Uxin shares drop 45% as predicted by InvestingPro’s Fair Value model

Introduction & Market Context

Blend Labs, Inc. (NYSE:BLND) presented its third quarter 2025 earnings results on November 6, 2025, highlighting performance that exceeded guidance despite ongoing challenges in the mortgage sector. The fintech company, which provides digital lending platforms to financial institutions, saw its stock drop 7.14% in regular trading and an additional 1.02% in after-hours trading, reflecting investor concerns about declining mortgage market share.

The company reported total revenue of $32.9 million, slightly above analyst expectations of $32.78 million, though this represented a modest 1% year-over-year decline. Despite the revenue beat, investors appeared focused on Blend's continued loss of mortgage market share and the sustainability of its growth strategy.

Quarterly Performance Highlights

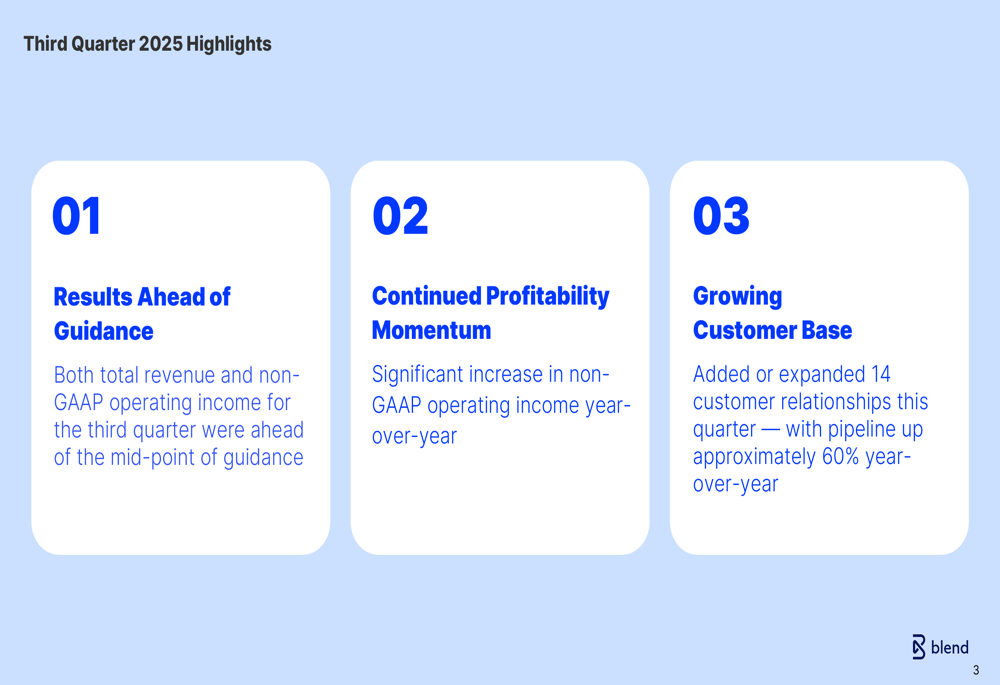

Blend Labs exceeded its guidance for both total revenue and non-GAAP operating income in Q3 2025. The company reported significant year-over-year improvement in non-GAAP operating income, achieving $4.6 million with a 14% operating margin. Additionally, Blend expanded its customer base, adding or expanding 14 customer relationships during the quarter, with its pipeline growing approximately 60% year-over-year.

As shown in the following chart of quarterly highlights:

The company maintained a strong cash position of $82.3 million while continuing its share repurchase program, buying back 1.6 million shares worth $5 million during the quarter.

Segment Analysis: Consumer Banking vs. Mortgage

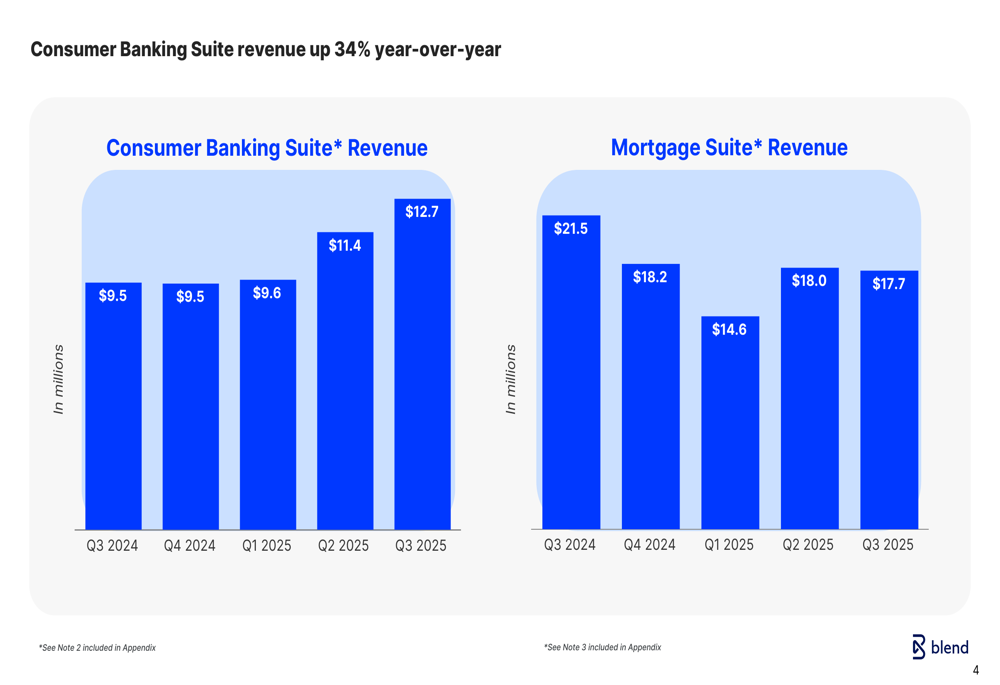

Blend's performance showed a clear divergence between its two main business segments. The Consumer Banking Suite demonstrated robust growth, generating $12.7 million in revenue for Q3 2025, a 34% increase year-over-year and an 11% improvement quarter-over-quarter. This growth highlights the success of Blend's diversification strategy beyond mortgage lending.

In contrast, the Mortgage Suite revenue declined to $17.7 million in Q3 2025 from $21.5 million in Q3 2024, reflecting broader industry challenges and customer churn. The following chart illustrates this divergence:

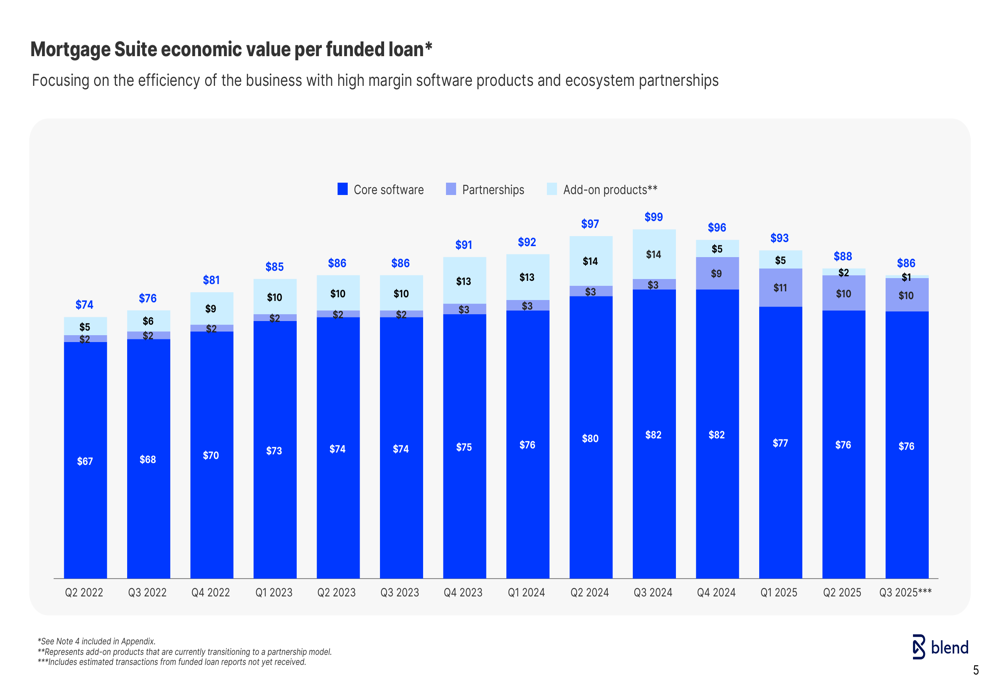

Despite the revenue decline in the Mortgage Suite, Blend has maintained strong economics per funded loan. The economic value per funded loan reached $86 in Q3 2025, with core software contributing $76, partnerships adding $10, and add-on products providing $1. This metric demonstrates the efficiency of Blend's business model with high-margin software products and ecosystem partnerships.

The breakdown of economic value per funded loan is illustrated here:

Margin Improvement and Operational Efficiency

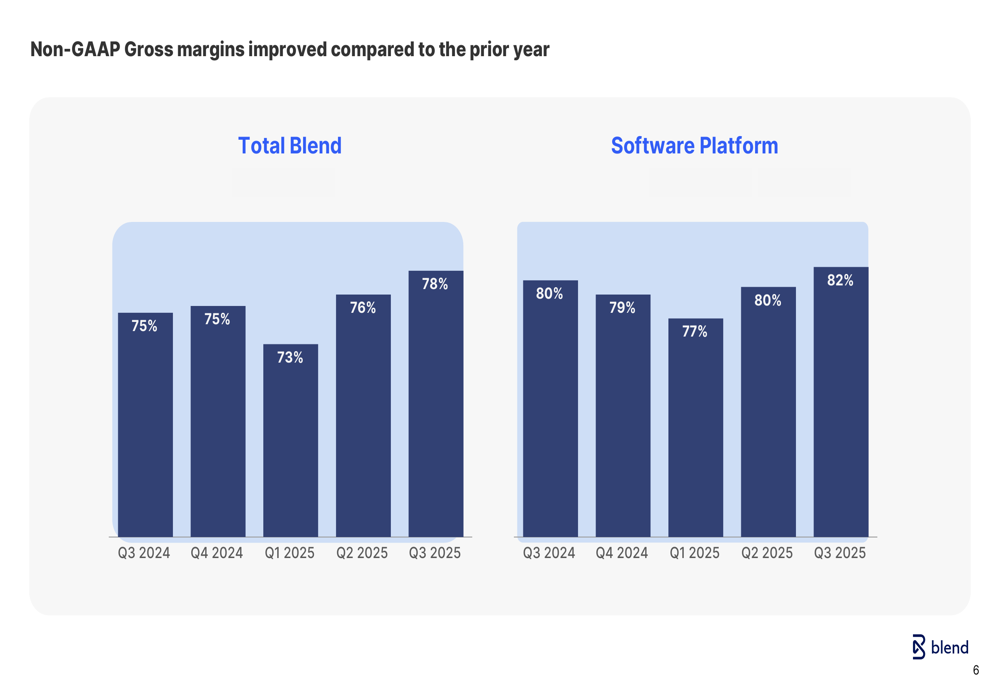

A key bright spot in Blend's presentation was the improvement in gross margins. The company's non-GAAP gross margin for the total business reached 78% in Q3 2025, up from 75% in Q3 2024. The Software Platform segment showed even stronger margins at 82% in Q3 2025, compared to 80% a year earlier.

The following chart shows the consistent margin improvement over the past five quarters:

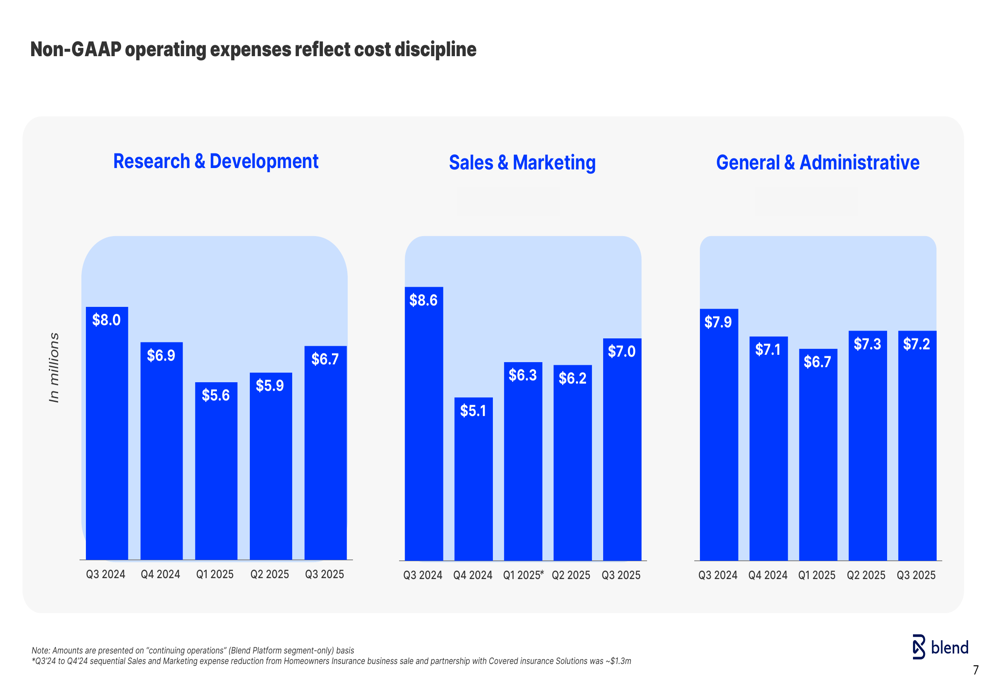

This margin expansion reflects Blend's focus on operational efficiency and higher-value offerings. The company has maintained disciplined expense management across research and development, sales and marketing, and general and administrative functions, as shown below:

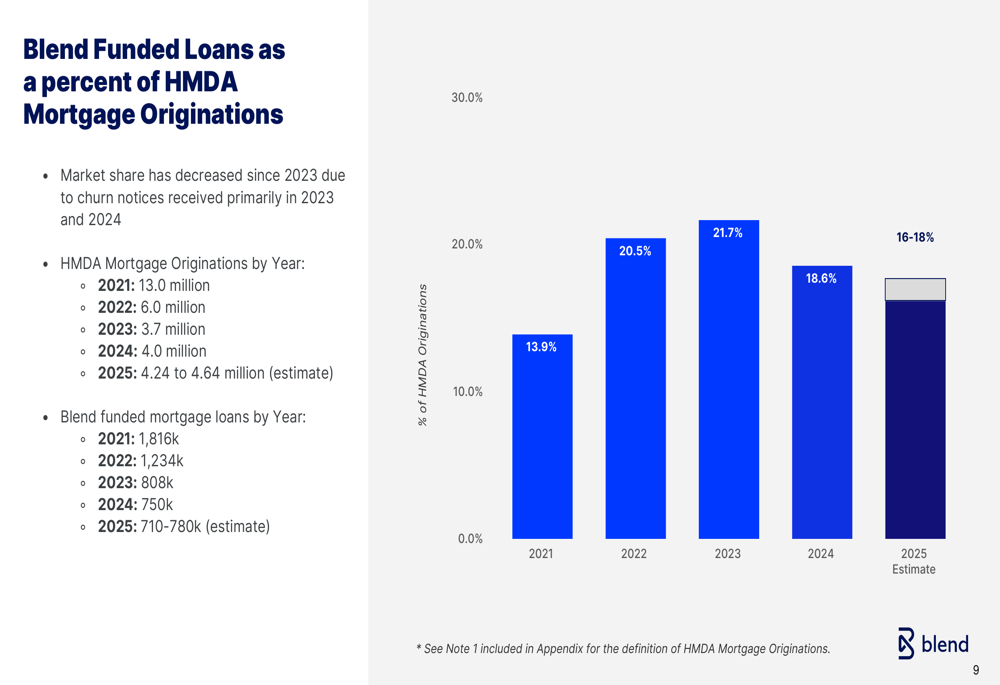

Market Share Challenges

Despite the positive financial metrics, Blend Labs faces significant challenges in maintaining its market share in mortgage originations. The company's funded loans as a percentage of HMDA mortgage originations has declined from a peak of 21.7% in 2023 to an estimated 16-18% in 2025.

The following chart illustrates this concerning trend:

Blend attributes this market share erosion primarily to customer churn notices received in 2023 and 2024. This decline represents a significant headwind for the company, as mortgage lending remains its largest revenue segment despite the growth in consumer banking.

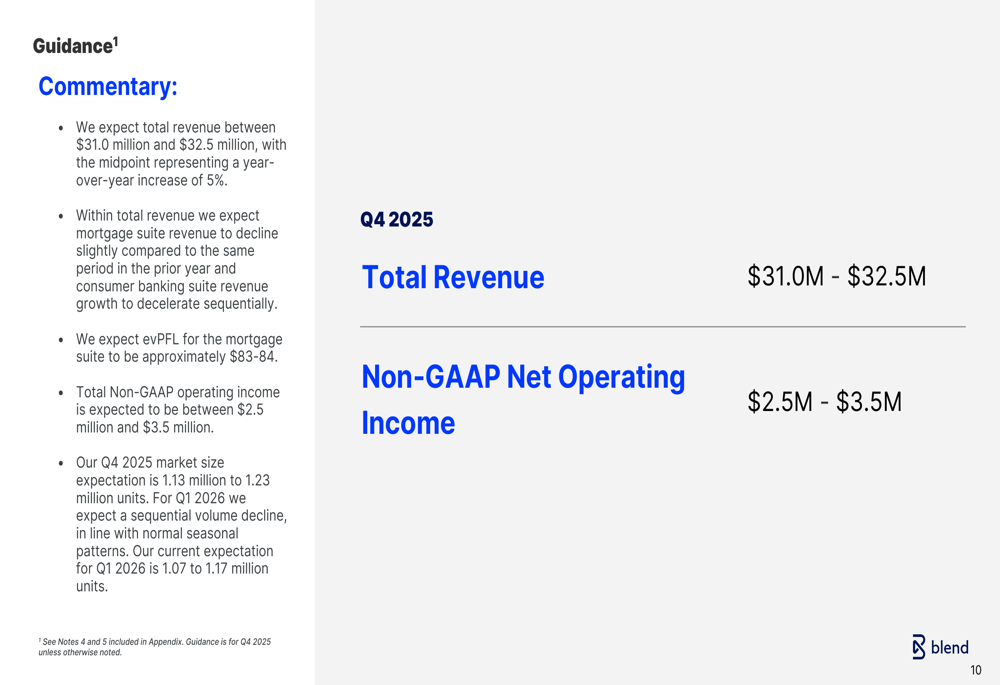

Forward Guidance and Outlook

Looking ahead to Q4 2025, Blend provided revenue guidance of $31.0-$32.5 million, with the midpoint representing a 5% year-over-year increase. The company expects non-GAAP net operating income between $2.5-$3.5 million, continuing its profitability momentum.

The guidance details are shown here:

During the earnings call, CEO Nima Ghamsari emphasized the company's forward-looking strategy, stating, "We are no longer just ready for what's next. We are building what's next." He highlighted the importance of AI in the company's product development, describing it as "almost like water for us at this point."

Jason Ream, Head of Finance and Administration, reinforced the company's commitment to product innovation, noting, "We have a strong portfolio of products that will continue to improve."

While Blend faces ongoing market share challenges in its mortgage business, the strong growth in consumer banking and improving operational efficiency provide some counterbalance. However, investors appear to remain cautious about the company's ability to reverse the mortgage market share decline while maintaining overall growth, as reflected in the stock's performance following the earnings release.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.