Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

Boise Cascade (NYSE:BCC) reported second-quarter 2025 results on August 5, showing significant year-over-year declines in both revenue and earnings as the company continues to navigate a challenging housing market environment. The stock closed at $82.71, up 0.79% on the day, but remains near its 52-week low of $80.30, reflecting ongoing investor concerns about the building products sector.

The company’s performance continues to be impacted by affordability challenges, elevated existing home inventory, and cautious consumer sentiment, despite some seasonal improvement in activity. These results follow a disappointing first quarter where Boise Cascade missed earnings expectations but slightly exceeded revenue forecasts.

Quarterly Performance Highlights

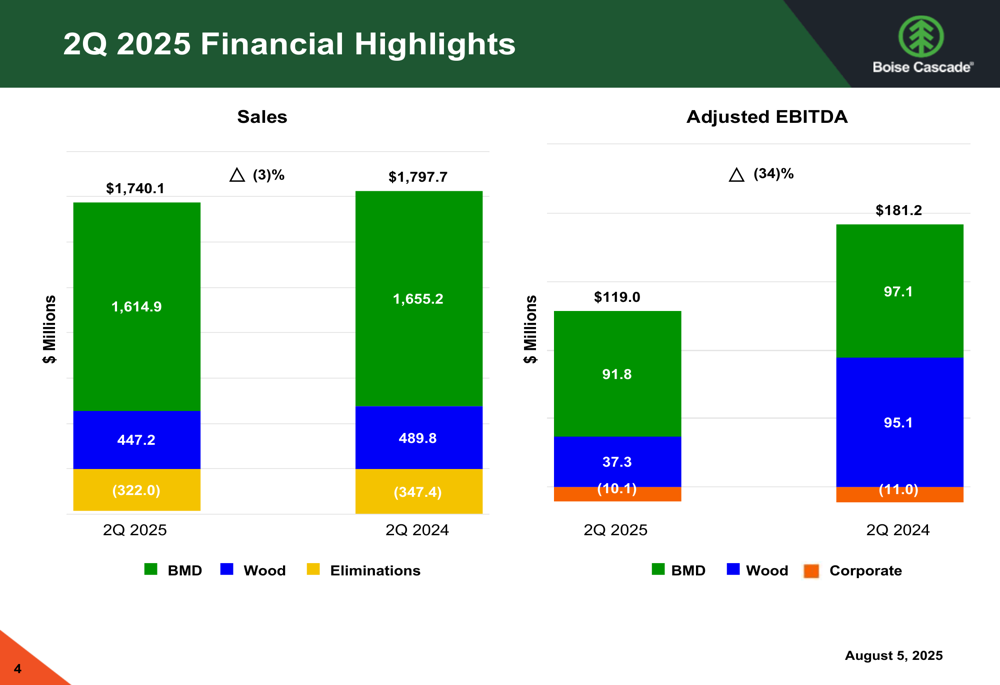

Boise Cascade reported second-quarter 2025 sales of $1.7 billion, representing a 3% decrease compared to the same period in 2024. Net income fell more sharply to $62.0 million ($1.64 per share), down from $112.3 million ($2.84 per share) in Q2 2024, representing a 42% decline in earnings per share.

Adjusted EBITDA for the quarter was $119.0 million, a 34% decrease from $181.2 million in the prior-year period. The quarter’s results include pre-tax gains of $7.7 million on non-operating asset sales, which partially offset the overall decline.

As shown in the following chart of sales and adjusted EBITDA comparison between Q2 2025 and Q2 2024:

The Building Materials Distribution (BMD) segment was particularly impacted, with segment EBITDA declining to $91.8 million from $97.1 million in Q2 2024. Meanwhile, Wood Products segment EBITDA fell more dramatically to $37.3 million from $95.1 million in the prior-year period.

Segment Performance Analysis

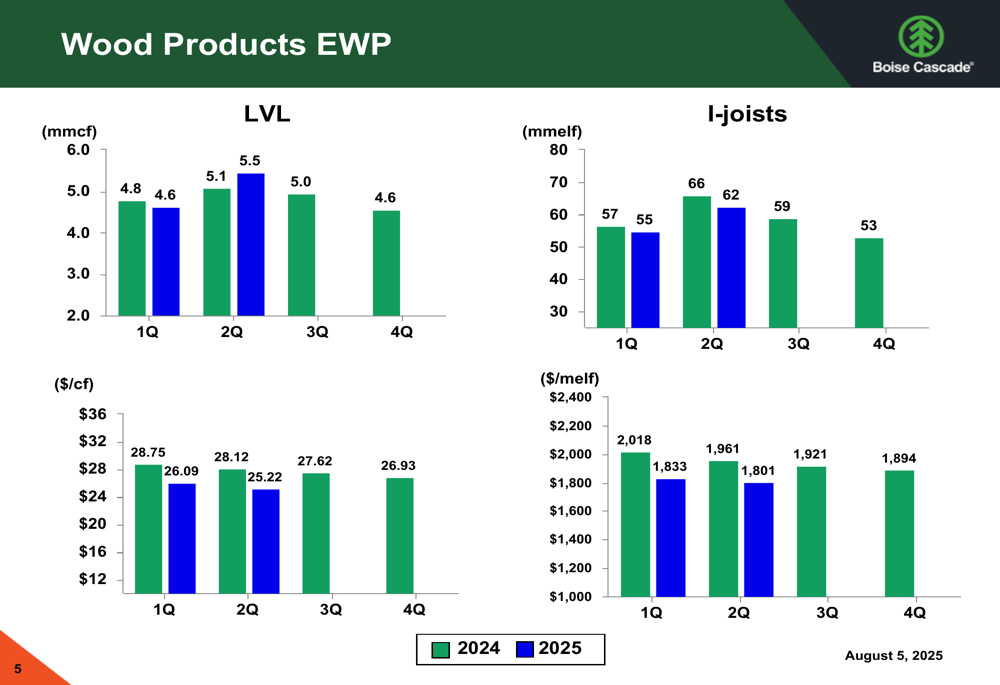

The Wood Products segment showed mixed volume trends but consistent price pressure across product categories. For Engineered Wood Products (EWP), LVL (Laminated Veneer Lumber) volumes increased to 5.5 million cubic feet in Q2 2025 from 5.1 million cubic feet in Q2 2024, but prices declined to $25.22 per cubic foot from $28.12 in the prior year. Similarly, I-Joist volumes grew to 66 million linear feet from 62 million linear feet, while prices fell to $1,801 per thousand linear feet from $1,961.

The following chart illustrates these trends in the Wood Products EWP segment:

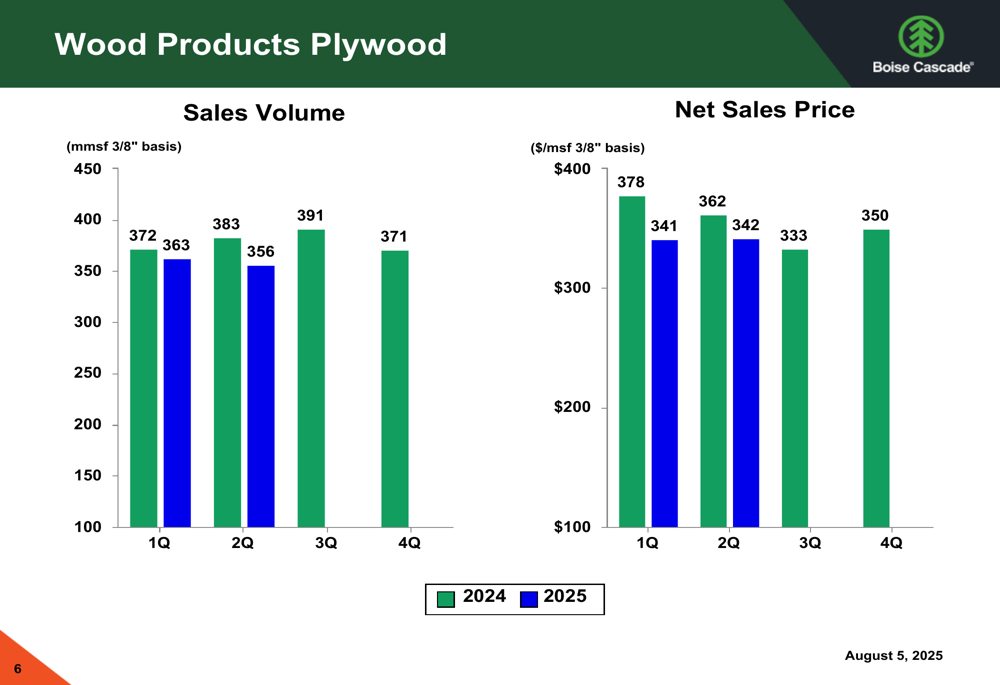

Plywood performance was more challenged, with sales volumes decreasing to 356 million square feet (3/8" basis) in Q2 2025 from 383 million square feet in Q2 2024. Net sales prices were also lower at $342 per thousand square feet compared to $362 in the prior-year period.

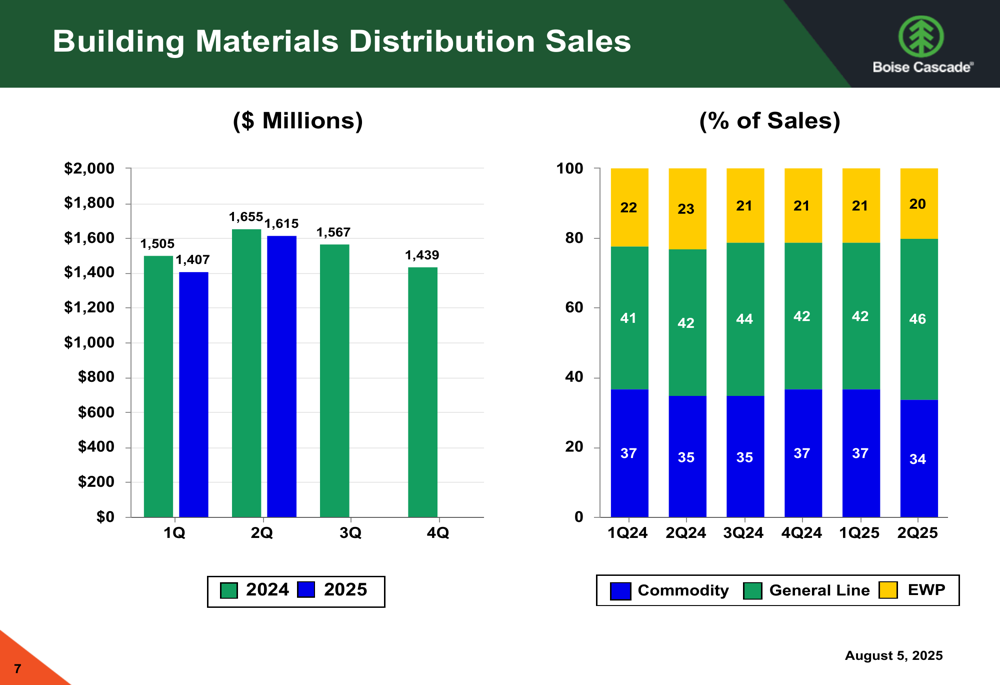

In the Building Materials Distribution segment, sales declined to $1,615 million in Q2 2025 from $1,655 million in Q2 2024. The product mix shifted notably, with General Line products increasing to 46% of sales (from 42% in Q2 2024), while EWP decreased to 20% (from 23%) and Commodity products declined to 34% (from 35%).

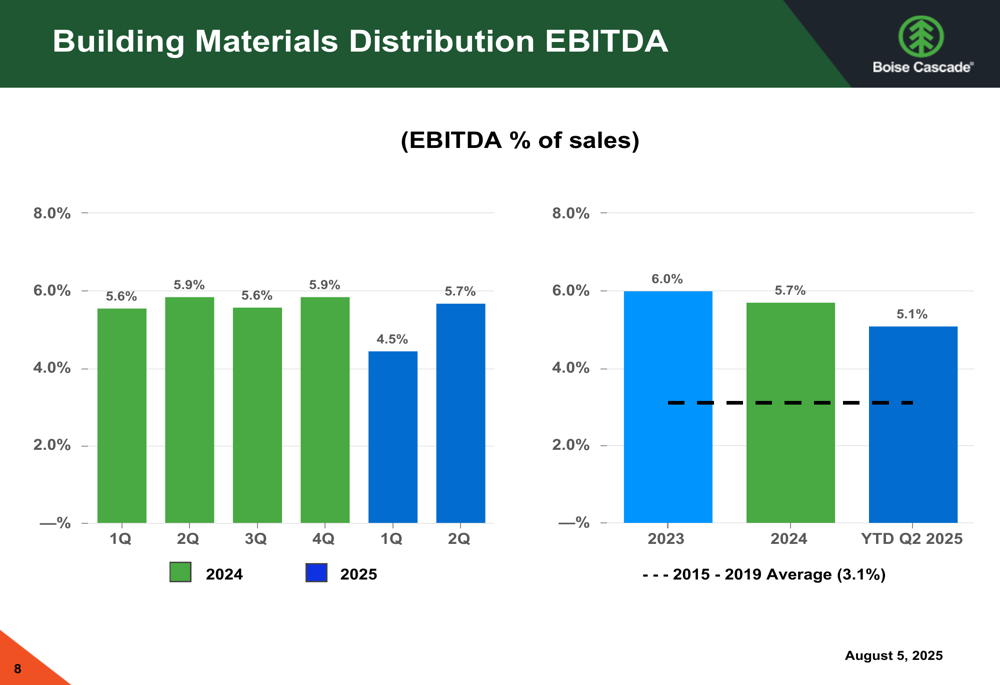

The following chart shows BMD sales trends and product mix changes:

Despite the challenging environment, BMD’s EBITDA as a percentage of sales remained relatively resilient at 5.7% in Q2 2025, only slightly below the 5.9% recorded in Q2 2024, but still well above the 2015-2019 average of 3.1%.

Capital Allocation & Shareholder Returns

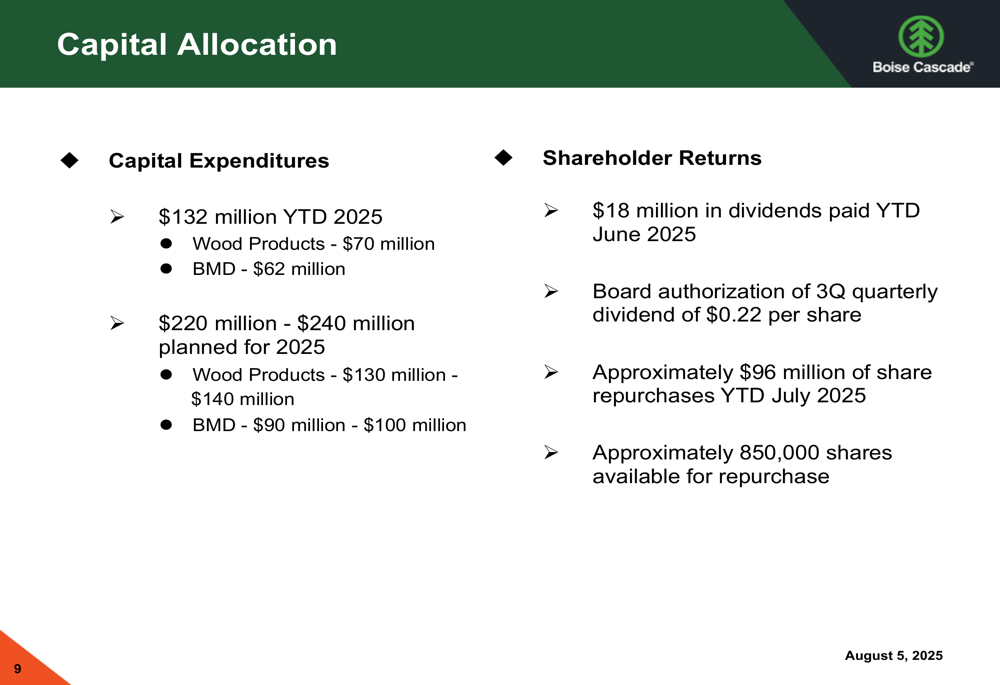

Despite the earnings pressure, Boise Cascade has maintained its commitment to both capital investments and shareholder returns. The company reported $132 million in capital expenditures year-to-date in 2025, with $70 million allocated to Wood Products and $62 million to BMD. For the full year 2025, Boise Cascade plans capital expenditures of $220-240 million.

On the shareholder return front, the company paid $18 million in dividends year-to-date through June 2025 and has authorized a Q3 quarterly dividend of $0.22 per share. Additionally, Boise Cascade has conducted approximately $96 million in share repurchases year-to-date through July 2025, with approximately 850,000 shares still available for repurchase under the current authorization.

The following chart details the company’s capital allocation strategy:

Forward Outlook

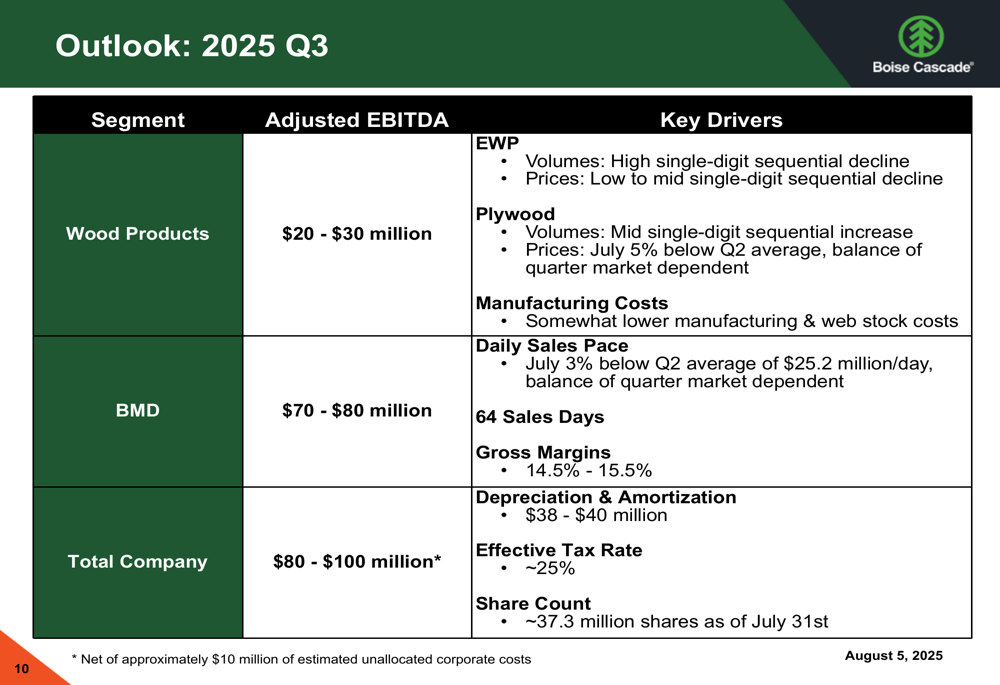

Looking ahead to the third quarter of 2025, Boise Cascade provided a cautious outlook, forecasting total company Adjusted EBITDA of $80-100 million, which would represent a sequential decline from Q2 levels. This guidance reflects expectations of continued challenges in both major segments.

For Wood Products, the company expects Adjusted EBITDA of $20-30 million in Q3, with EWP volumes projected to decline by high single digits sequentially and prices expected to fall by low to mid-single digits. Plywood volumes are anticipated to increase by mid-single digits, but July prices were already 5% below the Q2 average.

In the BMD segment, Adjusted EBITDA is projected at $70-80 million for Q3, with the daily sales pace in July running 3% below the Q2 average of $25.2 million per day. Gross margins are expected to range between 14.5% and 15.5%.

The detailed Q3 2025 outlook is presented in the following chart:

Strategic Initiatives

Despite near-term challenges, Boise Cascade continues to invest in its long-term growth strategy. The company noted that its Oakdale modernization project is substantially complete, which should enhance operational efficiency moving forward.

Management emphasized its commitment to aligning production rates and inventory strategies with demand while maintaining a positive view of long-term demand drivers for residential construction and repair & remodel activity. The company plans to continue investing in wood products assets throughout the business cycle, positioning itself to capitalize on what it describes as a "distribution-friendly demand environment."

"We remain focused on our long-term strategy while navigating the current market challenges," the company stated in its presentation, highlighting the balance between short-term performance management and long-term growth investments.

Market Context

Boise Cascade’s performance reflects broader challenges in the housing and building products markets. The company’s Q1 2025 earnings call had highlighted that housing starts were down 26% with single-family starts below 1 million annually, and the Q2 results suggest these headwinds have persisted.

The stock has continued its downward trend, falling from $92.47 after Q1 results to the current $82.71, approaching its 52-week low. This decline reflects investor concerns about the company’s ability to maintain profitability in the current environment, despite its strong dividend yield and strategic investments.

As the company navigates these challenges, its focus on maintaining operational flexibility while continuing to invest in long-term growth capabilities will be crucial to its ability to weather the current housing market downturn and position itself for recovery when market conditions improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.