.52 per Mcfe

- Power JV Adjusted EBITDA (100% share) of $130-170 million

The following table details BKV’s 2025 guidance:

The company’s hedging strategy provides downside protection, with 58% of natural gas volumes hedged at $3.45/MMBtu and 42% of NGL volumes hedged at $21.73/Bbl as of July 28, 2025. This approach aligns with BKV’s stated philosophy of supporting targeted price levels while managing exposure to commodity price fluctuations.

BKV’s long-term strategy continues to focus on its vertically integrated model, combining low-decline natural gas assets with power generation and carbon capture to create value throughout the commodity cycle. The company aims to maintain low net leverage of 1.0x-1.5x while funding organic investments through cash flow.

As illustrated in this overview of BKV’s investment proposition:

Analyst Perspectives

Following BKV’s Q1 2025 earnings beat, which saw adjusted EPS of $0.41 exceeding expectations, analysts have maintained a "Strong Buy" consensus recommendation according to InvestingPro data. Price targets range from $20 to $33, suggesting potential upside of up to 35% from current levels.

The Q2 2025 presentation reinforces several key elements that analysts have highlighted, including the company’s strong operational execution, strategic focus on high-growth areas such as carbon capture and power generation, and disciplined financial management. The Bedrock acquisition and continued expansion of the CCUS business align with BKV’s stated growth strategy and appear to support the bullish analyst outlook.

With a market capitalization of approximately $1.62 billion and trading near $20.12, BKV continues to position itself as a differentiated energy company with exposure to multiple growth drivers, including ERCOT power demand, data center expansion, and carbon capture incentives under recent legislation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.