S&P 500 jumps as tech rallies as investors eye end of government shutdown

Introduction & Market Context

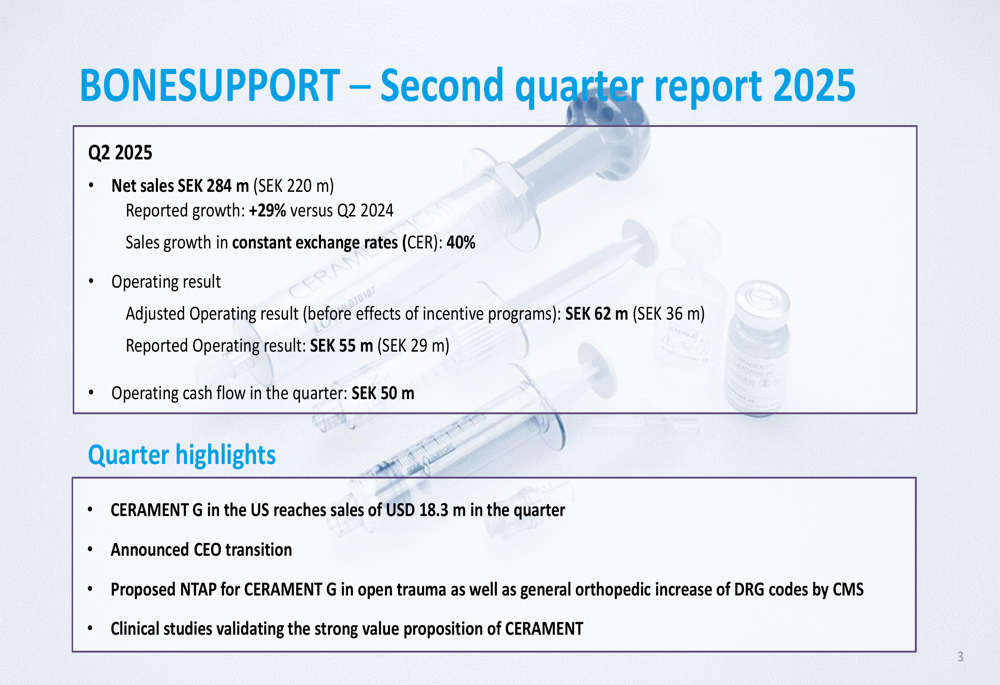

Bonesupport Holding AB (STO:BONEX) presented its Q2 2025 results on July 15, showing continued strong growth despite currency headwinds. The Swedish medical technology company, which specializes in injectable bone substitutes, reported a 29% increase in net sales compared to the same period last year, though this figure rises to 40% when measured in constant exchange rates (CER).

The company’s stock closed at SEK 296.6, down 0.94% on the day of the report, reflecting a slight pullback from its position after Q1 results when it traded at SEK 317.4. This comes after a quarter that showed solid performance but at a somewhat moderated pace compared to the exceptional 54% growth reported in Q1 2025.

Quarterly Performance Highlights

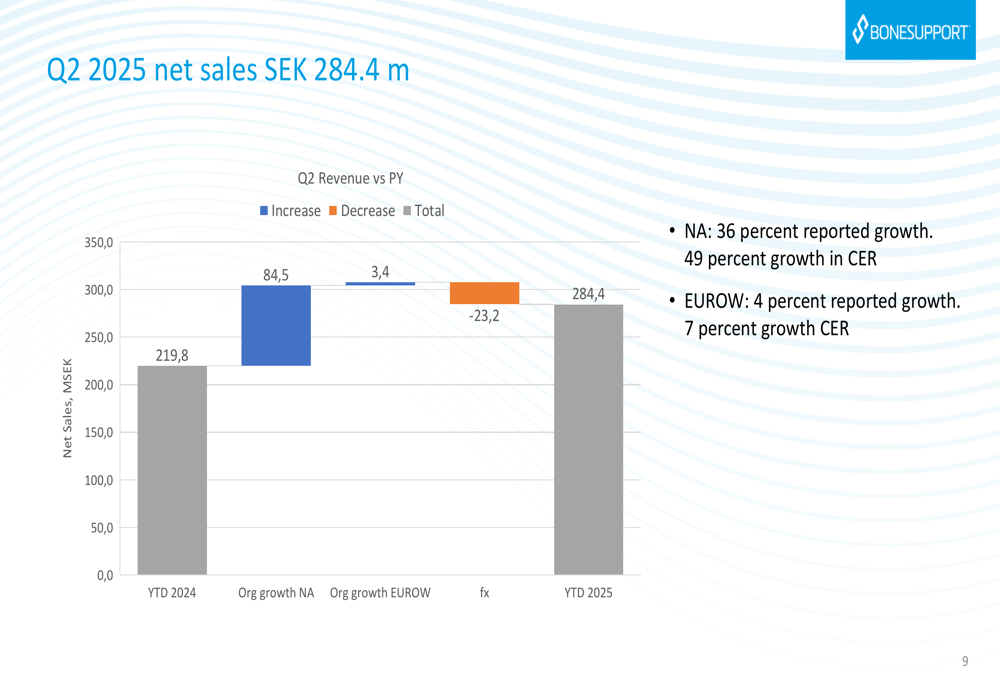

Bonesupport reported net sales of SEK 284 million for Q2 2025, representing a 29% increase over Q2 2024 on a reported basis. When adjusting for currency effects, particularly the USD/SEK depreciation, growth reached 40% in constant exchange rates.

The company achieved an adjusted operating result (before effects of incentive programs) of SEK 62 million, while the reported operating result stood at SEK 55 million. Operating cash flow remained strong at SEK 50 million for the quarter.

As shown in the following quarterly highlights slide:

The gross margin remained robust at 92.3%, only slightly below the 95% reported in Q1 2025. This high margin reflects the company’s efficient production and premium positioning in the bone graft substitute market.

Regional Performance Analysis

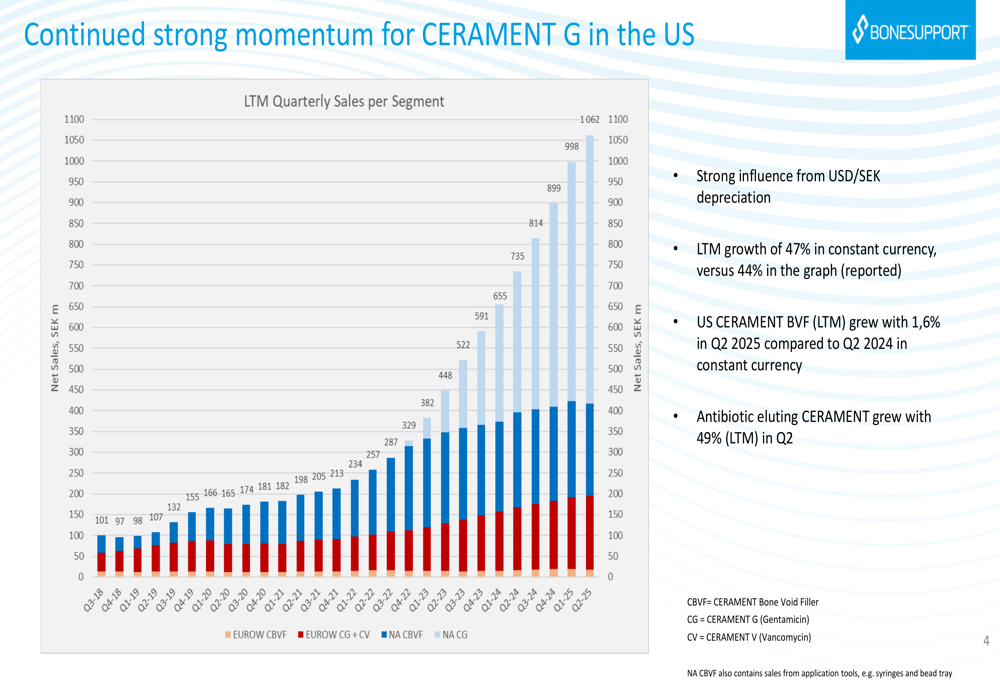

North America continues to be the primary growth driver for Bonesupport, with regional sales reaching SEK 236 million, representing a 36% increase (49% in CER) compared to Q2 2024. The company’s antibiotic-eluting CERAMENT G product has been particularly successful in the US market, generating USD 18.3 million in quarterly sales.

The following chart illustrates the momentum of CERAMENT G in the US market and the company’s overall sales trajectory:

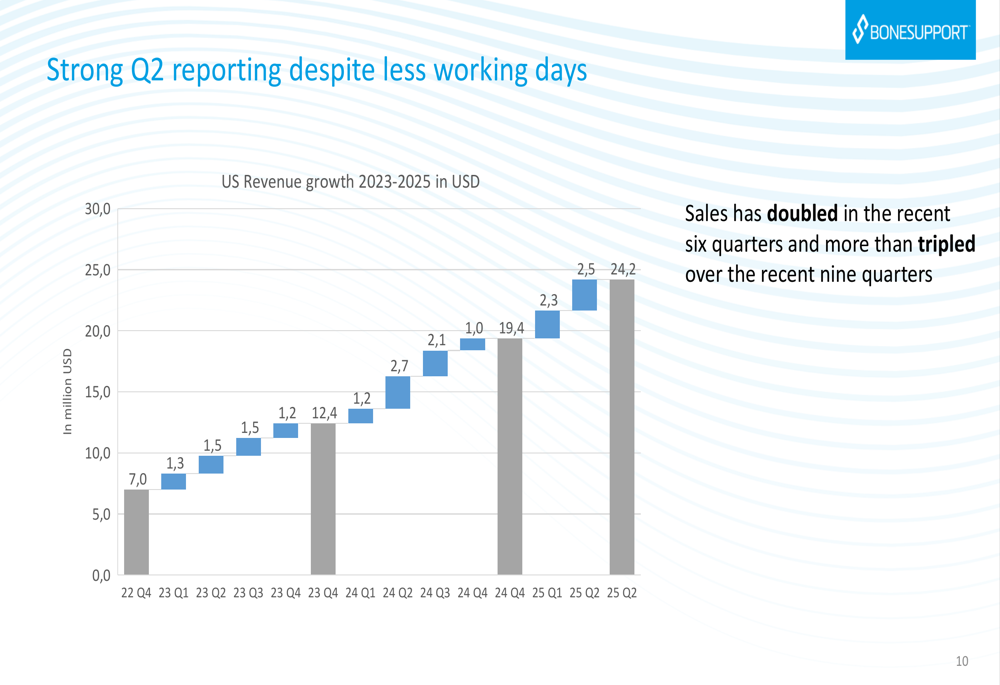

US revenue growth has been particularly impressive, with sales doubling over the past six quarters and more than tripling over the past nine quarters. The sequential growth pattern is clearly visible in this waterfall chart showing the steady revenue increases:

Meanwhile, performance in Europe and Rest of World (EUROW) was more modest but still positive, with sales of SEK 48.8 million representing 4% growth (7% in CER) compared to Q2 2024. The company noted ongoing hospital reforms and surgical protocol programs in Germany as factors affecting regional performance.

Strategic Initiatives & Market Expansion

A key strategic development highlighted in the presentation is Bonesupport’s planned entry into the spinal procedure market in North America. The company’s CERAMENT BVF product has regulatory approval for posterolateral procedures and interbody applications, with a launch planned for December 2025.

The company has conducted pre-clinical application studies with positive results and is currently recruiting a network of independent spine distributors while establishing a surgery advisory panel. This expansion represents a significant new market opportunity for Bonesupport’s bone substitute technology.

In the existing markets, Bonesupport continues to build clinical evidence supporting its products’ efficacy. The company highlighted studies on diabetic foot infection and open trauma, providing numerical results that validate the strong value proposition of CERAMENT.

Financial Health & Profitability Trends

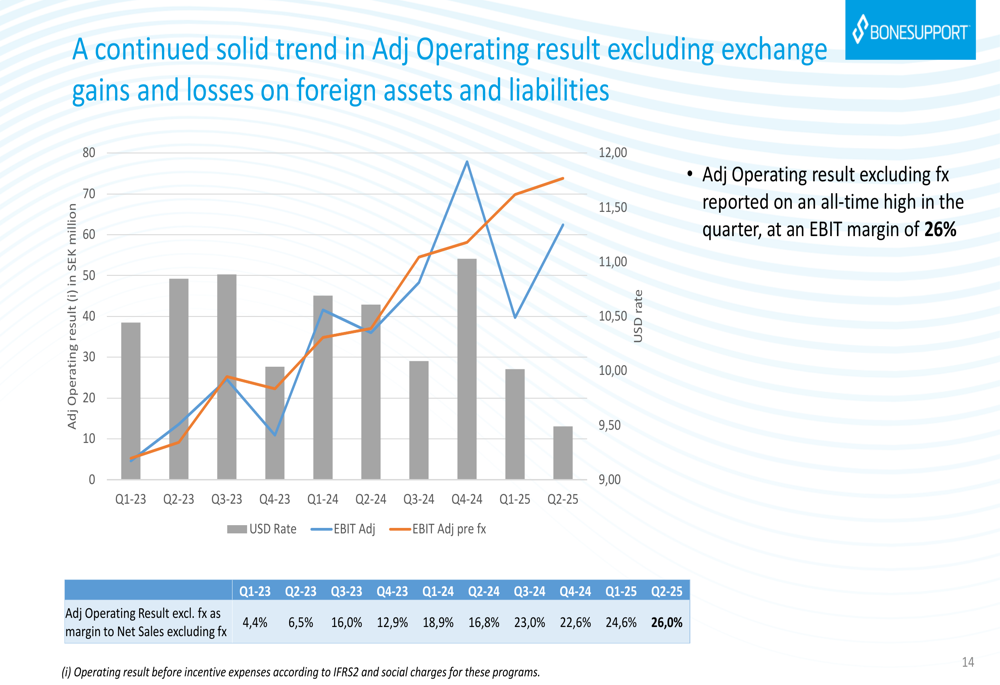

Bonesupport’s financial results demonstrate improving business scalability and profitability trends. The adjusted operating result excluding foreign exchange effects reached an all-time high in Q2 2025, with an EBIT margin of 26%.

As illustrated in the following chart showing the adjusted operating result trend:

This represents a consistent improvement from 4.4% in Q1 2023 to the current 26.0% in Q2 2025, demonstrating the company’s ability to scale operations efficiently as revenue grows.

The company’s net sales breakdown by region and growth components is clearly visualized in this chart:

Cash position remains strong, with SEK 309.7 million at the end of the period, supported by the SEK 50 million in operating cash flow generated during the quarter.

Forward-Looking Statements

Looking ahead, Bonesupport expects sales growth to exceed 40% (in CER) for the full fiscal year 2025. This guidance is supported by the continued strong performance of CERAMENT G in the US market and planned expansion into new applications.

The company also highlighted several potential catalysts, including a proposed New Technology Add-on Payment (NTAP) for CERAMENT G in open trauma, as well as general orthopedic increases of DRG codes by the Centers for Medicare & Medicaid Services (CMS).

Additionally, the company announced a CEO transition, though specific details about timing and succession were not elaborated in the presentation.

The spinal procedures market entry planned for December 2025 represents a significant growth opportunity, with the company planning to build further spine application techniques and initiate clinical data generation within 12 months of launch.

Despite currency headwinds and a slight moderation in growth rate compared to Q1, Bonesupport’s Q2 2025 results demonstrate continued strong execution of its strategy, with particular success in the US market driven by its antibiotic-eluting CERAMENT G product.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.