Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Bloom Energy (NYSE:BE) presented its Q1 2025 financial results on April 30, showcasing significant improvement across key metrics and achieving its first-ever positive Q1 non-GAAP EPS. The clean energy company, which focuses on on-site power generation solutions, continues to benefit from growing electricity demands and investments in AI data centers, despite facing potential headwinds from tariffs and broader market skepticism.

The company’s mission to "Make Clean, Reliable Energy Affordable for Everyone in the World" underpins its strategic focus as it navigates an increasingly competitive energy landscape. Despite the positive financial results, Bloom’s stock has experienced downward pressure, closing at $16.81 on May 1, 2025, down 8.24% from the previous close.

Quarterly Performance Highlights

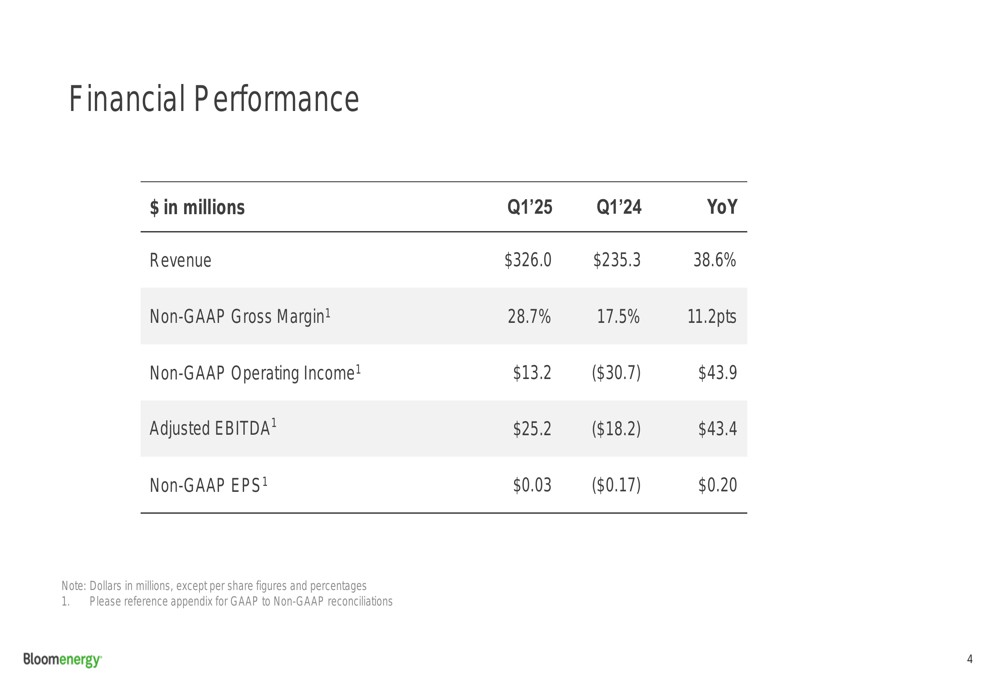

Bloom Energy reported substantial year-over-year improvements across all key financial metrics for Q1 2025. Revenue reached $326.0 million, representing a 38.6% increase compared to Q1 2024’s $235.3 million. This strong top-line growth was accompanied by significant margin expansion.

As shown in the following financial performance summary:

The company achieved a non-GAAP gross margin of 28.7%, an impressive 11.2 percentage point improvement from 17.5% in the same quarter last year. This margin expansion translated into a non-GAAP operating income of $13.2 million, a remarkable turnaround from the $30.7 million loss reported in Q1 2024.

Adjusted EBITDA similarly showed substantial improvement, reaching $25.2 million compared to negative $18.2 million in the prior-year period. Perhaps most notably, Bloom Energy reported its first-ever positive Q1 non-GAAP EPS of $0.03, compared to a loss of $0.17 per share in Q1 2024.

Detailed Financial Analysis

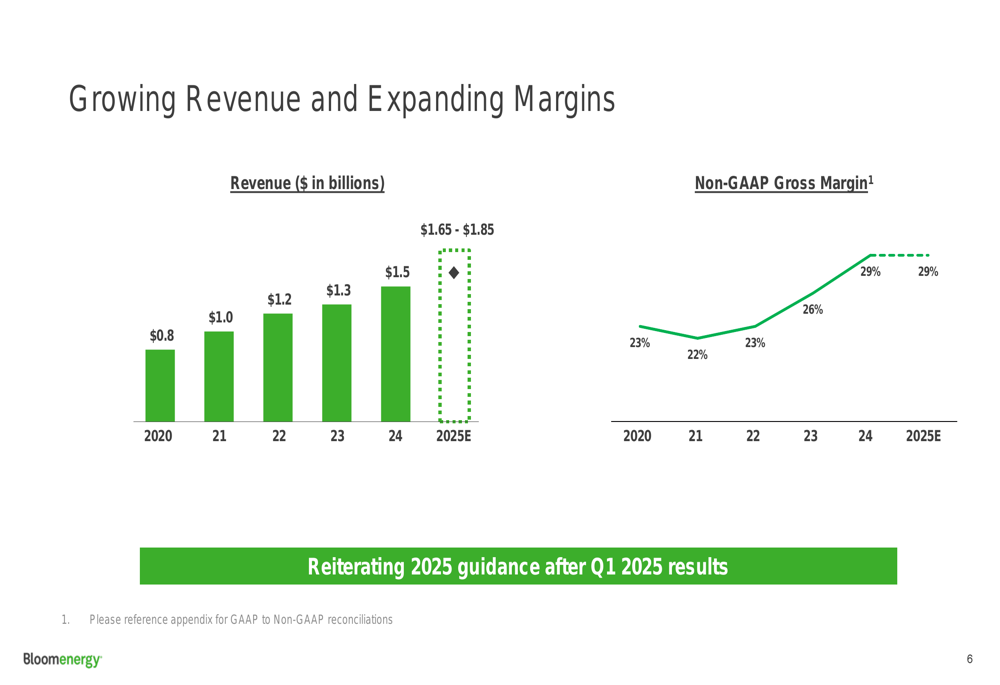

Bloom Energy’s financial trajectory shows consistent improvement over recent years. The company has been steadily growing revenue while simultaneously expanding margins, as illustrated in the following chart:

Revenue has grown from $0.8 billion in 2020 to $1.5 billion in 2024, with projections for 2025 ranging between $1.65 billion and $1.85 billion. Similarly, non-GAAP gross margins have improved from 23% in 2020 to 26% in 2024, with a target of approximately 29% for 2025.

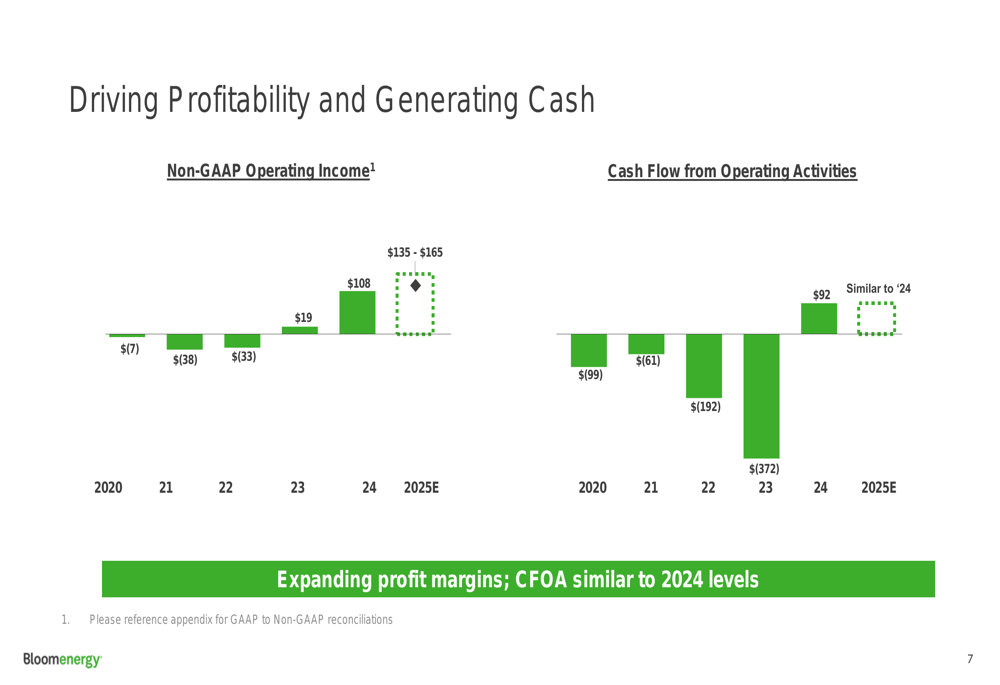

The company’s profitability metrics show even more dramatic improvement, as demonstrated in this chart of operating income and cash flow:

Non-GAAP operating income has increased from a $7 million loss in 2020 to $108 million in 2024, with 2025 projections between $135 million and $165 million. Cash flow from operating activities has similarly improved from negative $99 million in 2020 to positive $92 million in 2024, with 2025 expected to maintain similar levels.

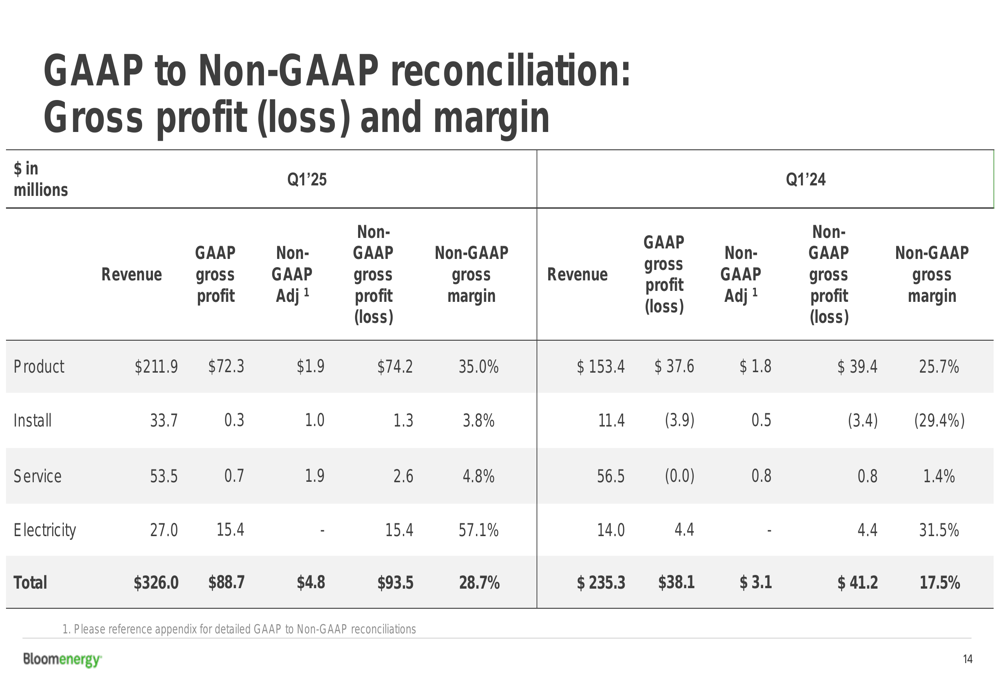

A closer examination of Bloom’s Q1 2025 performance by segment reveals varied contributions to overall profitability:

The product segment generated the highest revenue at $211.9 million with strong margins, while the electricity segment, though smaller at $27 million in revenue, delivered the highest non-GAAP gross margin at 57.1%. The install and service segments showed more modest profitability with non-GAAP gross margins of 3.8% and 4.8%, respectively.

Forward-Looking Statements

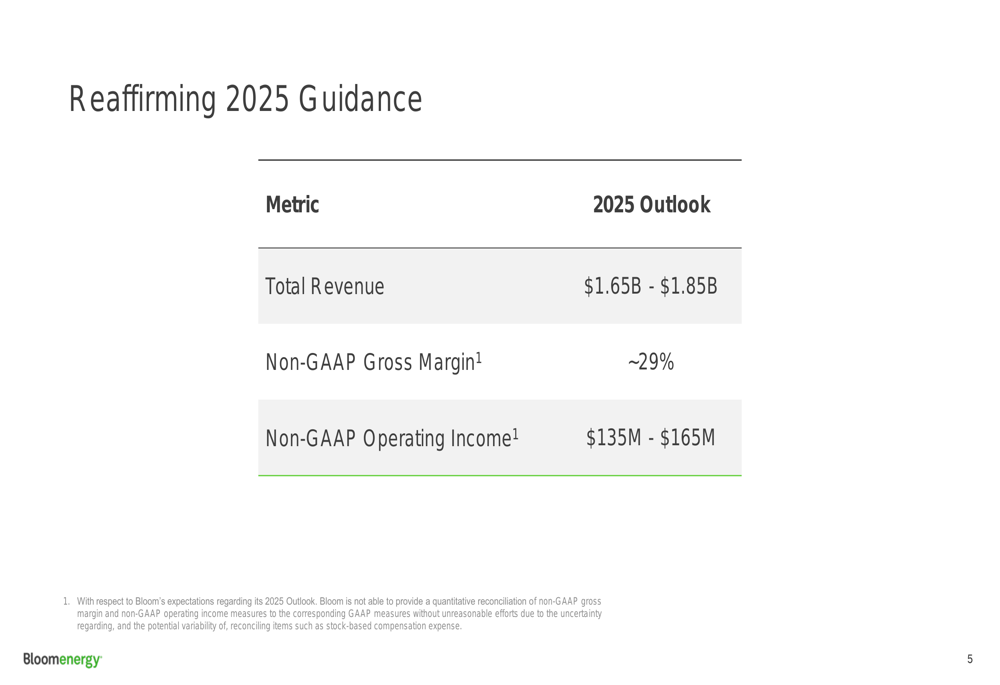

Bloom Energy has reaffirmed its guidance for 2025, maintaining confidence in its growth trajectory despite potential challenges. The company’s outlook remains positive, as shown in the following guidance summary:

For the full year 2025, Bloom Energy expects total revenue between $1.65 billion and $1.85 billion, representing continued growth from 2024’s $1.5 billion. The company projects a non-GAAP gross margin of approximately 29% and non-GAAP operating income between $135 million and $165 million.

According to the earnings call, Bloom Energy anticipates stronger revenue growth in the second half of 2025. However, the company also acknowledged potential headwinds, including tariff impacts that could affect gross margins by up to 100 basis points.

Market Reaction & Analyst Perspectives

Despite the strong financial performance and positive outlook, Bloom Energy’s stock has faced downward pressure. Following the earnings release, the stock declined 3.23% in aftermarket trading on April 30, and continued to fall, closing down 8.24% at $16.81 on May 1.

This disconnect between financial performance and market reaction may reflect broader concerns about the clean energy sector or specific challenges facing Bloom Energy. According to available market data, analyst price targets for Bloom Energy range from $10 to $35, suggesting significant potential upside from current levels, though the stock is currently trading above some fair value estimates.

CEO KR Sreedhar expressed confidence during the earnings call, emphasizing Bloom’s competitive edge in on-site power generation and stating, "The sale on on-site power being necessary, that briefcase is closed." The company continues to focus on technology improvements and cost reductions to maintain its market position.

As Bloom Energy moves forward in 2025, investors will be watching closely to see if the company can maintain its positive momentum and deliver on its full-year guidance, particularly in light of potential tariff challenges and the expectation for stronger performance in the second half of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.