Oil prices push higher amid worries over Russian supply disruptions

Introduction & Market Context

Bloomin’ Brands, Inc. (NASDAQ:BLMN) presented its Q2 FY2025 earnings results on August 6, 2025, revealing a company facing significant profitability challenges despite modest revenue growth. The restaurant operator, which owns Outback Steakhouse, Carrabba’s Italian Grill, Bonefish Grill, and Fleming’s Prime Steakhouse & Wine Bar, reported a slight increase in total revenues but experienced substantial margin compression across key metrics.

The company’s stock has struggled in recent months, trading near $8.95 as of August 5, 2025, significantly below its 52-week high of $18.72. This earnings presentation comes after a more positive Q1 2025 report when the company exceeded analyst expectations with adjusted EPS of $0.59.

Quarterly Performance Highlights

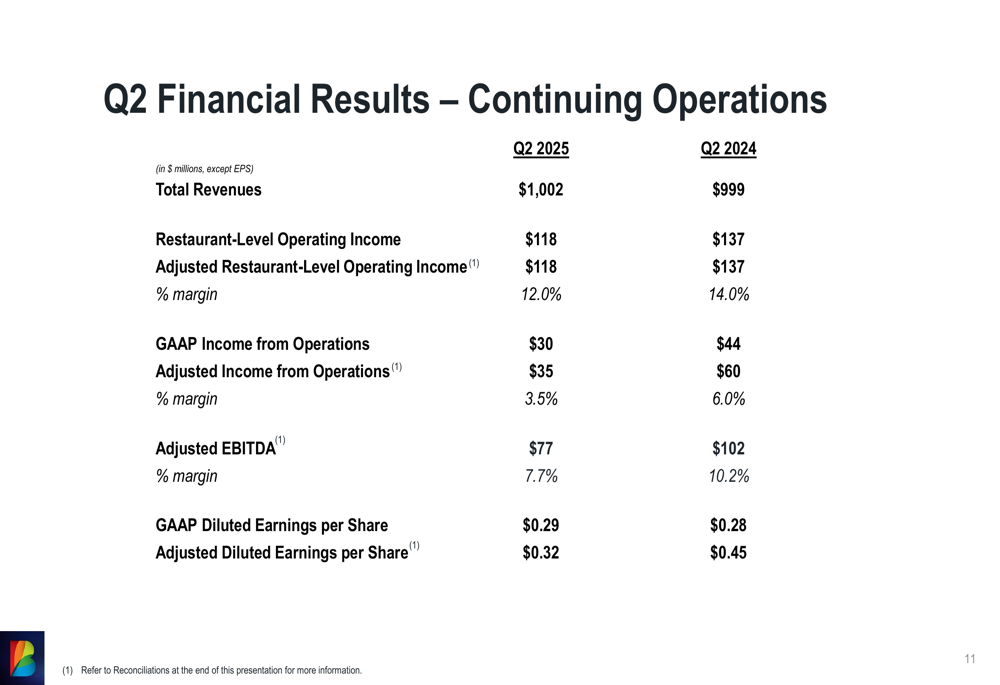

Bloomin’ Brands reported Q2 2025 total revenues of $1,002 million, a slight increase from $999 million in Q2 2024. However, profitability metrics showed significant deterioration year-over-year.

As shown in the following financial results summary:

Restaurant-level operating income fell to $118 million (12.0% margin) from $137 million (14.0% margin) in the prior year. Adjusted income from operations declined sharply to $35 million (3.5% margin) from $60 million (6.0% margin), while adjusted EBITDA dropped to $77 million (7.7% margin) from $102 million (10.2% margin).

Despite these challenges, GAAP diluted earnings per share increased slightly to $0.29 from $0.28, though adjusted diluted EPS fell significantly to $0.32 from $0.45 in Q2 2024.

These results reflect ongoing operational challenges, particularly with the company’s Outback Steakhouse brand, which management has specifically identified as needing a turnaround. The margin compression appears to be driven by continued inflationary pressures, with the company guiding to 3-3.5% commodity inflation and approximately 4% labor wage inflation for the full year.

Strategic Initiatives

Bloomin’ Brands outlined three key operating priorities to address current challenges:

The company is focusing on simplifying its agenda, delivering improved guest experiences, and specifically turning around its Outback Steakhouse brand. These priorities align with comments made during the Q1 earnings call, where CEO Mike Spannas acknowledged pricing challenges and the early stages of a turnaround effort.

The presentation also highlighted several organizational changes, including new leadership appointments across the company’s brands and corporate functions. These leadership changes appear designed to support the implementation of the company’s strategic priorities.

The company continues to position its restaurant portfolio as "iconic, founder-inspired brands," though the performance metrics suggest varying levels of success across the portfolio. The specific focus on turning around Outback Steakhouse indicates this flagship brand may be underperforming relative to others in the portfolio.

Brazil Transaction (JO:NTUJ) Update

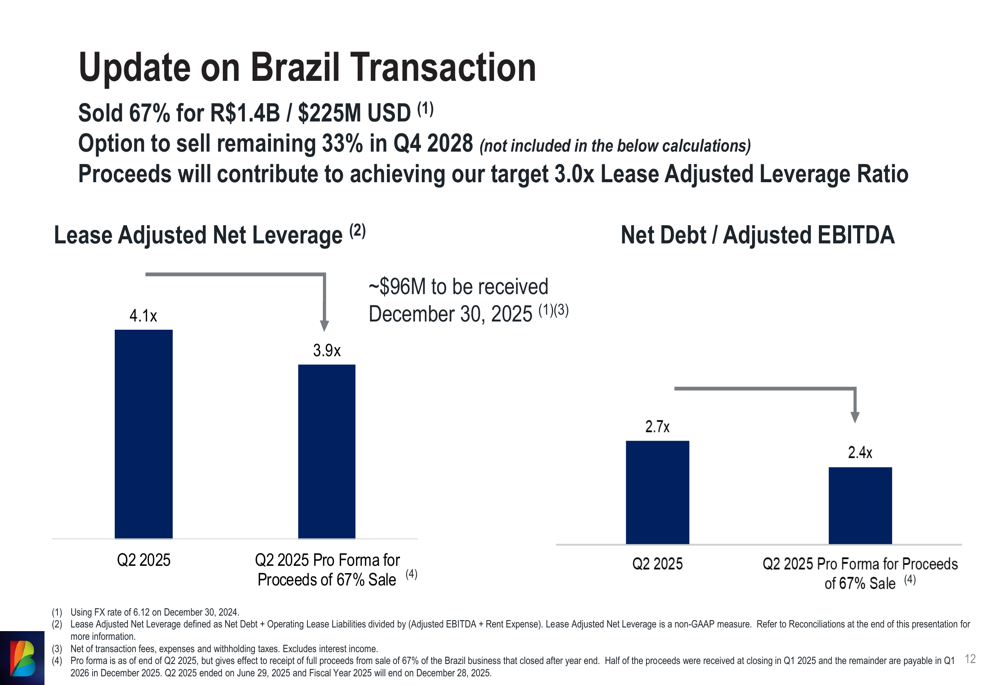

A significant development highlighted in the presentation is the partial divestiture of Bloomin’ Brands’ Brazil operations:

The company has sold 67% of its Brazil business for R$1.4 billion (approximately $225 million USD), with an option to sell the remaining 33% in Q4 2028. Management indicated that proceeds from this transaction will help achieve their target leverage ratio of 3.0x.

The transaction has already improved the company’s financial position, reducing lease-adjusted net leverage from 4.1x to 3.9x on a pro forma basis, and decreasing the net debt to adjusted EBITDA ratio from 2.7x to 2.4x. This balance sheet improvement provides some financial flexibility as the company works through its operational challenges.

Forward Guidance

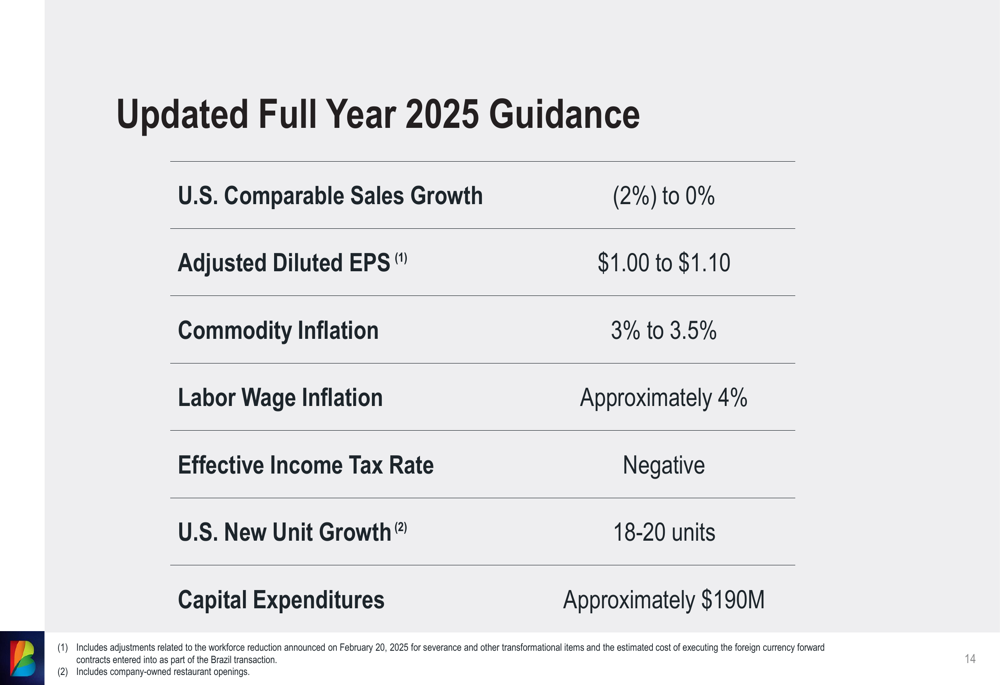

Bloomin’ Brands has lowered its full-year 2025 guidance, reflecting continued challenges:

The updated full-year guidance projects U.S. comparable sales growth between -2% and 0%, with adjusted diluted EPS of $1.00 to $1.10. This represents a reduction from the previous guidance of $1.20 to $1.40 provided during the Q1 earnings report.

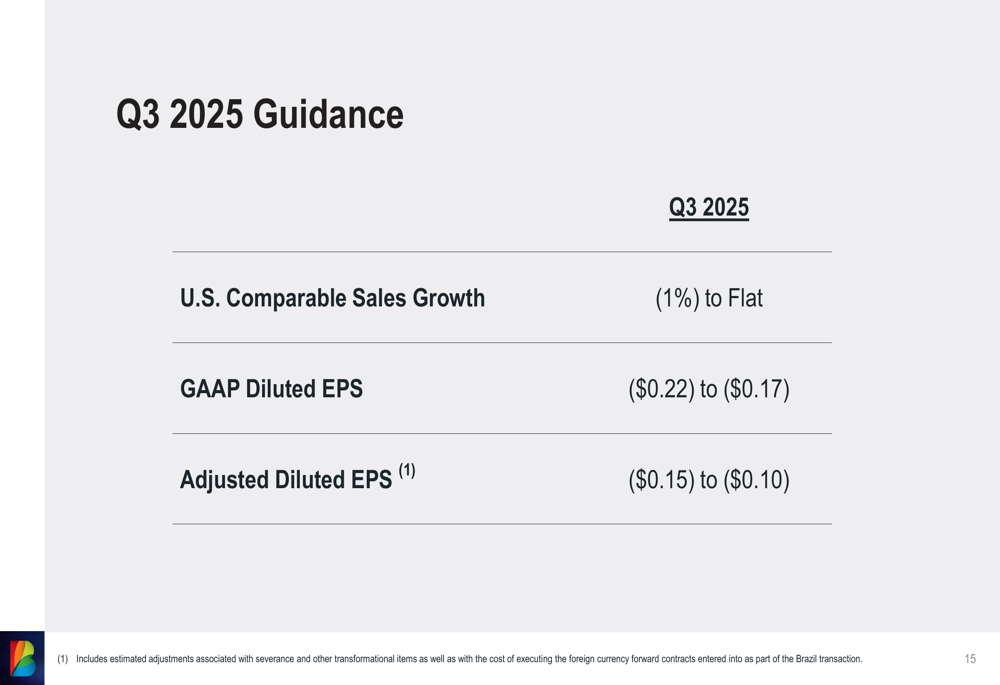

The near-term outlook appears even more challenging, with Q3 2025 guidance projecting negative earnings:

For Q3 2025, the company expects U.S. comparable sales growth between -1% and flat, with GAAP diluted EPS between -$0.22 and -$0.17, and adjusted diluted EPS between -$0.15 and -$0.10. This negative earnings projection for Q3 suggests continued margin pressure and operational challenges in the coming months.

Competitive Industry Position

Bloomin’ Brands operates in a highly competitive casual dining segment that continues to face macroeconomic pressures. The Q1 earnings report highlighted declining U.S. traffic (-3.9%) and challenges with competitive pricing, issues that appear to have persisted into Q2.

The company’s portfolio approach allows it to target different segments of the dining market, from the mainstream appeal of Outback Steakhouse to the premium positioning of Fleming’s Prime Steakhouse & Wine Bar. However, the specific focus on turning around Outback suggests this key brand may be losing market share to competitors.

Conclusion

Bloomin’ Brands’ Q2 2025 presentation reveals a company in transition, facing significant profitability challenges despite maintaining relatively stable revenues. The reduced guidance and projected negative earnings for Q3 indicate continued headwinds, though strategic initiatives focused on simplification and improved guest experiences could potentially drive improvement in future quarters.

The Brazil transaction provides some balance sheet relief, but investors will likely remain focused on operational execution, particularly the turnaround of the Outback brand. With the stock trading near its 52-week low and a dividend yield of approximately 7.57% (based on previous earnings data), the company’s ability to stabilize margins while maintaining its dividend will be closely watched in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.