S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

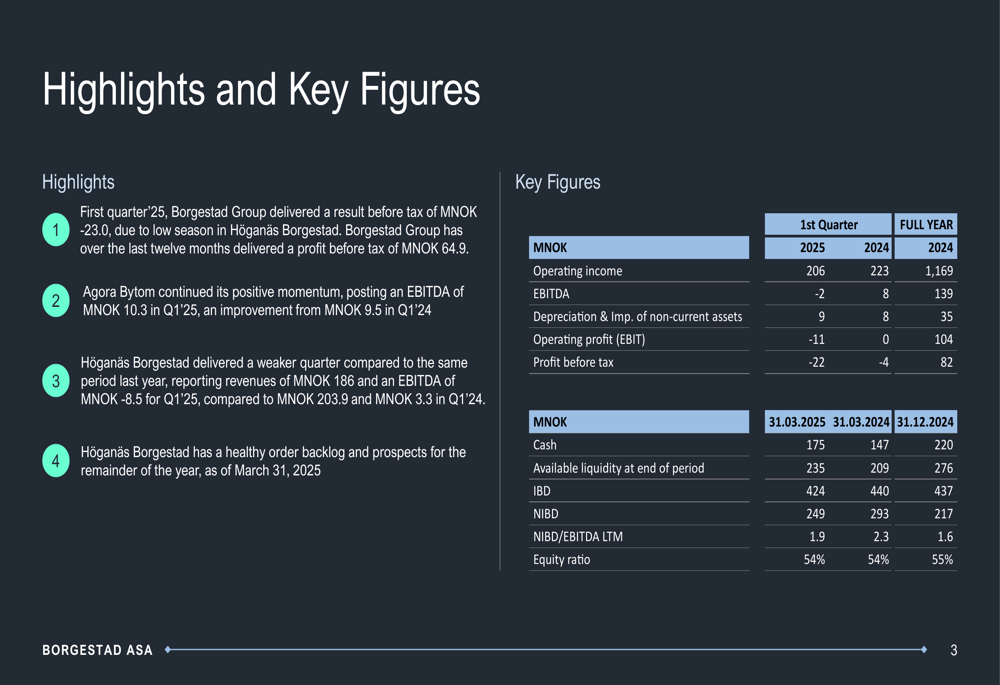

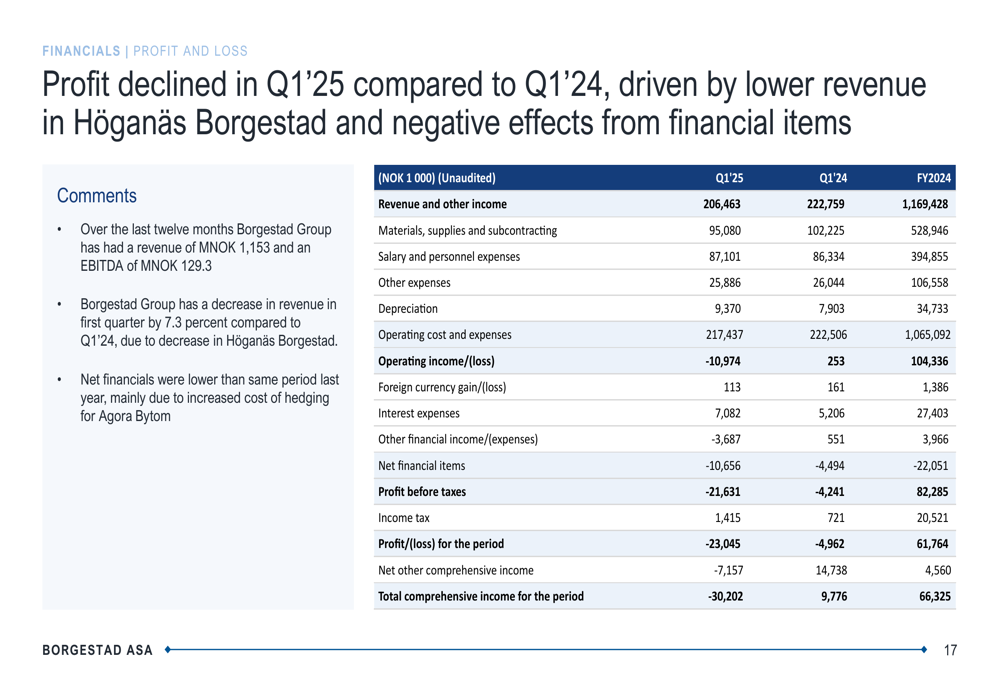

Borgestad ASA (OB:BOR) presented its first quarter 2025 financial results on May 22, 2025, revealing a challenging start to the year with a widening loss before tax of MNOK -23.0 compared to MNOK -4.2 in Q1 2024. The Norwegian industrial investment company, which focuses on real estate and refractory businesses, saw its stock decline 1.12% to NOK 17.7 following the presentation, continuing a downward trend after reaching a 52-week high of NOK 20.4.

The company’s performance reflects a stark contrast between its two main business segments: the Polish shopping center Agora Bytom continued to perform well, while the refractory business Höganäs Borgestad faced significant headwinds. This mixed performance comes after a strong finish to 2024, when the company reported its first annual profit in years and announced its first dividend since 2011.

Quarterly Performance Highlights

Borgestad’s Q1 2025 operating income fell to MNOK 206 from MNOK 223 in the same period last year, representing a 7.6% decline. The company reported negative EBITDA of MNOK -2 compared to positive MNOK 8 in Q1 2024, while operating profit (EBIT) deteriorated to MNOK -11 from breakeven a year ago. The loss before tax widened significantly to MNOK -22 from MNOK -4 in Q1 2024.

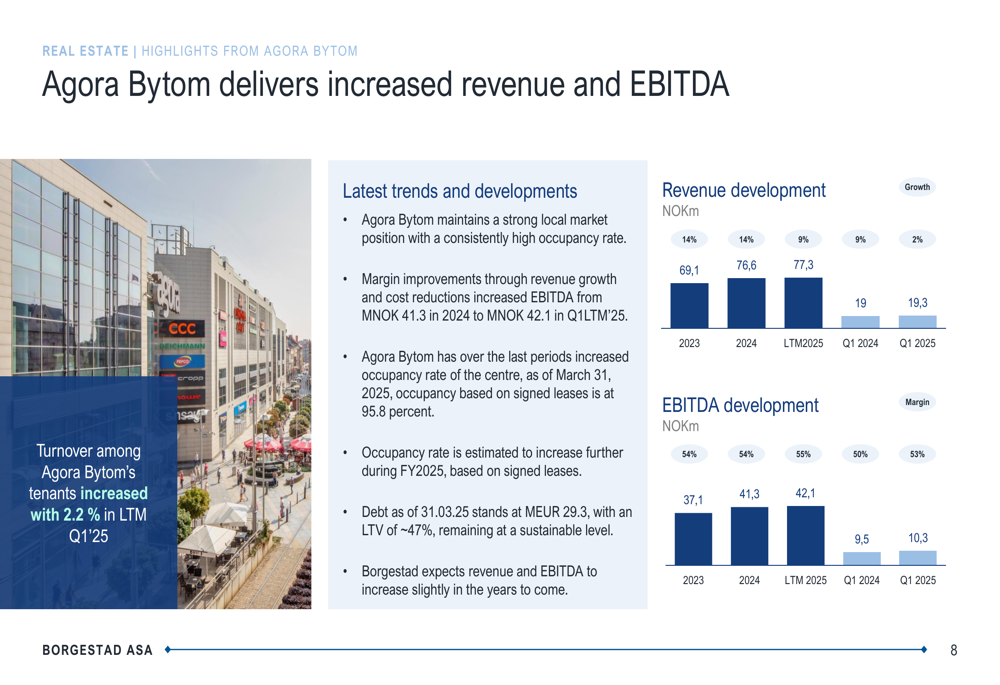

The real estate segment, centered around the Agora Bytom shopping center in Poland, continued to demonstrate resilience with an EBITDA of MNOK 10.3 in Q1 2025, up from MNOK 9.5 in Q1 2024. The shopping center maintained a high occupancy rate of 95.8% as of March 31, 2025, despite a slight 2.8% decrease in tenant turnover compared to the same period last year.

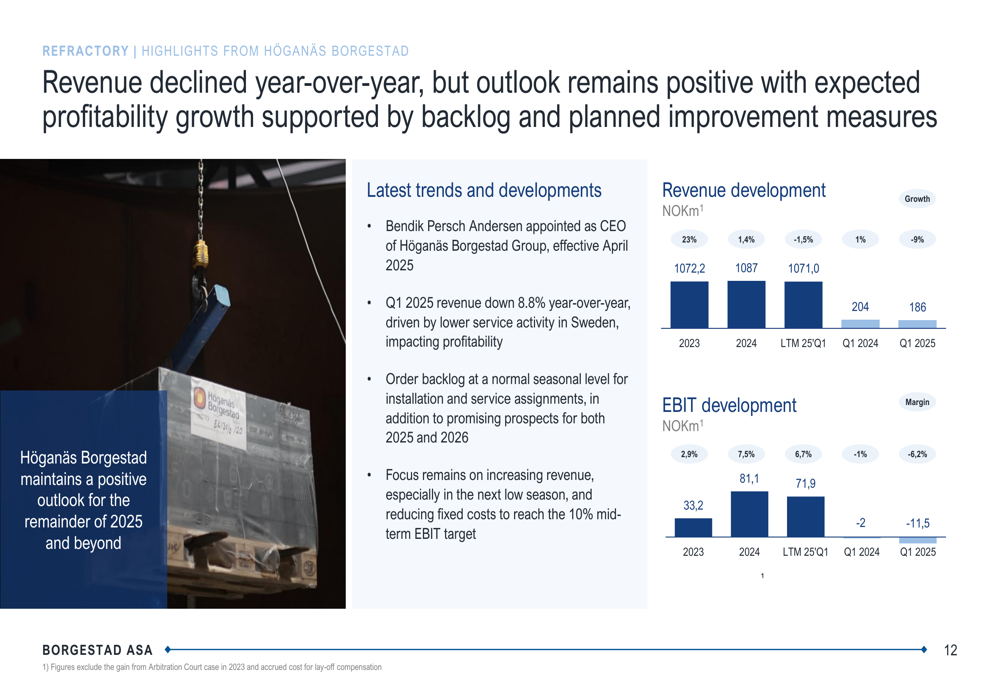

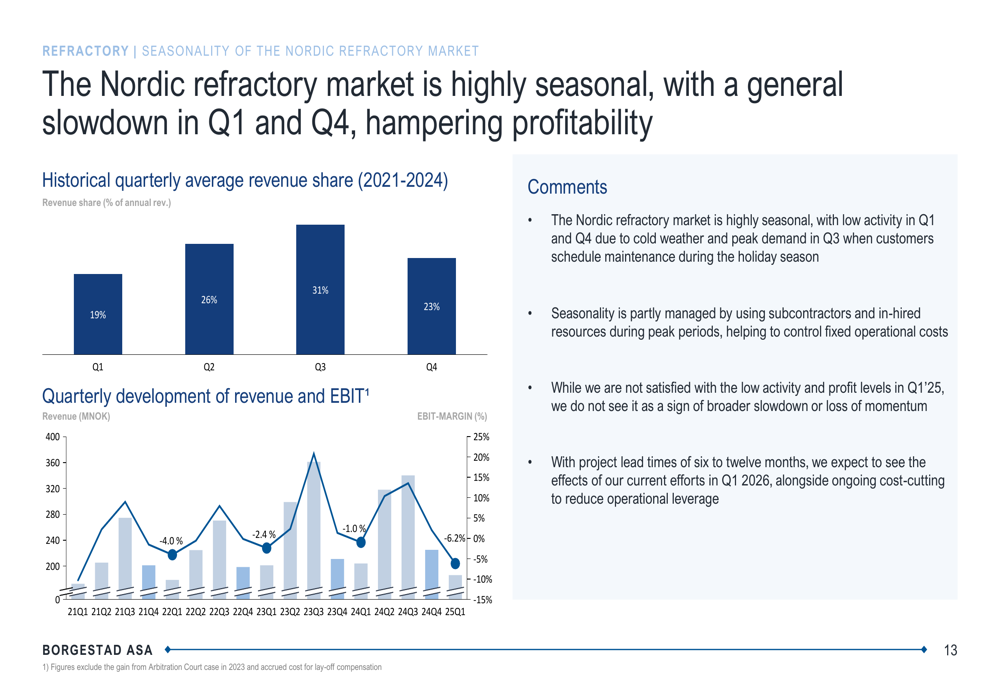

In contrast, the industrial segment Höganäs Borgestad delivered a notably weaker quarter with revenues of MNOK 186 and negative EBITDA of MNOK -8.5. This performance represents an 8.8% year-over-year revenue decline. However, management emphasized that the Nordic refractory market is highly seasonal, with the first quarter typically being the weakest period of the year.

The company’s presentation highlighted the seasonality of the Nordic refractory market, showing historical patterns that suggest stronger performance in later quarters. Management noted that while they are not satisfied with the low activity and profit levels in Q1 2025, they expect improvement with the current order backlog and prospects for the remainder of the year.

Detailed Financial Analysis

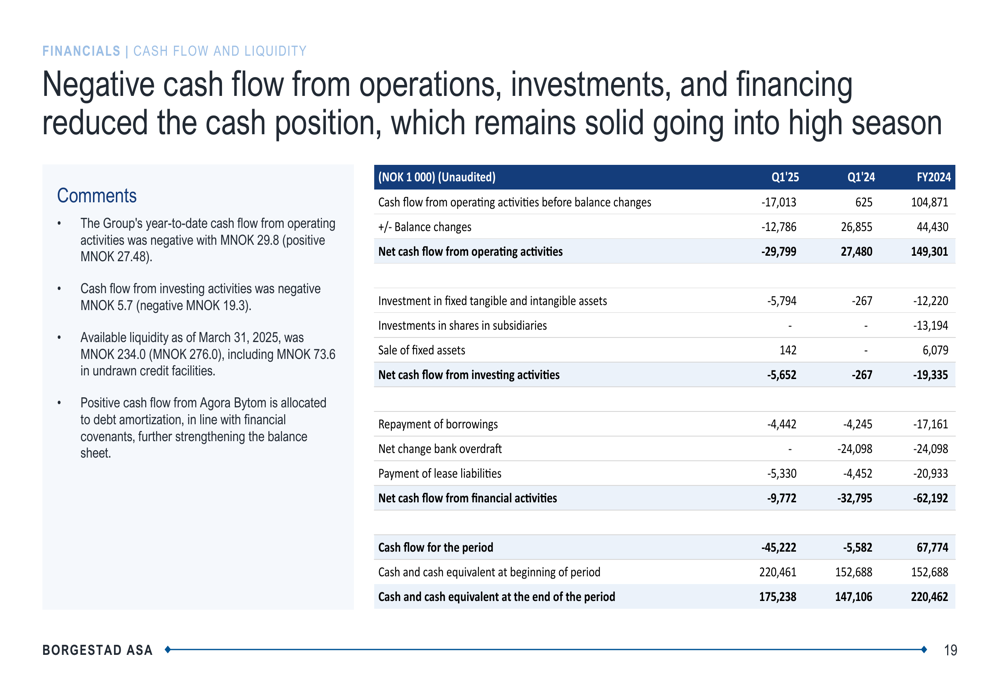

Borgestad’s balance sheet showed some positive developments despite the weak quarterly performance. The company maintained a solid cash position of MNOK 175 as of March 31, 2025, with available liquidity of MNOK 235. The net interest-bearing debt to EBITDA ratio improved to 1.9 from 2.3 a year ago, while the equity ratio remained stable at 54%.

The cash flow statement revealed negative cash flow from operations of MNOK -29.8 in Q1 2025, a significant deterioration from the positive MNOK 27.5 in Q1 2024. This decline was attributed to increased working capital ahead of the high season for the refractory business. The company also reported negative cash flows from investing activities (MNOK -5.7) and financing activities (MNOK -9.8), resulting in a total cash flow for the period of MNOK -45.2.

Agora Bytom’s financial performance showed steady improvement, with revenue increasing from MNOK 19.0 in Q1 2024 to MNOK 19.3 in Q1 2025. More importantly, EBITDA rose from MNOK 9.5 to MNOK 10.3 over the same period. On a last twelve months basis, revenue grew from MNOK 76.6 in 2024 to MNOK 77.3, while EBITDA improved from MNOK 41.3 to MNOK 42.1.

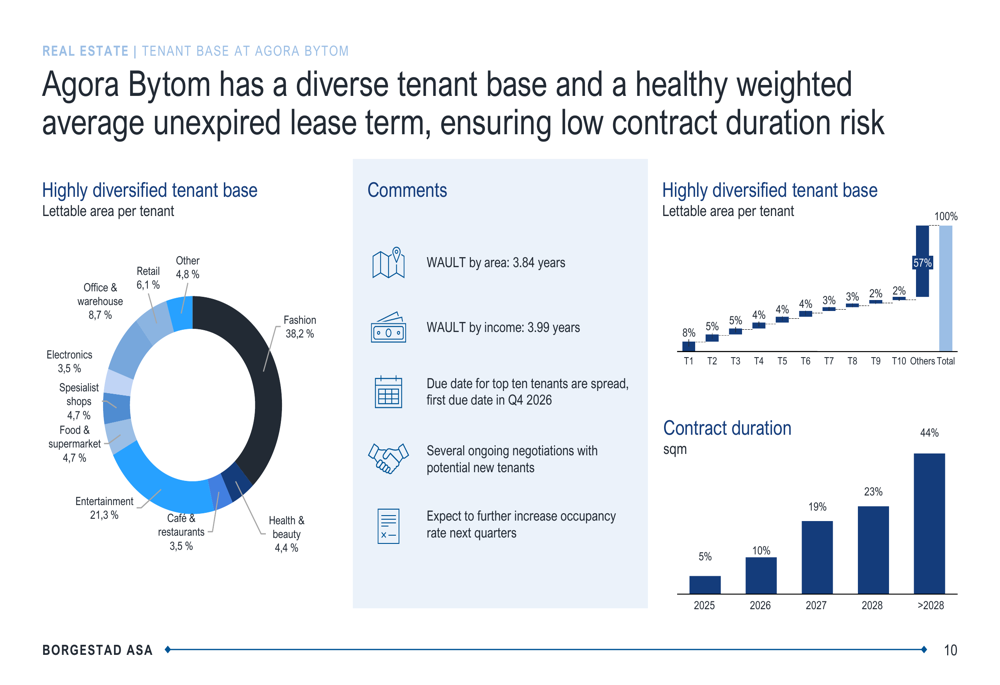

The Polish shopping center maintained a diversified tenant base, with fashion retailers occupying the largest share at 38.2% of lettable area, followed by entertainment at 21.3%. The weighted average unexpired lease term (WAULT) stood at 3.84 years by area and 3.99 years by income, providing stability for future revenue streams.

Strategic Initiatives & Outlook

Looking ahead, Borgestad outlined several strategic priorities for 2025. The company remains focused on operational improvements, capital efficiency, and cash flow gains. For Agora Bytom, management expects continued growth in revenue and EBITDA, while for Höganäs Borgestad, the mid-term EBIT target remains at 10%.

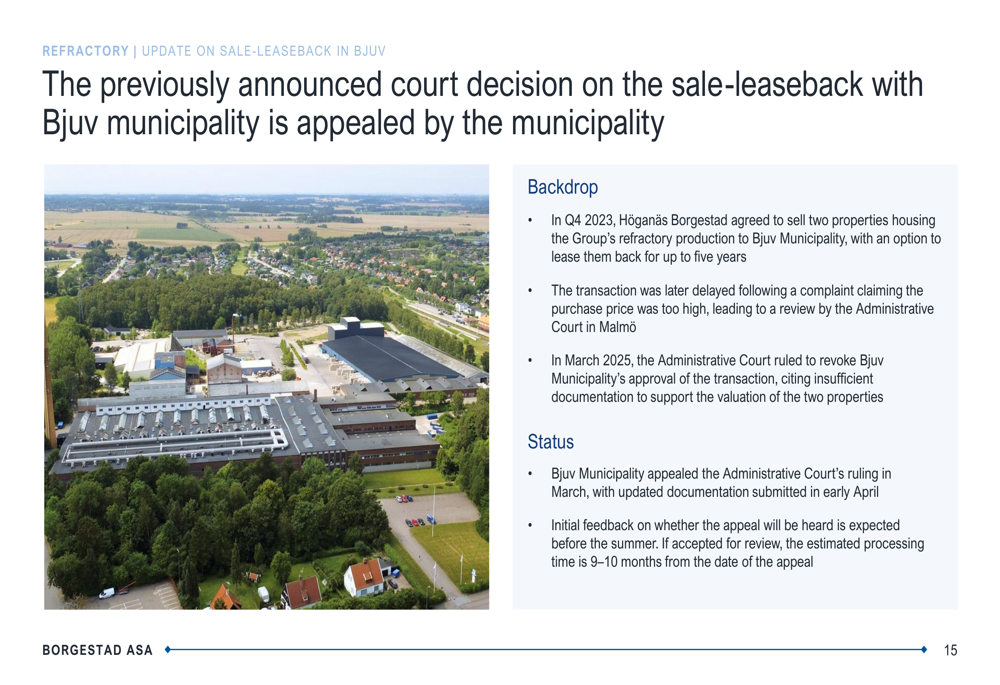

The presentation also addressed the previously announced sale-leaseback transaction with Bjuv municipality in Sweden. The deal, which was agreed upon in Q4 2023, has hit a roadblock as the municipality has appealed the Administrative Court’s ruling. This development adds uncertainty to the company’s strategic plans for its industrial segment.

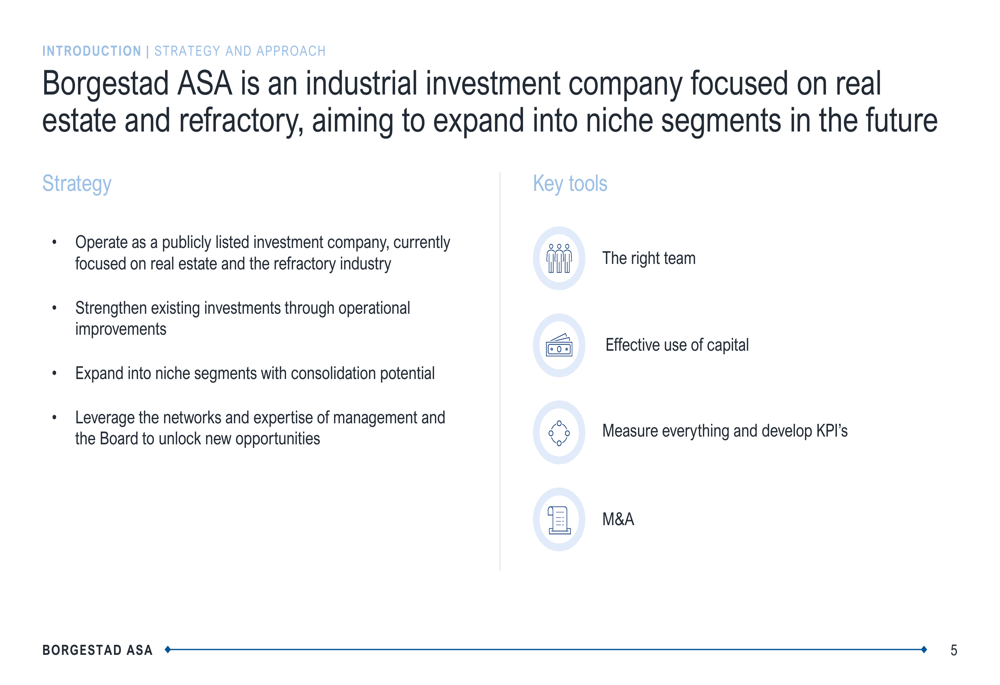

Borgestad continues to position itself as an industrial investment company with plans to expand into niche segments with consolidation potential. Management indicated they will evaluate strategic M&A opportunities both for the parent company and for Agora Bytom, suggesting potential portfolio changes in the future.

The company’s performance in Q1 2025 represents a step back from the progress made in 2024, when it reported a full-year profit before tax of 82.3 million USD, a significant improvement from a loss of 37.3 million USD in 2023. However, management remains confident in the company’s ability to deliver improved results in the coming quarters, particularly as the refractory business enters its traditionally stronger seasonal period.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.