Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Booking Holdings Inc. (NASDAQ:BKNG) presented its second quarter 2025 earnings results on July 29, revealing strong financial performance across key metrics despite facing some market skepticism. The travel giant reported significant growth in revenue, profitability, and operational metrics, while continuing to advance strategic initiatives in alternative accommodations and connected trip offerings.

Quarterly Performance Highlights

Booking Holdings delivered impressive financial results for Q2 2025, with revenue reaching $6.8 billion, representing a 16% year-over-year increase and exceeding the high end of guidance by four percentage points. The company’s constant currency revenue growth was approximately 12%.

As shown in the following chart of quarterly revenue growth:

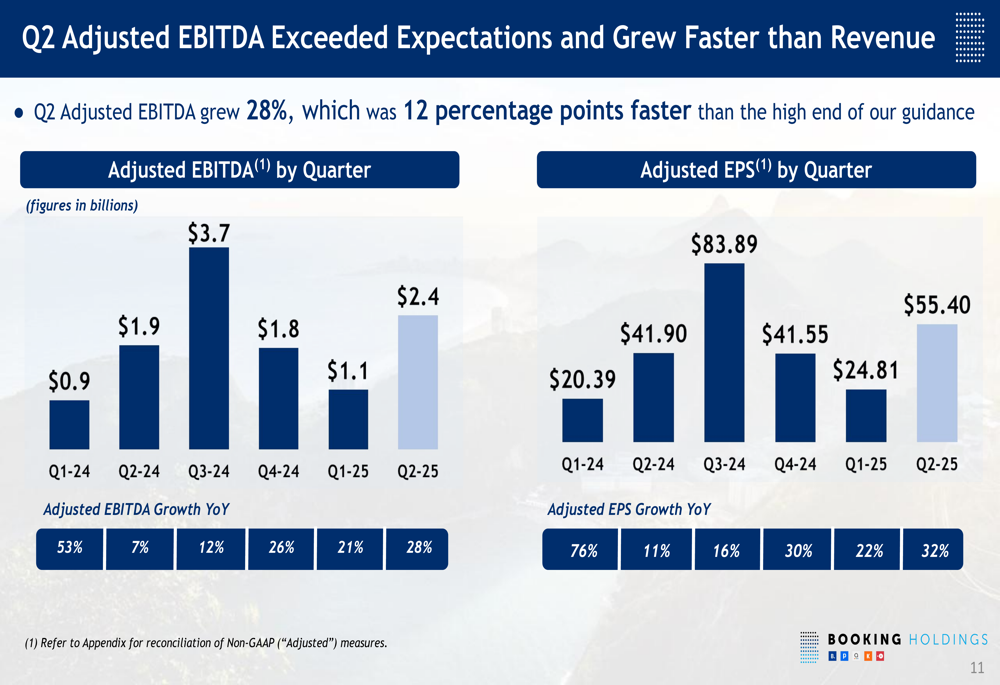

The company’s profitability metrics showed even stronger improvement, with adjusted EBITDA growing 28% year-over-year to $2.4 billion. Adjusted earnings per share reached $55.40, a 32% increase compared to Q2 2024, significantly outpacing revenue growth.

The following chart illustrates the company’s adjusted EBITDA and EPS growth:

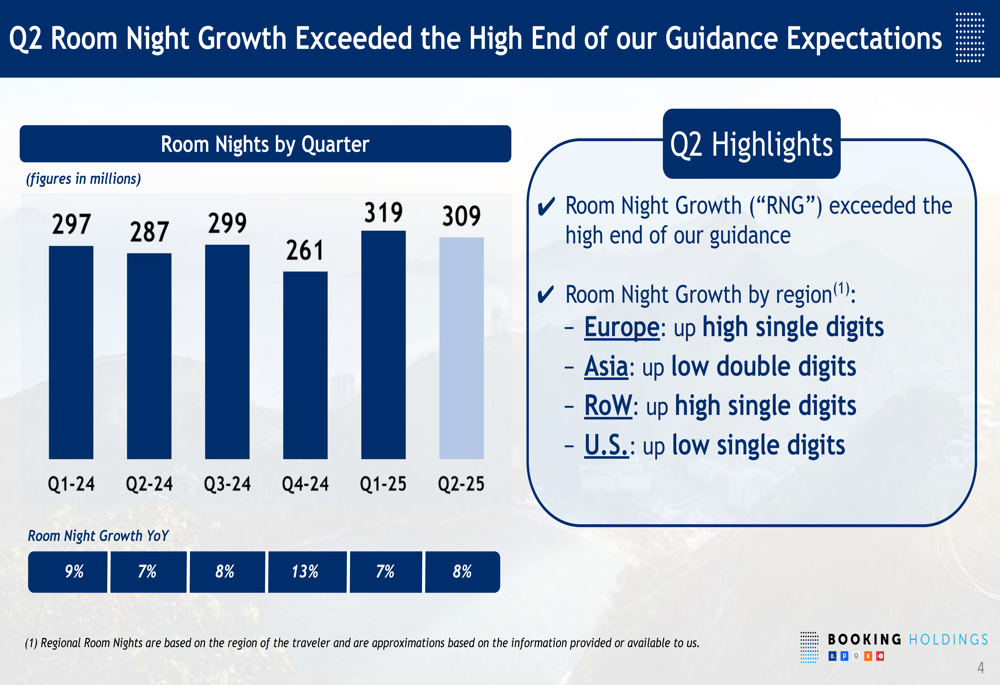

Room night growth, a key operational metric, increased by 8% year-over-year to 309 million, exceeding the high end of guidance. This growth varied by region, with Europe up high single digits, Asia up low double digits, Rest of World up high single digits, and the U.S. up low single digits.

The following visualization shows room night growth by quarter:

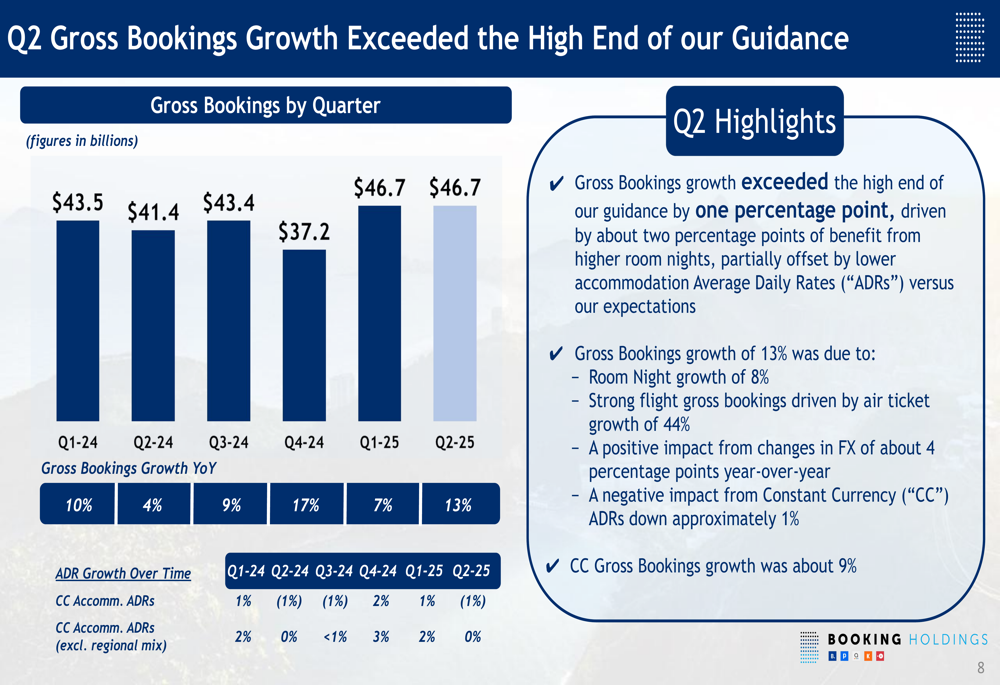

Gross bookings, which represent the total dollar value of all travel services booked, grew 13% year-over-year to $46.7 billion. This growth was driven by room night growth, strong flight bookings (up 44%), and a positive 4 percentage point impact from foreign exchange, partially offset by slightly lower accommodation average daily rates.

The following chart details gross bookings growth:

Strategic Initiatives

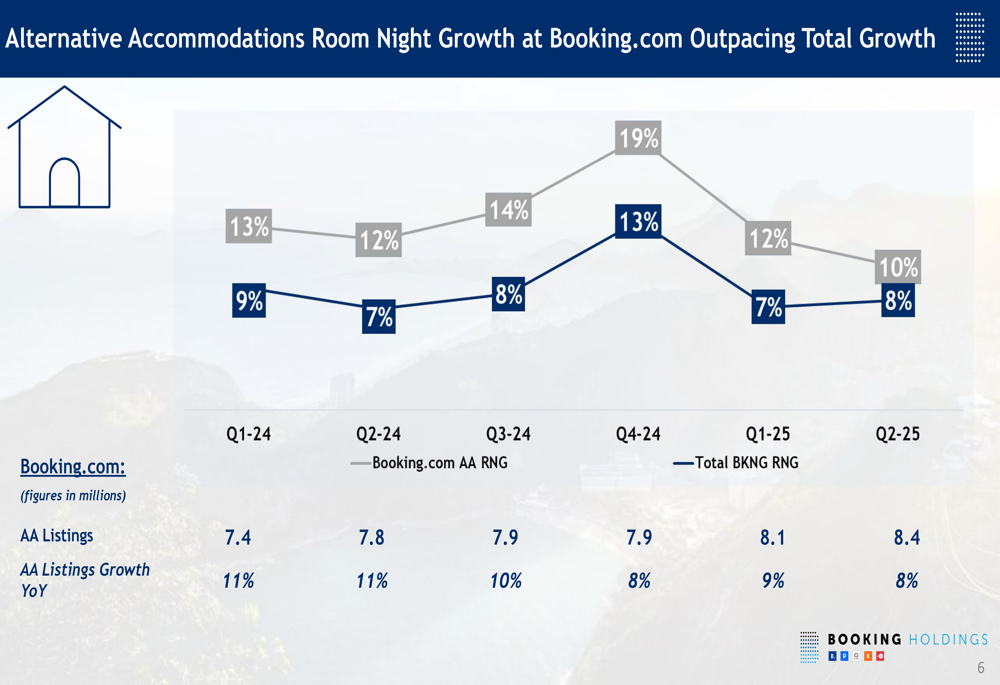

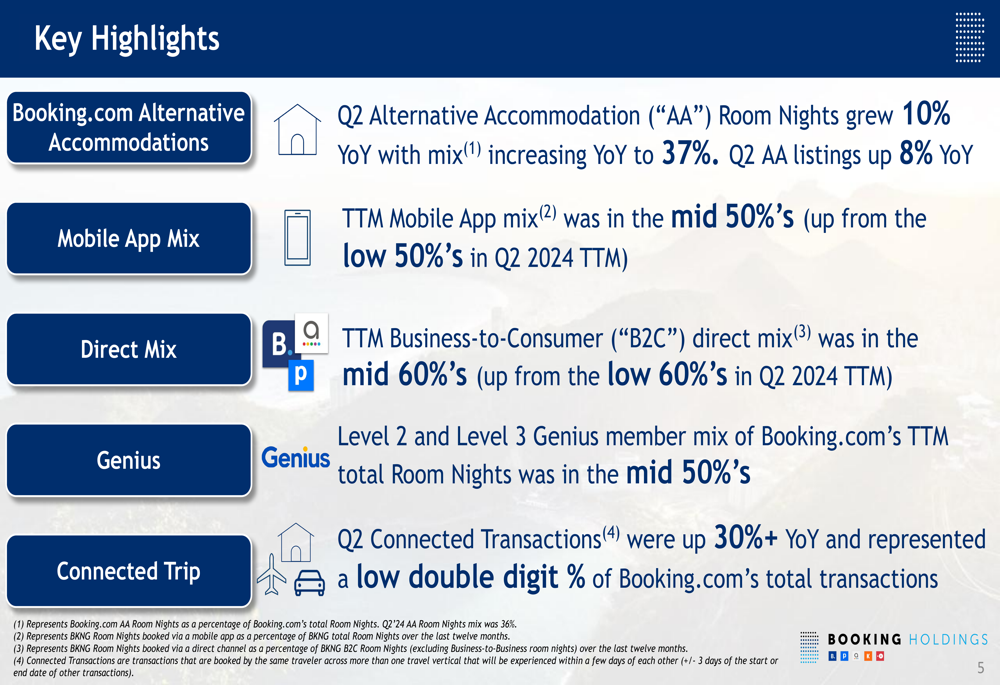

Booking Holdings continues to make progress on key strategic initiatives, particularly in alternative accommodations and mobile app usage. Alternative accommodation room nights grew 10% year-over-year in Q2 2025, outpacing overall room night growth, with alternative accommodations representing 37% of total room nights, an increase from the previous year.

The company’s alternative accommodation listings increased by 8% year-over-year to 8.4 million, demonstrating continued investment in this competitive segment.

As shown in the following chart comparing alternative accommodations growth to total room night growth:

Mobile app usage continues to increase, with the trailing twelve months mobile app mix reaching the mid-50% range, up from the low 50% range in Q2 2024. This growth in direct mobile bookings helps strengthen customer relationships and reduce dependency on third-party channels.

The company’s "connected trip" strategy is showing strong momentum, with connected transactions growing over 30% year-over-year and now representing a low double-digit percentage of Booking.com’s total transactions.

The following slide highlights key strategic achievements:

Forward-Looking Statements

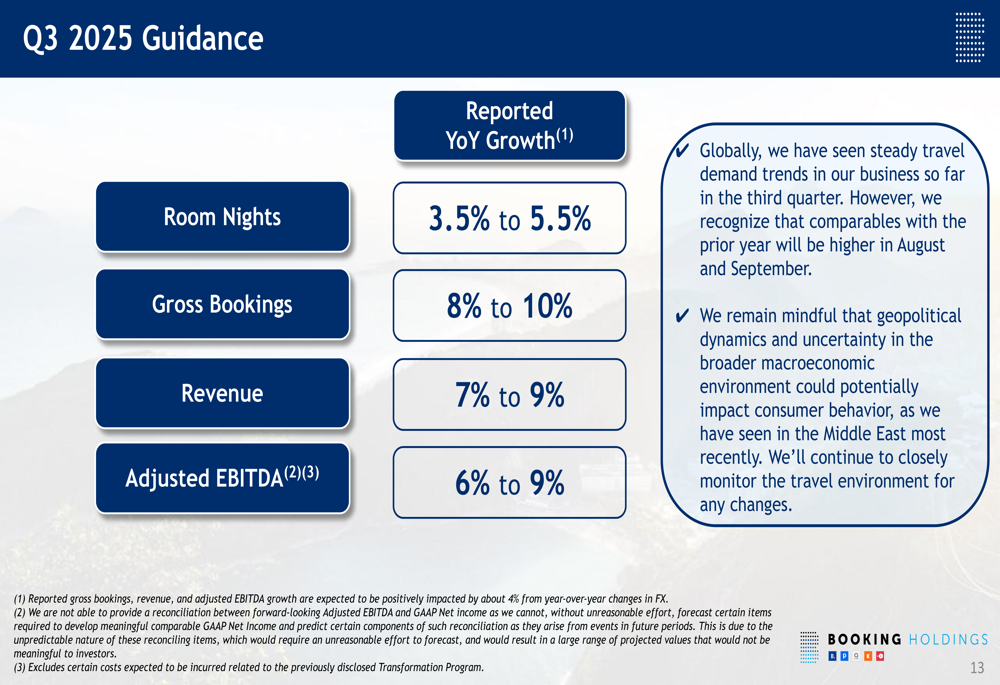

For the third quarter of 2025, Booking Holdings provided guidance for room night growth of 3.5% to 5.5%, gross bookings growth of 8% to 10%, revenue growth of 7% to 9%, and adjusted EBITDA growth of 6% to 9%. Management noted steady global travel demand but remained cautious about potential impacts from geopolitical dynamics and macroeconomic conditions.

As shown in the following Q3 2025 guidance slide:

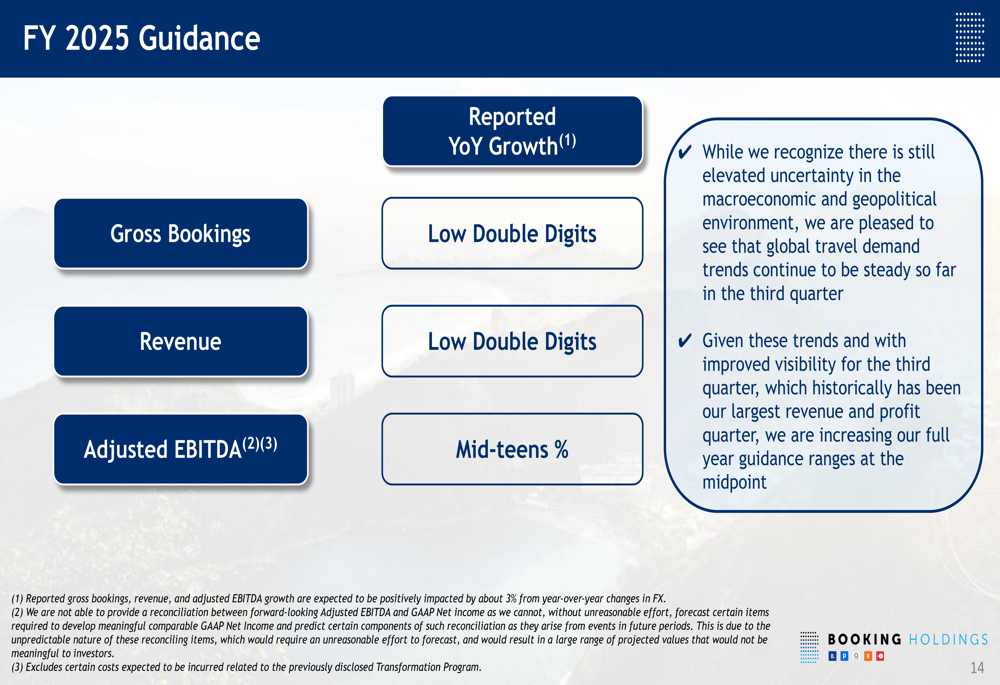

For the full year 2025, the company increased its guidance, now expecting low double-digit growth in gross bookings and revenue, with adjusted EBITDA growth in the mid-teens percentage range.

The following slide presents the full-year 2025 guidance:

Market Reaction

Despite the strong financial performance, Booking Holdings’ stock has faced selling pressure. According to the provided data, the stock closed down 1.55% at $5,590.77 on July 29, 2025, and was trading down an additional 1.91% in premarket trading on July 30, reaching $5,483.95.

This market reaction suggests investors may be concerned about the sustainability of growth rates or potential headwinds in the travel sector, despite the company’s strong execution and improved guidance. The stock has traded between $3,180 and $5,839.41 over the past 52 weeks.

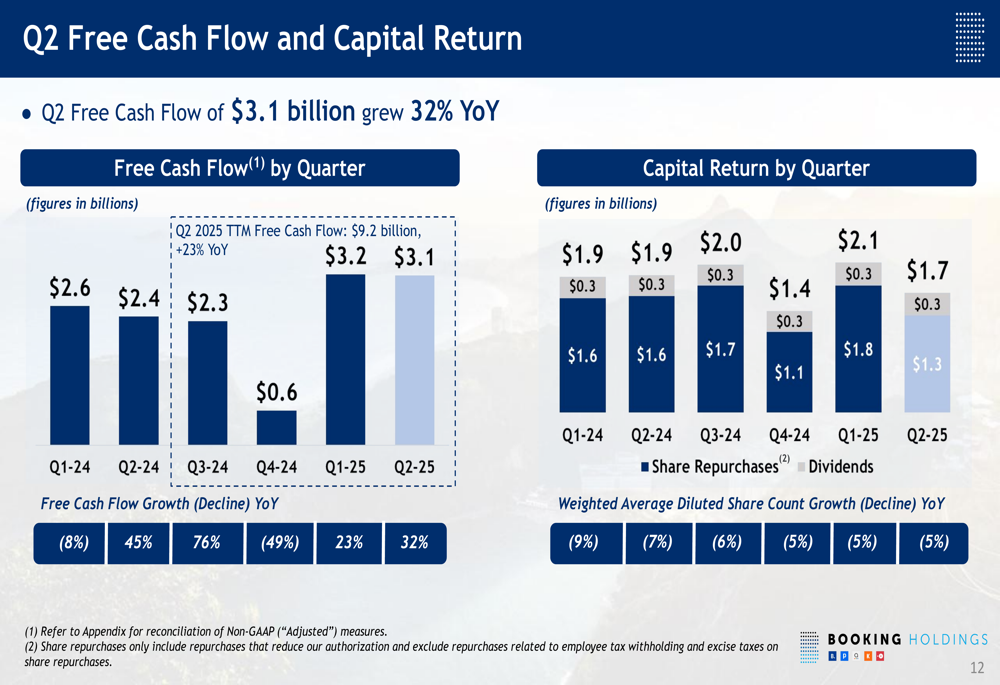

Booking Holdings continues to return capital to shareholders, with $1.3 billion in share repurchases and $0.3 billion in dividends during Q2 2025. The company’s free cash flow reached $3.1 billion for the quarter, a 32% increase year-over-year, and $9.2 billion for the trailing twelve months, up 23% from the previous year.

The following chart illustrates the company’s free cash flow and capital return:

With strong financial results across key metrics and continued progress on strategic initiatives, Booking Holdings appears well-positioned to navigate the evolving travel landscape, though market sentiment remains cautious as reflected in recent stock performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.