Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Blend Labs , Inc. (NYSE:BLND) released its Q2 2025 earnings presentation on August 7, 2025, highlighting continued operational improvements and growth in its Consumer Banking segment despite ongoing challenges in the mortgage market. The fintech company, which provides digital lending and banking solutions, reported its fourth consecutive quarter of non-GAAP operating profitability while continuing to diversify its revenue streams.

The presentation comes after a challenging Q1 where Blend missed earnings expectations but has since shown signs of recovery. The company’s stock closed at $3.57 on August 7, near the middle of its 52-week range of $2.79 to $5.525.

Quarterly Performance Highlights

Blend Labs reported Q2 2025 revenue of $31.5 million, exceeding the midpoint of its guidance and representing a 10% increase year-over-year. The company achieved a 15% non-GAAP operating margin, marking its fourth consecutive quarter of non-GAAP operating profitability. Additionally, Blend reported record remaining performance obligations of $190 million, boosted by a significant $50 million renewal and expansion.

As shown in the following quarterly highlights chart:

Despite these positive developments, Blend continues to report GAAP losses. For Q2 2025, the company posted a GAAP net loss attributable to common stockholders of $11.0 million, or $0.03 per share from continuing operations. This represents an improvement from previous quarters but highlights the ongoing gap between GAAP and non-GAAP results.

Revenue Growth and Segment Analysis

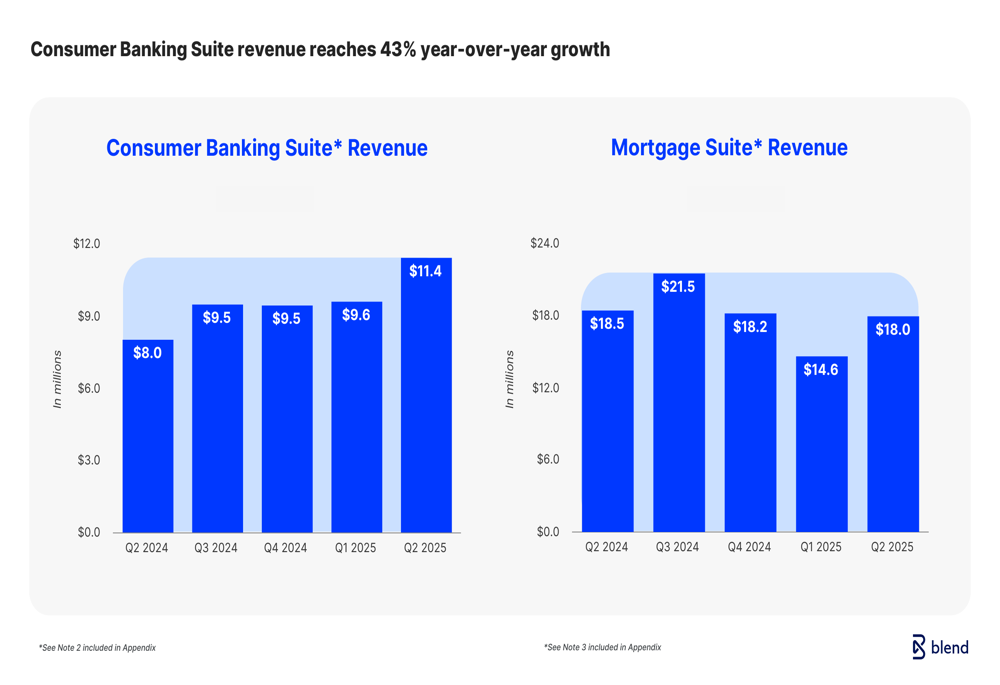

A key highlight of Blend’s Q2 performance was the strong growth in its Consumer Banking Suite, which generated revenue of $11.4 million, a 43% increase compared to Q2 2024. This growth demonstrates Blend’s successful diversification beyond mortgage products. Meanwhile, the Mortgage Suite generated $18.0 million in revenue, representing a slight 3% year-over-year decline, reflecting the challenging mortgage market conditions.

The following chart illustrates the revenue trends for both segments:

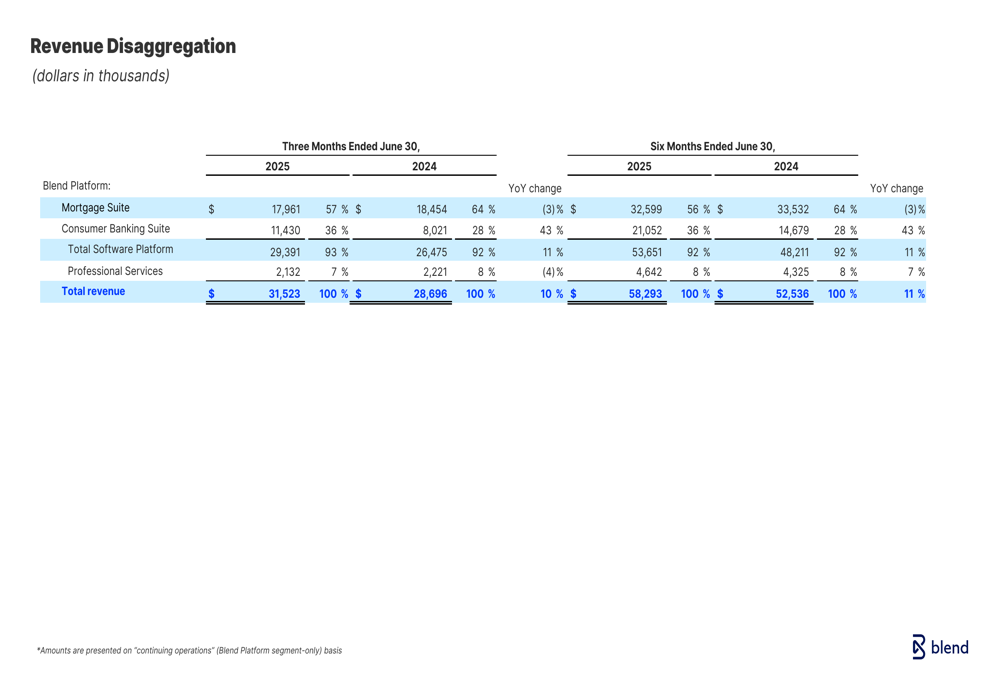

The revenue disaggregation shows that the Mortgage Suite still accounts for the majority of Blend’s revenue at 57% for the three months ended June 30, 2025, though this percentage has decreased from previous quarters as Consumer Banking continues to grow. The Consumer Banking Suite now represents 36% of total revenue, highlighting the company’s evolving business mix.

As shown in this detailed revenue breakdown:

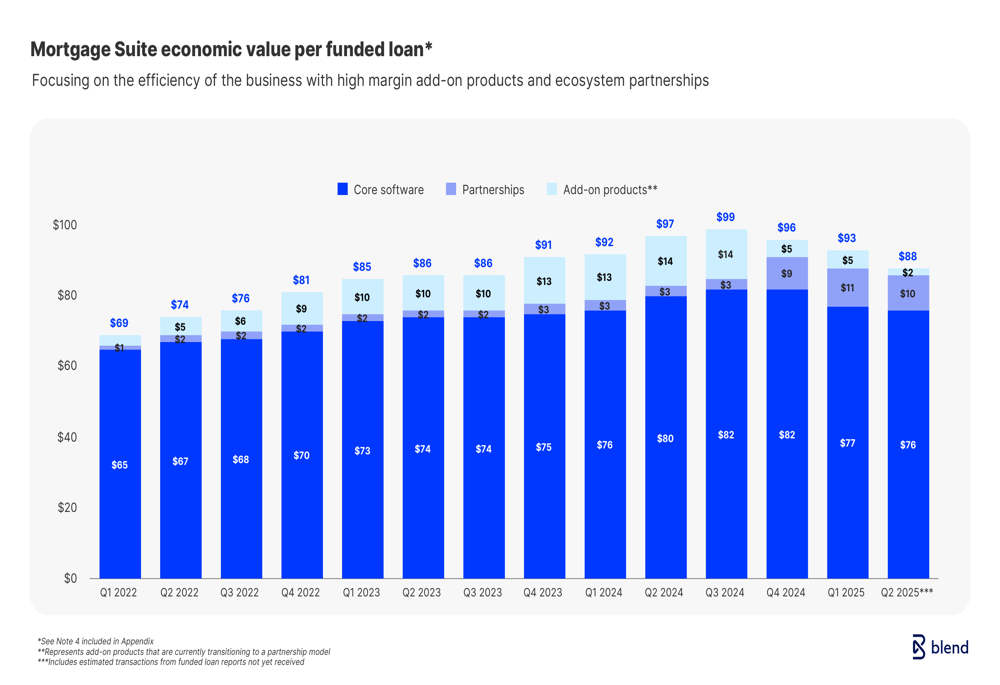

Blend has also maintained relatively stable economic value per funded loan in its Mortgage Suite, with a total value of $90 in Q2 2025 ($78 from core software, $2 from partnerships, and $10 from add-on products). This represents a slight decrease from the peak of $97 in Q2 2024 but shows resilience in a challenging mortgage environment.

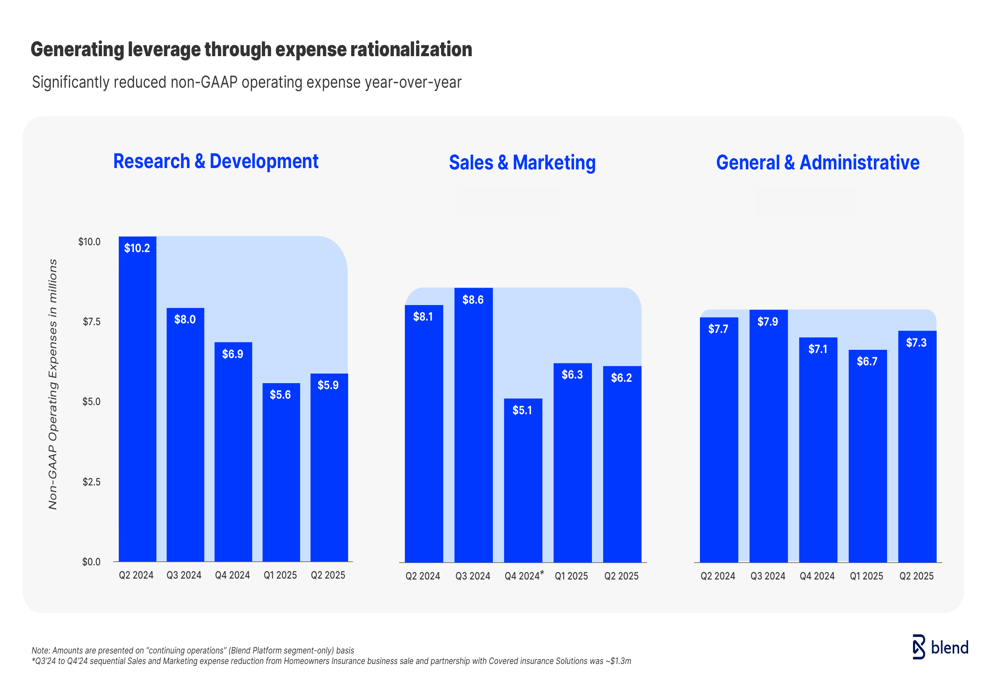

Margin Improvements and Cost Rationalization

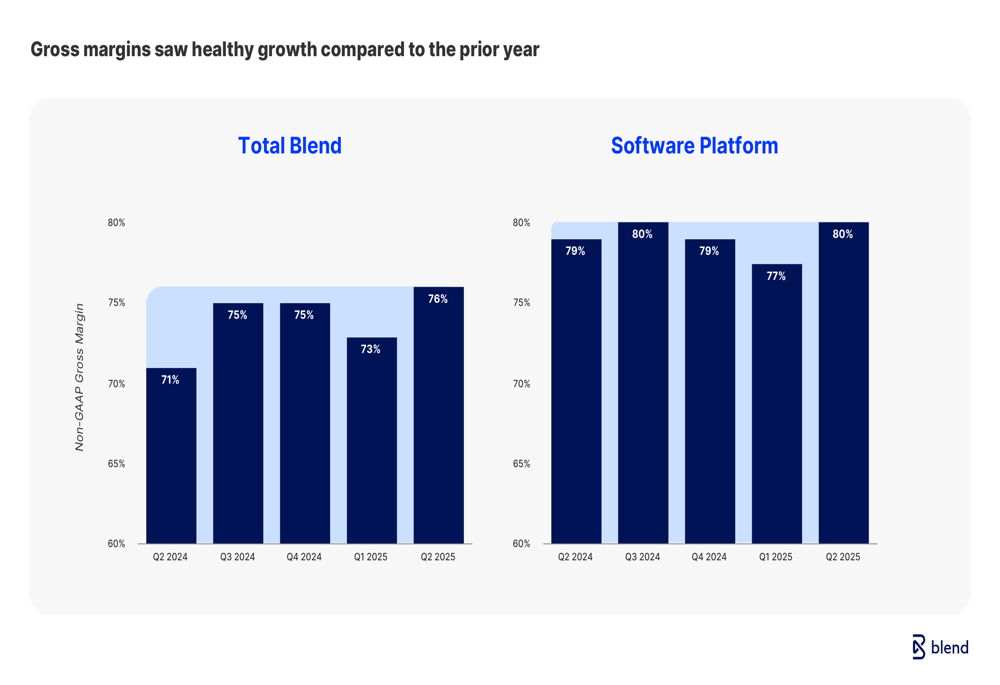

Blend’s gross margins have shown consistent improvement, with non-GAAP gross margin for Total (EPA:TTEF) Blend reaching 76% in Q2 2025, up from 71% in Q2 2024. The Software (ETR:SOWGn) Platform segment achieved an even higher gross margin of 80%, up from 79% in the same period last year.

The following chart demonstrates this positive trend in gross margins:

A significant contributor to Blend’s improved profitability has been its aggressive cost rationalization efforts. The company has substantially reduced operating expenses across all categories, with Research & Development expenses decreasing by more than half from $10.2 million in Q2 2024 to $5.0 million in Q2 2025. Sales & Marketing expenses also decreased from $8.1 million to $6.2 million, while General & Administrative expenses saw a slight reduction from $7.7 million to $7.3 million.

The operating expense reduction is clearly illustrated in this chart:

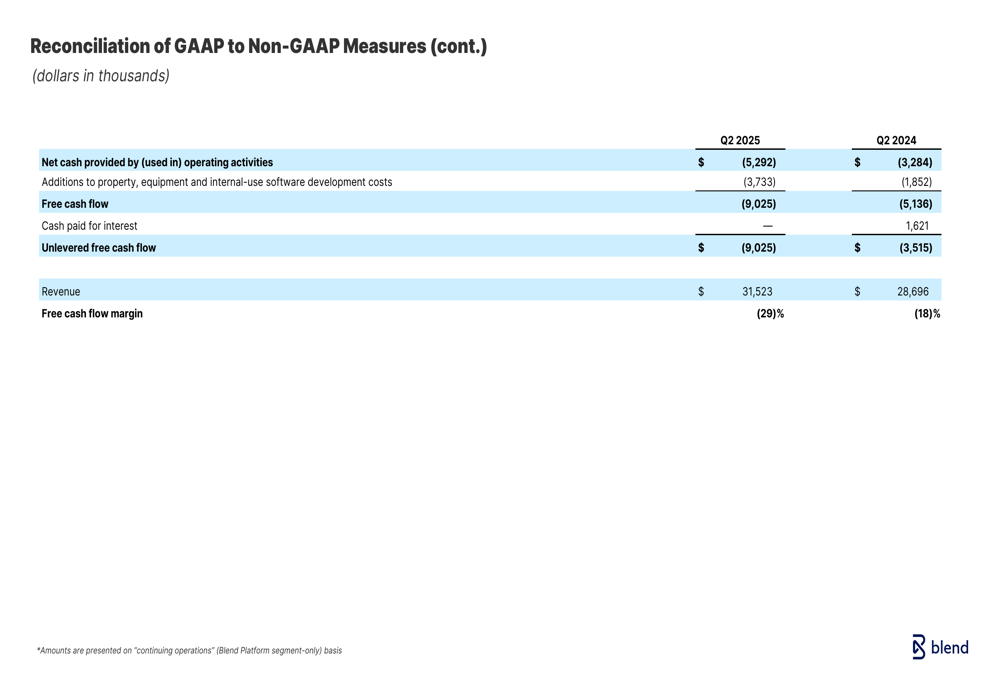

Despite these improvements in operating profitability, Blend’s free cash flow remains negative at ($9,025) for Q2 2025, worsening from ($5,136) in Q2 2024. The free cash flow margin deteriorated to (29)% from (18)% year-over-year. This contrasts with the positive free cash flow of $15.5 million reported in Q1 2025, suggesting significant quarter-to-quarter volatility in cash generation.

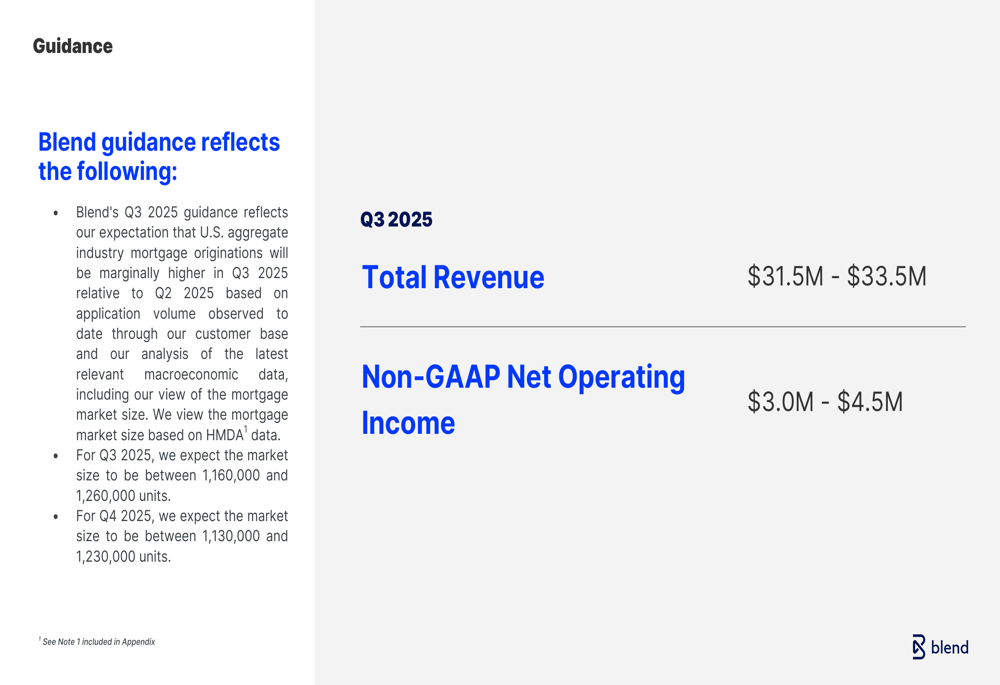

Forward Guidance and Outlook

Looking ahead to Q3 2025, Blend provided guidance for total revenue between $31.5 million and $33.5 million, suggesting flat to modest sequential growth. The company expects non-GAAP net operating income between $3.0 million and $4.5 million. These projections are based on expectations of marginally higher mortgage originations in Q3 relative to Q2, with the mortgage market size estimated between 1,160,000 and 1,260,000 units.

As shown in the company’s guidance slide:

Blend’s forward-looking statements reflect cautious optimism about its ability to maintain operating profitability while navigating a challenging mortgage market. The company’s continued investment in its Consumer Banking Suite appears to be paying dividends, providing a growing revenue stream that helps offset the volatility in the mortgage business.

The presentation suggests Blend is focusing on three key strategies: expanding its Consumer Banking offerings, maintaining its position in the Mortgage Suite despite market challenges, and continuing to optimize its cost structure to improve profitability. With record remaining performance obligations and improving margins, Blend appears positioned to continue its gradual recovery, though challenges remain in achieving consistent GAAP profitability and positive free cash flow.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.