AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

Blade Air Mobility, Inc. (NASDAQ:BLDE) presented its Q1 2025 investor presentation on May 12, 2025, highlighting the company’s first full year of adjusted EBITDA profitability and continued growth across its business segments. The presentation comes after the company’s shares surged 10.62% in pre-market trading to $3.23, according to recent market data, reflecting positive investor sentiment following the company’s financial milestone.

The urban air mobility provider operates through two primary segments: Medical (TASE:BLWV) (organ transport) and Passenger (short-distance air travel), with a strategic focus on its asset-light business model and future positioning for Electric Vertical Aircraft (EVA) adoption.

Financial Performance Highlights

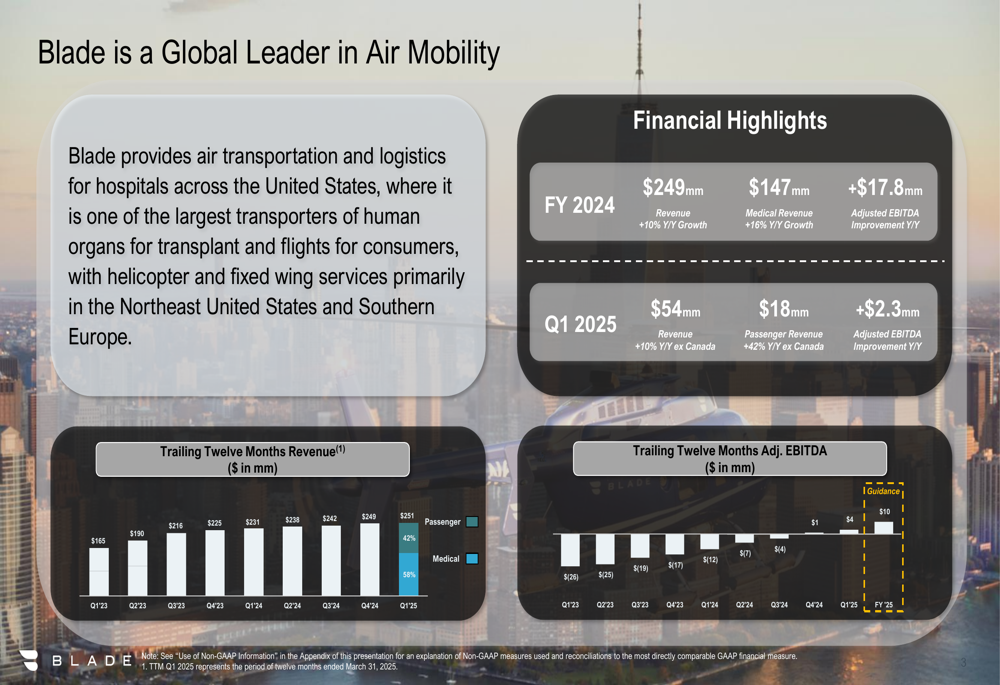

Blade reported strong financial results for FY 2024, with total revenue reaching $249 million, representing a 10% year-over-year increase. The company achieved its first full year of positive adjusted EBITDA, marking a significant improvement of $17.8 million compared to the previous year.

For Q1 2025, Blade generated $54 million in revenue, a 10% year-over-year increase excluding Canada operations. The company’s trailing twelve-month (TTM) revenue reached $251 million, up from $216 million in Q1 2023, while TTM adjusted EBITDA improved from a $7 million loss in Q1 2023 to a positive $4 million in Q1 2025.

As shown in the following financial highlights chart, the company has demonstrated consistent revenue growth and EBITDA improvement:

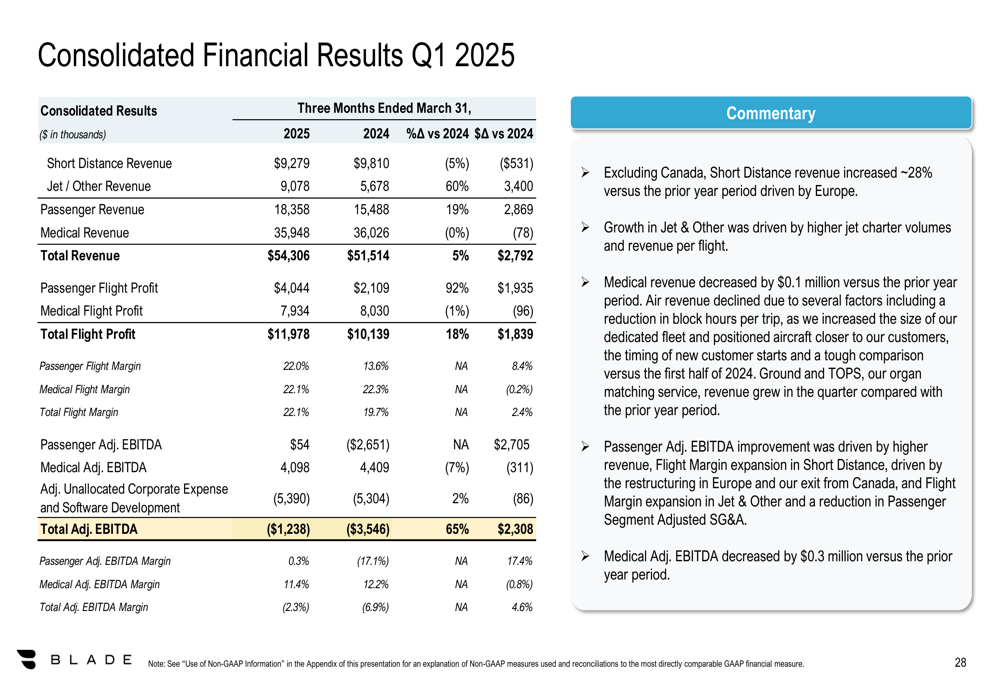

The detailed Q1 2025 financial results reveal that Passenger revenue increased by 19% year-over-year to $18.4 million, driven primarily by 60% growth in the Jet/Other segment. Medical revenue remained flat at $35.9 million. Total (EPA:TTEF) flight profit increased by 18% to $12 million, with both segments maintaining healthy margins above 22%.

Medical Segment Growth Strategy

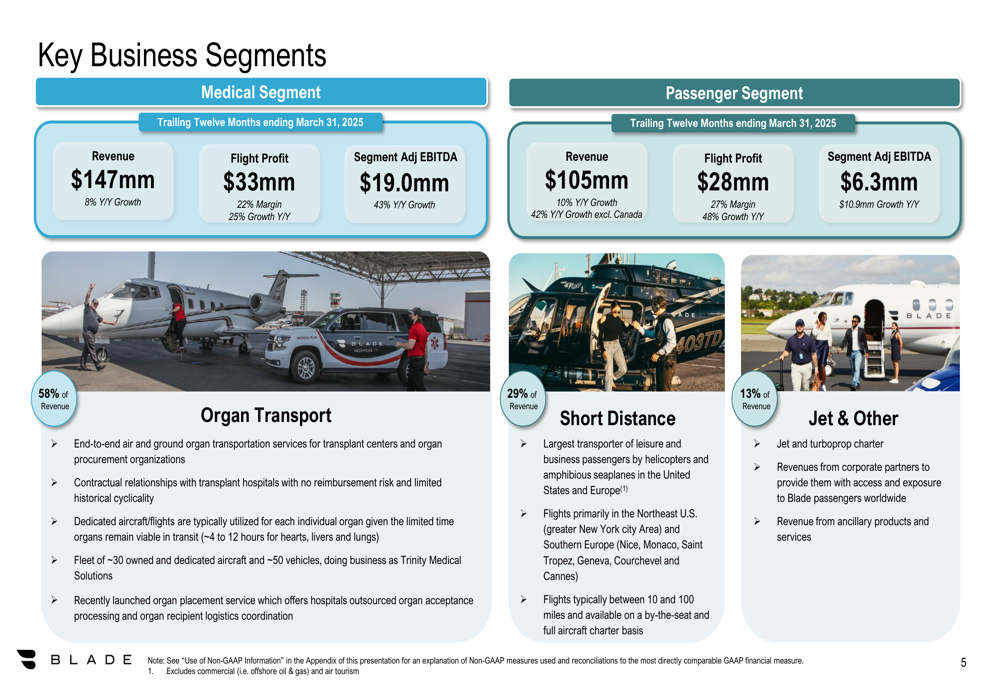

The Medical segment continues to be Blade’s primary growth driver, accounting for 58% of total revenue. This segment generated $147 million in TTM revenue (8% Y/Y growth) with an impressive adjusted EBITDA of $19 million (43% Y/Y growth) and a 22% flight profit margin.

Blade’s medical business focuses on organ transport services for transplant centers and organ procurement organizations, utilizing approximately 30 dedicated aircraft and 50 ground vehicles. The company has identified significant growth opportunities in this segment, as it currently serves only about 30% of the $1 billion addressable market for transplant air logistics.

The following chart illustrates the key business segments and their respective performance metrics:

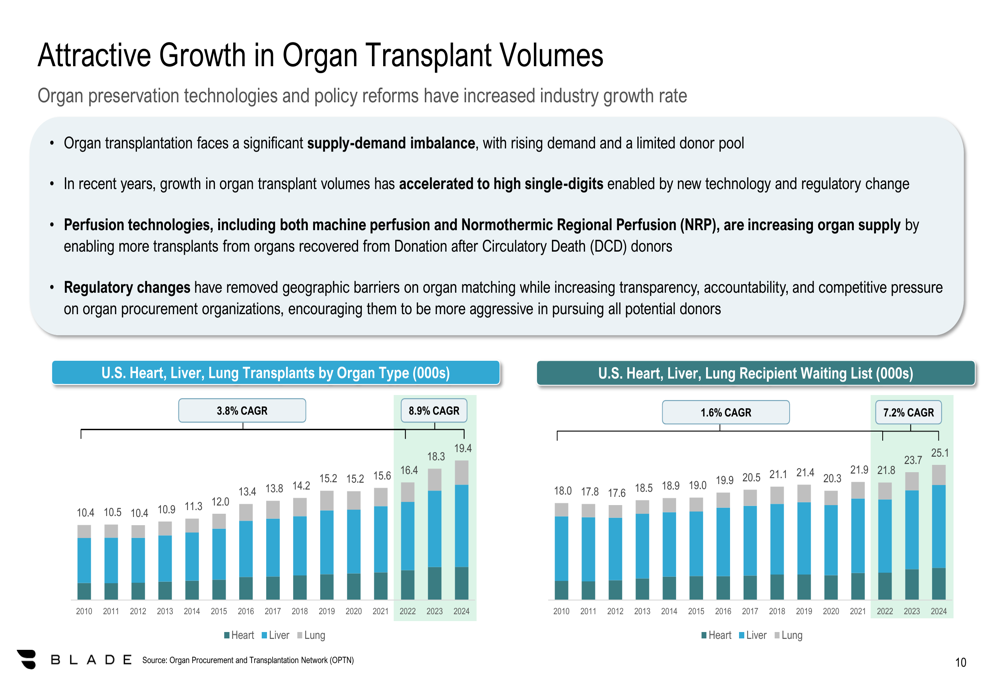

A key growth driver for the Medical segment is the increasing volume and distance of organ transplants. As shown in the chart below, U.S. heart, liver, and lung transplants have accelerated to an 8.9% CAGR in recent years, driven by new preservation technologies and regulatory changes:

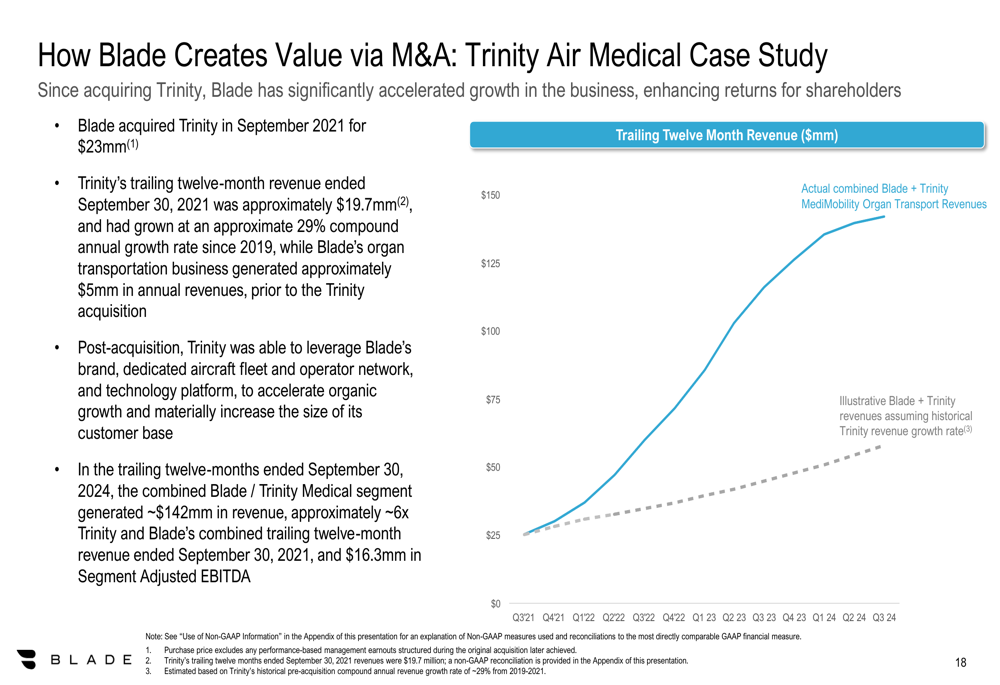

Blade’s acquisition of Trinity Air Medical in September 2021 for $23 million has proven to be a successful strategic move. The combined Medical segment has grown from $19.7 million in TTM revenue at acquisition to approximately $142 million in the TTM ended September 2024, with $16.3 million in segment adjusted EBITDA.

Passenger Segment Improvements

Blade’s Passenger segment has shown significant improvement, with TTM revenue of $105 million (10% Y/Y growth, 42% excluding Canada) and segment adjusted EBITDA of $6.3 million (10.9% Y/Y growth). The segment achieved a strong flight profit margin of 27%, representing 48% year-over-year growth.

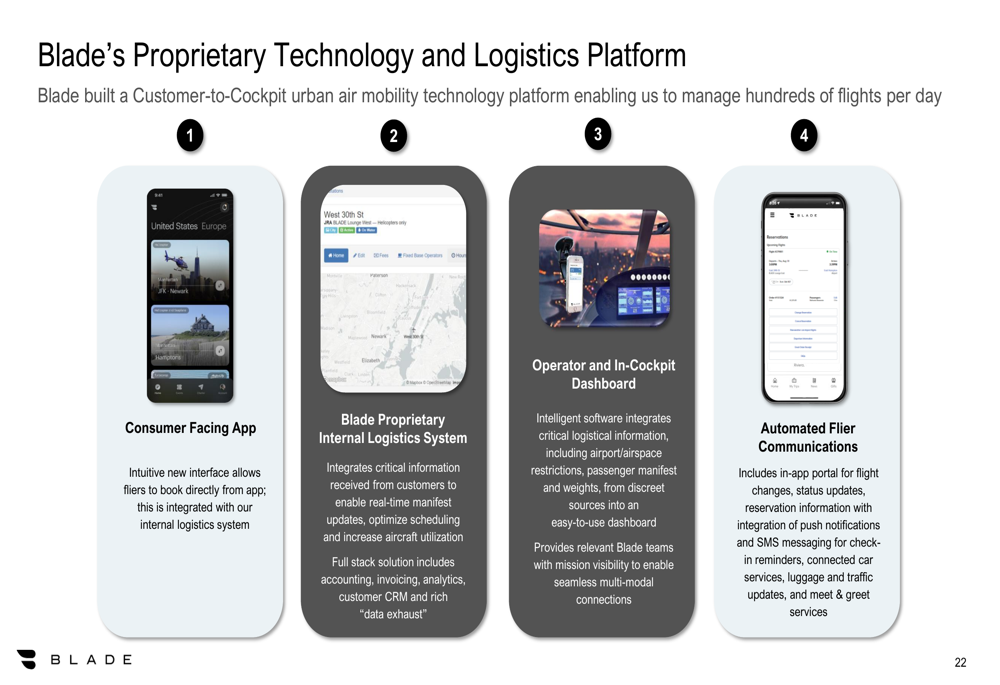

The company’s proprietary technology platform enhances the passenger experience through a consumer-facing app, internal logistics system, operator dashboard, and automated communications:

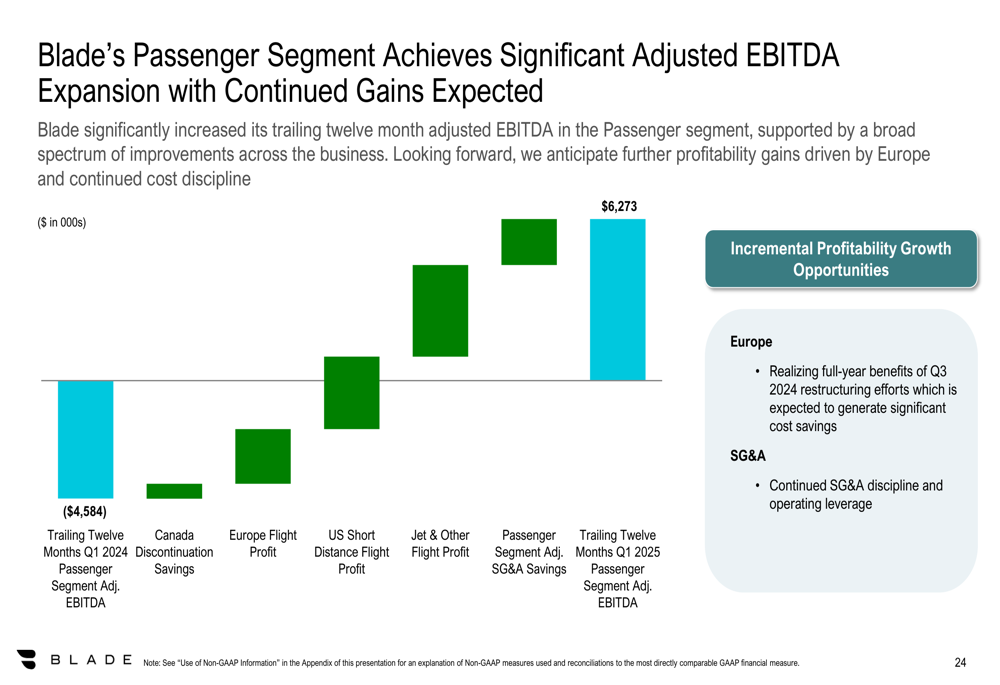

Blade has achieved substantial adjusted EBITDA expansion in its Passenger segment through strategic initiatives, including the restructuring of its international operations and improved flight margins:

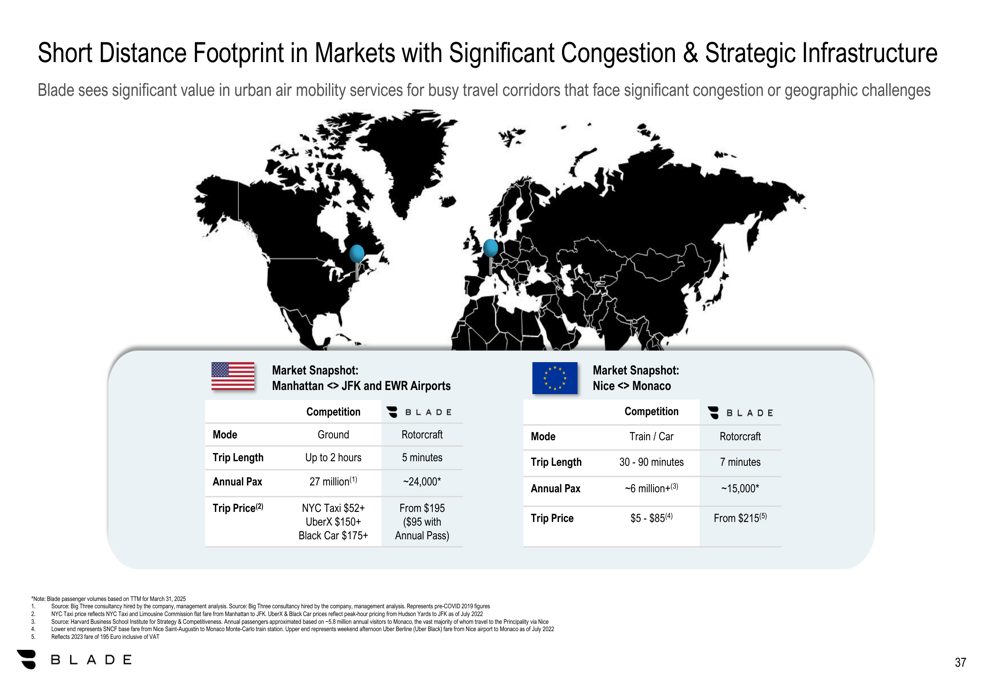

The company maintains a strategic infrastructure and terminal network in key locations, including Manhattan, Newark, Monaco, Nice, Cannes, and Atlantic City, providing competitive advantages in congested markets where air mobility offers significant time savings compared to ground transportation.

Strategic Positioning for EVA Transition

Blade is strategically positioning itself for the future transition to Electric Vertical Aircraft (EVA), which is expected to begin in late 2027 or early 2028. The company’s asset-light model provides flexibility to adapt to new aircraft technologies while maintaining profitability with conventional aircraft.

EVA’s lower noise footprint and zero emissions are expected to significantly expand Blade’s addressable market by enabling operations in areas that have historically been reluctant to embrace urban air mobility due to noise concerns. The company projects that EVA could reduce flight costs by approximately 23% compared to traditional rotorcraft, improving unit economics and potentially expanding the total addressable market to over $1 billion.

Blade’s strong balance sheet, with $120 million in cash and short-term investments and no debt, provides financial flexibility to pursue high-return investments in Medical aircraft and vehicles, as well as strategic M&A opportunities.

Outlook and Guidance

Looking ahead, Blade has provided guidance of $10 million in adjusted EBITDA for FY 2025, representing continued growth from the $4 million TTM figure reported in Q1 2025. The company expects to achieve this through:

1. Continued expansion in the Medical segment, targeting a 15% adjusted EBITDA margin

2. Further improvement in Passenger segment profitability

3. Strategic investments in owned aircraft for the Medical segment, with target ROICs of 30%+

4. Expansion of ground transport operations with payback periods of less than one year

5. Potential M&A opportunities, particularly in the Medical segment

The company’s asset-light model, with approximately 85% of aircraft capacity coming from third-party operators, provides operational flexibility while maintaining control over the customer experience and safety standards.

While Blade faces challenges, including flat medical revenue anticipated in the first half of 2025 and the exit from the Canadian market, the company’s diversified business model, strong balance sheet, and strategic positioning for the EVA transition provide multiple avenues for continued growth and profitability improvement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.